When it comes to retirement savings, many employees take advantage of 401(k) plans offered by their employers. A common question that arises is whether all contributions to a 401(k) plan are 100% tax-deductible. The short answer is that, generally, contributions made by employees to their 401(k) plans are tax-deductible up to certain limits. However, there are some nuances and exceptions to this rule. For instance, if an employee's income exceeds a certain threshold, their contribution limit may be reduced. Additionally, some plans may have Roth 401(k) options, which are funded with after-tax dollars and offer different tax benefits. It's important for employees to understand the specifics of their plan and consult with a financial advisor to maximize their retirement savings while minimizing their tax liability.

| Characteristics | Values |

|---|---|

| Tax Deductibility | Not 100% deductible |

| Contribution Limits | Subject to annual limits |

| Employer Matching | May be matched by employer |

| Investment Options | Limited to approved funds |

| Withdrawal Rules | Subject to penalties for early withdrawal |

| Loan Provisions | Loans may be available |

| Vesting Schedule | Immediate vesting |

| Required Minimum Distributions | Not required until age 72 |

| Beneficiary Designation | Allowed |

| Portability | Can be rolled over to other plans |

Explore related products

What You'll Learn

- Contribution Limits: Maximum annual contribution amounts and how they impact tax deductions

- Traditional vs. Roth 401(k): Differences in tax treatment between traditional and Roth 401(k) contributions

- Tax Deduction Phase-Out: Income thresholds that affect the deductibility of 401(k) contributions

- Catch-Up Contributions: Additional contributions allowed for employees aged 50 and older and their tax implications

- Employer Matching: How employer contributions to a 401(k) plan are treated for tax purposes

![]()

Contribution Limits: Maximum annual contribution amounts and how they impact tax deductions

