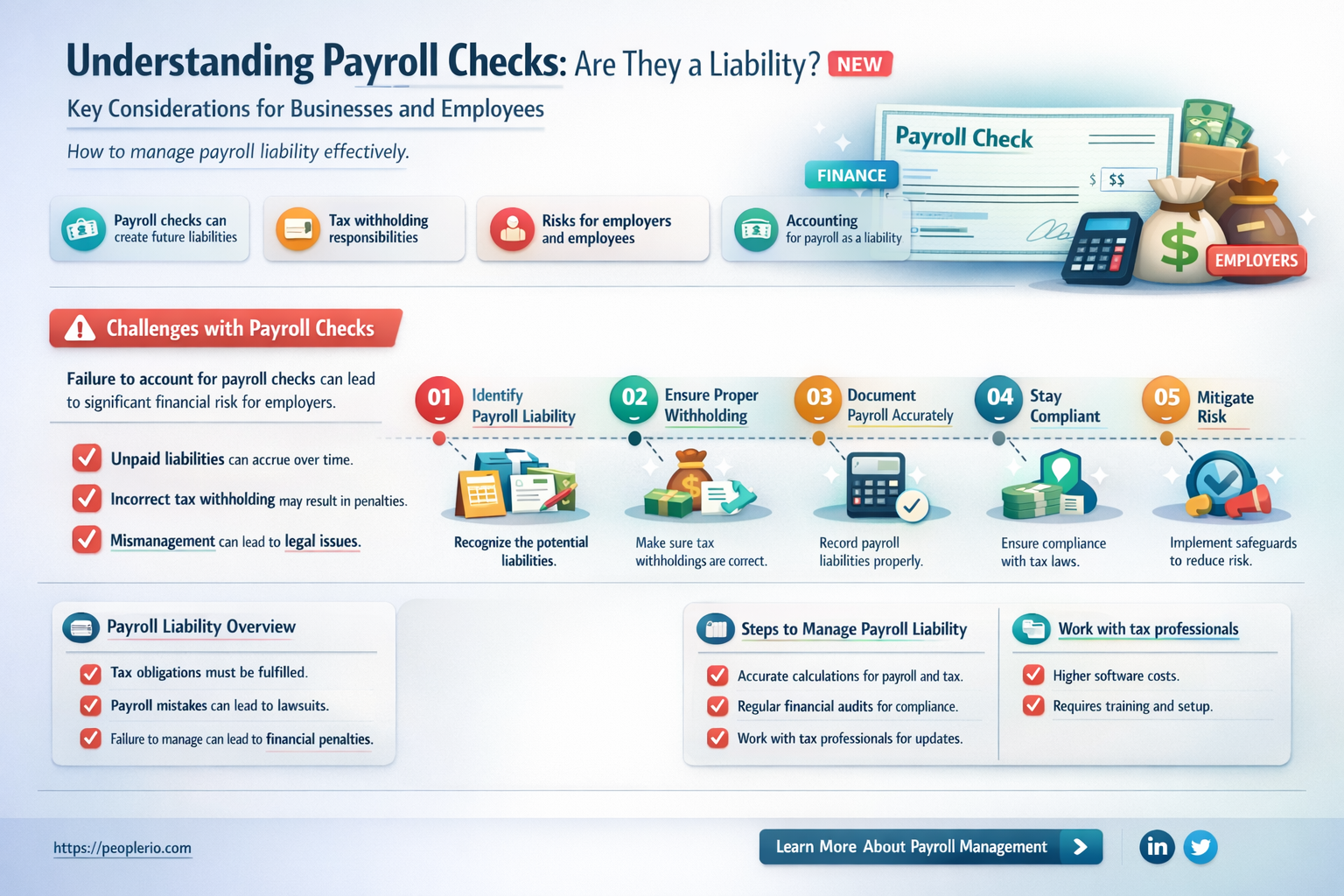

Payroll checks are a common financial instrument used by businesses to compensate their employees. When it comes to accounting and financial reporting, the classification of payroll checks can sometimes be a point of confusion. In this context, it's important to understand whether payroll checks are considered liabilities. A liability, in accounting terms, is an obligation or debt that a company owes to another party. Payroll checks, once issued, represent a commitment to pay employees for their services rendered. Therefore, until the checks are cashed or deposited, they are indeed considered liabilities on the company's balance sheet. This classification ensures that the financial statements accurately reflect the company's outstanding obligations.

