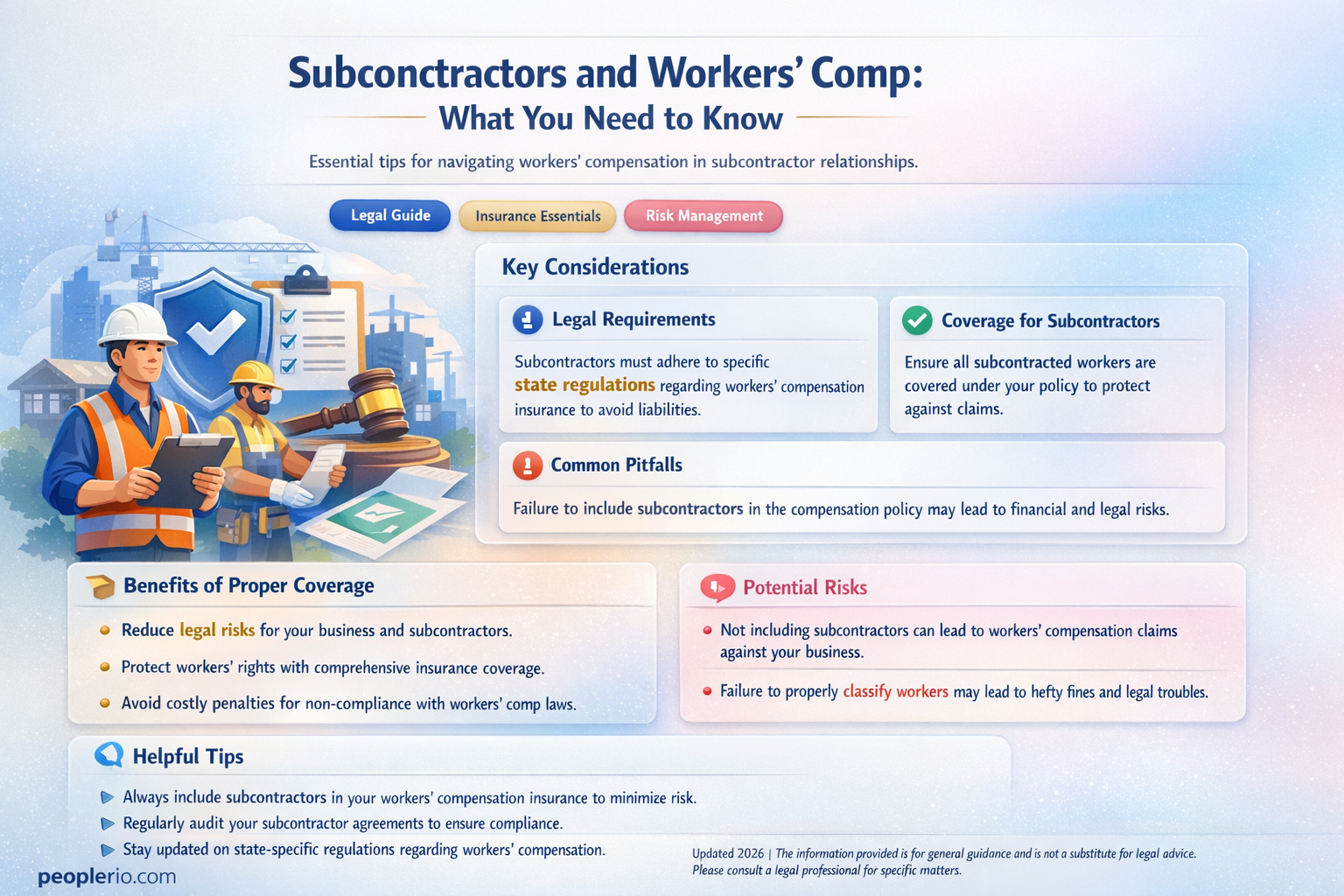

Workers' compensation insurance is a crucial aspect of business operations, especially for companies that engage subcontractors. This type of insurance provides coverage for work-related injuries or illnesses, ensuring that employees receive necessary medical treatment and wage replacement. When it comes to subcontractors, the requirement for workers' compensation insurance can vary depending on the jurisdiction and the specific terms of the subcontracting agreement. In many cases, subcontractors are indeed required to carry their own workers' compensation insurance to protect their employees and to limit the liability of the hiring company. This requirement helps to ensure that all workers on a project are adequately protected in the event of a workplace accident or injury.

