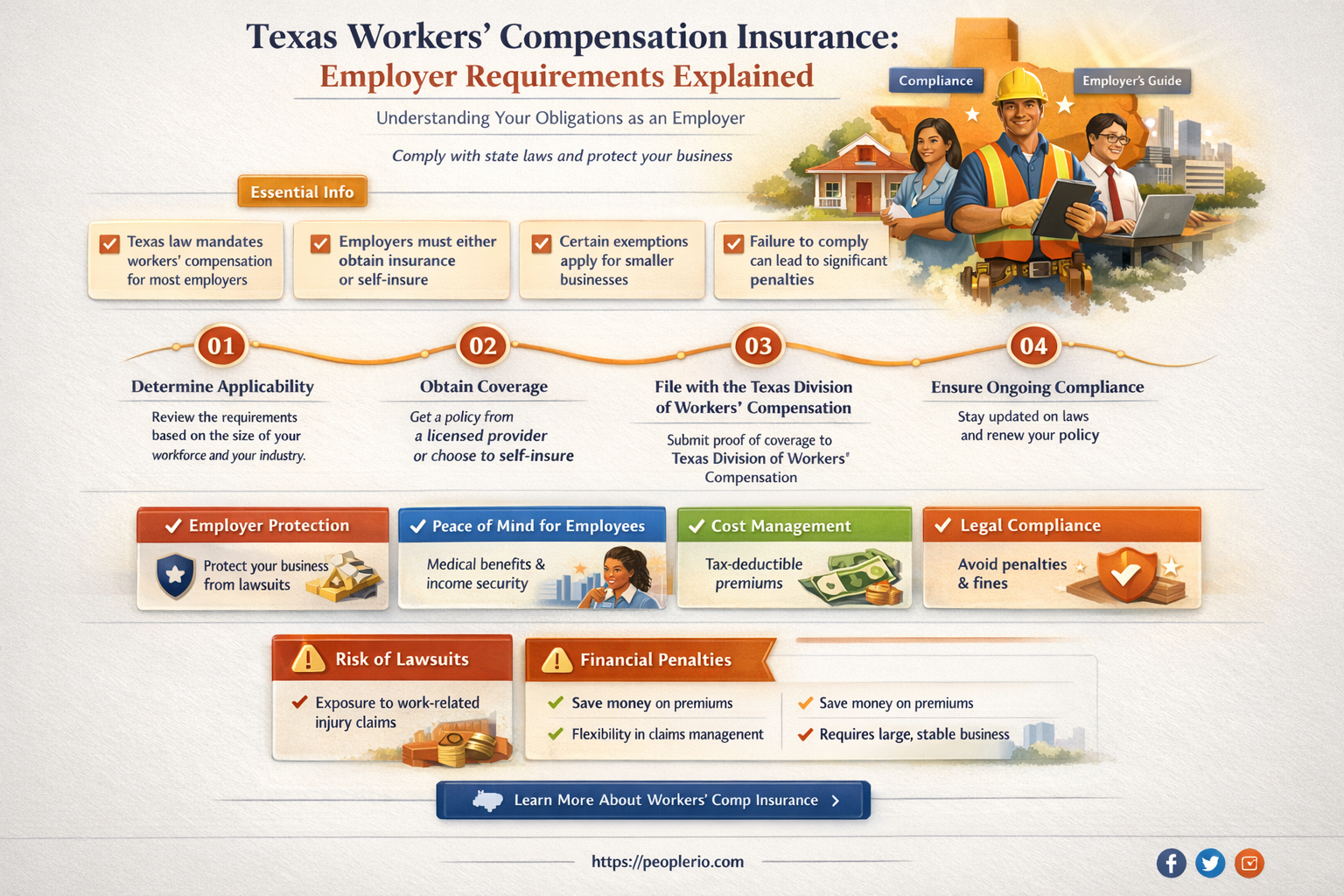

In the state of Texas, workers' compensation insurance is not mandatory for all employers. However, there are specific requirements and exceptions that businesses must be aware of. Employers with five or more employees are generally required to carry workers' compensation insurance, but there are some exemptions for certain industries and types of workers. For instance, employers in the construction industry with fewer than 10 employees may opt out of carrying workers' compensation insurance. Additionally, certain types of workers, such as independent contractors and some agricultural workers, may not be covered under workers' compensation. It is crucial for Texas employers to understand these regulations to ensure compliance and provide adequate protection for their employees.

| Characteristics | Values |

|---|---|

| Requirement | Yes, employers in Texas are generally required to have workers' compensation insurance. |

| Exceptions | Certain employers, such as those with fewer than 5 employees or those in specific industries, may be exempt. |

| Coverage | Workers' compensation insurance covers work-related injuries and illnesses, providing medical benefits and wage replacement. |

| Compliance | Employers must display a workers' compensation notice in their workplace and provide employees with information about their rights and benefits. |

| Penalties | Failure to carry workers' compensation insurance can result in fines and legal action against the employer. |

| Administration | The Texas Department of Insurance, Division of Workers' Compensation, oversees the workers' compensation system in Texas. |

