Employee life insurance premiums can be a significant benefit provided by employers, but understanding the tax implications is crucial for both employees and employers. In many jurisdictions, the tax deductibility of these premiums depends on specific conditions and regulations. Generally, if an employer pays for life insurance premiums on behalf of an employee, these payments may be considered taxable income to the employee. However, there are often exceptions and nuances based on the type of policy, the relationship between the employer and employee, and the tax laws of the relevant country or region. It's essential to consult with a tax professional or financial advisor to fully understand the tax implications of employee life insurance premiums in your specific situation.

| Characteristics | Values |

|---|---|

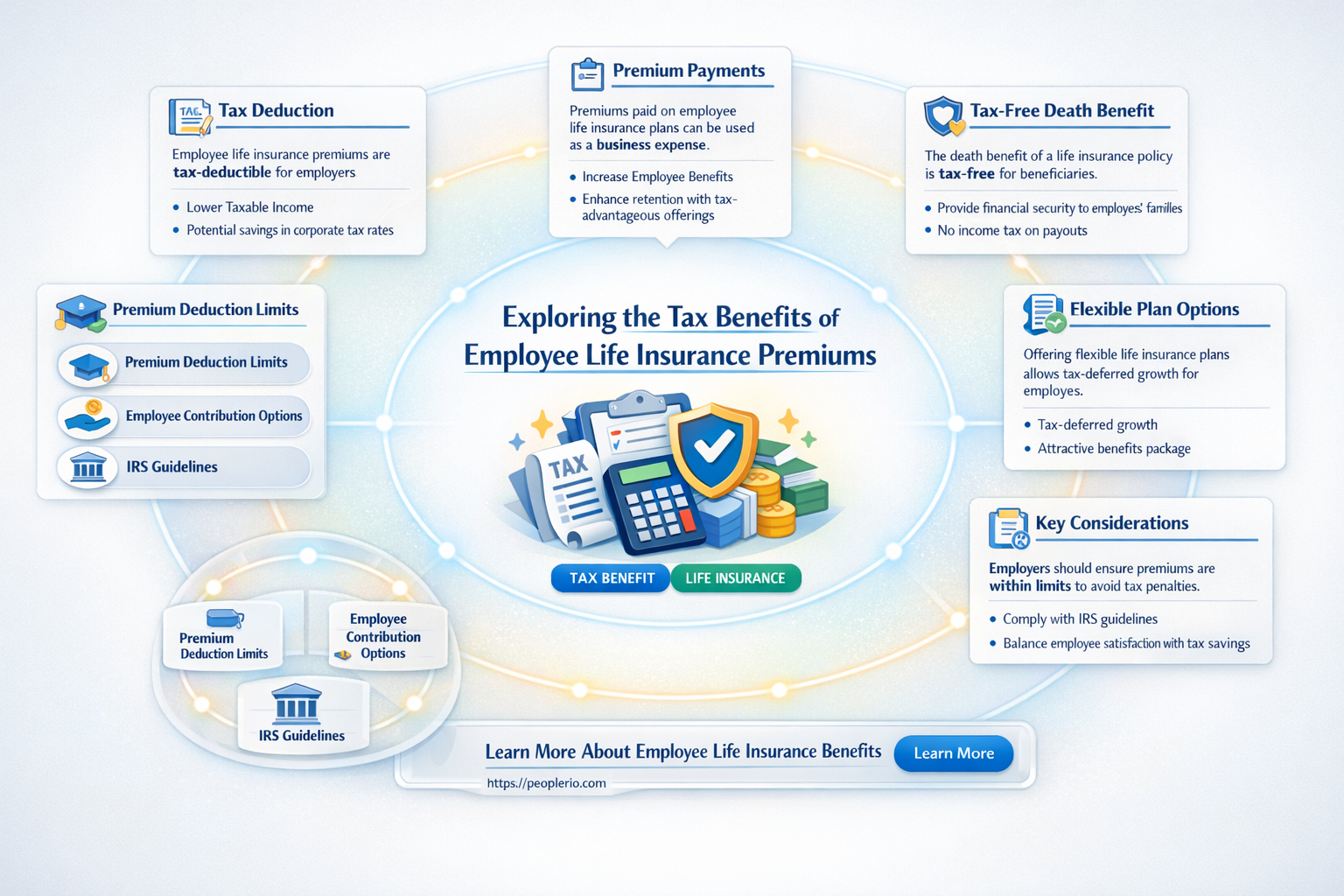

| Tax Deductibility | Employee life insurance premiums are generally not tax-deductible for the employee. However, they may be tax-deductible for the employer as a business expense. |

| Employer Contributions | If an employer pays for life insurance premiums, the premiums may be tax-deductible as a business expense. |

| Employee Contributions | If an employee pays for life insurance premiums through payroll deductions, the premiums are typically not tax-deductible. |

| Group Life Insurance | Group life insurance premiums paid by an employer for employees are usually tax-deductible for the employer. |

| Individual Life Insurance | Premiums paid by an individual for their own life insurance policy are not tax-deductible. |

| Key Person Life Insurance | Premiums paid by a business for key person life insurance may be tax-deductible as a business expense. |

| Tax Code Reference | The tax code reference for this information is typically found in the Internal Revenue Code (IRC) Section 605. |

| Consult a Tax Professional | It is recommended to consult a tax professional for specific guidance on tax deductibility of life insurance premiums. |

