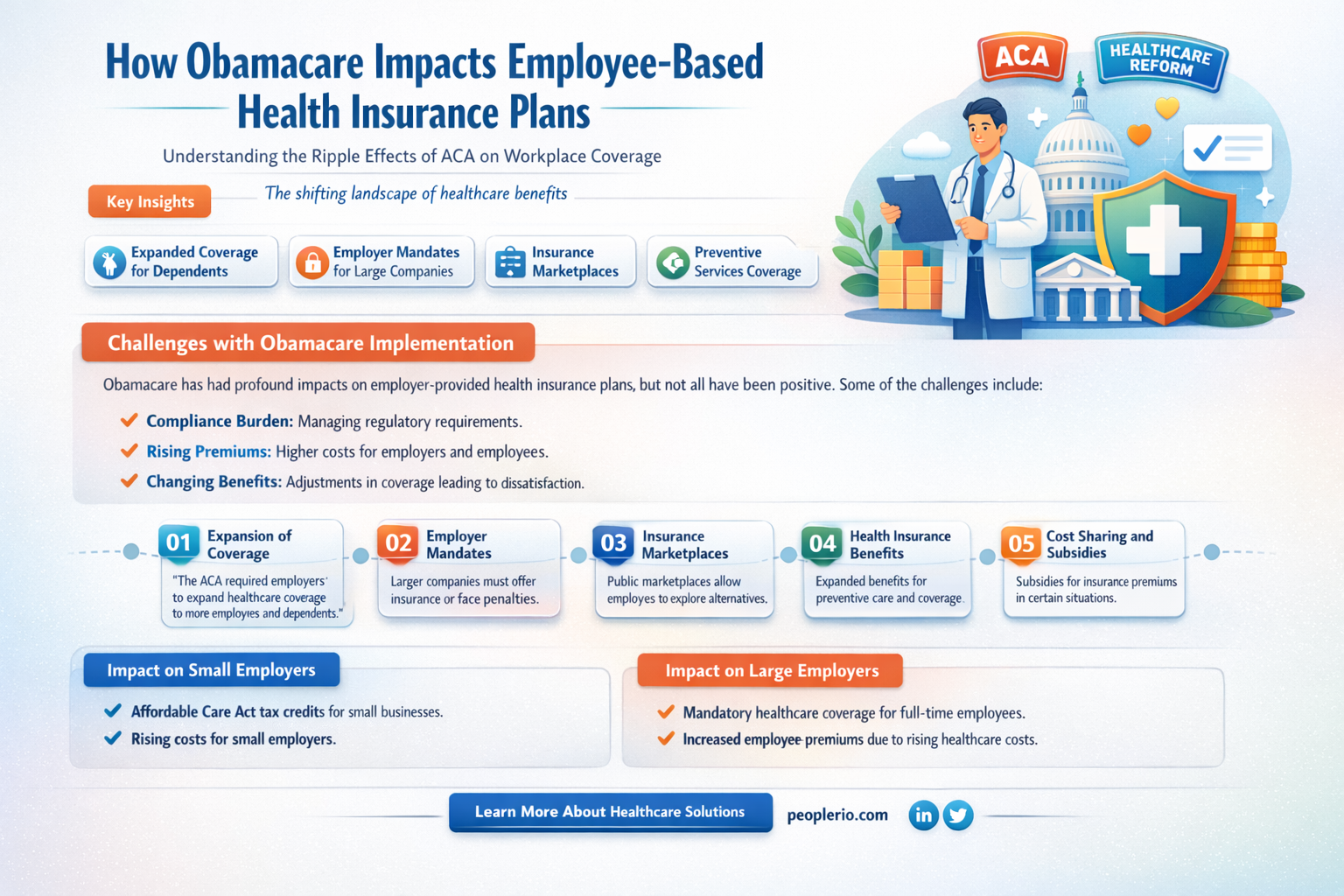

The Affordable Care Act (ACA), commonly known as Obamacare, has had a significant impact on the healthcare landscape in the United States. One area of particular interest is how the ACA affects employer-based health insurance plans. Prior to the ACA, employer-sponsored insurance was the primary source of health coverage for many Americans. The ACA introduced several changes aimed at improving access to healthcare and reducing costs, which have had both direct and indirect effects on employer-based plans. These changes include the requirement for employers to provide coverage to a certain percentage of their employees, the prohibition on denying coverage based on pre-existing conditions, and the establishment of health insurance exchanges. As a result, some employers have had to adjust their plans to comply with the new regulations, while others have chosen to discontinue offering health insurance altogether. The ACA has also led to an increase in the number of Americans eligible for Medicaid and other government-sponsored programs, which has further shifted the dynamics of the healthcare market. Overall, the ACA has had a complex and multifaceted impact on employer-based health insurance, with effects varying depending on the size and type of employer, as well as the specific provisions of the ACA.

| Characteristics | Values |

|---|---|

| Type of Insurance | Employee-based health insurance |

| Legislation Impact | Affordable Care Act (Obamacare) |

| Coverage Changes | Essential health benefits requirement, Minimum coverage standards |

| Cost Implications | Potential increase in premiums, Employer mandate penalties |

| Enrollment Adjustments | Open enrollment periods, Special enrollment rights |

| Pre-existing Conditions | Prohibited from denying coverage based on pre-existing conditions |

| Preventive Care | Required to cover preventive services without cost-sharing |

| Dependent Coverage | Extended coverage for dependents up to age 26 |

| Appeals Process | Enhanced appeals process for denied claims |

| Marketplaces | Option to purchase through health insurance marketplaces |

Explore related products

What You'll Learn

- Coverage Changes: New essential health benefits and pre-existing condition protections

- Cost Impacts: Premium increases or decreases due to ACA regulations

- Employer Mandates: Requirements for employers to provide health insurance

- Subsidy Eligibility: Employee eligibility for subsidies on health insurance premiums

- Network Adjustments: Changes in provider networks and out-of-pocket costs

![]()

Coverage Changes: New essential health benefits and pre-existing condition protections

