Employee contributions to health insurance are a common aspect of employment benefits, and understanding their tax implications is crucial for both employees and employers. In many countries, including the United States, employee contributions to health insurance are considered pre-tax deductions. This means that the amount an employee contributes to their health insurance plan is deducted from their gross income before taxes are calculated. As a result, these contributions can lower an employee's taxable income, potentially reducing their overall tax liability. However, it's important to note that the specific tax treatment of health insurance contributions can vary depending on the country's tax laws and the type of health insurance plan in place.

| Characteristics | Values |

|---|---|

| Type of Contribution | Employee contributions to health insurance |

| Tax Status | Pre-tax |

| Benefit | Reduces taxable income |

| Limit | Subject to IRS limits |

| Employer Involvement | Employer may match contributions |

| Portability | Contributions may be portable if changing jobs |

| Impact on Benefits | May affect eligibility for certain benefits |

| Documentation Required | May require proof of contribution for tax purposes |

Explore related products

What You'll Learn

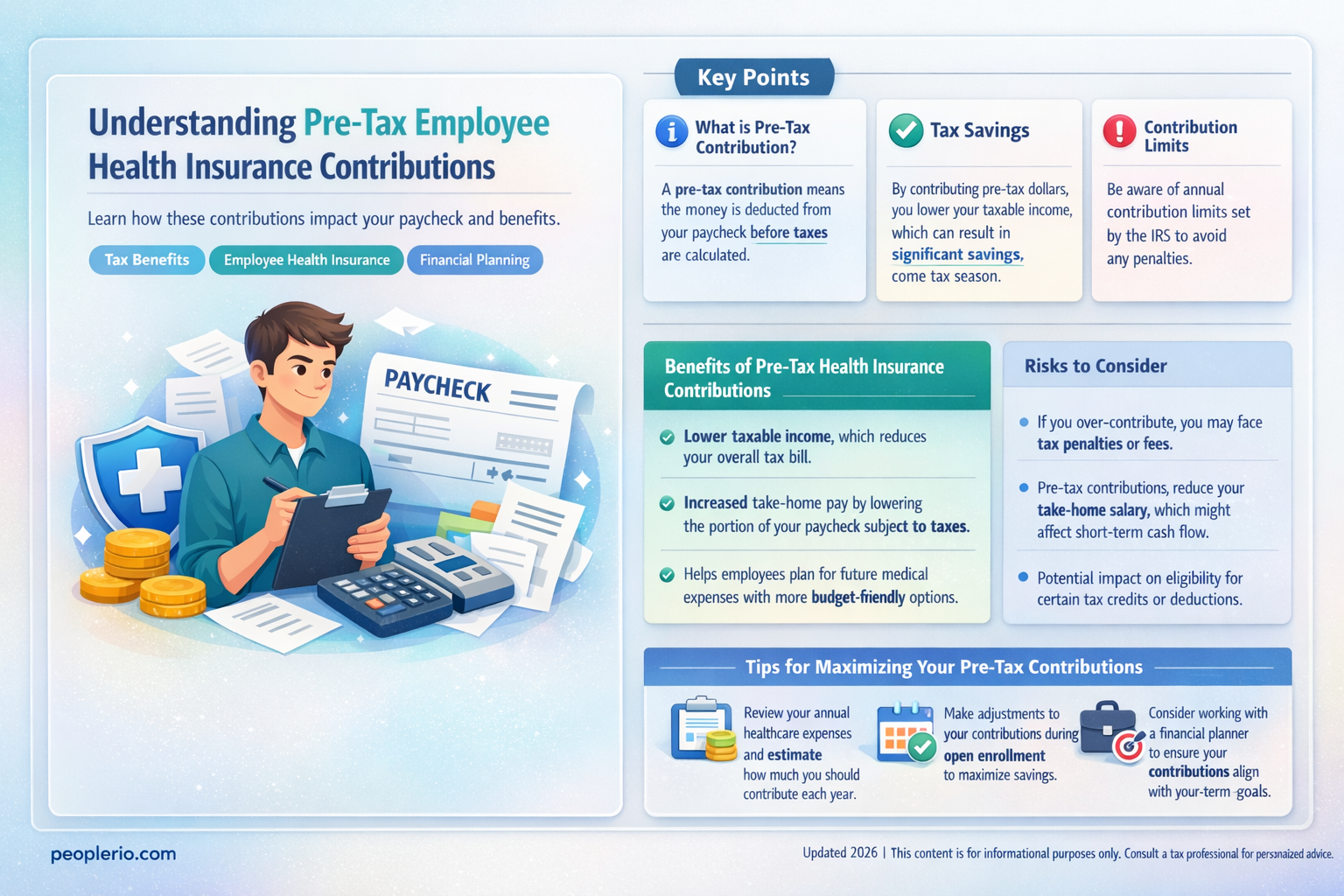

- Definition of Pre-Tax Contributions: Contributions made before taxes are deducted, reducing taxable income

