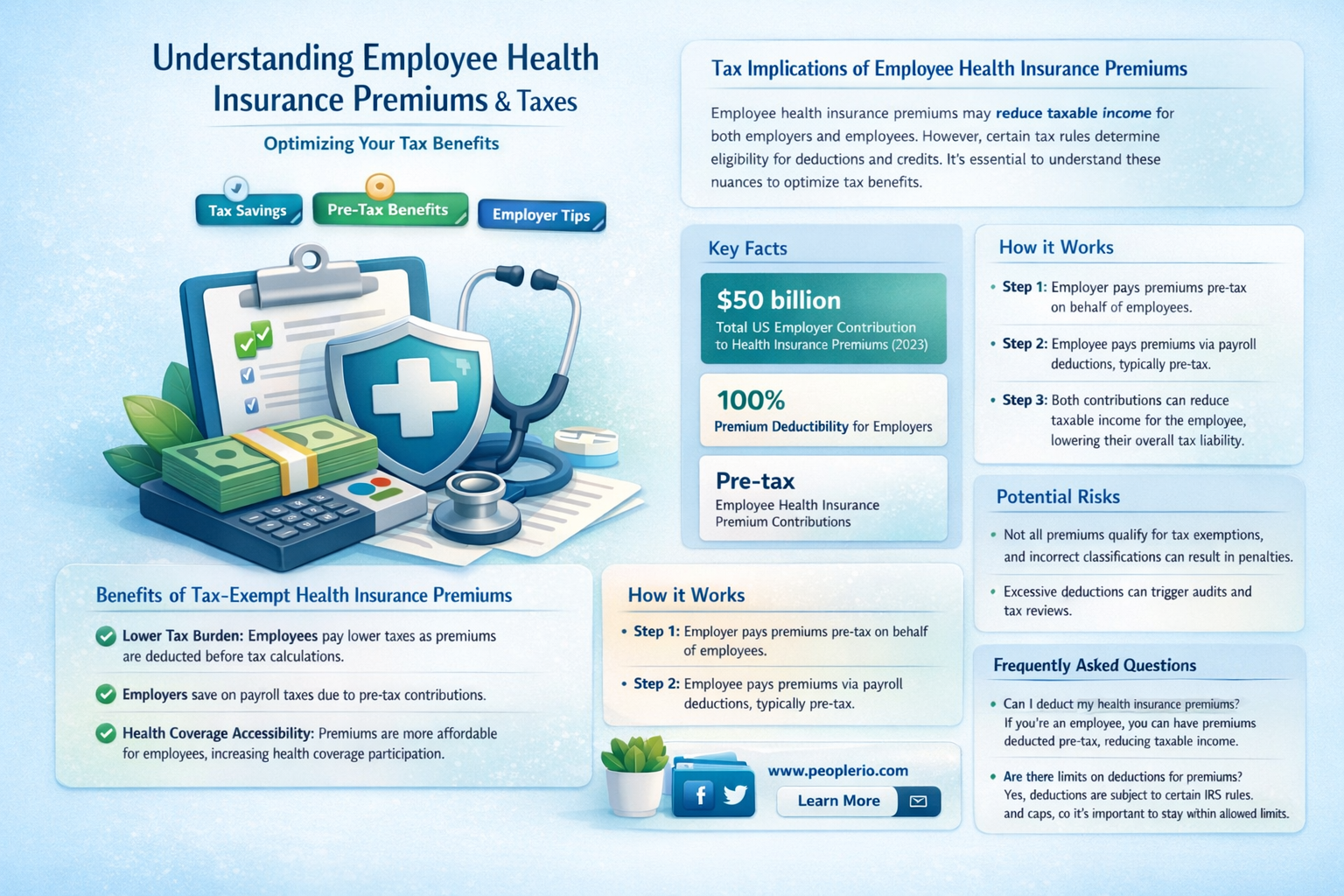

Employee health insurance premiums are a significant aspect of compensation for many workers, and understanding their tax implications is crucial. In the United States, health insurance premiums paid by employers on behalf of their employees are generally considered pre-tax expenses. This means that these premiums are deducted from the employee's gross income before taxes are calculated, reducing the overall taxable income. However, there are certain conditions and limitations to this rule, such as the requirement that the insurance plan must be a qualified health plan under IRS regulations. Additionally, the Affordable Care Act (ACA) has introduced specific guidelines regarding the tax treatment of health insurance premiums, particularly for small businesses. It's essential for both employers and employees to be aware of these tax rules to ensure compliance and optimize their financial planning.

