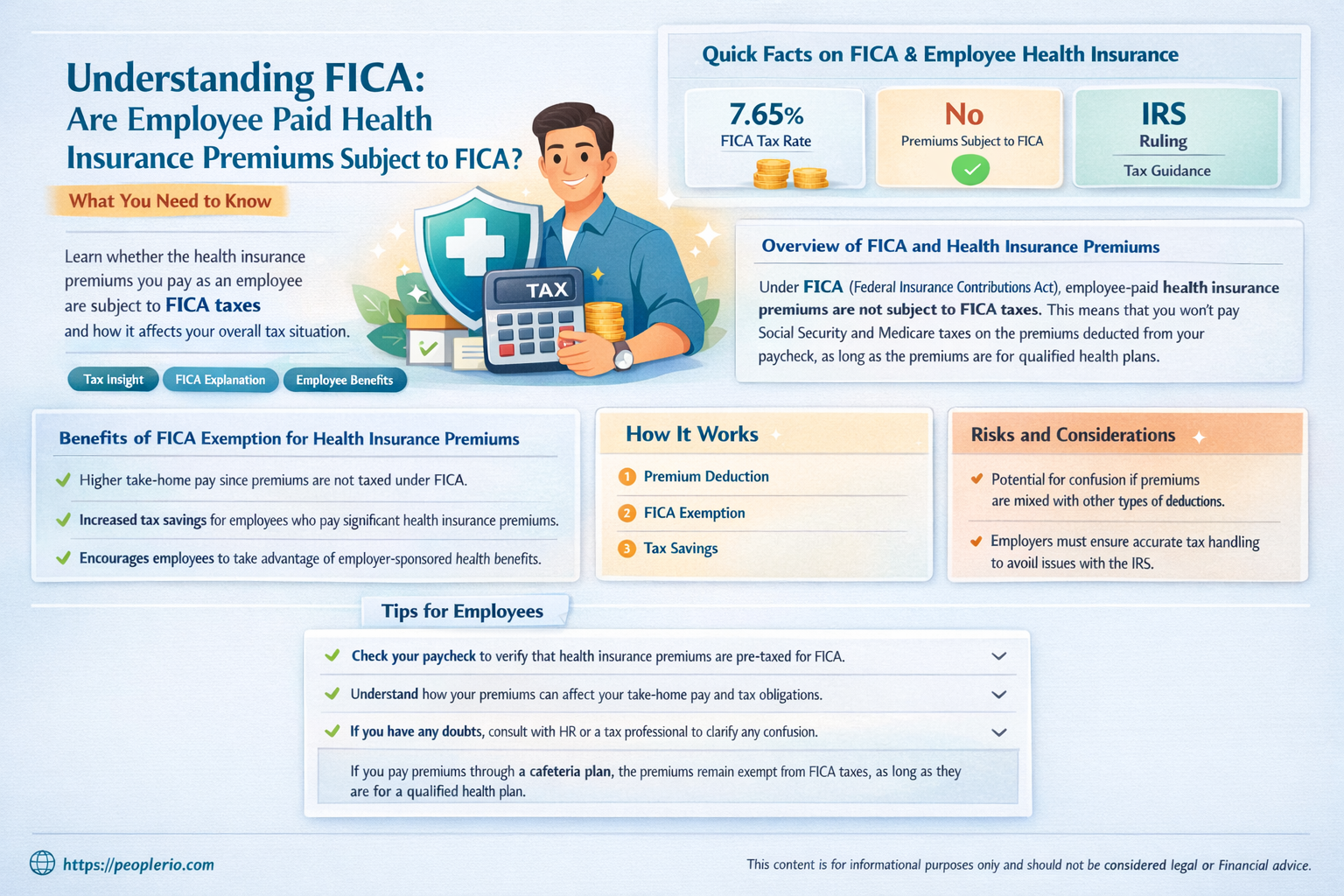

Employee-paid health insurance premiums are a common component of many workers' compensation packages in the United States. However, understanding the tax implications of these premiums can be complex. One key question that arises is whether these employee contributions are subject to Federal Insurance Contributions Act (FICA) taxes, which fund Social Security and Medicare. The answer to this question has significant implications for both employees and employers, affecting payroll taxes and overall financial planning. In general, employee-paid health insurance premiums are not considered taxable income under FICA, but there are specific conditions and exceptions that must be met to ensure compliance with IRS regulations.

Explore related products

What You'll Learn

- General Rule: Employee paid health insurance premiums are generally not subject to FICA taxes

- Exceptions: Certain exceptions apply, such as when premiums are paid for spouses or dependents

- Tax Implications: Understanding FICA tax implications can help employees make informed decisions about health insurance

- Employer Contributions: Employer contributions to health insurance premiums are typically subject to FICA taxes

- IRS Guidance: The IRS provides specific guidance on the tax treatment of health insurance premiums paid by employees

![]()

General Rule: Employee paid health insurance premiums are generally not subject to FICA taxes

Employee paid health insurance premiums are generally not subject to FICA taxes. This is a fundamental aspect of the U.S. tax code that impacts both employers and employees. FICA, which stands for Federal Insurance Contributions Act, encompasses Social Security and Medicare taxes. These taxes are typically withheld from an employee's wages and matched by the employer. However, when it comes to health insurance premiums paid by employees, these are usually considered non-taxable benefits.