- Benefits to Employees: Pre-tax contributions lower employees' tax burden and increase take-home pay

- Employer Contributions: Employers may also contribute pre-tax, reducing their payroll tax liabilities

- IRS Regulations: Specific IRS rules and limits apply to pre-tax health insurance contributions

- Impact on Tax Brackets: Higher contributions can lower an employee's tax bracket, providing additional savings

![]()

Definition of Pre-Tax Contributions: Contributions made before taxes are deducted, reducing taxable income

Pre-tax contributions refer to payments made towards certain benefits or expenses before any taxes are deducted from an individual's income. These contributions are typically subtracted from an employee's gross salary, thereby reducing their taxable income. This can result in a lower tax liability for the employee, as they are taxed on a smaller amount of income.

In the context of health insurance, pre-tax contributions are often used to pay for premiums or other related expenses. This is because health insurance premiums can be quite high, and paying for them pre-tax can help to reduce the overall cost for the employee. Additionally, pre-tax contributions can be used to fund other types of benefits, such as retirement plans or flexible spending accounts.

One important thing to note is that pre-tax contributions are subject to certain limits and regulations. For example, there may be a maximum amount that can be contributed pre-tax towards health insurance premiums each year. Additionally, pre-tax contributions may not be available for all types of health insurance plans or for all employees.

Another consideration is that pre-tax contributions can impact an individual's overall financial situation. While they can help to reduce taxable income and tax liability, they may also reduce the amount of take-home pay that an employee receives. Therefore, it is important for employees to carefully consider the benefits and drawbacks of making pre-tax contributions towards health insurance or other expenses.

In conclusion, pre-tax contributions can be a valuable tool for employees looking to reduce their tax liability and manage their expenses. However, it is important to understand the limits and regulations surrounding pre-tax contributions, as well as the potential impact on an individual's overall financial situation.

Maximizing Tax Benefits: Employee Car Allowances Explained

You may want to see also

![]()

Benefits to Employees: Pre-tax contributions lower employees' tax burden and increase take-home pay

Pre-tax contributions to health insurance offer significant financial benefits to employees. By allowing workers to deduct their health insurance premiums from their gross income before taxes are calculated, these contributions effectively lower their taxable income. This reduction in taxable income translates directly into a decreased tax burden, as employees are taxed on a smaller amount of their earnings. Consequently, this results in an increase in their take-home pay, providing them with more disposable income.

One of the key advantages of pre-tax contributions is that they enable employees to allocate a portion of their income towards health insurance without feeling the immediate financial pinch. This is particularly beneficial for those who may struggle to afford health insurance premiums out of their after-tax income. By reducing the upfront cost of health insurance, pre-tax contributions make it more accessible for employees to maintain or improve their health coverage.

Furthermore, pre-tax contributions can also have a positive impact on employee morale and job satisfaction. When employees perceive that their employer is offering them a valuable benefit that helps them save money, they are more likely to feel valued and appreciated. This can lead to increased loyalty and productivity, as well as a more positive work environment.

In addition to the direct financial benefits, pre-tax contributions to health insurance can also have long-term implications for employees' financial well-being. By reducing their tax burden and increasing their take-home pay, employees may be better positioned to save for retirement, pay off debts, or invest in other financial goals. This can contribute to a more secure financial future and reduce financial stress.

Overall, the benefits of pre-tax contributions to health insurance are multifaceted. They not only provide immediate financial relief but also contribute to employees' long-term financial stability and job satisfaction. As such, they are a valuable component of employee benefits packages and can play a significant role in attracting and retaining top talent.

Understanding the I-9 Tax Form: A Comprehensive Guide

You may want to see also

![]()

Employer Contributions: Employers may also contribute pre-tax, reducing their payroll tax liabilities

Employers have the option to contribute to their employees' health insurance premiums on a pre-tax basis. This means that the contributions are deducted from the employees' gross income before taxes are calculated, reducing the taxable income and, consequently, the payroll tax liabilities for both the employer and the employee. This can be a significant benefit for employers, as it allows them to offer competitive health insurance packages while also minimizing their tax burden.

One of the key advantages of employer pre-tax contributions is that they can help attract and retain top talent. By offering a comprehensive health insurance plan with pre-tax contributions, employers can make their compensation packages more appealing to potential employees. Additionally, pre-tax contributions can help reduce the overall cost of health insurance for employees, making it more affordable and accessible.

However, it's important for employers to understand the implications of pre-tax contributions on their payroll tax liabilities. While pre-tax contributions can reduce the taxable income of employees, they also reduce the employer's payroll tax liabilities. This means that employers need to carefully consider the impact of pre-tax contributions on their overall tax strategy and financial planning.

