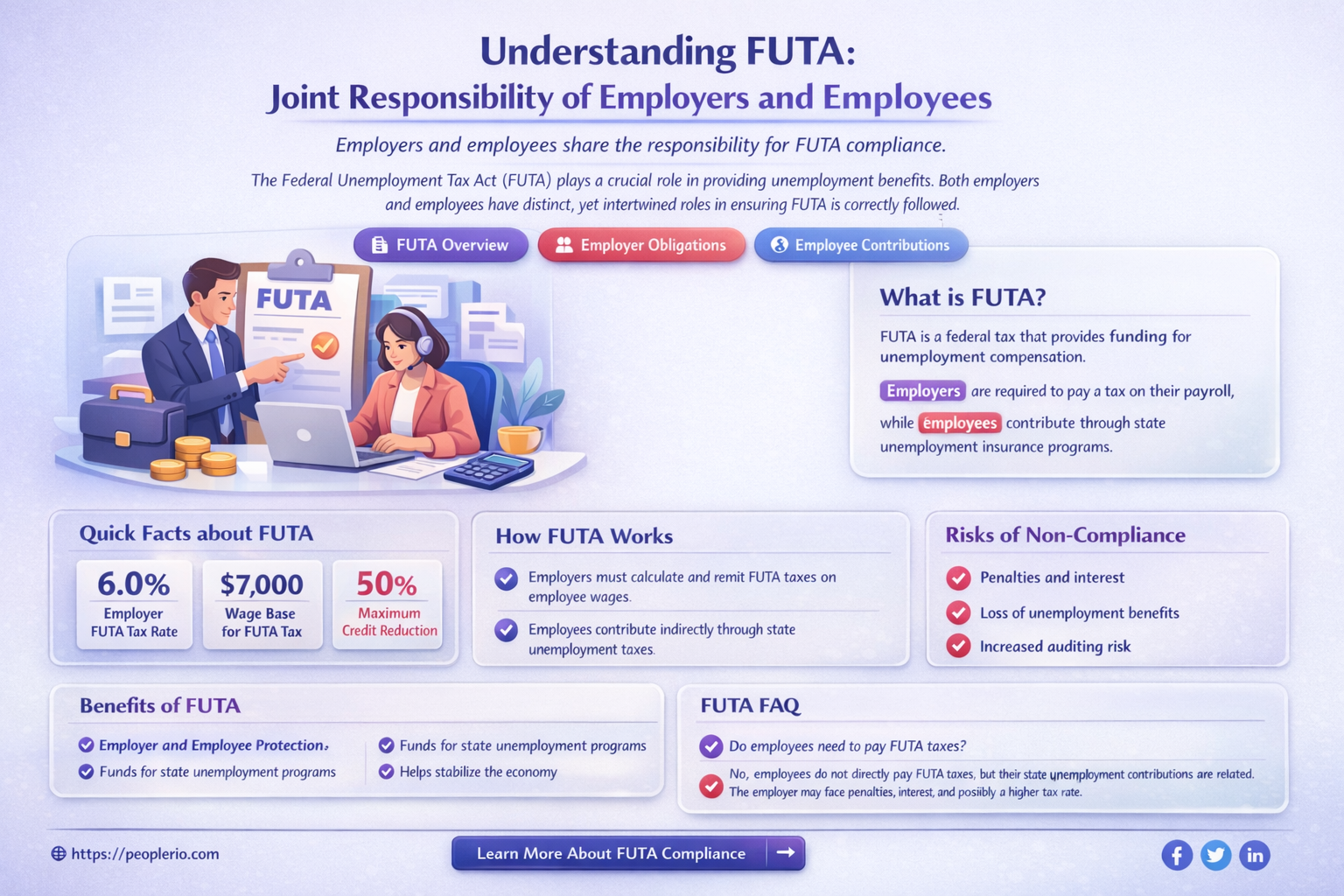

The Federal Unemployment Tax Act (FUTA) is a crucial component of the United States' unemployment insurance system. It mandates that both employees and employers contribute to a federal fund that provides unemployment benefits to eligible workers. While FUTA is primarily an employer-funded program, employees also play a role in supporting the system. This shared responsibility ensures that the fund remains solvent and capable of providing financial assistance to those who find themselves without employment through no fault of their own. Understanding the specifics of FUTA contributions is essential for both employers and employees to comply with federal regulations and support the broader economic safety net.

| Characteristics | Values |

|---|---|

| Employee Requirement | Yes |

| Employer Requirement | Yes |

| Type of Tax | Federal Unemployment Tax Act (FUTA) |

| Purpose | Funds state unemployment insurance programs |

| Employee Contribution | 0.8% of gross wages |

| Employer Contribution | 0.8% of gross wages |

| Maximum Taxable Wages (per employee) | $7,000 |

| Filing Frequency | Quarterly |

| Payment Method | Electronic Federal Tax Payment System (EFTPS) or check |

| Reporting Requirements | Form 940 (annual) and Form 941 (quarterly) |

Explore related products

What You'll Learn

- FUTA Tax Basics: Understanding the Federal Unemployment Tax Act and its implications for both employees and employers