The reasoning behind this general rule is rooted in the nature of health insurance itself. Health insurance premiums are seen as a form of compensation that provides future benefits, namely healthcare coverage. Since FICA taxes are levied on wages and salaries, and health insurance premiums are not considered part of an employee's wages, they are exempt from these taxes. This exemption is beneficial for employees as it reduces their overall tax burden, and for employers, it simplifies the payroll tax calculation process.

It's important to note that while employee paid health insurance premiums are generally not subject to FICA taxes, there are certain exceptions and nuances to this rule. For instance, if an employer contributes to an employee's health insurance premiums, those contributions may be subject to FICA taxes. Additionally, the Affordable Care Act (ACA) introduced new considerations regarding the tax treatment of health insurance premiums, particularly in relation to employer-sponsored health plans.

In practice, this general rule means that employees can expect their health insurance premiums to be deducted from their paychecks without the additional burden of FICA taxes. Employers, on the other hand, need to ensure that they are correctly classifying these premiums in their payroll systems to avoid any tax compliance issues. Understanding this rule is crucial for both parties to navigate the complexities of payroll taxes and employee benefits effectively.

Understanding Florida's Employee Health Care Act: Key Requirements Explained

You may want to see also

Explore related products

![]()

Exceptions: Certain exceptions apply, such as when premiums are paid for spouses or dependents

Under the Federal Insurance Contributions Act (FICA), employee-paid health insurance premiums are generally subject to taxation. However, there are specific exceptions to this rule that can provide relief to employees in certain circumstances. One such exception applies when employees pay health insurance premiums for their spouses or dependents. In these cases, the premiums are not considered taxable income under FICA, offering a financial advantage to employees who cover their family members' health insurance costs.

This exception is particularly beneficial for employees who have family members with significant health care needs or those who opt for family coverage plans. By excluding these premiums from FICA taxation, employees can effectively reduce their taxable income, leading to lower Social Security and Medicare taxes. This can result in substantial savings over time, especially for higher-income earners or those with multiple dependents.

To qualify for this exception, the health insurance plan must meet certain criteria. The plan must be a qualified health plan under the Internal Revenue Code, and the premiums must be paid directly by the employee. Additionally, the employee's spouse or dependent must be enrolled in the plan. It's important to note that this exception does not apply to health insurance premiums paid for other individuals, such as parents or siblings, unless they are considered dependents under tax law.

Employees should be aware of the documentation requirements to substantiate this exception. They may need to provide proof of their relationship to the spouse or dependent, as well as evidence of the health insurance coverage and premium payments. This can include marriage certificates, birth certificates, and health insurance invoices or receipts. By maintaining accurate records, employees can ensure they are in compliance with tax regulations and can take full advantage of this FICA exception.

In conclusion, the exception for employee-paid health insurance premiums for spouses or dependents can provide significant tax savings for employees. By understanding the eligibility criteria and documentation requirements, employees can make informed decisions about their health insurance coverage and maximize their tax benefits under FICA.

Understanding Employee Health: Key Factors for Workplace Well-Being

You may want to see also

Explore related products

![]()

Tax Implications: Understanding FICA tax implications can help employees make informed decisions about health insurance

Employee-paid health insurance premiums are generally not subject to FICA taxes, which include Social Security and Medicare taxes. This is because these premiums are considered tax-deductible expenses for the employee. However, there are some exceptions and nuances to this rule that employees should be aware of to make informed decisions about their health insurance.

For instance, if an employee's health insurance premiums are paid through a flexible spending account (FSA) or a health savings account (HSA), they are not subject to FICA taxes. This is because these accounts allow employees to pay for qualified medical expenses, including health insurance premiums, with pre-tax dollars. However, if an employee's employer pays for their health insurance premiums, these payments are considered taxable income and are subject to FICA taxes.

Another important consideration is the impact of FICA taxes on employees who are self-employed or have multiple jobs. Self-employed individuals are responsible for paying both the employer and employee portions of FICA taxes, which can significantly increase their tax liability. Employees with multiple jobs may also be subject to additional FICA taxes if their total earnings exceed the wage base limit for Social Security taxes.

Understanding the FICA tax implications of health insurance premiums can help employees make informed decisions about their coverage options. For example, an employee may choose to contribute to an FSA or HSA to reduce their taxable income and lower their FICA tax liability. Alternatively, an employee may opt to pay for their health insurance premiums out-of-pocket to avoid the potential tax consequences of employer-paid premiums.

In conclusion, while employee-paid health insurance premiums are generally not subject to FICA taxes, there are important exceptions and considerations that employees should be aware of. By understanding these tax implications, employees can make more informed decisions about their health insurance coverage and potentially reduce their tax liability.