Explore related products

What You'll Learn

- General Rule: Employee life insurance premiums are generally not tax-deductible for the employee

- Exceptions: Certain circumstances, like employer-provided coverage or specific tax laws, may allow deductions

- Employer Deductions: Employers may deduct life insurance premiums paid for employees as a business expense

- Tax Credits: Employees might be eligible for tax credits if they pay life insurance premiums for dependents

- Consultation: It's advisable to consult a tax professional for personalized guidance on life insurance tax implications

![]()

General Rule: Employee life insurance premiums are generally not tax-deductible for the employee

Employee life insurance premiums are generally not tax-deductible for the employee. This means that if you're an employee who pays for life insurance through payroll deductions, you cannot deduct these premiums from your taxable income. The reason behind this general rule is that life insurance premiums are considered a personal expense, and as such, they do not qualify for tax deductions.

However, there are some exceptions to this rule. For instance, if the life insurance policy is part of a group plan provided by your employer, and your employer pays for the premiums, then these premiums may be tax-deductible for the employer as a business expense. Additionally, if you're self-employed, you may be able to deduct life insurance premiums as a business expense, provided that the policy is in the name of your business and not your personal name.

It's also important to note that while the premiums themselves may not be tax-deductible, the death benefit paid out by the life insurance policy is generally tax-free. This means that if you were to pass away, your beneficiaries would receive the death benefit without having to pay taxes on it.

In summary, while employee life insurance premiums are generally not tax-deductible for the employee, there are some exceptions to this rule, such as when the policy is part of a group plan provided by the employer or when the individual is self-employed. It's always a good idea to consult with a tax professional to understand the specific tax implications of your life insurance policy.

Are Employee HSA Contributions Subject to FICA Tax?

You may want to see also

Explore related products

![]()

Exceptions: Certain circumstances, like employer-provided coverage or specific tax laws, may allow deductions

While the general rule is that employee life insurance premiums are not tax deductible, there are certain exceptions to this rule. One such exception is when the employer provides the life insurance coverage. In this case, the premiums paid by the employer may be tax deductible as a business expense. This is because the employer is providing the coverage as a benefit to their employees, and the premiums are considered part of the cost of doing business.

Another exception to the rule is when the employee is self-employed. Self-employed individuals may be able to deduct their life insurance premiums as a business expense, as long as the policy is in the name of the business and not the individual. This is because the premiums are considered part of the cost of running the business, and self-employed individuals are allowed to deduct business expenses on their tax return.

Additionally, there are certain tax laws that may allow deductions for life insurance premiums. For example, in some countries, life insurance premiums may be tax deductible if the policy is a qualifying long-term care insurance policy. This is because long-term care insurance policies are designed to cover the costs of long-term care, which can be a significant financial burden for individuals and their families.

It's important to note that the rules and regulations surrounding tax deductions for life insurance premiums can be complex and vary depending on the country and specific circumstances. As such, it's always a good idea to consult with a tax professional or financial advisor to determine if you are eligible for any deductions.

Decoding Employee Tax IDs: A Comprehensive Guide for Employers

You may want to see also

Explore related products

![]()

Employer Deductions: Employers may deduct life insurance premiums paid for employees as a business expense

Employers may deduct life insurance premiums paid for employees as a business expense, which can be a significant benefit for both the employer and the employee. This deduction is allowed because life insurance premiums are considered a necessary business expense, as they help to protect the company from the financial impact of an employee's death.

To qualify for this deduction, the employer must be the policyholder and pay the premiums directly. The employee cannot deduct the premiums themselves, even if they are paying for the policy out of their own pocket. Additionally, the policy must be for the benefit of the employee or their beneficiaries, and not for the employer's own benefit.

The amount of the deduction is limited to the actual premiums paid, and cannot exceed the employee's taxable income. If the employer pays for a group life insurance policy that covers multiple employees, the deduction must be allocated among the employees based on their individual coverage amounts.

It's important to note that this deduction is only available for life insurance premiums paid for employees, and not for other types of insurance such as health or disability insurance. Employers should also be aware that this deduction may be subject to certain limitations and restrictions, depending on the specific tax laws and regulations in their jurisdiction.

In conclusion, employer deductions for life insurance premiums can be a valuable tax benefit for businesses, but it's essential to understand the rules and limitations in order to take advantage of this deduction properly. Employers should consult with a tax professional or financial advisor to ensure that they are complying with all applicable laws and regulations.

