Employee health plans are a crucial aspect of compensation packages offered by many employers. One of the key benefits of these plans is that they are often provided on a pre-tax basis. This means that the premiums paid by employees for their health insurance are deducted from their gross income before taxes are calculated. As a result, employees can lower their taxable income, which in turn reduces their overall tax liability. This pre-tax advantage makes employee health plans an attractive and cost-effective way for workers to access essential healthcare services while also maximizing their take-home pay.

| Characteristics | Values |

|---|---|

| Tax Status | Pre-tax |

| Employer Contribution | Often employer-funded |

| Employee Contribution | Employee pays a portion |

| Plan Types | Various (HMO, PPO, FSA, etc.) |

| Eligibility | Full-time employees |

| Enrollment | Automatic or elective |

| Premiums | Deducted from employee's gross pay |

| Benefits | Health, dental, vision, etc. |

| Administration | Managed by employer or third-party |

| Compliance | Must comply with federal and state laws |

Explore related products

What You'll Learn

- Definition of Pre-Tax Plans: Understand what pre-tax employee health plans are and how they work

- Benefits to Employees: Explore the advantages employees gain from pre-tax health plan contributions

- Employer Contributions: Learn about employer contributions to pre-tax health plans and their implications

- Tax Implications: Discover the tax benefits and potential drawbacks of pre-tax health plans for both employees and employers

- Comparison with Post-Tax Plans: Compare pre-tax health plans with post-tax plans to understand which might be more beneficial in different scenarios

![]()

Definition of Pre-Tax Plans: Understand what pre-tax employee health plans are and how they work