Explore related products

What You'll Learn

- Legal Requirements: Texas law mandates workers' compensation insurance for employers with five or more employees

- Exceptions: Certain employers, like those in the construction industry, may be exempt from carrying workers' compensation insurance

- Consequences of Non-Compliance: Employers who fail to carry required insurance may face penalties, including fines and legal action

- Benefits Coverage: Workers' compensation insurance covers medical expenses, lost wages, and other benefits for injured employees

- Alternative Options: Employers may choose to self-insure or purchase alternative coverage, but must meet specific requirements

![]()

Legal Requirements: Texas law mandates workers' compensation insurance for employers with five or more employees

Texas law explicitly mandates that employers with five or more employees must carry workers' compensation insurance. This requirement is a critical aspect of employment law in the state, designed to protect workers who suffer job-related injuries or illnesses. Employers who fail to comply with this mandate may face significant legal and financial repercussions, including penalties and potential lawsuits from injured employees.

The legal framework for workers' compensation in Texas is governed by the Texas Workers' Compensation Act, which outlines the responsibilities of both employers and employees. Under this act, employers are required to provide workers' compensation coverage to their employees, which includes medical benefits, income replacement, and death benefits in certain cases. This coverage is intended to ensure that employees receive prompt medical attention and financial support if they are unable to work due to a work-related injury or illness.

One unique aspect of Texas workers' compensation law is the "opt-out" provision, which allows certain employers to exempt themselves from the state's workers' compensation system. However, this option is only available to employers who meet specific criteria and who provide alternative coverage to their employees. Employers who opt out of the state system must still provide medical benefits and income replacement to their injured employees, albeit through a private insurance plan or other means.

In addition to the legal requirements, there are practical considerations for employers when it comes to workers' compensation insurance. For example, employers must ensure that their insurance policies are up-to-date and provide adequate coverage for their employees. They must also be aware of the claims process and be prepared to handle potential disputes that may arise from workers' compensation claims.

Overall, the legal requirements for workers' compensation insurance in Texas are clear and stringent. Employers who fail to comply with these requirements may face serious consequences, both legally and financially. Therefore, it is essential for employers to understand their obligations under Texas law and to take steps to ensure that they are in compliance with these requirements.

Protecting Your Business: The Importance of Workers' Compensation Insurance

You may want to see also

Explore related products

![]()

Exceptions: Certain employers, like those in the construction industry, may be exempt from carrying workers' compensation insurance

In Texas, while most employers are mandated to carry workers' compensation insurance, there are notable exceptions. One such exemption applies to employers in the construction industry. This sector, characterized by its high-risk nature and the prevalence of independent contractors, operates under different rules compared to other industries.

The rationale behind this exemption stems from the unique operational dynamics of the construction industry. Many construction workers are classified as independent contractors rather than employees, which alters the employer's legal obligations. Independent contractors are typically responsible for their own insurance coverage, thereby reducing the employer's liability.

However, this exemption is not absolute. Construction employers may still be required to carry workers' compensation insurance if they meet certain criteria, such as employing a significant number of workers or engaging in specific types of construction projects. Additionally, some construction workers may be considered employees under Texas law, depending on factors such as the level of control exerted by the employer and the nature of the work performed.

Employers in the construction industry must carefully evaluate their operations to determine whether they are exempt from workers' compensation insurance requirements. This involves assessing the classification of their workers, the scope of their projects, and any applicable legal exceptions. Failure to comply with these regulations can result in significant legal and financial consequences, including penalties and potential lawsuits.

In conclusion, while the construction industry in Texas generally enjoys an exemption from workers' compensation insurance requirements, this exemption is subject to specific conditions and limitations. Employers must remain vigilant and ensure they understand and comply with the relevant laws and regulations to avoid potential legal issues.

Understanding Workers' Compensation Insurance: A Guide for Employers

You may want to see also

![]()

Consequences of Non-Compliance: Employers who fail to carry required insurance may face penalties, including fines and legal action

Employers in Texas who neglect to secure the mandated workers' compensation insurance may encounter severe repercussions. The state's regulatory framework imposes stringent penalties on non-compliant businesses, aiming to ensure that workers are protected in the event of job-related injuries or illnesses. These penalties can include substantial fines, which may be levied on a daily basis until the employer secures the required coverage. Additionally, legal action may be initiated against the employer, potentially leading to further financial liabilities and reputational damage.

The consequences of non-compliance extend beyond financial penalties. Employers may also face operational disruptions, as uninsured businesses may be forced to cease operations until they obtain the necessary insurance. This can lead to lost productivity, decreased revenue, and potential legal battles with employees who may have been injured on the job. Furthermore, uninsured employers may be held personally liable for medical expenses and lost wages of injured employees, which can have a devastating impact on both the business and the employer's personal assets.

To mitigate these risks, employers must take proactive steps to ensure compliance with Texas workers' compensation laws. This includes regularly reviewing and updating their insurance policies to reflect changes in the law or their business operations. Employers should also maintain accurate records of their insurance coverage and employee injuries, as these documents may be required in the event of an audit or legal action. By prioritizing compliance, employers can protect their businesses from the severe consequences of non-compliance and ensure that their employees are safeguarded in the event of workplace accidents.