The Affordable Care Act (ACA), commonly known as Obamacare, introduced significant changes to the healthcare landscape in the United States. One of the key areas impacted was employee-based health insurance, particularly in terms of coverage changes. The ACA mandated that all health insurance plans, including those provided by employers, must cover a set of essential health benefits. These benefits include preventive care, prescription drugs, mental health services, and maternity care, among others. This requirement aimed to ensure that all Americans have access to comprehensive healthcare, regardless of their employment status or pre-existing health conditions.

In addition to the essential health benefits, the ACA also implemented important protections for individuals with pre-existing conditions. Prior to the ACA, many people with pre-existing health issues faced difficulties obtaining health insurance, often being denied coverage or charged exorbitant premiums. The ACA prohibited insurance companies from denying coverage or charging higher premiums based on pre-existing conditions, making health insurance more accessible and affordable for millions of Americans.

For employers, these changes meant that they had to review and potentially modify their health insurance offerings to comply with the new regulations. This could involve updating plan documents, communicating changes to employees, and working with insurance providers to ensure that the plans met the ACA's requirements. Failure to comply with these regulations could result in penalties and legal consequences for employers.

The impact of these coverage changes was significant, particularly for small businesses and individuals who previously struggled to obtain affordable health insurance. By expanding coverage options and protecting those with pre-existing conditions, the ACA aimed to create a more equitable healthcare system. However, the implementation of these changes was not without challenges, as some employers and insurance providers faced difficulties in adapting to the new requirements.

Overall, the coverage changes introduced by the ACA represented a major shift in the healthcare system, with a focus on expanding access to comprehensive care and protecting vulnerable populations. While the transition was not seamless, the long-term goal of ensuring that all Americans have access to quality healthcare remained a driving force behind these reforms.

Are Employee Health Insurance Contributions Taxable? Key Facts Explained

You may want to see also

Explore related products

![]()

Cost Impacts: Premium increases or decreases due to ACA regulations

The Affordable Care Act (ACA), commonly known as Obamacare, has had a significant impact on the cost of employee-based health insurance premiums. One of the primary goals of the ACA was to make healthcare more affordable and accessible to all Americans. However, the effects on premium costs have been mixed, with some employers experiencing increases while others have seen decreases.

