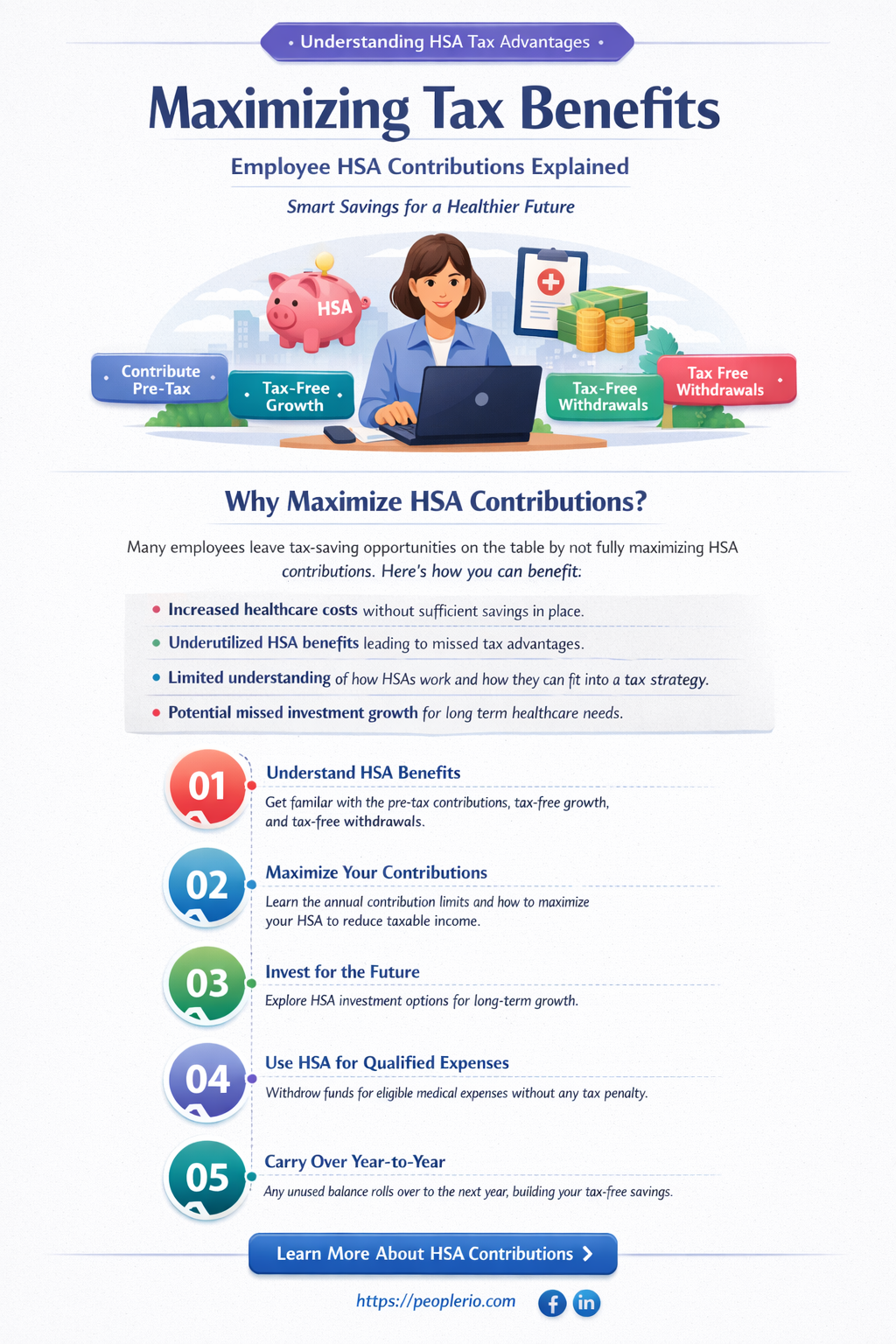

Employee contributions to a Health Savings Account (HSA) are indeed tax-deductible, offering a significant financial advantage for those who opt to save for medical expenses through this type of account. HSAs are designed to help individuals save money on healthcare costs by providing a tax-efficient way to set aside funds for qualified medical expenses. Contributions made by employees are deducted from their gross income, reducing their taxable income and, consequently, their tax liability. This benefit is particularly valuable as it allows individuals to lower their overall tax burden while simultaneously building a financial cushion for future healthcare needs.

| Characteristics | Values |

|---|---|

| Tax Deductibility | Yes, employee contributions to HSA are tax-deductible |

| Contribution Limits | $3,600 for individuals, $7,200 for families (2023 limits) |

| Eligibility | Must be enrolled in a qualified HSA-compatible health plan |

| Age Restrictions | No age restrictions for contributions |

| Withdrawal Rules | Can be withdrawn tax-free for qualified medical expenses |

| Investment Options | Often available, but specifics vary by HSA provider |

| Portability | HSA accounts are portable and can be carried from job to job |

| Required Documentation | May need to provide proof of medical expenses for withdrawals |

| Impact on Other Benefits | Does not affect Medicare or Medicaid eligibility |

| Employer Contributions | Employers can also contribute, but these are not tax-deductible for employees |

