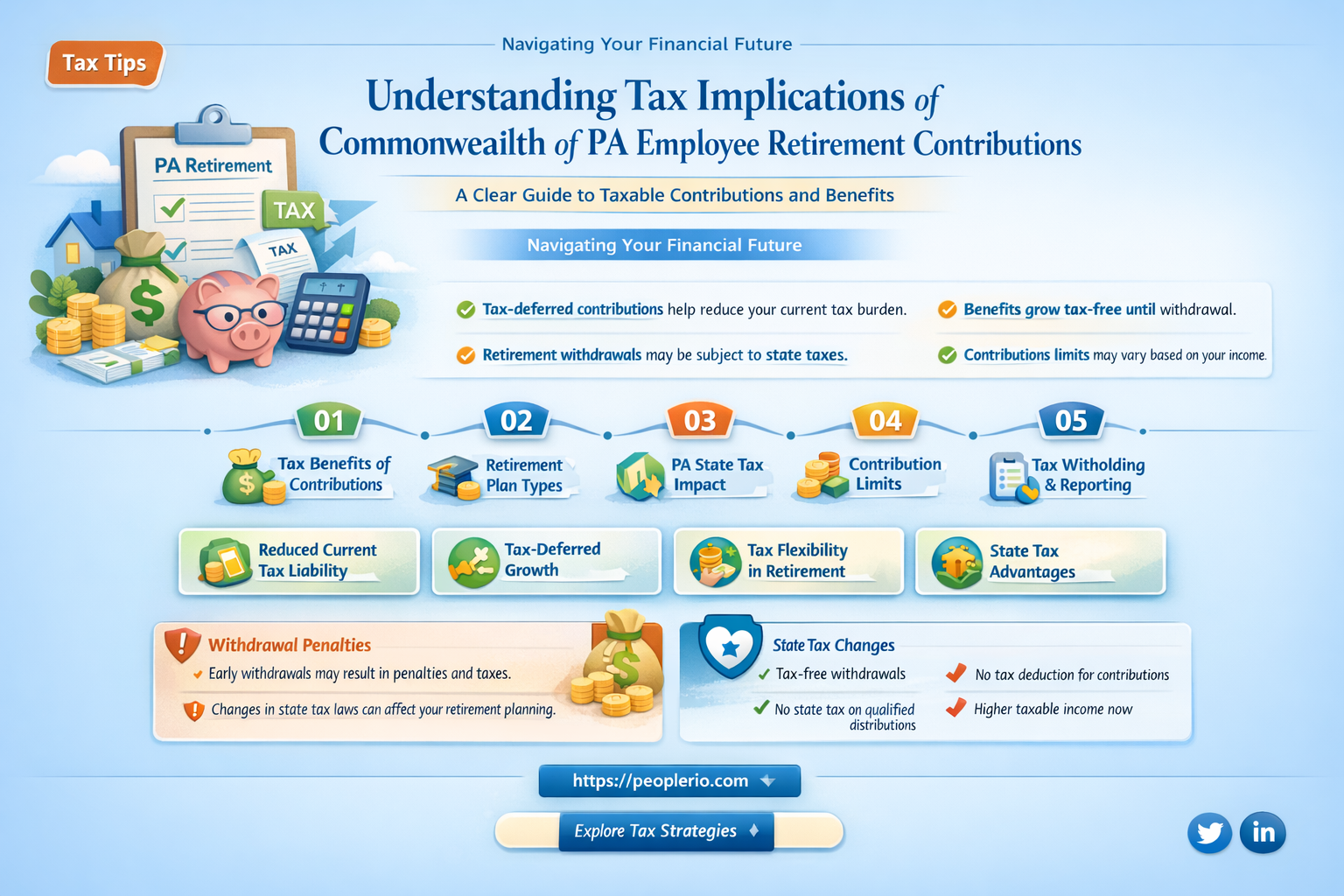

The taxation of retirement contributions for employees of the Commonwealth of Pennsylvania is a topic of interest for many public servants. Understanding the tax implications of these contributions is crucial for financial planning and compliance with state and federal tax laws. This paragraph will delve into the specifics of how these retirement contributions are treated for tax purposes, exploring both the state and federal tax considerations that Commonwealth employees need to be aware of. By examining the relevant tax codes and regulations, we can provide a comprehensive overview of the tax treatment of retirement contributions for Pennsylvania state employees.

| Characteristics | Values |

|---|---|

| Type of Contributions | Retirement contributions |

| Contributor | Commonwealth of Pennsylvania employees |

| Taxation Status | Taxed |

| Tax Type | State income tax |

| Tax Rate | Varies based on income and tax bracket |

| Tax Filing Requirement | Reported on state tax return |

| Tax Withholding | Withheld from paycheck |

| Tax Refund Possibility | Possible if over-withheld |

| Tax Implications | Affects state tax liability |

| Additional Tax Considerations | May affect federal tax return |

Explore related products

What You'll Learn

- Taxation Basics: Understand the fundamental tax rules applied to retirement contributions in Pennsylvania

- Commonwealth Employees: Specific regulations for those employed by the Commonwealth of Pennsylvania

- Retirement Plans: Overview of the types of retirement plans available to Commonwealth employees

- Contribution Limits: Maximum allowable contributions and how they impact taxation

- Tax Benefits: Explore potential tax benefits and deductions available for retirement contributions

![]()

Taxation Basics: Understand the fundamental tax rules applied to retirement contributions in Pennsylvania

Pennsylvania's tax laws have specific provisions for retirement contributions made by employees of the Commonwealth. Understanding these rules is crucial for employees to make informed decisions about their retirement savings.

