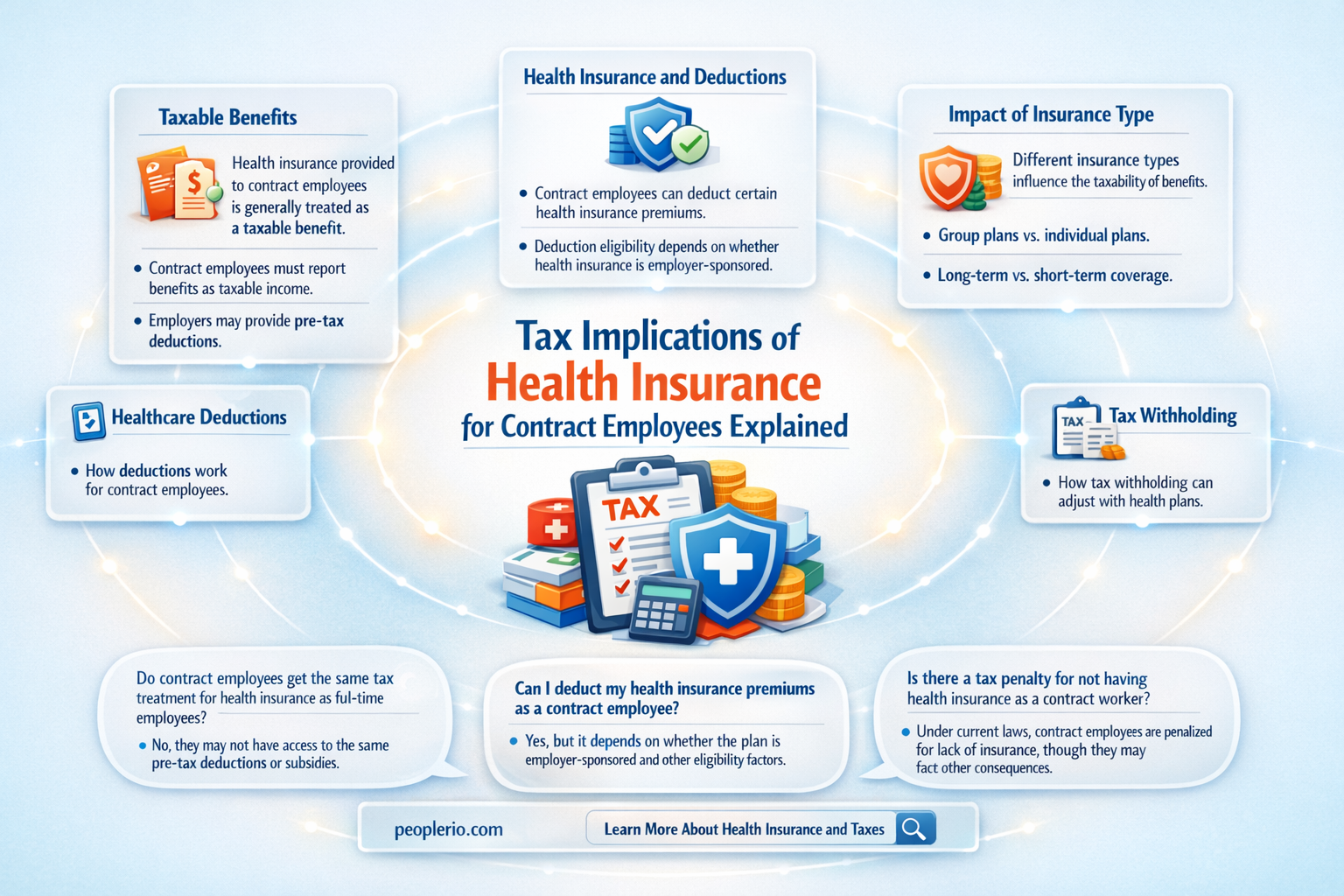

Health insurance payments made to a contract employee can have tax implications that vary depending on the specific circumstances and jurisdiction. Generally, if an employer provides health insurance to a contract employee, the premiums paid may be considered taxable income to the employee. This is because such payments can be viewed as a form of compensation. However, there are exceptions and nuances to this rule. For instance, if the contract employee is considered an independent contractor rather than an employee, the tax treatment might differ. Additionally, certain tax laws and regulations, such as those related to the Affordable Care Act in the United States, can impact how these payments are taxed. It's crucial for both employers and contract employees to understand these tax implications to ensure compliance with tax laws and to make informed decisions regarding health insurance coverage.

| Characteristics | Values |

|---|---|

| Taxability | Health insurance payments to a contract employee are generally taxable |

| Exceptions | Certain exceptions may apply, such as if the payments are made under a group health plan |

| Reporting | The payments may need to be reported on the contract employee's W-2 form |

| Withholding | Taxes may need to be withheld from the payments, depending on the specific circumstances |

| State laws | State laws may vary, so it's important to check the specific rules in the relevant jurisdiction |

| IRS guidance | The IRS has provided guidance on the taxability of health insurance payments to contract employees, which should be consulted for more information |