Explore related products

What You'll Learn

- Eligibility Criteria: Understand who can contribute to an HSA and the conditions they must meet

- Contribution Limits: Learn about the annual contribution limits set by the IRS for HSAs

- Tax Deduction Benefits: Explore how HSA contributions reduce taxable income and provide tax savings

- Qualified Expenses: Discover what types of medical expenses qualify for HSA withdrawals without penalty

- Impact on Other Benefits: Examine how HSA contributions may affect eligibility for other health benefits or subsidies

![]()

Eligibility Criteria: Understand who can contribute to an HSA and the conditions they must meet

To contribute to a Health Savings Account (HSA), an individual must meet specific eligibility criteria. Firstly, the person must be enrolled in a high-deductible health plan (HDHP) and not be enrolled in Medicare. The HDHP must meet certain IRS standards regarding deductibles and out-of-pocket maximums. Additionally, the individual cannot be claimed as a dependent on someone else's tax return.

The eligibility criteria also include age and employment status. Contributors must be under the age of 65, unless they are disabled. Employment status is crucial as well; individuals must be employed and not retired, with some exceptions for those who are self-employed or have certain types of income.

Furthermore, there are conditions related to the individual's health coverage. If a person has other health coverage, such as a flexible spending account (FSA) or a health reimbursement arrangement (HRA), they may not be eligible to contribute to an HSA. It's also important to note that individuals who are covered by a spouse's health plan may still be eligible to contribute to their own HSA, provided they meet the other criteria.

Understanding these eligibility criteria is essential for individuals who are considering contributing to an HSA. It's important to consult with a tax professional or a financial advisor to ensure that all conditions are met and to maximize the tax benefits associated with HSA contributions.

Mastering Employee Tax Filing: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![]()

Contribution Limits: Learn about the annual contribution limits set by the IRS for HSAs

The IRS sets annual contribution limits for Health Savings Accounts (HSAs) to ensure that individuals do not exceed a certain amount of tax-advantaged savings. For 2023, the contribution limit for individuals is $3,850, while for families, it is $7,750. These limits are subject to change annually based on inflation adjustments. It is crucial for HSA account holders to be aware of these limits to avoid any potential tax penalties or issues with their accounts.

One unique aspect of HSA contribution limits is the catch-up contribution provision. Individuals who are 55 years old or older are allowed to make an additional $1,000 catch-up contribution, on top of the regular contribution limits. This provision is designed to help older individuals save more for their healthcare expenses in retirement. It is important to note that this catch-up contribution is only available to those who are not enrolled in Medicare, as Medicare enrollment typically signifies that an individual is no longer eligible to contribute to an HSA.

Another important consideration regarding HSA contribution limits is the impact of employer contributions. If an employer contributes to an employee's HSA, those contributions are also subject to the annual limits. However, employer contributions do not count towards the employee's personal contribution limit. This means that an employee can still make their full personal contribution, even if their employer contributes to their HSA. It is essential for employees to coordinate with their employers to ensure that total contributions do not exceed the IRS limits.

In addition to the annual contribution limits, it is also important for HSA account holders to be aware of the rules regarding excess contributions. If an individual contributes more than the allowed limit, they may be subject to a 6% excise tax on the excess amount. This tax can be avoided by withdrawing the excess contributions before the end of the tax year; however, any earnings on the excess contributions will still be taxable. To prevent excess contributions, account holders should carefully monitor their contributions throughout the year and adjust their contributions as needed to stay within the IRS limits.

Understanding the IRS contribution limits for HSAs is essential for maximizing the tax benefits of these accounts while avoiding potential penalties. By staying informed about the limits and rules, individuals can make the most of their HSA contributions and ensure that they are saving effectively for their future healthcare expenses.

Maximize Your Savings: Understanding Pre-Tax Employee Stock Purchase Plans

You may want to see also

Explore related products

![Employee Warning Notice Forms Book: Track Disciplinary Actions and Employee Violations with Organized HR Write-Ups [A4]](https://m.media-amazon.com/images/I/612i0Jw94OL._AC_UY218_.jpg)

![]()

Tax Deduction Benefits: Explore how HSA contributions reduce taxable income and provide tax savings

HSA contributions offer a significant tax advantage by reducing taxable income. When employees contribute to their Health Savings Accounts, these contributions are deducted from their gross income before taxes are calculated. This lowers the overall taxable income, which in turn reduces the amount of federal and state taxes owed. For example, if an employee contributes $2,000 to their HSA in a year, their taxable income is reduced by $2,000, potentially saving them hundreds of dollars in taxes depending on their tax bracket.

The tax savings from HSA contributions can be particularly impactful for those in higher tax brackets. As the marginal tax rate increases, the value of each dollar contributed to an HSA also increases. For instance, an individual in the 32% tax bracket would save $640 in taxes with a $2,000 contribution, whereas someone in the 24% bracket would save $480. This makes HSA contributions an attractive tax-saving strategy for higher earners.