One of the key factors contributing to premium increases is the ACA's requirement for insurers to cover essential health benefits, such as preventive care, prescription drugs, and mental health services. This mandate has led to higher costs for insurers, which are often passed on to employers and employees in the form of higher premiums. Additionally, the ACA's prohibition on denying coverage based on pre-existing conditions has also contributed to premium increases, as insurers must now account for the potential costs of covering individuals with chronic illnesses.

On the other hand, the ACA has also implemented several measures aimed at reducing healthcare costs, which have helped to offset some of the premium increases. For example, the law includes provisions for value-based care, which incentivizes healthcare providers to focus on quality and efficiency rather than quantity of services. This approach has been shown to reduce overall healthcare spending, which can lead to lower premiums for employers and employees.

Another factor that has influenced premium costs is the ACA's creation of health insurance exchanges, which provide a marketplace for individuals and small businesses to purchase coverage. This increased competition among insurers has helped to drive down prices, which can benefit employers who offer health insurance to their employees.

In conclusion, the impact of the ACA on employee-based health insurance premiums has been complex and multifaceted. While some employers have experienced premium increases due to the law's mandates and regulations, others have seen decreases as a result of its cost-saving measures and increased competition among insurers. Ultimately, the specific effects on premium costs will depend on a variety of factors, including the size and type of employer, the health insurance plan offered, and the overall healthcare market in the employer's region.

Understanding Employee Health: Key Factors for Workplace Well-Being

You may want to see also

Explore related products

![]()

Employer Mandates: Requirements for employers to provide health insurance

Under the Affordable Care Act (ACA), also known as Obamacare, employer mandates were established to ensure that businesses provide health insurance to their employees. This requirement applies to employers with 50 or more full-time employees. The mandate aims to increase the number of Americans with health coverage and reduce the burden on public health programs. Employers that fail to comply with this mandate may face penalties, which can be substantial depending on the number of employees and the duration of non-compliance.

The employer mandate has been a subject of debate, with some arguing that it increases costs for businesses and may lead to job losses or reduced hours for employees. However, proponents of the mandate argue that it promotes fairness in the healthcare system, as businesses that do not provide health insurance may benefit from lower labor costs at the expense of their employees' health and well-being.

To comply with the employer mandate, businesses must offer health insurance that meets certain standards, including minimum essential coverage and affordability. Employers must also report information about the health insurance they offer to employees and the IRS. This reporting requirement helps to ensure transparency and accountability in the healthcare system.

In recent years, there have been changes to the employer mandate, including delays in implementation and modifications to the reporting requirements. These changes have been made in response to feedback from businesses and other stakeholders, as well as to address concerns about the impact of the mandate on the economy.

Overall, the employer mandate is a key component of the ACA, aimed at increasing access to health insurance for millions of Americans. While it has faced challenges and criticism, it remains an important part of the effort to reform the healthcare system and promote fairness and equality in access to healthcare.

Boosting Employee Wellness: Strategies for a Healthier, Happier Workforce

You may want to see also

Explore related products

![Obamacare Survival Guide (Paperback)--by Nick J. Tate [2012 Edition] ISBN: 9780893348625](https://m.media-amazon.com/images/I/41sDyKzHXEL._AC_UY218_.jpg)

![]()

Subsidy Eligibility: Employee eligibility for subsidies on health insurance premiums

Under the Affordable Care Act (ACA), also known as Obamacare, employee-based health insurance plans are indeed affected, particularly in terms of subsidy eligibility. Subsidies are financial assistance provided to individuals to help cover the cost of health insurance premiums. To be eligible for these subsidies, employees must meet certain criteria.

One key factor in determining subsidy eligibility is the employee's income level. The ACA provides subsidies to individuals whose income falls between 100% and 400% of the Federal Poverty Level (FPL). This means that employees earning up to four times the poverty level may qualify for assistance. The subsidy amount is calculated based on a sliding scale, with lower-income individuals receiving greater assistance.

