The question Am I allowed to do employee pre-tax catch-up? pertains to the regulations and options available to employees who wish to make additional pre-tax contributions to their retirement accounts, such as a 401(k) or IRA, beyond the standard limits. This topic is important for individuals who are looking to maximize their retirement savings and take advantage of tax-deferred growth. The answer to this question depends on various factors, including the specific retirement plan, the employee's current contribution levels, and the IRS regulations. Generally, catch-up contributions are permitted for individuals who are close to retirement age, as defined by the IRS, and are subject to certain limits. It is crucial for employees to understand these rules to make informed decisions about their retirement savings strategy.

| Characteristics | Values |

|---|---|

| Type of Contribution | Pre-tax catch-up contribution |

| Contribution Limit | Varies by plan, typically a percentage of salary |

| Eligibility | Employees who have not contributed the maximum allowed amount |

| Tax Treatment | Contributions are made before taxes are withheld |

| Impact on Take-Home Pay | Reduces take-home pay due to increased contributions |

| Benefits | Increases retirement savings, potentially lowers taxable income |

| Withdrawal Rules | Generally subject to the same withdrawal rules as other pre-tax contributions |

| Employer Matching | May be eligible for employer matching contributions, depending on the plan |

| Contribution Deadline | Typically by the end of the calendar year or plan year |

| Documentation Required | May require documentation of income or contribution limits |

Explore related products

What You'll Learn

- Eligibility Criteria: Understand the conditions that qualify you for pre-tax catch-up contributions

- Contribution Limits: Learn about the maximum amounts you can contribute pre-tax to your retirement plan

- Deadline for Contributions: Discover the cut-off dates for making pre-tax catch-up contributions to your retirement account

- Impact on Taxes: Explore how pre-tax catch-up contributions affect your taxable income and potential tax savings

- Plan Restrictions: Check if your employer's retirement plan allows for pre-tax catch-up contributions and any specific rules

![]()

Eligibility Criteria: Understand the conditions that qualify you for pre-tax catch-up contributions

