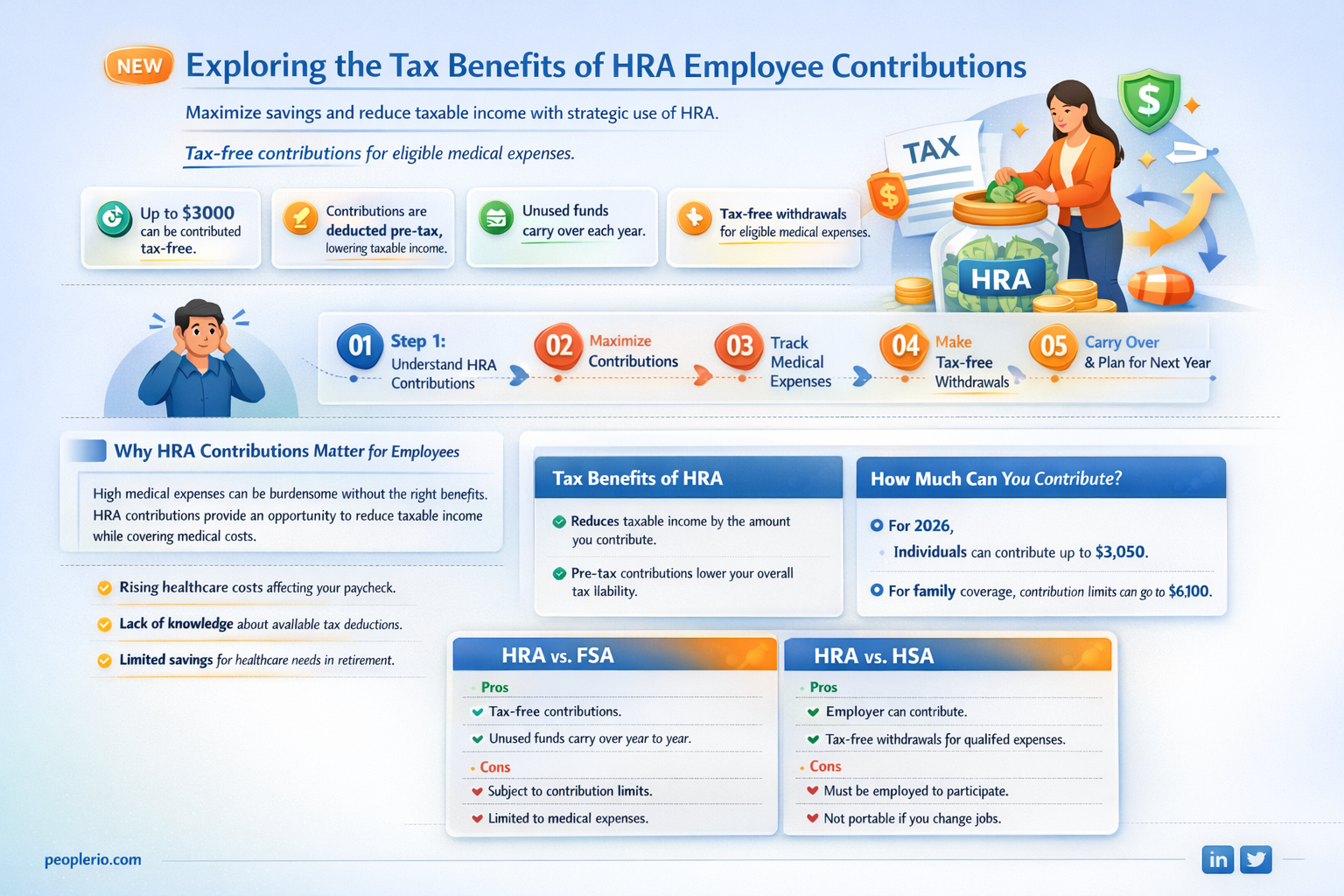

Health Reimbursement Arrangements (HRAs) are employer-funded plans that reimburse employees for qualified medical expenses. One common question regarding HRAs is whether employee contributions to these plans are tax-deductible. Generally, employee contributions to an HRA are not tax-deductible because they are considered employer contributions for tax purposes. However, the specific rules can vary depending on the type of HRA and the tax laws in the employee's country or region. It's essential for employees to consult with a tax professional or refer to their employer's HRA plan documents for detailed information on the tax implications of their contributions.