Understanding Workers' Compensation Insurance Costs: A Comprehensive Guide

You may want to see also

![]()

Benefits Coverage: Workers' compensation insurance covers medical expenses, lost wages, and other benefits for injured employees

Workers' compensation insurance in Texas is designed to provide a safety net for employees who suffer work-related injuries or illnesses. One of the primary benefits of this coverage is that it helps to ensure injured workers receive prompt medical attention without the burden of out-of-pocket expenses. This can include everything from emergency care and hospital stays to rehabilitation services and prescription medications. By covering these costs, workers' compensation insurance helps to alleviate the financial stress that can accompany a workplace injury, allowing employees to focus on their recovery.

In addition to medical expenses, workers' compensation insurance in Texas also provides coverage for lost wages. If an employee is unable to work due to a work-related injury or illness, they may be eligible to receive a portion of their regular wages through workers' compensation benefits. This can help to mitigate the financial impact of being out of work and ensure that injured employees can maintain some level of financial stability during their recovery period.

Beyond medical expenses and lost wages, workers' compensation insurance in Texas may also cover other benefits such as vocational rehabilitation and death benefits. Vocational rehabilitation services can help injured employees regain the skills and abilities needed to return to work or transition to a new occupation if their injury prevents them from performing their previous job duties. Death benefits, on the other hand, provide financial support to the dependents of employees who lose their lives as a result of a work-related injury or illness.

It's important to note that the specific benefits and coverage limits can vary depending on the employer's insurance policy and the circumstances of the claim. However, the overarching goal of workers' compensation insurance is to provide comprehensive support to injured employees, helping them to recover physically, financially, and professionally.

Employers in Texas are generally required to carry workers' compensation insurance if they have four or more employees, with some exceptions for certain industries and business types. Failure to maintain the required coverage can result in penalties and legal consequences. By understanding the benefits and requirements of workers' compensation insurance, both employers and employees can better navigate the complexities of workplace injuries and ensure that everyone is protected.

Securing Your Future: A Guide to Obtaining Disability Insurance

You may want to see also

![]()

Alternative Options: Employers may choose to self-insure or purchase alternative coverage, but must meet specific requirements

In Texas, while workers' compensation insurance is not mandated by state law, employers still have a responsibility to provide some form of coverage for work-related injuries or illnesses. This is where alternative options come into play. Employers may choose to self-insure, which means they assume the financial risk for providing workers' compensation benefits directly, without purchasing insurance from a third-party carrier. However, this option requires the employer to have sufficient financial resources to cover potential claims and to comply with state regulations regarding self-insurance.

Another alternative is for employers to purchase alternative coverage, such as a private insurance policy or a group health insurance plan that includes workers' compensation benefits. This option allows employers to transfer the financial risk to an insurance carrier while still providing coverage for their employees. However, employers must ensure that the alternative coverage meets the specific requirements set forth by the Texas Department of Insurance, Division of Workers' Compensation (TDI-DWC).

One of the key requirements for alternative coverage is that it must provide benefits that are at least equivalent to those provided under the Texas Workers' Compensation Act. This includes medical benefits, income benefits, and death benefits. Employers must also file a Form DWC-7 with the TDI-DWC to notify them of their intent to provide alternative coverage. Failure to meet these requirements can result in penalties and legal consequences for the employer.

Employers who choose to self-insure or purchase alternative coverage should carefully consider the potential risks and benefits of each option. Self-insurance can be a cost-effective option for large employers with sufficient financial resources, but it also exposes them to greater financial risk in the event of a large claim. Alternative coverage can provide more predictable costs, but employers must ensure that the policy meets the specific requirements of Texas law.

In conclusion, while employers in Texas are not required to have workers' compensation insurance, they are still obligated to provide some form of coverage for work-related injuries or illnesses. Alternative options, such as self-insurance or purchasing alternative coverage, can be viable choices for employers, but they must meet specific requirements to ensure compliance with state law and to provide adequate protection for their employees.

Understanding Workers' Compensation Insurance: A Mandate for Employers?

You may want to see also

Frequently asked questions

No, Texas is a non-mandatory state for workers' compensation insurance, meaning employers are not legally required to carry it.

There are a few exceptions. Employers in the construction industry with one or more employees must carry workers' compensation insurance. Additionally, certain public entities and political subdivisions may be required to have workers' compensation coverage.

Employers who opt out of workers' compensation insurance may face increased financial risks. They could be held personally liable for work-related injuries or illnesses, which could lead to costly lawsuits and settlements.

Employees in Texas may face challenges if they are injured on the job and their employer does not have workers' compensation insurance. They may need to rely on their own health insurance or seek legal action against their employer to cover medical expenses and lost wages.

Employers who want to provide some form of coverage for work-related injuries can consider alternative options such as occupational injury benefit plans or private insurance policies. These plans may offer more flexibility and cost savings compared to traditional workers' compensation insurance.