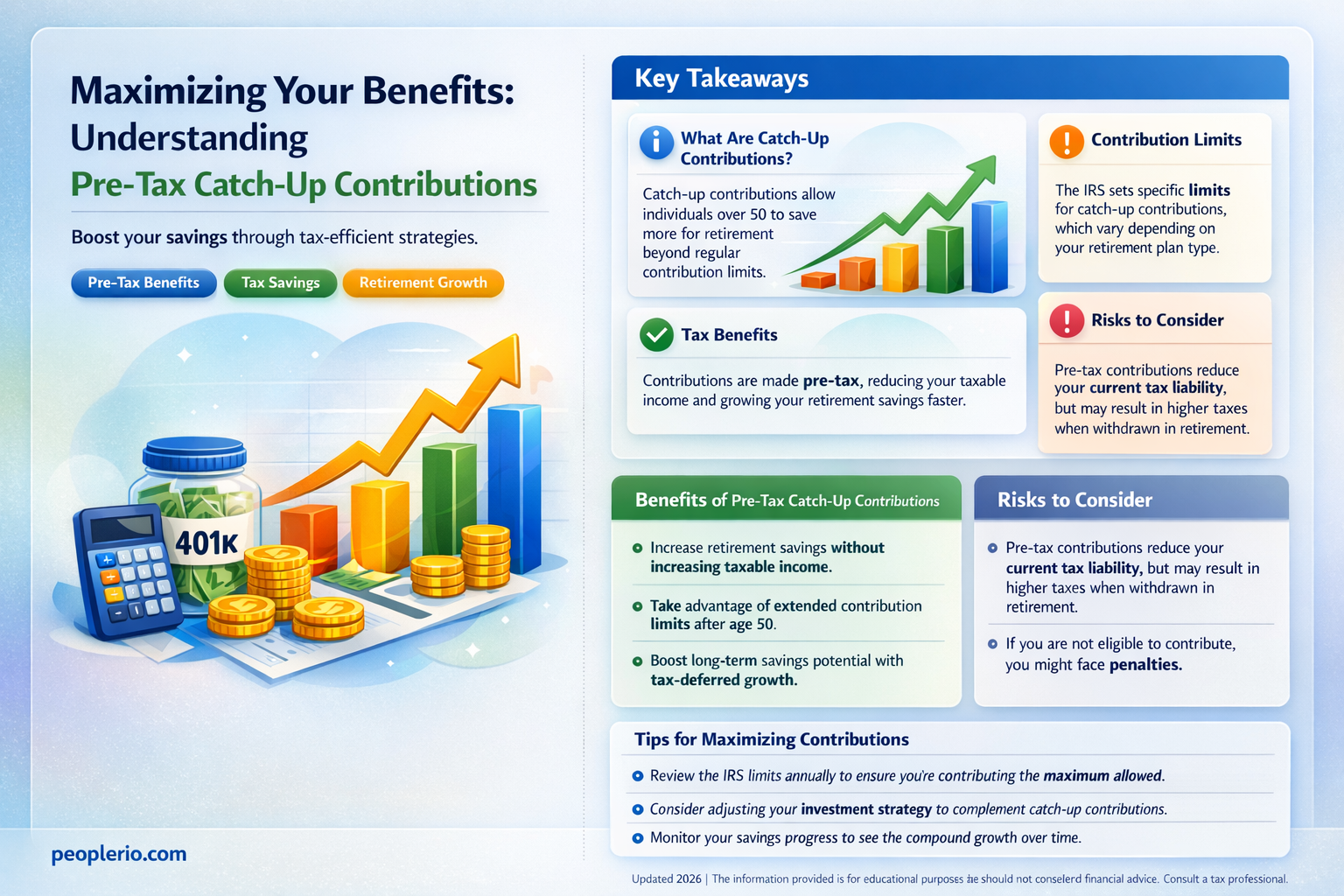

To qualify for pre-tax catch-up contributions, you must meet specific eligibility criteria set by the IRS. These criteria are designed to ensure that only individuals who are nearing retirement and have not yet maximized their retirement savings are able to take advantage of this opportunity. The catch-up contribution limit is in addition to the regular contribution limit and is intended to help those who may have started saving for retirement later in life or who have experienced a disruption in their savings plan.

One of the key eligibility criteria is age. You must be at least 50 years old in the year you make the catch-up contribution. This age requirement ensures that the catch-up contributions are targeted towards individuals who are approaching retirement and may need to accelerate their savings to achieve their retirement goals.

Another important criterion is the contribution limit. The catch-up contribution limit is separate from the regular contribution limit and is currently set at $6,500 for 2023. This limit is subject to change based on inflation and other economic factors. It's important to note that you can only make catch-up contributions to certain types of retirement accounts, such as 401(k) plans, 403(b) plans, and individual retirement accounts (IRAs).

Additionally, you must have earned income to make catch-up contributions. This means that you must have a job or be self-employed and receive compensation for your work. The amount of your catch-up contribution cannot exceed the amount of your earned income for the year.

It's also important to be aware of any employer-imposed restrictions on catch-up contributions. Some employers may not allow catch-up contributions or may have specific rules regarding how and when they can be made. It's essential to check with your employer's plan administrator to understand any limitations or requirements that may apply.

In summary, to qualify for pre-tax catch-up contributions, you must be at least 50 years old, have earned income, and contribute to a qualifying retirement account. The catch-up contribution limit is separate from the regular contribution limit and is subject to change. It's important to be aware of any employer-imposed restrictions and to consult with a financial advisor to determine the best strategy for maximizing your retirement savings.

