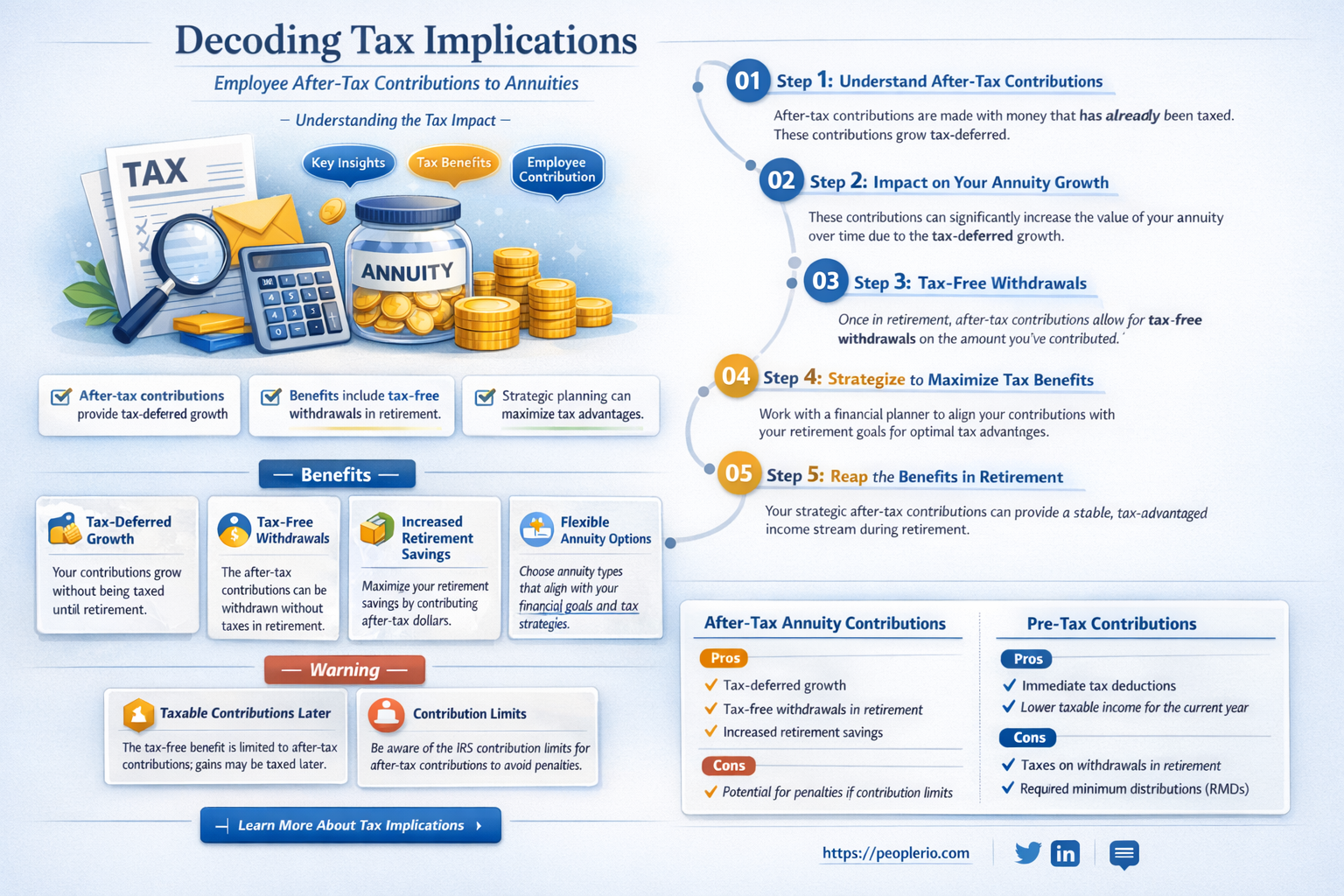

Employee after-tax contributions to annuities are a common financial strategy used to supplement retirement income. These contributions are made from an employee's net pay, meaning the money has already been taxed once. The question arises whether these after-tax contributions are subject to additional taxation. Understanding the tax implications of such contributions is crucial for both employees planning their retirement and employers offering annuity plans as part of their benefits package. This paragraph will delve into the specifics of how after-tax annuity contributions are treated under current tax laws, exploring the nuances and potential benefits or drawbacks for employees.

| Characteristics | Values |

|---|---|

| Taxability | After-tax contributions to annuities made by employees are generally not taxable as income to the employee. |

| Contribution Source | Contributions are made from the employee's after-tax income. |

| Tax Treatment | The contributions are considered tax-deferred, meaning taxes are paid when the funds are withdrawn, typically in retirement. |

| Employer Involvement | Employers may offer annuities as part of a retirement plan, but the tax treatment remains the same. |

| Exceptions | Certain exceptions may apply, such as if the annuity is a non-qualified plan or if the employee receives a lump sum payment. |

| Reporting Requirements | Employees may need to report contributions on their tax return, depending on the type of annuity and the tax laws in their jurisdiction. |