One key aspect to consider is the tax treatment of contributions to the Pennsylvania State Employees' Retirement System (SERS). Contributions made by employees are generally not taxable by the Commonwealth, meaning that the money is deducted from their gross income before state taxes are applied. This can result in a lower taxable income and, consequently, a reduced state tax liability.

However, it's important to note that while these contributions are not taxed by Pennsylvania, they may still be subject to federal income tax. Employees should consult with a tax professional to understand how their retirement contributions impact their federal tax obligations.

Another consideration is the tax treatment of retirement benefits received from SERS. When employees retire and begin receiving pension benefits, these payments are generally taxable by both the Commonwealth and the federal government. The tax rate applied to these benefits will depend on the retiree's income level and tax bracket.

To maximize their retirement savings and minimize their tax liability, Commonwealth employees should consider contributing the maximum amount allowed to their retirement accounts each year. They should also explore other tax-advantaged retirement savings options, such as Roth IRAs or 457 plans, to diversify their retirement portfolio and potentially reduce their overall tax burden.

In conclusion, understanding the tax rules applied to retirement contributions in Pennsylvania is essential for Commonwealth employees to make the most of their retirement savings. By taking advantage of tax-deferred contributions and exploring other tax-efficient savings options, employees can better prepare for their financial future while minimizing their tax obligations.

Maximizing Tax Benefits: A Guide to Reporting Employee Retention Credit

You may want to see also

Explore related products

![]()

Commonwealth Employees: Specific regulations for those employed by the Commonwealth of Pennsylvania

For Commonwealth employees in Pennsylvania, retirement contributions are subject to specific regulations that govern how these funds are managed and taxed. One key aspect is the mandatory contribution rate, which is a percentage of the employee's salary. As of the latest information available up to June 2024, Commonwealth employees are required to contribute a certain percentage of their earnings towards their retirement fund. This rate can vary depending on the specific retirement plan and the employee's classification.

The taxation of these retirement contributions is another critical area. Generally, contributions made by employees towards their retirement plans are considered pre-tax contributions, meaning they are deducted from the employee's gross income before taxes are calculated. This can provide a significant tax advantage, as it reduces the amount of income subject to taxation in the current year. However, it's important to note that these contributions will be taxed when withdrawn during retirement.

Additionally, there are specific rules regarding the vesting of retirement contributions. Vesting refers to the process by which an employee gains ownership of the funds in their retirement account. For Commonwealth employees, vesting typically occurs over a period of time, during which the employee must remain employed by the Commonwealth to fully vest in their contributions and any employer-provided benefits.

Commonwealth employees also need to be aware of the retirement age and eligibility requirements. The retirement age can vary depending on the specific plan and the employee's classification. Early retirement options may be available, but they could come with penalties or reduced benefits. Employees should carefully review their retirement plan documents to understand the specific requirements and options available to them.

Lastly, it's crucial for Commonwealth employees to regularly review and manage their retirement accounts. This includes monitoring investment performance, adjusting contribution rates as needed, and ensuring that beneficiary designations are up to date. By staying informed and proactive, employees can better prepare for their financial future and make the most of their retirement benefits.

Maximizing Deductions: Understanding Business Expenses on State Tax Returns

You may want to see also

Explore related products

$17.99

![]()

Retirement Plans: Overview of the types of retirement plans available to Commonwealth employees

Commonwealth employees have access to several retirement plans, each designed to cater to different needs and preferences. The two primary types of retirement plans available are defined benefit plans and defined contribution plans. Defined benefit plans, such as the State Employees' Retirement System (SERS) and the Public School Employees' Retirement System (PSERS), provide a guaranteed retirement income based on a formula that takes into account factors like years of service and average salary. These plans are funded by both employee contributions and employer contributions, and they offer a level of security and predictability in retirement.

On the other hand, defined contribution plans, like the Deferred Compensation Plan (DCP) and the Pennsylvania Personal Retirement Account (PA-PRAC), allow employees to contribute a portion of their salary to a retirement account, with the employer often matching a percentage of the contributions. The investments in these plans are typically managed by the employee, offering more flexibility and control over the retirement savings. However, the eventual retirement income from these plans depends on the performance of the investments and the amount contributed over time.

In addition to these primary retirement plans, Commonwealth employees may also have access to other retirement savings options, such as Individual Retirement Accounts (IRAs) and annuities. These options can provide additional ways to save for retirement and may offer tax advantages or other benefits. Employees should carefully consider their retirement goals, risk tolerance, and financial situation when choosing the right retirement plan or combination of plans for their needs.