Explore related products

What You'll Learn

- General Rule: Payments to contract employees are generally not taxable as employee compensation

- Exceptions: Certain payments may be taxable if they constitute wages or salaries

- Factors Considered: IRS considers factors like the nature of the work, payment structure, and employer-employee relationship

- Reporting Requirements: Employers must report payments to contract employees on Form 1099-MISC

- Tax Implications: Contract employees are responsible for paying self-employment taxes on their earnings

![]()

General Rule: Payments to contract employees are generally not taxable as employee compensation

In the realm of taxation, understanding the nuances between different types of payments is crucial. When it comes to contract employees, the general rule is that payments made to them are not considered taxable as employee compensation. This distinction is significant because it affects how both the payer and the recipient report and pay taxes. For the payer, it means that they do not need to withhold taxes such as Social Security and Medicare from the payments made to contract employees. For the recipient, it means that they are responsible for paying their own self-employment taxes.

However, this general rule is not without its exceptions. One notable exception is when a contract employee is considered to be an employee under common law. In such cases, even though the individual is labeled as a contract employee, they may still be subject to taxation as an employee. This can happen if the individual performs services that are typically associated with employment, such as working regular hours, being supervised by the payer, and having the payer control the manner and means of the work performed.

Another important consideration is the type of payment being made. For instance, if a contract employee is being reimbursed for expenses incurred while performing services, these reimbursements are generally not taxable. However, if the payments are made as compensation for services rendered, then they may be subject to taxation. It is also worth noting that if a contract employee receives non-cash compensation, such as health insurance benefits, these benefits may be taxable.

In conclusion, while the general rule is that payments to contract employees are not taxable as employee compensation, there are several exceptions and nuances that must be considered. It is important for both payers and recipients to understand these rules to ensure compliance with tax laws and to avoid any potential penalties or fines.

Navigating Spousal Coverage: Employee Health Insurance Obligations Explained

You may want to see also

Explore related products

![]()

Exceptions: Certain payments may be taxable if they constitute wages or salaries

In the context of health insurance payments to contract employees, it's crucial to understand the exceptions that may apply regarding taxability. While health insurance premiums are generally not taxable, certain payments can be considered taxable if they constitute wages or salaries. This exception is significant and requires careful examination to ensure compliance with tax regulations.

To determine if health insurance payments are taxable, it's essential to assess whether they are being provided as compensation for services rendered. If the payments are made in lieu of wages or as a form of remuneration, they may be subject to taxation. This can be particularly relevant in situations where contract employees are receiving health insurance benefits as part of their overall compensation package.

For example, if a contract employee is receiving a stipend or allowance specifically for health insurance, this amount may be considered taxable income. Similarly, if the employer is paying the health insurance premiums directly and the employee is not contributing any portion, this could also be viewed as a taxable benefit. It's important to note that the specific circumstances and the nature of the employment relationship will play a significant role in determining the taxability of these payments.

In some cases, health insurance payments may be partially taxable. For instance, if the employer pays a portion of the health insurance premium and the employee pays the remainder, only the employer's contribution may be considered taxable. This highlights the importance of understanding the nuances of the employment agreement and the breakdown of the health insurance payments.

To navigate these complexities, it's advisable for employers and contract employees to consult with a tax professional or legal advisor. They can provide guidance on the specific tax implications of health insurance payments and help ensure that all parties are in compliance with applicable tax laws. Additionally, keeping detailed records of all health insurance payments and contributions can be instrumental in accurately reporting and withholding taxes as required.

In summary, while health insurance payments to contract employees are generally not taxable, exceptions do exist when these payments constitute wages or salaries. It's essential to carefully evaluate the nature of the payments and the employment relationship to determine the correct tax treatment. Seeking professional advice and maintaining thorough documentation can help mitigate any potential tax issues and ensure that all parties are well-informed and compliant with the law.

CVS Health Employees: Are They Healthcare Workers?

You may want to see also

Explore related products

![]()

Factors Considered: IRS considers factors like the nature of the work, payment structure, and employer-employee relationship

The IRS scrutinizes several key factors to determine whether health insurance payments made to a contract employee are taxable. One of the primary considerations is the nature of the work being performed. If the work is considered an integral part of the employer's regular business operations, it may suggest an employment relationship, potentially making the health insurance payments taxable. Conversely, if the work is more peripheral or project-based, it might be viewed as a contractual arrangement, which could imply that the payments are not taxable.

Another critical factor is the payment structure. If the contract employee is paid a fixed fee for their services, it is more likely to be considered a contractual relationship, which may exempt the health insurance payments from taxation. However, if the employee is paid hourly or receives a salary, it could indicate an employment relationship, making the payments taxable. The IRS also looks at the level of control the employer has over the employee's work. If the employer has significant control over the employee's schedule, tasks, and methods of work, it may suggest an employment relationship, potentially making the health insurance payments taxable.