| Characteristics | Values |

|---|---|

| Tax Status | Pre-tax |

| Applies To | Employee health insurance premiums |

| Benefit | Reduces taxable income |

| Limitations | May be subject to annual limits |

| Impact on Take-Home Pay | Increases take-home pay by reducing tax liability |

| Employer Contribution | Often employer-provided as part of benefits package |

| Employee Contribution | May require employee co-payment |

| Types of Plans | Applies to various types of health insurance plans |

| Legislation | Governed by tax laws and regulations |

| Example | If an employee pays $100/month for health insurance, this amount may be deducted from their taxable income |

Explore related products

What You'll Learn

- Definition of Pre-Tax Premiums: Understanding what pre-tax health insurance premiums mean for employees and employers

- Tax Benefits for Employers: Exploring how employers can benefit from offering pre-tax health insurance premiums

- Employee Savings: Discussing how employees can save money with pre-tax health insurance premiums

- IRS Regulations: Overview of IRS rules and regulations governing pre-tax health insurance premiums

- Impact on Take-Home Pay: Analyzing how pre-tax premiums affect an employee's take-home pay

![]()

Definition of Pre-Tax Premiums: Understanding what pre-tax health insurance premiums mean for employees and employers

Pre-tax health insurance premiums refer to the portion of an employee's health insurance costs that are deducted from their gross income before taxes are applied. This means that the employee does not pay income tax on the amount deducted for health insurance premiums. For example, if an employee's gross income is $50,000 per year and their health insurance premiums are $5,000 per year, the pre-tax deduction would reduce their taxable income to $45,000.

From an employer's perspective, offering pre-tax health insurance premiums can be a valuable benefit to attract and retain employees. It reduces the overall cost of health insurance for employees, making it more affordable and increasing the likelihood that they will enroll in the company's health insurance plan. Additionally, employers may also benefit from tax savings, as they can deduct the cost of health insurance premiums from their business expenses.

However, it's important to note that not all health insurance premiums are eligible for pre-tax deductions. The IRS has specific guidelines that must be followed, such as the requirement that the health insurance plan must be a qualified plan under Section 106 of the Internal Revenue Code. Additionally, the amount of pre-tax deductions may be limited based on the employee's income level and other factors.

In conclusion, understanding pre-tax health insurance premiums is crucial for both employees and employers. It can help employees make informed decisions about their health insurance coverage and reduce their overall costs, while also providing employers with a valuable tool to attract and retain top talent. By following the IRS guidelines and working with a qualified health insurance provider, both employees and employers can benefit from the advantages of pre-tax health insurance premiums.

Maximizing Tax Benefits: Understanding the Employee Retention Credit Impact

You may want to see also

Explore related products

![]()

Tax Benefits for Employers: Exploring how employers can benefit from offering pre-tax health insurance premiums

Offering pre-tax health insurance premiums is a strategic move for employers looking to enhance their financial efficiency and employee satisfaction. This approach allows employers to deduct the cost of health insurance premiums from their taxable income, resulting in significant tax savings. For instance, if an employer pays $10,000 in health insurance premiums, they can reduce their taxable income by the same amount, potentially saving thousands in taxes depending on their tax bracket.

From an employee perspective, pre-tax premiums can also lead to increased take-home pay. When health insurance costs are deducted pre-tax, employees pay less in federal, state, and local taxes. This can be a valuable benefit, especially for employees in higher tax brackets. For example, an employee earning $75,000 per year could save approximately $2,000 annually in taxes if their $5,000 health insurance premium is paid pre-tax.