When it comes to the taxation of retirement contributions, Commonwealth employees may be eligible for tax deductions or credits on their state and federal income taxes. For example, contributions to traditional IRAs and certain employer-sponsored retirement plans are often tax-deductible, reducing the employee's taxable income for the year. Roth IRAs and Roth 401(k)s, on the other hand, are funded with after-tax dollars but offer tax-free growth and withdrawals in retirement. Understanding the tax implications of different retirement plans can help employees make informed decisions about their retirement savings strategy.

In conclusion, Commonwealth employees have a range of retirement plan options available to them, each with its own features, benefits, and tax considerations. By carefully evaluating these options and considering their individual retirement goals and financial circumstances, employees can make the most of their retirement savings opportunities and ensure a secure financial future.

Maximizing Tax Benefits: Understanding the Employee Retention Credit Impact

You may want to see also

![]()

Contribution Limits: Maximum allowable contributions and how they impact taxation

Contribution limits play a crucial role in determining the tax implications of retirement contributions for Commonwealth of Pennsylvania employees. The maximum allowable contributions are set by the Internal Revenue Service (IRS) and can vary depending on the type of retirement plan and the employee's age. For example, in 2023, the contribution limit for 401(k) plans is $22,500 for individuals under 50 years old and $30,000 for those 50 and older. These limits directly impact taxation because contributions made within these limits are generally tax-deferred, meaning they are not subject to federal income tax until they are withdrawn in retirement.

Exceeding these contribution limits can result in tax penalties and additional taxes. For instance, if an employee contributes more than the allowable limit to their 401(k), they may be subject to a 6% excise tax on the excess amount. Furthermore, the excess contributions may also be subject to regular income tax, reducing the overall tax benefit of contributing to the retirement plan. It is essential for employees to be aware of these limits and to monitor their contributions to avoid these penalties.

In addition to federal tax implications, state tax laws can also affect the taxation of retirement contributions. In Pennsylvania, contributions to certain retirement plans, such as the State Employees' Retirement System (SERS), may be exempt from state income tax. However, the specifics of these exemptions can be complex and may depend on factors such as the employee's income level and the type of retirement plan.

To maximize the tax benefits of retirement contributions, employees should consider contributing up to the maximum allowable limit each year. This can be achieved through regular payroll deductions or by making catch-up contributions if they are eligible. Additionally, employees should be aware of any employer matching contributions, as these can also impact the overall tax implications of their retirement savings.

In conclusion, understanding contribution limits is essential for Commonwealth of Pennsylvania employees to optimize their retirement savings and minimize their tax liability. By staying within these limits and taking advantage of tax-deferred contributions, employees can effectively plan for their financial future while also complying with federal and state tax laws.

Maximizing Tax Benefits: The Truth About Employee Wage Deductions

You may want to see also

![]()

Tax Benefits: Explore potential tax benefits and deductions available for retirement contributions

Pennsylvania employees contributing to retirement plans may be eligible for several tax benefits and deductions. One such benefit is the Pennsylvania state income tax deduction for contributions to a retirement plan. This deduction can reduce the amount of state income tax owed, providing a financial advantage to those saving for retirement. Additionally, contributions to certain retirement plans, such as 401(k)s and IRAs, may also be eligible for federal tax deductions or credits, further reducing the tax burden on retirement savers.

To maximize these tax benefits, it's essential to understand the specific rules and limitations associated with each type of retirement plan. For example, 401(k) contributions are typically made pre-tax, reducing taxable income for the year, while Roth IRA contributions are made after-tax but offer tax-free growth and withdrawals in retirement. By strategically choosing the right retirement plan and contribution amount, employees can optimize their tax savings while working towards their retirement goals.

It's also important to consider the impact of required minimum distributions (RMDs) on retirement tax planning. RMDs are mandatory withdrawals from certain retirement accounts that must begin at age 72 (or 70 1/2 if born before July 1, 1949). These distributions are taxed as ordinary income and can significantly increase an individual's tax liability in retirement. However, by planning ahead and considering strategies such as Roth conversions or charitable donations from retirement accounts, employees can potentially minimize the tax impact of RMDs.

In conclusion, understanding and leveraging the tax benefits available for retirement contributions can be a powerful tool for Pennsylvania employees. By carefully selecting the right retirement plan, maximizing contributions, and planning for RMDs, individuals can reduce their tax burden and build a more secure financial future.

Mastering Employee Tax Filing: A Step-by-Step Guide for Employers

You may want to see also

Frequently asked questions

Yes, retirement contributions made by Commonwealth of Pennsylvania employees are generally subject to federal income tax. However, they may be exempt from state and local taxes depending on specific conditions and agreements.

At the federal level, retirement contributions are taxed as ordinary income. This means that the amount contributed is added to the employee's gross income and taxed at their marginal tax rate.

Yes, there are special considerations for certain types of retirement contributions. For example, contributions to a 401(k) or 403(b) plan may be made on a pre-tax basis, which can reduce the employee's taxable income. Additionally, some retirement plans may offer a Roth option, which allows contributions to be made after-tax but grows tax-free.