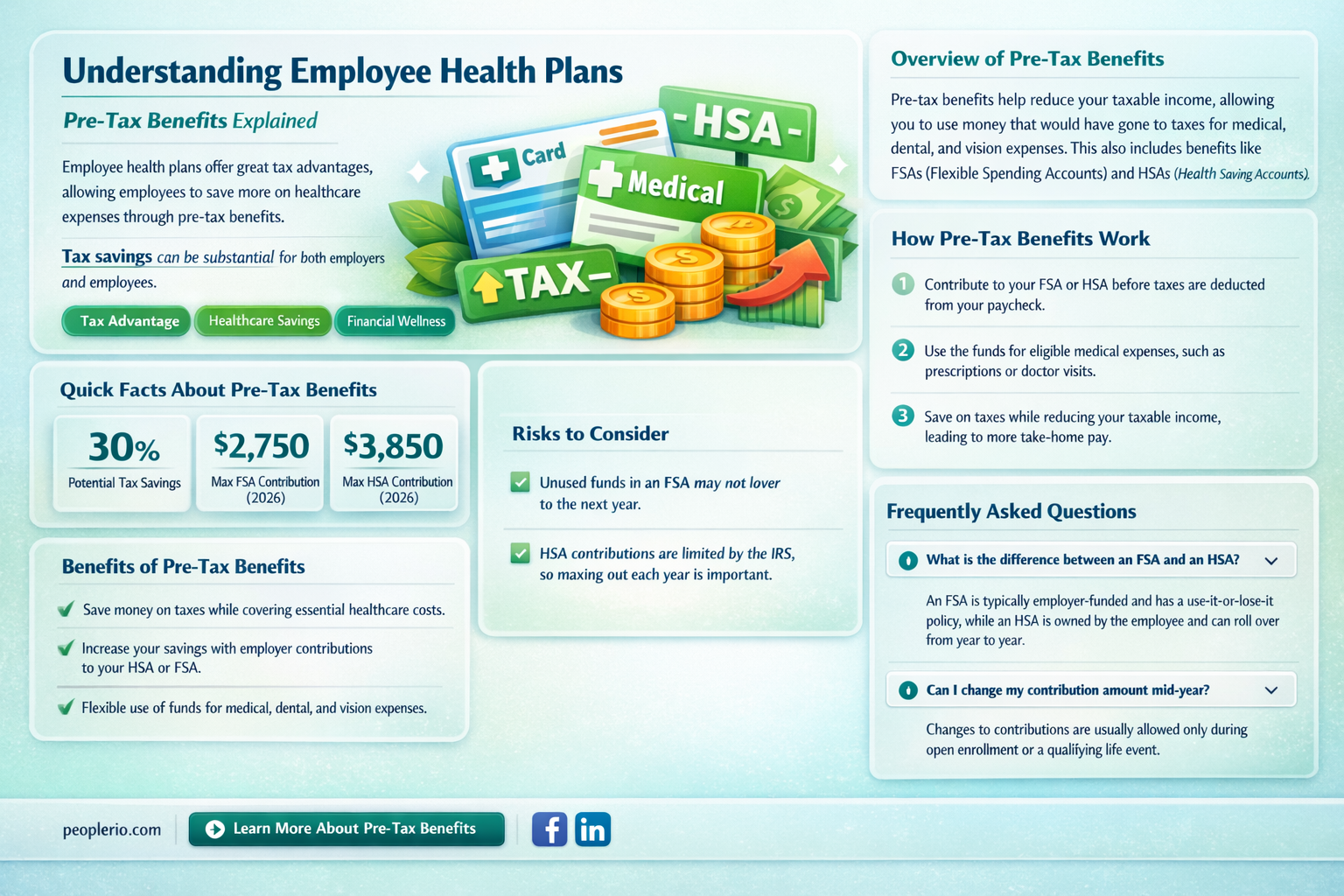

Pre-tax employee health plans are a type of benefit offered by employers to their employees, allowing them to pay for health insurance premiums with pre-tax dollars. This means that the money deducted from an employee's paycheck for health insurance is not subject to federal income tax, resulting in a lower taxable income and potentially a lower tax bill.

These plans work by setting aside a portion of an employee's salary in a pre-tax account, which is then used to pay for health insurance premiums. The employer typically contracts with a third-party administrator to manage the plan and ensure that the funds are used solely for health insurance purposes.

One of the key benefits of pre-tax employee health plans is that they can help to reduce the overall cost of health insurance for both employers and employees. By using pre-tax dollars, employees can save money on their tax bill, while employers can reduce their payroll tax liability.

However, it's important to note that pre-tax employee health plans are subject to certain regulations and limitations. For example, the amount of money that can be set aside in a pre-tax account is typically capped, and employees may be required to provide proof of health insurance coverage to their employer.

In conclusion, pre-tax employee health plans can be a valuable benefit for both employers and employees, offering a way to reduce the cost of health insurance and save money on taxes. However, it's important to understand the regulations and limitations surrounding these plans to ensure that they are used effectively and in compliance with the law.

Unraveling the Tax Deduction Mystery: Employee Entertainment Expenses Explained

You may want to see also

Explore related products

![]()

Benefits to Employees: Explore the advantages employees gain from pre-tax health plan contributions

Pre-tax health plan contributions offer significant financial benefits to employees. By deducting health insurance premiums from their gross income before taxes are calculated, employees can reduce their taxable income, leading to lower federal and state tax liabilities. This immediate tax savings can result in increased take-home pay, allowing employees to allocate more funds towards other essential expenses or savings goals.

Another advantage is the potential for long-term financial growth. Employees who invest their tax savings wisely, such as contributing to retirement accounts or other investment vehicles, can benefit from compound interest and capital gains over time. This can lead to a more secure financial future and improved overall wealth accumulation.

Furthermore, pre-tax health plan contributions can also reduce the financial burden of out-of-pocket medical expenses. Many health plans offer tax-advantaged accounts, such as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs), which allow employees to set aside pre-tax dollars for qualified medical expenses. This can help employees manage healthcare costs more effectively and avoid the need to dip into taxable savings or incur debt to cover unexpected medical bills.

In addition to these financial benefits, pre-tax health plan contributions can also promote employee well-being. By making health insurance more affordable, employees are more likely to enroll in and maintain coverage, which can lead to better access to preventive care and early treatment for health issues. This, in turn, can result in improved health outcomes and reduced absenteeism, ultimately benefiting both employees and employers.

Overall, pre-tax health plan contributions provide employees with a valuable financial advantage, enabling them to save on taxes, invest for the future, manage healthcare costs, and maintain their health and well-being. Employers who offer such benefits can also reap the rewards of a healthier, more productive workforce and increased employee satisfaction and loyalty.

Understanding AFLC Payments: Pre-Tax or Post-Tax?

You may want to see also

Explore related products

![Employee benefits survey : an MLR reader / U.S. Dept. of Labor, Bureau of Labor Statistics. 1990 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

$69.03 $125.68

![]()

Employer Contributions: Learn about employer contributions to pre-tax health plans and their implications

Employers play a significant role in the healthcare landscape by contributing to pre-tax health plans. These contributions are a crucial aspect of employee benefits packages and have several implications for both employers and employees. Understanding the dynamics of employer contributions can help employees make informed decisions about their healthcare options and financial planning.

One key implication of employer contributions to pre-tax health plans is the tax advantage it provides. By contributing to these plans on a pre-tax basis, employers can reduce their taxable income, which in turn lowers their tax liability. This can be a significant benefit for businesses looking to optimize their financial performance. Additionally, pre-tax contributions can also reduce the employee's taxable income, resulting in lower tax withholdings and potentially increasing their take-home pay.

Another important aspect to consider is the impact of employer contributions on employee morale and retention. Offering a comprehensive health benefits package, including pre-tax plans, can be a valuable tool for attracting and retaining top talent. Employees often view health benefits as a critical component of their overall compensation, and employers that provide robust health plans may be seen as more competitive in the job market.

Furthermore, employer contributions to pre-tax health plans can also influence employee health outcomes. By incentivizing participation in these plans, employers may encourage employees to prioritize their health and wellness. This can lead to a healthier workforce, which in turn can reduce healthcare costs and improve productivity.