| Characteristics | Values |

|---|---|

| Type of Document | Payroll Checks |

| Classification | Liability |

| Reason for Classification | Payroll checks represent amounts owed to employees for wages and salaries. |

| Accounting Treatment | Payroll checks are recorded as a liability on the balance sheet until they are paid. |

| Impact on Cash Flow | Payroll checks can affect cash flow as they represent a future cash outflow. |

| Related Accounts | Payroll checks are typically associated with the Payroll Liabilities account. |

| Financial Reporting | Payroll liabilities are reported on the balance sheet under current liabilities. |

| Compliance | Proper classification of payroll checks is important for accurate financial reporting and compliance with accounting standards. |

Explore related products

What You'll Learn

- Definition of Liabilities: Understanding what constitutes a liability in accounting terms

- Payroll Check Classification: Determining whether payroll checks are considered liabilities

- Accounting Treatment: How payroll checks are recorded in financial statements

- Impact on Cash Flow: Analyzing the effect of payroll checks on a company's liquidity

- Related Accounting Principles: Exploring GAAP and IFRS guidelines relevant to payroll liabilities

![]()

Definition of Liabilities: Understanding what constitutes a liability in accounting terms

In accounting, liabilities are defined as the financial obligations or debts that a company owes to external parties. These can arise from various transactions and events, such as borrowing money, purchasing goods on credit, or incurring expenses that have not yet been paid. Liabilities are an essential component of a company's balance sheet, as they help to determine its financial health and solvency.

There are several key characteristics that define a liability. First, it must be a present obligation that the company is legally bound to fulfill. This means that the company has a contractual or legal responsibility to pay the amount owed. Second, the liability must be measurable in monetary terms, meaning that the amount owed can be quantified and recorded on the company's financial statements. Finally, the liability must be settled in the future, either by paying cash or by providing goods or services to the creditor.

Liabilities can take many forms, including accounts payable, accrued expenses, loans, bonds, and leases. Accounts payable are amounts owed to suppliers for goods or services purchased on credit, while accrued expenses are expenses that have been incurred but not yet paid. Loans and bonds are forms of long-term debt that the company has borrowed from lenders or investors, and leases are agreements to rent assets from a lessor.

Payroll checks, on the other hand, are not typically considered liabilities. Payroll checks are a form of payment made to employees for their wages or salaries. Once the payroll checks are issued and cashed, the obligation to pay the employees is fulfilled, and the amount is no longer considered a liability. However, if the payroll checks are not issued or cashed, the amount owed to employees may be considered a liability until it is paid.

In conclusion, understanding what constitutes a liability is crucial for accurate financial reporting and analysis. Liabilities represent a company's financial obligations to external parties and can have a significant impact on its financial health and solvency. Payroll checks, while related to employee compensation, are not typically considered liabilities unless they remain unpaid.

Understanding Your Pay: A Guide to Payroll Check Stubs

You may want to see also

Explore related products

![]()

Payroll Check Classification: Determining whether payroll checks are considered liabilities

Payroll checks are a common financial instrument used by businesses to compensate employees for their work. However, there is often confusion regarding whether these checks should be classified as liabilities on a company's balance sheet. To determine this, it's essential to understand the nature of liabilities and how payroll checks fit into this category.