Explore related products

![H&R Block Tax Software Deluxe + State 2022 with Refund Bonus Offer (Amazon Exclusive) [PC Download] (Old Version)](https://m.media-amazon.com/images/I/71L-QsTnZhL._AC_UY218_.jpg)

What You'll Learn

- General Rule: Contributions to HRAs are generally tax-deductible for the employer

- Employee Contributions: Employees' HRA contributions are typically made pre-tax, reducing taxable income

- Limits and Conditions: There may be limits on the amount that can be contributed tax-free

- Withdrawal Rules: Tax implications may arise if HRA funds are withdrawn for non-qualified expenses

- State Tax Considerations: Some states may have different tax rules regarding HRA contributions

![]()

General Rule: Contributions to HRAs are generally tax-deductible for the employer

Contributions to Health Reimbursement Arrangements (HRAs) are generally tax-deductible for employers, providing a significant financial incentive for companies to offer these benefits. This deduction can be claimed for contributions made to HRAs that cover qualified medical expenses, including those for employees, their spouses, and dependents. The tax-deductible nature of these contributions can help employers reduce their taxable income, thereby lowering their overall tax liability.

To qualify for the deduction, the HRA must meet certain criteria. For instance, the plan must be in writing and must provide benefits only for qualified medical expenses. Additionally, the employer must substantiate the expenses claimed under the HRA, ensuring that they are legitimate and meet the IRS's guidelines. Employers should also be aware of the annual contribution limits and any carryover provisions to maximize the tax benefits while remaining compliant with the regulations.

One key advantage of HRAs is their flexibility. Employers can design the plan to suit their specific needs and budget, choosing which expenses to cover and setting the contribution amounts. This flexibility allows companies to tailor the HRA to provide the most value to their employees while also optimizing their tax savings. Furthermore, HRAs can be a valuable tool for employee recruitment and retention, as they demonstrate the employer's commitment to supporting the health and well-being of their workforce.

In conclusion, the general rule that contributions to HRAs are tax-deductible for employers offers a compelling reason for companies to consider offering these plans. By understanding the criteria for qualification and the potential benefits, employers can make informed decisions about implementing an HRA to support their employees' health needs while also enhancing their own financial position.

Unlocking the Tax Benefits of Employee Awards: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Employee Contributions: Employees' HRA contributions are typically made pre-tax, reducing taxable income

Employee contributions to Health Reimbursement Arrangements (HRAs) are generally made on a pre-tax basis, which can significantly reduce an individual's taxable income. This tax advantage is one of the primary benefits of participating in an HRA, as it allows employees to set aside funds for medical expenses without incurring an immediate tax liability. The pre-tax nature of these contributions means that the money is deducted from an employee's paycheck before federal, state, and local taxes are calculated, thereby lowering the overall tax burden.

For example, if an employee contributes $2,000 to their HRA in a given year, this amount would be subtracted from their gross income before taxes are applied. Assuming the employee is in a 25% tax bracket, this would result in a tax savings of $500 ($2,000 x 0.25). This reduction in taxable income can also potentially lower the employee's tax bracket, leading to additional savings.

It is important to note that while HRA contributions are pre-tax, they are not tax-free. The funds must be used for qualified medical expenses, and any unused balance may be forfeited or carried over to future years, depending on the plan's provisions. Additionally, if an employee withdraws HRA funds for non-qualified expenses, they may be subject to income tax and a 20% penalty.

Employers may also contribute to an employee's HRA, and these contributions are generally tax-deductible for the employer as a business expense. This can provide an additional incentive for employers to offer HRAs as part of their employee benefits package.

In summary, the pre-tax nature of employee HRA contributions can offer significant tax savings, making it an attractive option for individuals looking to manage their healthcare expenses more effectively. However, it is crucial to understand the rules and limitations associated with HRAs to maximize their benefits while avoiding potential tax pitfalls.

Decoding IRS Returns: Employee Plans vs. Payroll Taxes Explained

You may want to see also

Explore related products

![]()

Limits and Conditions: There may be limits on the amount that can be contributed tax-free

While HRA contributions can offer significant tax benefits, it's crucial to understand that these benefits are not unlimited. The IRS imposes specific limits on the amount of money that can be contributed to an HRA on a tax-free basis. For the 2023 tax year, the maximum contribution limit for an individual is $3,650, while for families, it's $7,300. These limits are subject to change, so it's essential to stay updated on the current tax laws.

One key condition to note is that HRA contributions must be made before the end of the tax year to qualify for the deduction. This means that if you're considering making a contribution, you should do so before December 31st to ensure you receive the tax benefits for that year. Additionally, the funds in your HRA must be used for qualified medical expenses; otherwise, you may face penalties or taxes on the unused funds.