Understanding Tax Rates for 1099 Employees: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Contribution Limits: Learn about the maximum amounts you can contribute pre-tax to your retirement plan

The IRS sets annual contribution limits for retirement plans, which dictate the maximum amount you can contribute pre-tax. For 2023, the limit for 401(k) and 403(b) plans is $22,500, with an additional $7,500 catch-up contribution allowed for those aged 50 and older. These limits are subject to change, so it's essential to stay informed about the current year's limits to maximize your retirement savings.

Exceeding these contribution limits can result in penalties, including taxes on the excess contributions and potential withdrawal restrictions. Therefore, it's crucial to monitor your contributions throughout the year to avoid surpassing the limit. If you're unsure about your contribution status, consult with your plan administrator or a financial advisor.

One strategy to optimize your retirement savings is to contribute the maximum allowed amount each year. If you're unable to do so, consider increasing your contributions gradually over time as your income and financial situation permit. Additionally, take advantage of any employer matching contributions, as this can significantly boost your retirement savings.

It's also important to note that contribution limits may vary depending on the type of retirement plan you have. For example, IRAs have different contribution limits and rules compared to employer-sponsored plans like 401(k)s. Familiarize yourself with the specific limits and guidelines for your plan to make the most of your retirement savings opportunities.

In summary, understanding and adhering to contribution limits is a key aspect of retirement planning. By staying informed about the current limits and strategies for maximizing your contributions, you can set yourself on a path to a more secure financial future.

Maximizing Your Retirement Savings: The Tax Benefits of Employer 401(k) Matches

You may want to see also

Explore related products

![]()

Deadline for Contributions: Discover the cut-off dates for making pre-tax catch-up contributions to your retirement account

The deadline for making pre-tax catch-up contributions to your retirement account is a critical date to remember. For those eligible, this deadline offers an opportunity to boost their retirement savings with tax-advantaged contributions. Typically, the cut-off date for such contributions is December 31st of the current year, but it's essential to check with your plan administrator or financial advisor for any specific deadlines or requirements that may apply to your situation. Missing this deadline could mean losing out on valuable tax benefits and the chance to maximize your retirement fund.

Understanding the rules surrounding catch-up contributions is crucial. These contributions are designed for individuals who are behind in their retirement savings and are nearing retirement age. The IRS allows those aged 50 and older to contribute additional amounts to their retirement accounts beyond the standard contribution limits. This can be a significant advantage for those looking to play catch-up with their retirement savings. However, it's important to note that these contributions are subject to annual limits, and exceeding these limits can result in penalties.

When planning for catch-up contributions, it's also important to consider the impact of these contributions on your overall financial situation. While pre-tax contributions can reduce your taxable income for the year, they will be taxed when you withdraw the funds in retirement. Therefore, it's essential to balance the immediate tax benefits with the long-term tax implications. Consulting with a financial advisor can help you make informed decisions about how to best utilize catch-up contributions within your retirement planning strategy.

In addition to the tax considerations, there are other factors to keep in mind when making catch-up contributions. For example, if you are covered by a retirement plan at work, your employer may have specific rules or restrictions regarding catch-up contributions. It's also important to consider the investment options available within your retirement account and how they align with your risk tolerance and retirement goals. By carefully evaluating these factors, you can make the most of the catch-up contribution opportunity and ensure that you are on track for a secure retirement.

Understanding Household Employees: Tax Implications and Responsibilities Explained

You may want to see also

Explore related products

![]()

Impact on Taxes: Explore how pre-tax catch-up contributions affect your taxable income and potential tax savings

Pre-tax catch-up contributions can significantly impact your taxable income and potential tax savings. By contributing to your retirement plan on a pre-tax basis, you reduce your taxable income for the year, which can lead to a lower tax bill. This is because the money you contribute is deducted from your gross income before taxes are calculated. As a result, you pay taxes on a smaller amount of income, which can translate into substantial savings, especially if you are in a higher tax bracket.

For example, if you contribute $5,000 to your 401(k) plan on a pre-tax basis and you are in the 25% tax bracket, you would save $1,250 in taxes for that year. This is because the $5,000 contribution reduces your taxable income by that amount, and 25% of $5,000 is $1,250. Over time, these tax savings can add up, allowing you to accumulate more wealth in your retirement plan.