Explore related products

What You'll Learn

- Taxation Basics: Understanding the fundamental tax rules applicable to employee contributions

- Types of Annuities: Differentiating between qualified and non-qualified annuities for tax purposes

- Contribution Limits: Exploring the maximum allowable contributions and their tax implications

- Tax-Deferred Growth: Analyzing how taxes are deferred on annuity contributions and earnings

- Withdrawal Rules: Discussing the tax consequences of withdrawing funds from an annuity

![]()

Taxation Basics: Understanding the fundamental tax rules applicable to employee contributions

Employee contributions to annuities are a common component of retirement planning, but understanding the tax implications can be complex. In general, contributions made with after-tax dollars are not taxable when withdrawn, as the taxes have already been paid. However, the earnings on these contributions grow tax-deferred and are taxed as ordinary income when withdrawn.

There are specific rules and limits to consider when making after-tax contributions to an annuity. For example, the IRS has contribution limits for traditional IRAs and 401(k)s, which are indexed for inflation each year. In 2023, the contribution limit for traditional IRAs is $6,500, or $7,500 if you are age 50 or older. For 401(k)s, the limit is $22,500, or $30,000 if you are age 50 or older.

It's also important to note that after-tax contributions to an annuity may be subject to the 10% early withdrawal penalty if taken before age 59 1/2, unless an exception applies. Additionally, the taxation of annuity withdrawals can be affected by the type of annuity contract, the payout option chosen, and the tax laws in your state.

To maximize the tax benefits of after-tax contributions to an annuity, it's essential to understand the rules and consult with a tax professional or financial advisor. They can help you navigate the complexities of annuity taxation and develop a retirement plan that aligns with your financial goals and objectives.

Understanding 401k Deferrals: Are They Subject to Payroll Taxes?

You may want to see also

Explore related products

![]()

Types of Annuities: Differentiating between qualified and non-qualified annuities for tax purposes

Annuities can be broadly categorized into two types for tax purposes: qualified and non-qualified annuities. Qualified annuities are those that are purchased with pre-tax dollars, typically through employer-sponsored retirement plans such as 401(k)s or IRAs. Non-qualified annuities, on the other hand, are purchased with after-tax dollars. The primary difference between these two types lies in how they are taxed. Qualified annuities grow tax-deferred, meaning that the earnings on the investment are not taxed until they are withdrawn. Non-qualified annuities, however, do not have this tax advantage. The earnings on non-qualified annuities are taxed as ordinary income in the year they are received.

When it comes to employee after-tax contributions to annuities, it is important to understand the implications of these contributions on the tax treatment of the annuity. If an employee contributes after-tax dollars to a qualified annuity, these contributions are generally not deductible. However, the earnings on these contributions will grow tax-deferred, which can be a significant advantage over time. In contrast, contributions to non-qualified annuities do not have the same tax-deferred growth benefit, but they may be eligible for a tax deduction in the year they are made.

One key consideration for employees is the impact of these contributions on their overall tax liability. Contributing to a qualified annuity can reduce taxable income in the contribution year, potentially lowering the employee's tax bracket. However, this benefit must be weighed against the future tax liability when the funds are withdrawn. Non-qualified annuities do not offer the same immediate tax benefit, but they can provide a steady stream of taxable income in retirement.

Another important factor to consider is the flexibility of the annuity. Qualified annuities often have more stringent rules regarding withdrawals and may incur penalties for early distributions. Non-qualified annuities, on the other hand, typically offer more flexibility in terms of withdrawals and may not have the same penalty structures.

In conclusion, understanding the differences between qualified and non-qualified annuities is crucial for employees considering after-tax contributions. While qualified annuities offer tax-deferred growth, non-qualified annuities may provide more immediate tax benefits and flexibility. Employees should carefully evaluate their individual financial situation and tax goals when deciding which type of annuity is most appropriate for their needs.

Unreimbursed Clergy Expenses: Tax Deductibility Under Recent Legislation

You may want to see also

Explore related products

![]()

Contribution Limits: Exploring the maximum allowable contributions and their tax implications

Understanding contribution limits is crucial when navigating the complex landscape of retirement savings and tax implications. The maximum allowable contributions to retirement accounts, such as 401(k)s and IRAs, are set by the IRS and can change annually due to inflation adjustments. For example, in 2023, the contribution limit for a 401(k) is $22,500 for individuals under 50, with an additional $7,500 catch-up contribution allowed for those 50 and older.

These limits have significant tax implications. Contributions to traditional 401(k)s and IRAs are made on a pre-tax basis, reducing taxable income for the year. However, withdrawals in retirement are taxed as ordinary income. Roth accounts, on the other hand, allow for after-tax contributions, meaning the money grows tax-free and qualified withdrawals are tax-free.