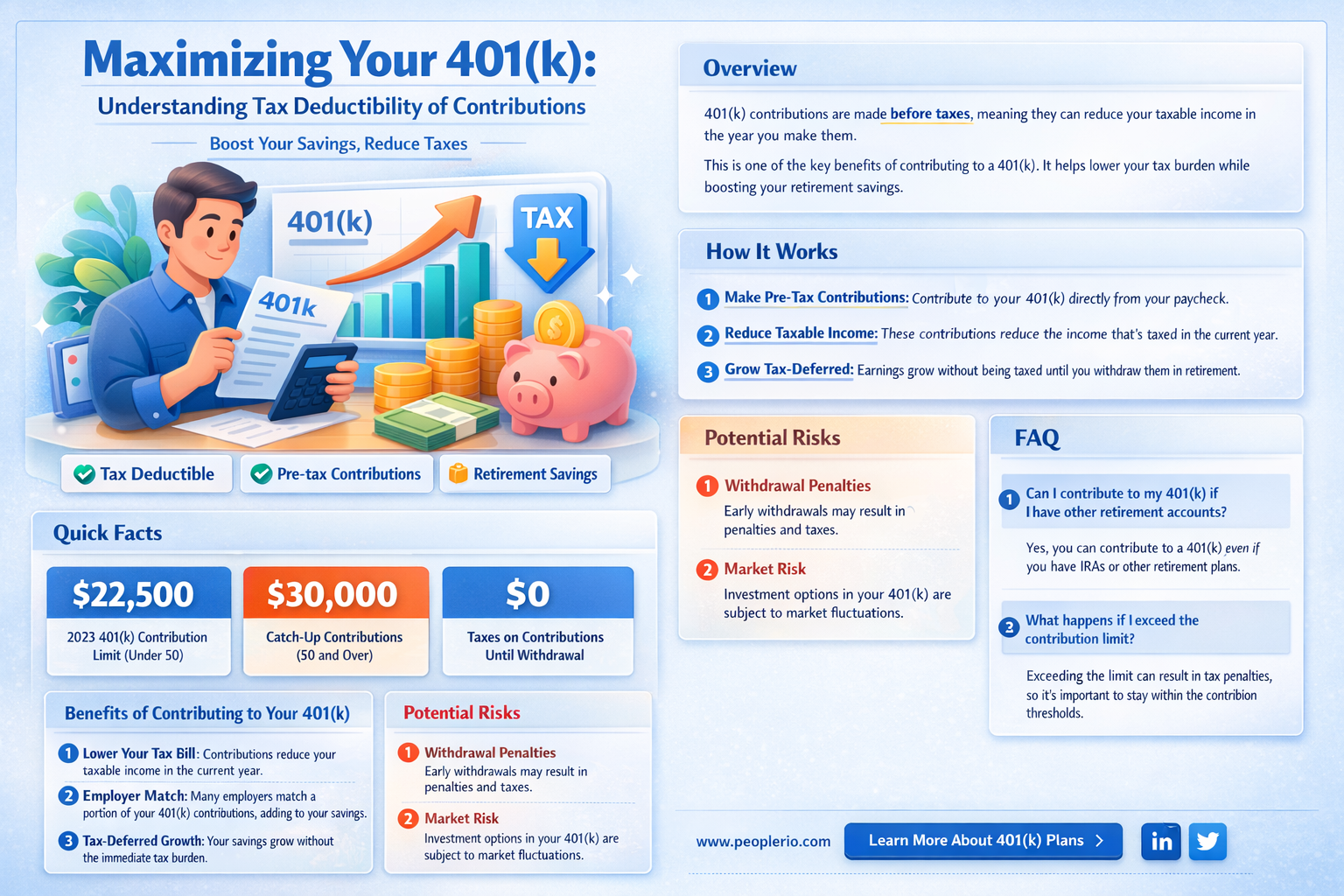

The IRS sets annual contribution limits for 401(k) plans, which can significantly impact the tax deductions available to contributors. For 2023, the maximum annual contribution limit for employees is $22,500, with an additional $7,500 catch-up contribution allowed for those aged 50 and older. These limits are subject to change based on inflation and other economic factors.

Exceeding these contribution limits can result in tax penalties and may require the excess contributions to be withdrawn from the plan. It's essential for employees to monitor their contributions throughout the year to avoid surpassing these limits. Employers may also impose their own contribution limits or matching contribution limits, which can further affect the tax deductions available.

The tax deductibility of 401(k) contributions is generally limited to the amount contributed, up to the annual limit. Contributions made with pre-tax dollars are deducted from the contributor's taxable income, reducing their overall tax liability. However, catch-up contributions made by those aged 50 and older may not be fully tax-deductible if they exceed the standard contribution limit.

To maximize tax deductions, employees should consider contributing the maximum allowable amount to their 401(k) plan each year. If an employer offers a matching contribution, employees should contribute at least enough to receive the full match, as this is essentially free money that can further reduce taxable income.

It's also important to note that the tax treatment of 401(k) contributions may vary depending on the type of plan and the contributor's individual circumstances. For example, contributions to a Roth 401(k) plan are made with after-tax dollars and do not provide an immediate tax deduction, but qualified withdrawals in retirement are tax-free.

In conclusion, understanding the contribution limits and tax implications of 401(k) plans is crucial for maximizing retirement savings and minimizing tax liability. Employees should carefully monitor their contributions, take advantage of employer matching contributions, and consider the long-term tax benefits of different types of 401(k) plans when making their retirement planning decisions.

Mastering Employee Tax Filing: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![]()

Traditional vs. Roth 401(k): Differences in tax treatment between traditional and Roth 401(k) contributions

Traditional 401(k) contributions are made with pre-tax dollars, which means they are deducted from your gross income before taxes are calculated. This can lower your taxable income for the year, resulting in a smaller tax bill. However, when you withdraw the funds in retirement, they are taxed as ordinary income.

Roth 401(k) contributions, on the other hand, are made with after-tax dollars. This means you pay taxes on the money before it is contributed to your account. The upside is that the funds grow tax-free, and qualified withdrawals in retirement are tax-free as well.

One key difference between the two is the timing of taxation. With a traditional 401(k), you get a tax break upfront, but pay taxes on withdrawals later. With a Roth 401(k), you pay taxes upfront, but get tax-free growth and withdrawals later.

Another difference is the income limits for contributions. Traditional 401(k) contributions are not subject to income limits, while Roth 401(k) contributions are. For 2023, the income limit for Roth 401(k) contributions is $138,000 for single filers and $218,000 for married couples filing jointly.

When deciding between a traditional and Roth 401(k), it's important to consider your current tax bracket, your expected tax bracket in retirement, and your overall financial goals. If you expect to be in a higher tax bracket in retirement, a Roth 401(k) may be a better choice. If you expect to be in a lower tax bracket in retirement, a traditional 401(k) may be more beneficial.

Boosting Business Stability: Understanding the Employee Retention Tax Credit

You may want to see also

Explore related products

![]()

Tax Deduction Phase-Out: Income thresholds that affect the deductibility of 401(k) contributions

While many employees are aware that their 401(k) contributions can be tax-deductible, fewer understand the nuances of the tax deduction phase-out. This phase-out begins at specific income thresholds, which can significantly impact the deductibility of contributions. For the 2023 tax year, the phase-out starts at $68,000 for single filers and $109,000 for joint filers. As income increases beyond these thresholds, the deduction gradually reduces until it is completely phased out.