- Employer Responsibilities: Detailed breakdown of employer duties regarding FUTA tax, including payment and reporting obligations

- Employee Contributions: Explanation of how employees contribute to FUTA and the impact on their paychecks

- Tax Calculation: Step-by-step guide on calculating FUTA tax for both employers and employees

- Penalties and Compliance: Overview of potential penalties for non-compliance and tips for ensuring proper FUTA tax handling

![]()

FUTA Tax Basics: Understanding the Federal Unemployment Tax Act and its implications for both employees and employers

The Federal Unemployment Tax Act (FUTA) is a crucial component of the United States' unemployment insurance system. It mandates that both employers and employees contribute to a federal fund that provides unemployment benefits to eligible workers. This tax is separate from state unemployment taxes and is used to fund federal unemployment programs, including those for military veterans and individuals who have exhausted their state benefits.

Employers are responsible for paying the majority of the FUTA tax. As of 2023, the employer tax rate is 6% on the first $7,000 of each employee's wages. However, employers can claim a credit of up to 5.4% for state unemployment taxes they pay, effectively reducing the federal tax rate to 0.6% for those who pay the maximum state tax. Employers must deposit their FUTA taxes quarterly with the IRS and file an annual Form 940 to report their total FUTA tax liability.

Employees also contribute to the FUTA tax, but at a lower rate than employers. The employee tax rate is 0.6% on their wages, up to the same $7,000 limit. This tax is typically withheld from employees' paychecks and remitted to the IRS by the employer. Unlike employers, employees do not need to file a separate FUTA tax form, as their contributions are reported on their W-2 forms at the end of the year.

Understanding the FUTA tax is essential for both employers and employees. Employers need to ensure they are correctly calculating and remitting their FUTA taxes to avoid penalties and interest. Employees should be aware of their own contributions and how they impact their take-home pay. Additionally, both parties should understand the broader implications of the FUTA tax, such as its role in supporting the unemployment insurance system and its potential impact on economic stability during times of high unemployment.

In conclusion, the FUTA tax is a shared responsibility between employers and employees, with each party contributing to a vital federal fund that supports unemployed workers. By understanding the basics of the FUTA tax, both employers and employees can fulfill their obligations and contribute to the overall health of the unemployment insurance system.

Decoding 1099 Taxes: A Comprehensive Guide for Freelancers

You may want to see also

Explore related products

![]()

Employer Responsibilities: Detailed breakdown of employer duties regarding FUTA tax, including payment and reporting obligations

Employers have specific responsibilities when it comes to FUTA tax, which is a federal unemployment tax. One of the primary duties is to pay the tax, which is calculated as a percentage of employee wages. The current FUTA tax rate is 6%, but employers may be eligible for a credit reduction, which can lower the effective rate to as low as 0.6%. To calculate the tax, employers must determine which wages are subject to FUTA tax and then apply the appropriate rate.

In addition to paying the tax, employers are also required to report their FUTA tax liability on a quarterly basis. This is done using Form 940, which is filed with the IRS. Employers must also provide information about their employees, including their names, social security numbers, and wages earned. This information is used by the IRS to determine the amount of FUTA tax owed and to issue refunds or credits as applicable.

Employers are also responsible for depositing their FUTA tax payments with the IRS. This can be done electronically using the Electronic Federal Tax Payment System (EFTPS) or by mailing a check or money order to the IRS. Employers must make sure to deposit their payments on time to avoid penalties and interest.

Another important responsibility of employers is to keep accurate records of their FUTA tax payments and reporting. This includes maintaining copies of Forms 940 and any other relevant documents, as well as keeping track of employee wages and tax credits. Employers may be subject to audits by the IRS, so it is important to have accurate and complete records available.

Finally, employers should be aware of any changes to FUTA tax laws and regulations. This includes changes to tax rates, credit reductions, and reporting requirements. Employers can stay informed about these changes by subscribing to IRS newsletters or consulting with a tax professional. By staying up-to-date on FUTA tax requirements, employers can ensure that they are meeting their obligations and avoiding potential penalties.

Employer Obligations: Paying Employees for Jury Duty Explained

You may want to see also

Explore related products

![]()

Employee Contributions: Explanation of how employees contribute to FUTA and the impact on their paychecks

Employees contribute to the Federal Unemployment Tax Act (FUTA) through payroll deductions. This means that a portion of each paycheck is withheld and sent to the federal government to fund unemployment insurance programs. The FUTA tax rate is 6.2% of the first $7,000 of an employee's annual wages. However, employers are responsible for paying the full FUTA tax amount, and employees do not directly pay any portion of this tax.

The impact of FUTA contributions on an employee's paycheck is indirect. While employees do not pay FUTA taxes directly, their employers may adjust their wages or benefits to account for the cost of FUTA taxes. This could potentially result in lower take-home pay or reduced benefits for employees. However, it is important to note that FUTA taxes are a necessary part of the unemployment insurance system, which provides financial support to workers who lose their jobs through no fault of their own.