Understanding Employee-Sponsored Health Insurance: Benefits, Costs, and Coverage Explained

You may want to see also

Explore related products

![]()

Employer Contributions: Employer contributions to health insurance premiums are typically subject to FICA taxes

Employer contributions to health insurance premiums are generally subject to FICA taxes, which include Social Security and Medicare taxes. This is because these contributions are considered a form of compensation to the employee, and thus are taxable under FICA. However, there are some exceptions to this rule. For example, if the employer is a tax-exempt organization, such as a non-profit or government entity, their contributions may not be subject to FICA taxes. Additionally, if the health insurance plan is a self-insured plan, the employer's contributions may not be taxable.

It's important to note that the FICA tax rate is 15.3% of the employee's gross wages, with the employer paying 6.2% for Social Security and 1.45% for Medicare, and the employee paying the remaining 7.65%. This means that if an employer contributes $10,000 to an employee's health insurance premiums, the employer would be responsible for paying $1,530 in FICA taxes on that contribution.

One way to avoid FICA taxes on employer contributions to health insurance premiums is to use a Health Savings Account (HSA) or a Flexible Spending Account (FSA). These accounts allow employees to set aside pre-tax dollars to pay for qualified medical expenses, including health insurance premiums. By using these accounts, employees can reduce their taxable income and thus lower their FICA tax liability.

Another option for employers is to offer a health insurance plan that is not subject to FICA taxes. For example, a self-insured plan, also known as a self-funded plan, is not subject to FICA taxes. In a self-insured plan, the employer assumes the financial risk for providing health care benefits to its employees. Instead of paying premiums to an insurance company, the employer pays for each out-of-pocket claim as they are incurred. This can be a more cost-effective option for employers, especially those with a large workforce.

In conclusion, while employer contributions to health insurance premiums are typically subject to FICA taxes, there are some exceptions and alternatives that can help employers and employees reduce their tax liability. It's important for employers to understand the tax implications of their health insurance contributions and to explore options that can help them save money while still providing quality health care benefits to their employees.

Understanding Employee Health Screening: Benefits, Process, and Importance

You may want to see also

Explore related products

![]()

IRS Guidance: The IRS provides specific guidance on the tax treatment of health insurance premiums paid by employees

The Internal Revenue Service (IRS) provides specific guidance on the tax treatment of health insurance premiums paid by employees. According to the IRS, employee-paid health insurance premiums are generally not subject to Federal Insurance Contributions Act (FICA) taxes. FICA taxes, which include Social Security and Medicare taxes, are typically withheld from employees' wages and paid by both employees and employers. However, the IRS has issued guidance that clarifies certain exceptions and conditions under which employee-paid health insurance premiums may be subject to FICA taxes.

One notable exception is when an employer reimburses an employee for health insurance premiums. In this case, the reimbursement is considered taxable income and is subject to FICA taxes. Additionally, if an employee pays health insurance premiums with pre-tax dollars from a flexible spending account (FSA) or a health savings account (HSA), the premiums are not subject to FICA taxes. However, if the employee pays the premiums with after-tax dollars, they may be able to deduct the premiums on their federal income tax return, but the premiums are still not subject to FICA taxes.

The IRS guidance also addresses the tax treatment of health insurance premiums paid by employees under a cafeteria plan. Under a cafeteria plan, employees can choose from a variety of benefits, including health insurance, and pay for them with pre-tax dollars. The IRS has ruled that health insurance premiums paid under a cafeteria plan are not subject to FICA taxes, as long as the plan meets certain requirements.

In summary, the IRS provides specific guidance on the tax treatment of health insurance premiums paid by employees. Generally, employee-paid health insurance premiums are not subject to FICA taxes, but there are certain exceptions and conditions that may apply. Employers and employees should consult the IRS guidance for more information on the tax treatment of health insurance premiums.

Are Employee Health Insurance Contributions Taxable? Key Facts Explained

You may want to see also

Frequently asked questions

Yes, employee paid health insurance premiums are subject to FICA taxes. FICA, which stands for Federal Insurance Contributions Act, requires employers to withhold taxes from employees' wages to fund Social Security and Medicare. Health insurance premiums paid by employees are considered part of their wages for FICA purposes.

FICA taxes on employee health insurance premiums are calculated based on the total premium amount. The employer is responsible for withholding the applicable FICA tax rate, which is currently 7.65% (6.2% for Social Security and 1.45% for Medicare), from the employee's wages. This withholding is in addition to any other FICA taxes withheld from the employee's regular wages.

There are some exceptions and special rules for FICA taxes on employee health insurance premiums. For example, premiums paid for certain types of health coverage, such as long-term care insurance or health savings accounts, may not be subject to FICA taxes. Additionally, there are rules regarding the timing of FICA tax withholding and reporting for health insurance premiums paid by employees. Employers should consult with a tax professional or refer to IRS guidance for more information on these exceptions and rules.

![NatureWise Curcumin Turmeric 2250mg - 95% Curcuminoids & BioPerine Black Pepper Extract for Advanced Absorption - Daily Joint and Immune Health Support - Vegan, Non-GMO, 180 Count[60-Day Supply]](https://m.media-amazon.com/images/I/714UFxWRUFL._AC_UL320_.jpg)