The phase-out works on a sliding scale. For single filers, the deduction is reduced by $0.50 for every $1 of income above $68,000. For joint filers, the reduction is $0.50 for every $1 of income above $109,000. This means that as income rises, the tax benefit of contributing to a 401(k) diminishes. For example, a single filer earning $78,000 would see their deduction reduced by $5,000 (10,000 * $0.50), while a joint filer earning $129,000 would see a reduction of $10,000 (20,000 * $0.50).

It's important to note that the phase-out thresholds are adjusted annually for inflation. This means that employees need to stay informed about the current thresholds to maximize their tax benefits. Additionally, the phase-out only affects the federal tax deduction for 401(k) contributions. State tax deductions may have different rules and thresholds.

Employees who are close to the phase-out thresholds may want to consider strategies to maximize their deductions. This could include contributing more to their 401(k) before reaching the threshold or exploring other tax-advantaged retirement savings options, such as a Roth IRA. Understanding the tax deduction phase-out can help employees make informed decisions about their retirement savings and tax planning strategies.

Unlocking Tax Benefits: Employee Pension Contributions Explained

You may want to see also

Explore related products

![]()

Catch-Up Contributions: Additional contributions allowed for employees aged 50 and older and their tax implications

Employees aged 50 and older are allowed to make additional contributions to their 401(k) plans, known as catch-up contributions. These contributions are designed to help older workers save more for retirement, as they may have less time to accumulate savings compared to younger employees. Catch-up contributions are subject to the same tax implications as regular 401(k) contributions, meaning they are generally tax-deductible.

The amount of catch-up contributions allowed is set by the IRS and is adjusted annually for inflation. In 2023, the catch-up contribution limit is $7,500 for employees aged 50 and older. This is in addition to the regular 401(k) contribution limit of $22,500. By taking advantage of catch-up contributions, older workers can significantly increase their retirement savings.

It's important to note that catch-up contributions are only available to employees who are at least 50 years old. This means that if an employee turns 50 during the year, they may be eligible to make catch-up contributions for that year. Additionally, catch-up contributions are only allowed for 401(k) plans, and not for other types of retirement plans such as IRAs or Roth IRAs.

Employers are not required to offer catch-up contributions, but many do as a way to encourage older employees to save more for retirement. If an employer does offer catch-up contributions, they must allow all eligible employees to participate. Employers may also choose to match catch-up contributions, which can further boost an employee's retirement savings.

In conclusion, catch-up contributions are a valuable tool for older workers looking to increase their retirement savings. By understanding the tax implications and eligibility requirements, employees can make informed decisions about whether to take advantage of this opportunity.

Smart Tax Strategies: How a W2 Employee Reduced His Taxes

You may want to see also

Explore related products

![]()

Employer Matching: How employer contributions to a 401(k) plan are treated for tax purposes

Employer contributions to a 401(k) plan are generally tax-deductible for the employer. This means that when an employer matches an employee's contribution to their 401(k) plan, the employer can deduct the amount of the match from their taxable income. This deduction can help reduce the employer's tax liability, making it a beneficial incentive for employers to offer matching contributions.

However, there are certain limits and conditions that apply to employer matching contributions. For example, the total contribution limit for an employee, including both their own contributions and employer matching, is $19,500 in 2022 ($26,000 for those age 50 and older). Employers must also ensure that their matching contributions do not discriminate in favor of highly compensated employees.

From a tax perspective, employer matching contributions are considered a form of compensation to the employee. As such, they are subject to payroll taxes, including Social Security and Medicare taxes. However, the employer's matching contributions are not taxable to the employee until they are withdrawn from the plan.

It's important for employers to understand the tax implications of offering matching contributions to their employees' 401(k) plans. By doing so, they can make informed decisions about how to structure their retirement benefits and maximize the tax advantages available to them.

Tax Savings Guide for 1099 Employees: Smart Strategies for Financial Peace

You may want to see also

Frequently asked questions

Generally, yes. Employee contributions to a traditional 401k plan are made pre-tax, which means they are deducted from your gross income before taxes are calculated. This reduces your taxable income for the year.

For 2023, the maximum employee contribution to a 401k plan is $22,500. If you are age 50 or older, you can make an additional catch-up contribution of up to $7,500, bringing the total to $30,000.

No, you cannot contribute more than the maximum allowed amount set by the IRS for each year. Exceeding this limit can result in penalties and taxes on the excess contributions.

Yes, employer matching contributions to your 401k are also tax-deductible for the employer. They are considered a business expense and can reduce the employer's taxable income.