Employers should also be aware of the potential risks associated with pre-tax contributions. For example, if an employee's health insurance premiums are paid with pre-tax dollars and the employee later receives a tax refund, the employer may be required to repay the pre-tax contributions. Additionally, pre-tax contributions may be subject to certain limits and restrictions, so employers need to ensure that they are in compliance with all applicable laws and regulations.

In conclusion, employer pre-tax contributions to health insurance can be a valuable tool for attracting and retaining employees, while also reducing payroll tax liabilities. However, employers need to carefully consider the implications and potential risks associated with pre-tax contributions to ensure that they are making informed decisions about their health insurance and tax strategies.

Mastering Employee Payroll Taxes: A Step-by-Step Guide for Employers

You may want to see also

![]()

IRS Regulations: Specific IRS rules and limits apply to pre-tax health insurance contributions

The IRS has established specific rules and limits regarding pre-tax health insurance contributions, which are crucial for both employers and employees to understand. One key regulation is the requirement that health insurance premiums must be paid with pre-tax dollars to qualify for tax advantages. This means that employees can deduct their health insurance premiums from their taxable income, reducing their overall tax liability. However, there are limits to these deductions, and exceeding these limits can result in additional taxes and penalties.

Another important IRS rule is the prohibition on using pre-tax dollars to pay for health insurance premiums if the employee is also receiving tax credits for health insurance through a government exchange. This is known as the "premium tax credit" rule, and it is designed to prevent double-dipping on tax benefits. Employees who are eligible for tax credits through a government exchange must use post-tax dollars to pay for their health insurance premiums if they want to receive the tax credit.

The IRS also has rules regarding the timing of pre-tax health insurance contributions. Employers must make pre-tax contributions to health insurance plans on behalf of their employees by the end of the calendar year in which the premiums are due. This means that employers cannot make pre-tax contributions for premiums that are due in a future year. Employees who make their own pre-tax contributions must also do so by the end of the calendar year in which the premiums are due.

In addition to these rules, the IRS has also established limits on the amount of pre-tax contributions that can be made to health insurance plans. These limits are based on the employee's age and the type of health insurance plan. For example, employees under the age of 65 can contribute up to $3,600 per year to a health savings account (HSA) on a pre-tax basis, while employees over the age of 65 can contribute up to $4,600 per year.

Understanding these IRS regulations is essential for both employers and employees to ensure compliance and maximize tax benefits. Employers should work with their tax advisors to ensure that their health insurance plans comply with IRS rules, and employees should consult with their tax advisors to determine the best way to make pre-tax contributions to their health insurance plans.

Understanding 401k Deferrals: Are They Subject to Payroll Taxes?

You may want to see also

![]()

Impact on Tax Brackets: Higher contributions can lower an employee's tax bracket, providing additional savings

Higher contributions to health insurance can indeed lower an employee's tax bracket, leading to additional savings. This is because the money contributed to health insurance premiums is often deducted from the employee's gross income before taxes are calculated. As a result, the taxable income is reduced, which can push the employee into a lower tax bracket.

For example, if an employee earns $50,000 per year and contributes $5,000 to their health insurance premiums, their taxable income would be reduced to $45,000. Depending on the tax brackets in their country or region, this could potentially lower their tax rate from 25% to 20%, resulting in significant savings.

It's important to note that the specific impact on tax brackets will vary depending on the individual's income level, the amount contributed to health insurance, and the tax laws in their jurisdiction. Employees should consult with a tax professional or use online tax calculators to determine the exact impact of their health insurance contributions on their tax bracket.

In addition to lowering the tax bracket, higher health insurance contributions can also lead to other benefits, such as reduced out-of-pocket expenses and improved health outcomes. By investing more in their health insurance, employees can potentially save money in the long run by avoiding costly medical bills and procedures.

Overall, understanding the impact of health insurance contributions on tax brackets is an important aspect of financial planning for employees. By making informed decisions about their health insurance premiums, employees can optimize their tax savings and improve their overall financial well-being.

Unlocking the Tax Benefits of Employee Bonuses: A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, in many cases, employee contributions to health insurance are considered pre-tax. This means that the money is deducted from your gross income before taxes are calculated, which can lower your taxable income and potentially reduce your tax liability.

Pre-tax health insurance contributions are typically made through payroll deductions. Your employer deducts the amount you've chosen to contribute from your paycheck before federal, state, and local taxes are withheld. This reduces your gross income, which in turn can lower your tax bracket and the amount of taxes you owe.

The primary benefit of pre-tax health insurance contributions is that they can reduce your taxable income, which may lead to lower taxes. Additionally, pre-tax contributions can make health insurance more affordable by spreading the cost over time through payroll deductions.

Yes, there are some limitations. For example, the amount you can contribute pre-tax may be limited by IRS regulations. Additionally, if you have a Health Savings Account (HSA) or a Flexible Spending Account (FSA), there may be specific rules about how these accounts interact with pre-tax health insurance contributions. It's important to check with your employer or a tax professional for details.