Liabilities are financial obligations or debts that a company owes to external parties, such as creditors, suppliers, or employees. They are typically settled by the company paying out cash or other assets. Payroll checks, in this context, represent a company's obligation to pay its employees for their services rendered. Therefore, they can be considered a type of liability, specifically an accrued liability, since the obligation to pay arises as employees work, even if the payment is not yet due.

The classification of payroll checks as liabilities is further supported by accounting standards and practices. Generally Accepted Accounting Principles (GAAP) dictate that liabilities should be recognized when they are incurred, regardless of when the payment is due. This means that as soon as employees perform their work, the company should record the corresponding liability on its balance sheet, even if the payroll check is not yet issued.

In practice, this classification can have significant implications for a company's financial reporting and analysis. By recognizing payroll checks as liabilities, companies can more accurately reflect their financial obligations and ensure that their balance sheets provide a true picture of their financial position. This can be particularly important for companies with large workforces or those that issue payroll checks frequently, as the aggregate amount of these liabilities can be substantial.

Moreover, the classification of payroll checks as liabilities can impact a company's cash flow management and financial planning. By acknowledging these obligations, companies can better anticipate their future cash outflows and make informed decisions about budgeting, investing, and financing. This can help to ensure that they have sufficient liquidity to meet their payroll obligations and avoid potential financial difficulties.

In conclusion, payroll checks should be classified as liabilities on a company's balance sheet, as they represent a financial obligation to employees for services rendered. This classification is supported by accounting standards and practices, and it has important implications for a company's financial reporting, analysis, and planning. By recognizing payroll checks as liabilities, companies can more accurately reflect their financial obligations and make informed decisions about their financial management.

Does Meijer Cash Payroll Checks? A Complete Guide for Employees

You may want to see also

Explore related products

![]()

Accounting Treatment: How payroll checks are recorded in financial statements

Payroll checks are a critical component of a company's financial operations, representing the compensation paid to employees for their services. In accounting terms, these checks are recorded as expenses on the income statement and as liabilities on the balance sheet. The process begins when a company accrues wages and salaries, which are then paid out to employees in the form of payroll checks. At the time of payment, the company debits its cash account and credits its wages and salaries payable account, thereby reducing the liability.

The accounting treatment for payroll checks involves several key steps. First, the company must calculate the total amount of wages and salaries earned by employees during the pay period. This includes not only the base pay but also any overtime, bonuses, or other forms of compensation. Once the total amount is determined, the company records an expense on the income statement for the current period. Simultaneously, a corresponding liability is recorded on the balance sheet under the category of wages and salaries payable.

When the payroll checks are issued, the company debits its cash account for the total amount of the checks and credits its wages and salaries payable account. This transaction reduces the cash balance and eliminates the liability, as the employees have now been paid. It is essential to ensure that the payroll checks are recorded accurately and in a timely manner to maintain the integrity of the financial statements.

In addition to the direct accounting treatment, there are other considerations related to payroll checks. For example, companies must also account for payroll taxes, such as Social Security and Medicare, which are typically withheld from employees' paychecks. These taxes are recorded as additional expenses and liabilities on the financial statements. Furthermore, companies may need to consider the impact of payroll checks on their cash flow, as large payments can significantly affect liquidity.

Overall, the accounting treatment for payroll checks is a complex process that requires careful attention to detail. By understanding the steps involved and the implications for financial reporting, companies can ensure that their payroll operations are conducted efficiently and accurately.

Mastering Payroll: A Step-by-Step Guide to Calculating Your Check

You may want to see also

Explore related products

![]()

Impact on Cash Flow: Analyzing the effect of payroll checks on a company's liquidity

Payroll checks can have a significant impact on a company's cash flow, particularly in terms of liquidity. When a company issues payroll checks, it is essentially committing a portion of its cash reserves to cover the wages and salaries of its employees. This can lead to a decrease in the company's available cash, which can affect its ability to meet other financial obligations, such as paying bills or investing in new projects.