It's important to note that while pre-tax contributions can reduce your taxable income, they do not eliminate taxes altogether. You will still need to pay taxes on the contributions when you withdraw the money from your retirement plan in retirement. However, by that time, you may be in a lower tax bracket, which can further enhance your tax savings.

Additionally, pre-tax catch-up contributions can be particularly beneficial if you are nearing retirement and have not yet maximized your retirement savings. The catch-up contribution rules allow individuals who are 50 or older to contribute more to their retirement plans than the standard contribution limits. This can help you boost your retirement savings and take advantage of the tax benefits associated with pre-tax contributions.

In conclusion, pre-tax catch-up contributions can have a significant impact on your taxable income and potential tax savings. By contributing to your retirement plan on a pre-tax basis, you can reduce your tax bill for the year and accumulate more wealth in your retirement plan over time. This can be especially beneficial if you are in a higher tax bracket or are nearing retirement and looking to maximize your savings.

Maximize Your Savings: Understanding Pre-Tax Employee Stock Purchase Plans

You may want to see also

![]()

Plan Restrictions: Check if your employer's retirement plan allows for pre-tax catch-up contributions and any specific rules

To determine if your employer's retirement plan permits pre-tax catch-up contributions, you must first review the plan's official documents. These documents will outline the specific rules and regulations governing catch-up contributions. Catch-up contributions are additional funds that employees aged 50 and older can contribute to their retirement accounts on a pre-tax basis, above the standard contribution limits.

The first step is to locate the plan's Summary Plan Description (SPD), which is a document that employers are required to provide to all participants. The SPD will detail the plan's features, including any provisions for catch-up contributions. Look for sections that specifically mention "catch-up contributions" or "pre-tax contributions for participants aged 50 and older."

Next, review the plan's administrative rules and procedures. These rules may outline any specific requirements or limitations on making catch-up contributions. For example, some plans may require participants to have reached a certain age or to have contributed a minimum amount to the plan before they are eligible to make catch-up contributions.

Additionally, check if the plan has any specific deadlines or enrollment requirements for making catch-up contributions. Some plans may require participants to enroll in the catch-up contribution program by a certain date or to make their contributions within a specific timeframe.

It is also important to note that the rules governing catch-up contributions can vary significantly from plan to plan. Some plans may allow for unlimited catch-up contributions, while others may impose strict limits. Furthermore, the tax implications of catch-up contributions can be complex, and it is advisable to consult with a tax professional or financial advisor to ensure that you are making the most informed decisions.

In conclusion, to determine if your employer's retirement plan allows for pre-tax catch-up contributions, you must carefully review the plan's official documents, including the Summary Plan Description and administrative rules. By doing so, you can gain a clear understanding of the plan's specific provisions and make informed decisions about your retirement savings.

Understanding the I-9 Tax Form: A Comprehensive Guide

You may want to see also

Frequently asked questions

An employee pre-tax catch-up contribution is a type of retirement savings contribution that allows employees to save more money for retirement by contributing a portion of their income before taxes are taken out.

Eligibility for employee pre-tax catch-up contributions typically depends on the specific retirement plan offered by an employer. Generally, employees who are at least 50 years old and have reached the maximum contribution limit for their plan may be eligible to make catch-up contributions.

The amount an employee can contribute as a pre-tax catch-up varies depending on the plan and the year. For example, in 2023, the IRS allows an additional catch-up contribution of up to $7,500 for those aged 50 and older in certain retirement plans.

Yes, employee pre-tax catch-up contributions are generally tax-deductible. This means that the amount contributed is subtracted from the employee's taxable income, reducing their overall tax liability.

Employee pre-tax catch-up contributions are not subject to Social Security taxes. This means that the amount contributed does not count towards the employee's Social Security taxable income, potentially reducing the amount of Social Security taxes owed.