The employer-employee relationship is also a crucial consideration. If the contract employee is treated similarly to regular employees, with access to the same benefits and privileges, it may indicate an employment relationship, making the health insurance payments taxable. On the other hand, if the contract employee is clearly an independent contractor with their own business, equipment, and clients, it is more likely that the payments will not be taxable.

In addition to these factors, the IRS may also consider the duration of the relationship and the employee's role within the company. If the contract employee has been working for the company for an extended period and holds a significant position, it may suggest an employment relationship, potentially making the health insurance payments taxable. However, if the employee is hired for a short-term project or has a limited role, it might be viewed as a contractual arrangement, which could imply that the payments are not taxable.

Ultimately, the determination of whether health insurance payments to a contract employee are taxable depends on a careful analysis of these factors. Employers and contract employees should consult with a tax professional to ensure compliance with IRS regulations and to understand the specific implications of their unique situation.

Decoding Employee Health Insurance Premiums: Taxable or Not?

You may want to see also

Explore related products

![]()

Reporting Requirements: Employers must report payments to contract employees on Form 1099-MISC

Employers are required to report payments made to contract employees on Form 1099-MISC, which is a crucial aspect of tax compliance. This form is used to report miscellaneous income, including payments made to independent contractors for services rendered. The IRS uses this information to ensure that contract employees are paying their fair share of taxes and that employers are accurately reporting the payments they make.

When it comes to health insurance payments made to contract employees, it's important to note that these payments are generally considered taxable income. This means that employers must report these payments on Form 1099-MISC, along with any other payments made to the contract employee. The taxable amount of the health insurance payments should be included in Box 7 of the form, which is designated for nonemployee compensation.

It's worth noting that there are some exceptions to this rule. For example, if the health insurance payments are made directly to the insurance provider and not to the contract employee, they may not be considered taxable income. Additionally, if the contract employee is already receiving health insurance coverage through another source, such as a spouse's employer, the payments made by the employer may not be taxable.

To ensure compliance with tax laws, employers should carefully review the instructions for Form 1099-MISC and consult with a tax professional if they have any questions or concerns. It's also important for contract employees to be aware of their tax obligations and to report any income they receive, including health insurance payments, on their tax returns.

In summary, employers must report payments made to contract employees, including health insurance payments, on Form 1099-MISC. This is an important aspect of tax compliance, and both employers and contract employees should be aware of their obligations under the law.

Understanding Florida's Employee Health Care Act: Key Requirements Explained

You may want to see also

Explore related products

![]()

Tax Implications: Contract employees are responsible for paying self-employment taxes on their earnings

Contract employees, unlike traditional employees, bear the responsibility of paying self-employment taxes on their earnings. This includes both the employer and employee portions of Social Security and Medicare taxes. Typically, an employer would cover the employer's share and withhold the employee's share from their paycheck. However, as a contract employee, you must account for both parts, which can significantly impact your take-home pay.

One of the key aspects of managing self-employment taxes is understanding the tax rate. As of the latest tax laws, the self-employment tax rate is 15.3% of your net earnings. This rate encompasses 12.4% for Social Security and 2.9% for Medicare. It's crucial to set aside funds to cover these taxes, as they are not withheld from your income. Failure to do so can lead to a substantial tax bill at the end of the year, along with potential penalties and interest.

To mitigate the impact of self-employment taxes, contract employees can take advantage of certain deductions. For instance, you can deduct the employer portion of the self-employment tax from your taxable income. Additionally, you may be able to deduct health insurance premiums if you purchase your own coverage. Keeping accurate records of your income and expenses is essential to ensure you can claim these deductions correctly.

Another strategy to consider is making estimated tax payments throughout the year. This can help you avoid underpayment penalties and spread out the tax burden more evenly. The IRS provides forms and guidelines for making estimated tax payments, which can be particularly useful for contract employees who may not have a consistent income stream.

In summary, as a contract employee, it's imperative to understand and manage your self-employment tax obligations. This includes knowing the tax rate, setting aside funds, taking advantage of deductions, and making estimated tax payments. By staying informed and proactive, you can minimize the financial impact of self-employment taxes and ensure compliance with tax laws.

Exploring the Differences Between Employee and Union Health Plans

You may want to see also

Frequently asked questions

Generally, health insurance payments made by an employer to a contract employee are considered taxable income. This is because the IRS views these payments as a form of compensation, which is subject to federal income tax.

One exception is if the contract employee is considered an independent contractor rather than an employee. In this case, the health insurance payments may not be taxable. Another exception is if the health insurance plan is a qualified health plan under the Affordable Care Act, in which case the payments may be tax-free.

Health insurance payments to contract employees are typically reported on Form 1099-MISC as non-employee compensation. The employer must also report the payments on their own tax return, as they are considered a business expense.

If an employer fails to report health insurance payments to contract employees correctly, they may be subject to penalties and fines from the IRS. These penalties can include a failure to file penalty, a failure to pay penalty, and an accuracy-related penalty. In addition, the employer may be required to pay back taxes and interest on the unreported income.