One way to analyze the effect of payroll checks on a company's liquidity is to look at the timing of the checks. If a company issues payroll checks on a weekly or bi-weekly basis, this can lead to a more consistent outflow of cash, which can be easier to manage. However, if a company issues payroll checks on a monthly basis, this can lead to a larger, more irregular outflow of cash, which can be more challenging to manage.

Another way to analyze the effect of payroll checks on a company's liquidity is to look at the amount of the checks. If a company has a large workforce or high salaries, this can lead to a significant outflow of cash, which can affect the company's liquidity. Additionally, if a company offers bonuses or other forms of compensation, this can also impact the company's cash flow.

To mitigate the impact of payroll checks on a company's liquidity, there are several strategies that can be employed. One strategy is to implement a cash flow management system, which can help the company track its cash inflows and outflows and make more informed decisions about when to issue payroll checks. Another strategy is to consider alternative forms of compensation, such as direct deposit or prepaid debit cards, which can reduce the need for physical payroll checks and improve the company's cash flow.

In conclusion, payroll checks can have a significant impact on a company's cash flow and liquidity. By analyzing the timing and amount of payroll checks, and implementing strategies to manage cash flow, companies can better navigate the challenges associated with payroll and maintain a healthy financial position.

Understanding Payroll Check Clearing Times: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Related Accounting Principles: Exploring GAAP and IFRS guidelines relevant to payroll liabilities

Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) provide comprehensive guidelines for financial reporting, including the classification of payroll liabilities. Under GAAP, payroll liabilities are typically recorded as current liabilities on the balance sheet. This classification is based on the assumption that these liabilities will be settled within one year or within the company's normal operating cycle, whichever is longer.

IFRS, on the other hand, may classify payroll liabilities differently depending on the specific circumstances. For instance, if the liabilities are due within 12 months, they are generally classified as current liabilities. However, if they are due beyond 12 months, they may be classified as non-current liabilities. This distinction is crucial for accurate financial reporting and analysis, as it affects the liquidity and solvency ratios of the company.

One key difference between GAAP and IFRS in the context of payroll liabilities is the treatment of accrued wages and salaries. Under GAAP, accrued wages and salaries are typically recorded as current liabilities, while under IFRS, they may be recorded as either current or non-current liabilities, depending on the timing of the payment. This difference can lead to variations in the financial statements of companies that operate in multiple jurisdictions or have adopted different accounting standards.

Another important consideration is the disclosure requirements for payroll liabilities. Both GAAP and IFRS require companies to disclose information about their payroll liabilities in the financial statements. However, the specific disclosure requirements may vary between the two standards. For example, IFRS may require more detailed disclosures about the nature and timing of payroll liabilities, while GAAP may focus more on the aggregate amount of these liabilities.

In conclusion, understanding the differences between GAAP and IFRS guidelines for payroll liabilities is essential for accurate financial reporting and analysis. Companies must carefully consider the classification, measurement, and disclosure of these liabilities to ensure compliance with the relevant accounting standards and to provide users with a clear and transparent picture of their financial position.

Direct Deposit Dilemmas: Can You Deposit Your Payroll Check Into Someone Else's Account?

You may want to see also

Frequently asked questions

Yes, payroll checks are typically listed under liabilities in accounting. This is because they represent amounts owed to employees for their work, which the company has not yet paid.

Payroll checks are classified as liabilities because they are financial obligations that the company must fulfill. Until the checks are issued and cleared, the company is responsible for paying the employees, making it a debt or liability.

Payroll checks are recorded in the general ledger by debiting the payroll expense account and crediting the cash account. This reflects the decrease in cash and the recognition of the expense.

If payroll checks are not paid on time, it can lead to several issues. Employees may become dissatisfied, leading to decreased morale and productivity. Additionally, the company may face legal consequences and penalties for late payments.

Generally, payroll checks are always listed as liabilities. However, in some cases, if the checks are issued and cleared immediately, they may not be recorded as liabilities. Instead, the expense would be recognized directly.