Employers can further leverage this benefit by structuring their health insurance offerings to maximize tax advantages. This might include selecting plans that qualify for pre-tax treatment under IRS regulations or implementing flexible spending accounts (FSAs) that allow employees to pay for out-of-pocket health expenses with pre-tax dollars. By doing so, employers not only reduce their own tax liabilities but also provide a more attractive benefits package to their workforce.

Another key consideration is the impact of pre-tax health insurance premiums on overall compensation strategies. Employers may choose to offer pre-tax premiums as part of a broader effort to optimize their benefits packages and remain competitive in the job market. This can be particularly important in industries where talent is in high demand and employers need to differentiate themselves through their benefits offerings.

In conclusion, offering pre-tax health insurance premiums is a multifaceted strategy that can yield significant financial benefits for both employers and employees. By understanding the tax implications and structuring their benefits packages accordingly, employers can enhance their financial efficiency, improve employee satisfaction, and maintain a competitive edge in the marketplace.

Understanding California Disability Employee Tax: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Employee Savings: Discussing how employees can save money with pre-tax health insurance premiums

One of the most significant benefits of pre-tax health insurance premiums is the potential for substantial savings for employees. By deducting health insurance premiums from an employee's paycheck before taxes are calculated, the taxable income is reduced, leading to lower tax liabilities. This can result in hundreds or even thousands of dollars in savings annually, depending on the employee's income level and the cost of the health insurance plan.

To maximize these savings, employees should consider contributing the maximum allowable amount to their health savings accounts (HSAs) or flexible spending accounts (FSAs). These accounts allow employees to set aside pre-tax dollars for qualified medical expenses, further reducing their taxable income and increasing their overall savings. Additionally, employees should take advantage of any employer matching contributions to these accounts, as this is essentially free money that can be used to cover healthcare costs.

Another strategy for employees to save money with pre-tax health insurance premiums is to carefully select their health insurance plan during open enrollment periods. Employees should compare the costs and benefits of different plans, considering factors such as deductibles, copays, and out-of-pocket maximums. By choosing a plan that best meets their healthcare needs and budget, employees can minimize their overall healthcare expenses while still taking advantage of pre-tax premium deductions.

It's also important for employees to be aware of any changes to their health insurance plans or tax laws that may impact their savings. For example, changes to the Affordable Care Act or the introduction of new tax legislation could alter the way pre-tax health insurance premiums are treated. By staying informed and adjusting their contributions and plan selections accordingly, employees can continue to maximize their savings and make the most of their pre-tax health insurance benefits.

In conclusion, pre-tax health insurance premiums offer employees a valuable opportunity to save money on their healthcare costs. By understanding how these premiums work, maximizing their contributions to tax-advantaged accounts, carefully selecting their health insurance plans, and staying informed about changes to laws and regulations, employees can make the most of this benefit and achieve significant savings.

Tax-Free Employee Gifts: What Employers Need to Know

You may want to see also

Explore related products

![]()

IRS Regulations: Overview of IRS rules and regulations governing pre-tax health insurance premiums

The Internal Revenue Service (IRS) has established specific rules and regulations regarding the tax treatment of employee health insurance premiums. According to IRS guidelines, premiums paid by employers for employee health insurance are generally considered tax-deductible business expenses. This means that employers can deduct the cost of these premiums from their taxable income, reducing their overall tax liability.

For employees, the IRS rules state that health insurance premiums paid by their employers are not considered taxable income. This is a significant benefit for employees, as it allows them to receive health insurance coverage without having to pay taxes on the premiums. However, it's important to note that this tax-free treatment applies only to premiums paid for coverage under a qualified health plan.

Qualified health plans are those that meet certain IRS standards, such as providing minimum essential coverage and being offered through a health insurance exchange or directly by an insurer. Employers must also ensure that they are not discriminating in favor of highly compensated employees when offering health insurance benefits.