Moreover, HSA contributions are not subject to payroll taxes, such as Social Security and Medicare taxes. This further enhances the tax benefits, as employees can save an additional 7.65% on their contributions compared to other types of savings accounts. For example, on a $2,000 contribution, this would result in an extra $153 in savings.

The tax advantages of HSA contributions extend beyond the immediate reduction in taxable income. The funds within an HSA grow tax-free, meaning any investment gains or interest earned are not subject to taxation. This allows the account balance to grow more rapidly over time, providing a larger pool of funds for future healthcare expenses. Additionally, qualified medical expenses paid from an HSA are tax-free, further enhancing the overall tax benefits of these accounts.

In summary, HSA contributions offer a powerful tax-saving tool for employees. By reducing taxable income, avoiding payroll taxes, and allowing for tax-free growth and withdrawals for qualified expenses, HSAs provide a unique and valuable benefit that can significantly impact an individual's financial well-being.

Maximize Your Retirement Savings: Understanding Pre-Tax 401(k) Contributions

You may want to see also

Explore related products

$14.99 $25

$14.99 $25

![]()

Qualified Expenses: Discover what types of medical expenses qualify for HSA withdrawals without penalty

To determine if employee contributions to an HSA are tax-deductible, it's essential to understand the concept of qualified expenses. These are medical expenses that qualify for HSA withdrawals without penalty. Typically, qualified expenses include costs for medical care, such as doctor visits, hospital stays, and prescription medications. However, they can also encompass other health-related costs like dental and vision care, over-the-counter medications, and even certain wellness programs.

One crucial aspect to consider is that these expenses must be incurred by the HSA account holder or their dependents. Furthermore, the expenses must not be covered by another health plan or insurance. For instance, if an individual has a separate dental insurance plan, they cannot use their HSA funds to cover dental expenses.

It's also important to note that qualified expenses are not limited to immediate medical needs. HSA funds can be used for long-term care expenses, such as nursing home care or home health care services. Additionally, HSA withdrawals for qualified expenses are tax-free, which can provide significant savings over time.

When it comes to employee contributions to an HSA, these are generally tax-deductible, reducing the employee's taxable income. This can lead to lower federal and state tax liabilities. However, it's crucial to ensure that the contributions are within the annual limits set by the IRS. For 2023, the contribution limit for individuals is $3,850, while for families, it's $7,750.

In conclusion, understanding qualified expenses is key to maximizing the tax benefits of an HSA. By using HSA funds for qualified medical expenses, individuals can save on taxes and make the most of their health savings account.

Understanding Texas Taxation: Are Andrews Employee Exemptions Taxed?

You may want to see also

Explore related products

![]()

Impact on Other Benefits: Examine how HSA contributions may affect eligibility for other health benefits or subsidies

HSA contributions can have a significant impact on an individual's eligibility for other health benefits and subsidies. One key consideration is the effect on Medicaid eligibility. If an individual's income is close to the Medicaid eligibility threshold, contributing to an HSA could potentially push their income over the limit, disqualifying them from Medicaid benefits. This is because HSA contributions are generally considered income for Medicaid eligibility purposes.

Another important factor to consider is the interaction between HSA contributions and the Earned Income Tax Credit (EITC). The EITC is a refundable tax credit available to low-to-moderate-income individuals and families. HSA contributions can reduce an individual's taxable income, which may increase their EITC eligibility or the amount of the credit they receive. However, it's crucial to note that the EITC is subject to income limits, and contributing too much to an HSA could potentially disqualify an individual from the credit.

Additionally, HSA contributions can affect eligibility for the Children's Health Insurance Program (CHIP). CHIP provides health coverage to children in families with incomes too high to qualify for Medicaid but who cannot afford private insurance. If an individual's income is close to the CHIP eligibility threshold, contributing to an HSA could potentially disqualify their children from CHIP benefits.

It's also important to consider the impact of HSA contributions on Medicare benefits. While HSA contributions do not directly affect Medicare eligibility, they can impact the amount of Medicare premiums an individual pays. This is because Medicare premiums are based on an individual's income, and HSA contributions can reduce taxable income, potentially lowering premium costs.

In conclusion, while HSA contributions can offer significant tax advantages, it's essential to consider their impact on eligibility for other health benefits and subsidies. Individuals should carefully evaluate their specific situation and consult with a tax professional or healthcare advisor to ensure they are making informed decisions about their HSA contributions.

Maximizing Tax Benefits: Employee Health Insurance Contributions Explained

You may want to see also

Frequently asked questions

Yes, employee contributions to a Health Savings Account (HSA) are tax deductible.

The tax deduction limit for HSA contributions varies by year. For 2023, individuals can deduct up to $3,850, and families can deduct up to $7,750.

No, you cannot deduct HSA contributions if you are enrolled in Medicare.

Yes, employer contributions to an HSA are also tax deductible for the employee.

It depends on the state. Some states allow HSA contributions to be deducted from state taxes, while others do not. Check with your state's tax laws for more information.