In terms of practical implications, employees should be aware that their FUTA contributions are not optional and are a mandatory part of their employment. Employers are required to withhold FUTA taxes from employee wages and remit them to the federal government on a quarterly basis. Failure to do so can result in penalties and fines for employers.

Overall, while employees do not directly pay FUTA taxes, their contributions are an essential part of the unemployment insurance system. The impact on their paychecks may be indirect, but it is a necessary cost of employment that helps to ensure financial stability for workers during times of unemployment.

Understanding Holiday Pay Entitlements for Part-Time Employees

You may want to see also

Explore related products

![]()

Tax Calculation: Step-by-step guide on calculating FUTA tax for both employers and employees

To calculate FUTA tax, employers must first determine their taxable wage base. This includes all wages paid to employees, up to a certain limit, which is subject to change annually. For example, in 2023, the taxable wage base limit is $7,000 per employee. Employers then multiply the taxable wage base by the current FUTA tax rate, which is 6%. However, employers may be eligible for a credit reduction of up to 5.4% if they pay state unemployment taxes on time.

Employees, on the other hand, do not have to calculate their own FUTA tax. Their contribution is automatically deducted from their wages by their employer. The employee's FUTA tax rate is 0.6%, which is taken out of their gross wages, up to the same taxable wage base limit. It's important to note that employees do not have to file a separate FUTA tax return, as their employer is responsible for reporting and paying the tax on their behalf.

One common mistake employers make when calculating FUTA tax is failing to account for the taxable wage base limit. This can result in overpaying the tax. To avoid this, employers should ensure they are only taxing wages up to the current limit. Additionally, employers should be aware of any changes to the FUTA tax rate or taxable wage base limit, as these can impact their tax calculations.

In conclusion, calculating FUTA tax involves determining the taxable wage base, applying the current tax rate, and accounting for any eligible credits. Employers are responsible for calculating and paying FUTA tax, while employees' contributions are automatically deducted from their wages. By understanding the calculation process and staying informed about any changes to the tax rate or taxable wage base limit, employers can ensure they are accurately reporting and paying FUTA tax.

Fair Compensation: A Guide to Determining Employee Pay

You may want to see also

Explore related products

![]()

Penalties and Compliance: Overview of potential penalties for non-compliance and tips for ensuring proper FUTA tax handling

Employers who fail to comply with FUTA tax regulations may face significant penalties, including interest on unpaid taxes, fines for late filing, and even criminal charges in severe cases. The IRS can also impose penalties for negligence or intentional disregard of tax laws. To avoid these penalties, employers should ensure timely and accurate filing of FUTA tax returns, maintain proper records of employee wages and tax withholdings, and consult with a tax professional if unsure about any aspect of FUTA tax compliance.

One common mistake employers make is failing to report all employee wages subject to FUTA tax. This can lead to underpayment of taxes and potential penalties. Employers should carefully review their payroll records to ensure all wages, including bonuses, commissions, and severance pay, are properly reported. Additionally, employers should be aware of the FUTA tax rate and any changes to it, as well as the wage base limit, which is the maximum amount of an employee's wages subject to FUTA tax.

Employees, on the other hand, are not directly responsible for paying FUTA tax, but they may be indirectly affected by their employer's non-compliance. If an employer fails to pay FUTA tax, the employee may be liable for the tax if they knew or should have known about the non-compliance. To protect themselves, employees should ensure their employer is withholding the correct amount of FUTA tax from their wages and filing the necessary tax returns. If an employee suspects their employer is not complying with FUTA tax laws, they should consult with a tax professional or contact the IRS for guidance.

In conclusion, both employers and employees have a role to play in ensuring proper FUTA tax handling. Employers must comply with tax regulations to avoid penalties, while employees should be aware of their employer's tax obligations and take steps to protect themselves if necessary. By understanding their responsibilities and taking proactive measures, both employers and employees can help ensure proper FUTA tax compliance and avoid potential penalties.

Understanding Your Rights: Paid Time Off for Voting

You may want to see also

Frequently asked questions

Yes, both employees and employers are required to pay FUTA (Federal Unemployment Tax Act) taxes. Employers must withhold FUTA taxes from their employees' wages and also pay a matching amount from their own funds.

The current FUTA tax rate is 6.2% on the first $7,000 of an employee's wages. Employers pay 6.2% directly, and employees have 0.2% withheld from their wages, resulting in a total of 6.4% paid into the FUTA system.

Yes, there are some exceptions. For example, employers with fewer than 501 employees may be exempt from paying the employer portion of FUTA taxes if they meet certain criteria. Additionally, some types of workers, such as independent contractors, are not subject to FUTA taxes.

Employers report and pay FUTA taxes through the Electronic Federal Tax Payment System (EFTPS). They must file Form 940, Employer's Annual Federal Unemployment Tax Return, by January 31st of the year following the tax year.

If an employer fails to pay FUTA taxes, they may be subject to penalties and interest. The IRS can also impose a lien on the employer's property or assets to collect the unpaid taxes. In severe cases, the employer may face criminal charges.