Another important consideration is the cost of the employer-sponsored health insurance plan. If the employer's plan is deemed unaffordable, employees may be eligible for subsidies to purchase coverage through the health insurance marketplace. This is particularly relevant for employees whose employer-sponsored plan exceeds 9.86% of their income, as they may opt out of the employer's plan and seek subsidies for marketplace coverage.

It's also worth noting that employees who are offered employer-sponsored health insurance but choose to purchase coverage through the marketplace without receiving subsidies from their employer may still be eligible for ACA subsidies. However, if an employee receives any form of employer assistance, they are generally not eligible for marketplace subsidies.

In summary, employee eligibility for subsidies on health insurance premiums under the ACA is primarily determined by income level and the affordability of the employer-sponsored plan. Employees earning up to 400% of the FPL and those with unaffordable employer plans may qualify for subsidies to help cover the cost of health insurance. Understanding these criteria is essential for employees navigating the complexities of health insurance coverage under Obamacare.

Understanding Florida's Employee Health Care Act: Key Requirements Explained

You may want to see also

Explore related products

$12.12 $15.9

![]()

Network Adjustments: Changes in provider networks and out-of-pocket costs

Under the Affordable Care Act (ACA), also known as Obamacare, significant changes have occurred in the landscape of employee-based health insurance. One of the key areas impacted is the provider networks and the associated out-of-pocket costs for employees. These changes have been driven by the ACA's emphasis on expanding coverage, improving quality of care, and controlling healthcare costs.

One notable adjustment is the shift towards narrower provider networks. To comply with the ACA's requirements, many employers have had to renegotiate contracts with healthcare providers, often resulting in more limited choices for employees. This has led to concerns about access to preferred doctors and specialists, as well as potential increases in out-of-pocket expenses for out-of-network care.

Another significant change is the impact on out-of-pocket costs. The ACA has introduced new rules and regulations aimed at reducing these costs, such as the elimination of lifetime limits on coverage and the requirement for plans to cover preventive care without cost-sharing. However, these changes have also led to increased premiums for some employees, as insurers pass on the costs of these new requirements.

Employers have had to adapt to these changes by reevaluating their health insurance offerings and making difficult decisions about plan design and provider networks. Some have chosen to self-insure, taking on more risk but also gaining more control over plan design and costs. Others have opted to move to fully insured plans, shifting the risk to insurers but potentially facing higher premiums.

In conclusion, the ACA has brought about significant network adjustments and changes in out-of-pocket costs for employee-based health insurance. While these changes have expanded coverage and improved quality of care, they have also led to challenges for employers and employees alike. As the healthcare landscape continues to evolve, it is essential for employers to stay informed and adapt their strategies to ensure they are providing the best possible health insurance options for their employees.

Ensuring Workplace Wellness: Effective Strategies for Monitoring Employee Health

You may want to see also

Frequently asked questions

The Affordable Care Act has introduced several changes to employer-sponsored health insurance plans, including the requirement for plans to cover essential health benefits, the prohibition of denying coverage based on pre-existing conditions, and the mandate for employers with 50 or more full-time employees to offer health insurance or face penalties.

Yes, under Obamacare, the tax-free status of employer-sponsored health insurance premiums has been maintained. However, the law has introduced new taxes on health insurance providers and employers, such as the health insurance tax and the Cadillac tax on high-value health plans.

The impact of Obamacare on the cost of employer-sponsored health insurance has been mixed. While some provisions, such as the requirement to cover essential health benefits, may have increased costs, others, like the prohibition of denying coverage based on pre-existing conditions, may have helped to stabilize or reduce costs over time.

Employers are required to report certain information about their health insurance plans to the IRS and to employees. This includes providing a summary of benefits and coverage (SBC) to employees at the time of enrollment and annually thereafter, as well as filing Forms 1094-B and 1095-B with the IRS to report health insurance coverage.

Obamacare has influenced the design of employer-sponsored health insurance plans by requiring them to meet certain standards, such as covering essential health benefits and providing a minimum level of coverage. Additionally, the law has encouraged the adoption of wellness programs and preventive care services as part of employer-sponsored plans.