In conclusion, employer contributions to pre-tax health plans are a multifaceted issue with implications for tax planning, employee morale, and overall health outcomes. Understanding these dynamics can help employees make informed decisions about their healthcare options and financial planning, while also providing employers with valuable insights into how to optimize their benefits packages and improve their bottom line.

California Employers: Obligations on Withholding State Income Tax

You may want to see also

Explore related products

![]()

Tax Implications: Discover the tax benefits and potential drawbacks of pre-tax health plans for both employees and employers

Pre-tax health plans offer significant tax advantages for both employees and employers. For employees, the primary benefit is the ability to pay for health insurance premiums with pre-tax dollars, reducing their taxable income. This can result in substantial savings, especially for those in higher tax brackets. For instance, an employee earning $50,000 per year who contributes $5,000 to a pre-tax health plan would only be taxed on $45,000, potentially saving them over $1,000 in taxes annually.

Employers also benefit from pre-tax health plans by reducing their payroll tax liabilities. Since the employer's contribution to the health plan is not subject to payroll taxes, such as Social Security and Medicare, companies can save a considerable amount on their tax obligations. Additionally, offering pre-tax health plans can be an attractive benefit for employees, aiding in recruitment and retention efforts.

However, there are potential drawbacks to consider. One significant concern is the impact on employees' take-home pay. While pre-tax contributions reduce taxable income, they also decrease the amount of money employees receive in their paychecks. This can be a disadvantage for employees who need to cover immediate expenses and may not fully appreciate the long-term tax benefits.

Another potential drawback is the administrative burden placed on employers. Managing pre-tax health plans requires careful record-keeping and compliance with IRS regulations, which can be time-consuming and costly. Employers must ensure that all contributions are properly documented and that the plans meet specific eligibility requirements to maintain their tax-advantaged status.

In conclusion, pre-tax health plans offer valuable tax benefits for both employees and employers, but they also come with potential drawbacks. Employees must weigh the immediate impact on their take-home pay against the long-term tax savings, while employers need to consider the administrative costs and compliance requirements. By carefully evaluating these factors, both parties can make informed decisions about whether pre-tax health plans are the right choice for their needs.

Understanding the Tax Implications of Employee Advances

You may want to see also

Explore related products

![]()

Comparison with Post-Tax Plans: Compare pre-tax health plans with post-tax plans to understand which might be more beneficial in different scenarios

Understanding the differences between pre-tax and post-tax health plans is crucial for making informed decisions about employee benefits. Pre-tax plans, such as Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs), allow employees to set aside money before taxes are deducted, reducing their taxable income. This can lead to significant savings, especially for those in higher tax brackets. For instance, if an employee contributes $2,000 to an HSA, they could potentially save around $700 in taxes, depending on their tax rate.

On the other hand, post-tax plans, like Health Reimbursement Arrangements (HRAs), are funded by employers and do not offer the same tax advantages. However, they can still be beneficial in certain scenarios. For example, HRAs can provide more predictable costs for employers and may be more suitable for companies that want to offer a specific level of health coverage without the administrative burden of managing pre-tax contributions.

When comparing pre-tax and post-tax plans, it's essential to consider the specific needs and circumstances of both the employer and the employees. Pre-tax plans are generally more advantageous for employees who want to save money on taxes and have more control over their health care spending. However, post-tax plans can be a better fit for employers who prioritize simplicity and predictability in their benefits offerings.

In conclusion, the choice between pre-tax and post-tax health plans depends on various factors, including tax implications, administrative considerations, and the desired level of employee involvement in health care decision-making. By carefully evaluating these aspects, employers can select the most suitable option for their organization and employees.

Unleashing Fitness Incentives: The Tax Benefits of Employee Gym Memberships

You may want to see also

Frequently asked questions

Yes, employee health plans are typically pre-tax. This means that the premiums paid for health insurance are deducted from an employee's gross income before taxes are calculated, reducing the taxable income.

Pre-tax health plans benefit employees by lowering their taxable income, which can result in a lower tax liability. This allows employees to save money on taxes while also making health insurance more affordable.

Yes, there are limits to the pre-tax contributions for health plans. These limits are set by the IRS and can vary depending on the type of plan and the employee's age. For example, in 2023, the maximum pre-tax contribution for a Health Savings Account (HSA) is $3,600 for individuals and $7,200 for families.

If an employee exceeds the pre-tax contribution limits, the excess amount may be subject to taxes. Additionally, the employee may face penalties for over-contributing to their health plan.

Not all types of health plans are eligible for pre-tax contributions. For example, premiums paid for health insurance through a health insurance marketplace (such as the Affordable Care Act marketplace) are not eligible for pre-tax contributions. However, premiums paid for employer-sponsored health plans, HSAs, and Flexible Spending Accounts (FSAs) are typically eligible for pre-tax contributions.