In addition to these general rules, the IRS has also established specific regulations for health savings accounts (HSAs) and health reimbursement arrangements (HRAs). These accounts allow employees to save money on a tax-free basis for qualified medical expenses, including health insurance premiums. Employers can contribute to these accounts on behalf of their employees, but must follow IRS guidelines to ensure that the contributions are not considered taxable income.

Overall, the IRS regulations governing pre-tax health insurance premiums are designed to provide tax benefits to both employers and employees. By understanding these rules, employers can take advantage of tax deductions and provide valuable benefits to their employees, while employees can receive tax-free health insurance coverage and save money on medical expenses through tax-advantaged accounts.

Understanding Employee Tax Deductions: A Comprehensive Guide for Workers

You may want to see also

Explore related products

![]()

Impact on Take-Home Pay: Analyzing how pre-tax premiums affect an employee's take-home pay

Analyzing the impact of pre-tax health insurance premiums on an employee's take-home pay reveals a significant financial consideration for both employers and employees. Pre-tax premiums are deducted from an employee's gross income before taxes are calculated, which can lead to a lower taxable income and, consequently, a higher take-home pay. This mechanism is a common practice in many countries, including the United States, where employer-sponsored health insurance is prevalent.

From an analytical perspective, the effect of pre-tax premiums on take-home pay can be quantified by comparing the net pay with and without the pre-tax deduction. For instance, if an employee's gross income is $50,000 per year and their health insurance premium is $5,000, the taxable income would be $45,000 if the premium is deducted pre-tax. Assuming a tax rate of 20%, the employee would save $1,000 in taxes ($5,000 premium x 20% tax rate). This results in a higher take-home pay compared to if the premium were deducted post-tax.

Instructively, employees can benefit from understanding how pre-tax premiums influence their overall compensation package. By recognizing the tax advantages, employees may be more inclined to participate in employer-sponsored health insurance plans, which can also lead to better health outcomes and increased job satisfaction. Employers, on the other hand, can use pre-tax premiums as a tool to attract and retain talent, as well as to promote a healthier workforce.

Persuasively, the argument in favor of pre-tax health insurance premiums is grounded in the principle of reducing the financial burden on employees. By lowering the taxable income, pre-tax premiums can help employees save money on taxes, which can be particularly beneficial for those in higher tax brackets. Additionally, pre-tax premiums can make health insurance more affordable for employees, encouraging them to maintain coverage and access necessary medical care.

Comparatively, pre-tax premiums can be contrasted with post-tax deductions, where the premium is subtracted from the employee's net pay after taxes have been calculated. In this scenario, the employee does not receive the same tax benefit, as the premium is not reducing their taxable income. This can result in a lower take-home pay and potentially discourage employees from participating in health insurance plans.

Descriptively, the landscape of employee health insurance is complex, with various factors influencing the cost and accessibility of coverage. Pre-tax premiums are just one aspect of this landscape, but they play a crucial role in shaping the financial incentives for both employees and employers. As healthcare costs continue to rise, understanding the impact of pre-tax premiums on take-home pay becomes increasingly important for making informed decisions about health insurance and compensation.

Maximize Your Take-Home Pay: Tax Reduction Strategies for W2 Employees

You may want to see also

Frequently asked questions

Yes, employee health insurance premiums are typically pre-tax. This means that the premiums are deducted from your gross income before taxes are calculated, reducing your taxable income.

Pre-tax health insurance premiums lower your taxable income, which in turn reduces the amount of taxes withheld from your paycheck. This can increase your take-home pay compared to if the premiums were taxed.

There is no specific limit on the amount that can be deducted pre-tax for health insurance premiums. However, there may be limits on the total amount of pre-tax deductions allowed, which can vary by employer or tax jurisdiction.

If you change your health insurance plan during the year, your employer will adjust the pre-tax deductions accordingly. You may need to provide updated information to ensure the correct amount is deducted.

Yes, pre-tax health insurance premiums are typically reported on your W-2 form in Box 12, with the code "DD" indicating the amount deducted. This information is used when filing your taxes to reconcile any differences between the pre-tax deductions and the actual tax liability.