Another important consideration is that HRA contributions are not deductible if you're also claiming the standard deduction. This means that if you're not itemizing your deductions, you won't be able to take advantage of the tax benefits offered by your HRA contributions. It's also worth noting that if you're covered by your spouse's HRA, you cannot make contributions to your own HRA.

To maximize the benefits of your HRA, it's essential to carefully plan your contributions and ensure that you're using the funds for qualified expenses. By understanding the limits and conditions associated with HRA contributions, you can make informed decisions about your tax strategy and potentially save money on your healthcare costs.

Understanding 401(k) Tax Exemptions in New Mexico: A Guide for Employees

You may want to see also

Explore related products

![Employee Warning Notice Forms Book: Track Disciplinary Actions and Employee Violations with Organized HR Write-Ups [A4]](https://m.media-amazon.com/images/I/612i0Jw94OL._AC_UY218_.jpg)

![]()

Withdrawal Rules: Tax implications may arise if HRA funds are withdrawn for non-qualified expenses

When it comes to House Rent Allowance (HRA), one of the key considerations for employees is understanding the tax implications of withdrawing funds for non-qualified expenses. While HRA contributions are generally tax-deductible, the withdrawal of these funds for purposes other than rent can lead to taxable income. This means that employees need to be cautious and well-informed about the rules governing HRA withdrawals to avoid unexpected tax liabilities.

For instance, if an employee withdraws HRA funds to cover expenses such as utilities, furniture, or other household costs, these amounts may be considered taxable income. The tax implications can vary depending on the specific circumstances and the tax laws applicable in the employee's jurisdiction. It is essential for employees to keep accurate records of their HRA withdrawals and to consult with a tax professional if they are unsure about the tax treatment of specific expenses.

To mitigate potential tax issues, employees should familiarize themselves with the qualifying expenses for HRA withdrawals. Typically, HRA funds can be withdrawn tax-free for rent payments, but there may be other eligible expenses depending on the employer's plan and local tax regulations. By understanding these rules and ensuring that withdrawals are made for qualified expenses, employees can maximize the tax benefits of their HRA contributions while minimizing the risk of taxable income.

In addition to considering the tax implications, employees should also be aware of any penalties or fees associated with HRA withdrawals. Some employers may impose penalties for early withdrawals or for withdrawals made for non-qualified expenses. Understanding these potential costs can help employees make informed decisions about when and how to withdraw their HRA funds.

Overall, while HRA contributions can provide significant tax benefits, it is crucial for employees to navigate the withdrawal rules carefully to avoid unintended tax consequences. By staying informed and seeking professional advice when needed, employees can make the most of their HRA while ensuring compliance with tax regulations.

Unreimbursed Clergy Expenses: Tax Deductibility Under Recent Legislation

You may want to see also

Explore related products

$14.99 $25

![]()

State Tax Considerations: Some states may have different tax rules regarding HRA contributions

While federal tax laws provide a general framework for the deductibility of HRA contributions, state tax regulations can introduce significant variations. It's crucial for employees to understand these state-specific rules to accurately assess the tax benefits of their HRA contributions.

For instance, some states may fully conform to federal tax laws, allowing employees to deduct HRA contributions from their state taxable income. However, other states may have different rules, potentially limiting or eliminating the state tax deduction for HRA contributions. This can significantly impact the overall tax savings for employees, especially those in higher tax brackets.

To navigate these complexities, employees should consult their state's tax code or seek guidance from a tax professional familiar with state-specific regulations. Additionally, employers may provide resources or guidance to help employees understand the tax implications of their HRA contributions under state law.

In some cases, state tax rules may interact with federal tax laws in unexpected ways. For example, a state may allow a deduction for HRA contributions but then require employees to report the federal tax deduction as income on their state tax return. This can lead to a reduction in the overall tax benefit, highlighting the importance of considering both federal and state tax implications when evaluating the deductibility of HRA contributions.

Ultimately, understanding state tax considerations is essential for employees looking to maximize the tax benefits of their HRA contributions. By being aware of these rules, employees can make informed decisions about their contributions and avoid potential tax pitfalls.

Understanding Tax Rates for 1099 Employees: A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, HRA (House Rent Allowance) employee contributions are tax deductible under Section 80C of the Income Tax Act, 1961.

The maximum amount of HRA that can be claimed as a tax deduction is ₹1.5 lakh per financial year.

Yes, both husband and wife can claim HRA deduction individually if they are both employed and paying rent for separate accommodations.

To claim HRA deduction, you need to provide rent receipts, rent agreement, and a declaration stating that you are not claiming HRA from any other source.

No, you cannot claim HRA deduction if you are living in your own house. HRA is only applicable for rented accommodations.