Unwrapping the Tax Implications of Employee Gifts: A Comprehensive Guide

You may want to see also

Explore related products

![Life and Health Insurance License Study Cards: Life Health Insurance Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

![]()

Tax Credits: Employees might be eligible for tax credits if they pay life insurance premiums for dependents

Employees who pay life insurance premiums for their dependents may be eligible for tax credits, which can help offset the cost of these premiums. This is an important consideration for many workers, as life insurance can provide financial security for their loved ones in the event of their passing. To qualify for these tax credits, employees must meet certain criteria, such as having a dependent who is a qualifying relative for tax purposes. Additionally, the life insurance policy must be a qualifying contract, which means it must meet specific requirements set forth by the tax code.

One of the key benefits of tax credits for life insurance premiums is that they can help make life insurance more affordable for employees. This is especially important for those who may not be able to afford life insurance otherwise. By reducing the cost of premiums, tax credits can help ensure that more employees have access to this important financial protection. Furthermore, tax credits can also help incentivize employees to purchase life insurance, which can be beneficial for both the employee and their employer.

To claim tax credits for life insurance premiums, employees will need to provide documentation to their employer, such as a copy of the life insurance policy and proof of payment of premiums. Employers will then need to verify this information and ensure that the employee meets the eligibility criteria. Once verified, the employer can provide the employee with a tax credit, which can be used to reduce their taxable income. This can result in a lower tax bill for the employee, which can help offset the cost of the life insurance premiums.

It is important to note that tax credits for life insurance premiums are subject to certain limits and restrictions. For example, there may be a cap on the amount of tax credits that an employee can claim in a given year. Additionally, tax credits may only be available for certain types of life insurance policies, such as term life insurance or whole life insurance. Employees should consult with their employer or a tax professional to determine their eligibility for tax credits and to understand the specific requirements and limitations.

In conclusion, tax credits for life insurance premiums can be a valuable benefit for employees, helping to make life insurance more affordable and accessible. By understanding the eligibility criteria and requirements, employees can take advantage of these tax credits to help protect their loved ones financially. Employers can also play a role in promoting the use of tax credits for life insurance premiums, which can help attract and retain top talent while also providing a valuable benefit to their employees.

Understanding Tax Deductions: A Guide to Employee Allowances

You may want to see also

Explore related products

$14.99 $25

![]()

Consultation: It's advisable to consult a tax professional for personalized guidance on life insurance tax implications

Navigating the complexities of life insurance tax implications can be challenging, which is why consulting a tax professional is highly advisable. A tax expert can provide personalized guidance tailored to your specific financial situation, helping you make informed decisions about your life insurance policy. They can assist in determining whether your employee life insurance premiums are tax-deductible and advise on the best strategies to minimize your tax liability.

One of the key benefits of consulting a tax professional is their ability to interpret the nuances of tax laws and regulations. They can help you understand the differences between term life insurance and whole life insurance, and how each type may impact your taxes. Additionally, they can guide you on how to properly report your life insurance premiums on your tax return to ensure compliance with IRS guidelines.

A tax professional can also help you avoid common mistakes that could lead to penalties or audits. For example, they can advise on the proper documentation required to substantiate your life insurance premiums and ensure that you are not overstating your deductions. Furthermore, they can provide insights into other tax-saving opportunities related to life insurance, such as utilizing a Health Savings Account (HSA) or Flexible Spending Account (FSA) to pay for premiums.

In addition to providing tax guidance, a tax professional can also offer financial planning advice. They can help you assess your overall financial goals and determine how life insurance fits into your broader financial strategy. This may include evaluating the adequacy of your life insurance coverage, exploring options for supplemental insurance, and advising on the potential use of life insurance as an investment vehicle.

Ultimately, consulting a tax professional can provide you with the confidence and clarity needed to make sound decisions about your life insurance and tax planning. Their expertise can help you optimize your financial situation, ensuring that you are well-prepared for the future while minimizing your tax burden.

Understanding the Tax Implications of Employee Advances

You may want to see also

Frequently asked questions

Yes, employee life insurance premiums are generally tax deductible for the employer as a business expense. This deduction helps reduce the employer's taxable income, providing a financial benefit for offering such benefits to employees.

Typically, if the employer pays for the life insurance premiums, the premiums are considered tax-free income for the employee. However, if the employee pays for the premiums themselves, they may be able to deduct them as a medical expense, subject to certain conditions and limits.

For group term life insurance policies, the premiums paid by the employer are usually tax deductible. The portion of the premiums that the employee pays may also be tax deductible as a medical expense, provided it meets the IRS's criteria for medical expenses.

Generally, life insurance payouts are tax-free to the beneficiary. This means that if an employee receives a payout from a life insurance policy, they will not have to pay taxes on the amount received, providing financial security without additional tax burdens.