It's important to note that exceeding these contribution limits can result in penalties, including a 6% excise tax on the excess amount. Additionally, the IRS may require the excess contributions to be withdrawn, potentially leading to further tax consequences.

When planning for retirement, it's essential to consider these contribution limits and their tax implications. Maximizing contributions within these limits can help individuals save more for retirement while minimizing their tax burden. Consulting with a financial advisor can provide personalized guidance on how to optimize retirement savings within the framework of current tax laws and contribution limits.

Railroad Employee Tax Filing Guide: Simplify Your Tax Process

You may want to see also

Explore related products

![]()

Tax-Deferred Growth: Analyzing how taxes are deferred on annuity contributions and earnings

Annuities offer a unique advantage in the realm of retirement planning: tax-deferred growth. This means that the contributions you make to an annuity, as well as the earnings it generates, are not subject to taxation until you begin receiving distributions. This can be a powerful tool for accumulating wealth over time, as it allows your money to grow without the drag of annual taxes.

To understand how this works, let's break it down step by step. When you contribute to an annuity, your money is invested in various assets, such as stocks, bonds, or mutual funds. As these investments grow, the earnings are reinvested back into the annuity, compounding over time. Because these earnings are not taxed as they are generated, they can grow more rapidly than if they were subject to annual taxation.

The tax-deferred nature of annuities is particularly beneficial for those in higher tax brackets. By deferring taxes until retirement, when you may be in a lower tax bracket, you can potentially reduce your overall tax liability. Additionally, because the earnings are not taxed annually, you don't have to worry about capital gains taxes or other investment-related taxes.

However, it's important to note that tax-deferred does not mean tax-free. When you begin receiving distributions from the annuity, typically in retirement, the payments will be subject to taxation. The key is to time your distributions strategically to minimize your tax burden.

In conclusion, tax-deferred growth is a significant advantage of annuities, allowing your contributions and earnings to grow without the hindrance of annual taxes. By understanding how this works and planning accordingly, you can make the most of this powerful retirement planning tool.

Understanding State Tax Exemptions for Employees: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Withdrawal Rules: Discussing the tax consequences of withdrawing funds from an annuity

Withdrawing funds from an annuity can have significant tax implications, and understanding these rules is crucial for financial planning. Generally, withdrawals from an annuity are taxed as ordinary income, which means they are subject to federal and state income taxes. However, there are some exceptions and strategies that can help minimize the tax burden.

One important consideration is the age at which withdrawals are made. If withdrawals are taken before age 59½, they may be subject to a 10% early withdrawal penalty in addition to regular income taxes. This penalty is designed to discourage early withdrawals and encourage individuals to keep their retirement funds invested until they reach a certain age.

Another factor to consider is the type of annuity. There are two main types: immediate annuities and deferred annuities. Immediate annuities begin paying out benefits immediately after purchase, while deferred annuities accumulate value over time and begin paying out at a later date. The tax treatment of withdrawals can vary depending on the type of annuity and the specific contract terms.

To minimize taxes on annuity withdrawals, individuals can consider several strategies. One approach is to annuitize the contract, which means converting the accumulated value into a stream of regular payments. This can help spread out the tax liability over time and potentially reduce the overall tax burden. Another strategy is to take withdrawals in lower-income years, when the individual's tax bracket is lower. This can help reduce the amount of taxes owed on the withdrawals.

It's also important to consider the impact of required minimum distributions (RMDs). Once an individual reaches age 72 (or age 70½ if they are a beneficiary), they are required to take a minimum amount of withdrawals from their retirement accounts each year. Failure to take the required distributions can result in a 50% penalty on the amount that should have been withdrawn.

In conclusion, understanding the tax consequences of withdrawing funds from an annuity is essential for effective retirement planning. By considering factors such as age, annuity type, and withdrawal strategies, individuals can minimize their tax liability and make the most of their retirement savings.

Understanding COBRA Premiums: Are They Pre-Tax for Employees?

You may want to see also

Frequently asked questions

Generally, employee after-tax contributions to annuities are not taxable when they are made with after-tax dollars. This is because the employee has already paid taxes on this money before contributing it to the annuity.

While the contributions themselves are not taxable, you may need to report the earnings on your tax return. The specific reporting requirements can vary depending on the type of annuity and the tax laws in your jurisdiction.

After-tax annuity contributions do not directly affect your taxable income since they are made with money that has already been taxed. However, the growth of the annuity over time may be subject to taxation when you withdraw the funds.

Yes, there can be exceptions and special rules depending on the specific annuity plan and the tax regulations in your country. For example, some plans may have contribution limits or specific withdrawal rules that can impact the tax treatment of the contributions and earnings.