| Characteristics | Values |

|---|---|

| Requirement | Subcontractors are typically required to have workers' compensation insurance |

| Purpose | To cover work-related injuries or illnesses of their employees |

| Beneficiary | The subcontractor's employees |

| Coverage | Medical expenses, lost wages, rehabilitation costs, and other related expenses |

| Legal Mandate | Varies by jurisdiction, but commonly required by law or contract |

| Verification | Contractors may need to provide proof of insurance to the primary contractor or client |

| Exceptions | Some jurisdictions or contracts may have specific exemptions or requirements |

Explore related products

What You'll Learn

- Legal Requirements: Vary by state, generally required if subcontractors have employees

- Coverage Types: Policies may cover medical expenses, lost wages, rehabilitation costs

- Cost Factors: Premiums depend on industry risk, number of employees, claims history

- Compliance Verification: Contractors should ensure subcontractors provide proof of adequate coverage

- Consequences of Non-Compliance: Failure to carry required insurance can lead to legal penalties, financial liability

![]()

Legal Requirements: Vary by state, generally required if subcontractors have employees

Workers' compensation insurance is a critical aspect of business operations, especially for subcontractors who employ workers. The legal requirements for this type of insurance vary significantly by state, making it essential for subcontractors to understand and comply with the specific regulations in their jurisdiction. Generally, if a subcontractor has employees, they are required to carry workers' compensation insurance to provide coverage for work-related injuries or illnesses.

The first step for subcontractors is to research the workers' compensation laws in their state. This includes understanding the minimum coverage limits, the types of employees who must be covered, and any exemptions that may apply. For example, some states may exempt small businesses with a certain number of employees or those in specific industries. Subcontractors should also be aware of the consequences of non-compliance, which can include hefty fines, penalties, and even legal action.

Once the legal requirements are understood, subcontractors must obtain the appropriate workers' compensation insurance policy. This typically involves working with an insurance broker or carrier who specializes in this type of coverage. The policy should be tailored to the specific needs of the business, taking into account factors such as the number of employees, the nature of the work, and the risk of workplace injuries.

In addition to obtaining the required insurance, subcontractors should also establish clear safety protocols and training programs to minimize the risk of workplace accidents. This can include regular safety meetings, hazard assessments, and providing personal protective equipment (PPE) as needed. By prioritizing workplace safety, subcontractors can not only reduce the likelihood of workers' compensation claims but also create a more positive and productive work environment.

Finally, subcontractors should regularly review and update their workers' compensation insurance policies to ensure ongoing compliance with state regulations. This may involve adjusting coverage limits, adding or removing employees from the policy, or making changes to the business operations that impact the risk profile. By staying proactive and informed, subcontractors can avoid costly mistakes and ensure that their employees are protected in the event of a workplace injury or illness.

Understanding Workers' Compensation Insurance: A Mandate for Employers?

You may want to see also

Explore related products

![]()

Coverage Types: Policies may cover medical expenses, lost wages, rehabilitation costs

Workers' compensation insurance is a critical safety net for employees, providing financial protection in the event of work-related injuries or illnesses. For subcontractors, understanding the types of coverage available is essential to ensure they are adequately protected. Policies typically cover medical expenses, lost wages, and rehabilitation costs, but the specifics can vary widely depending on the policy and the jurisdiction.

Medical expenses coverage is generally comprehensive, encompassing everything from emergency care to ongoing treatment and medications. This ensures that subcontractors can receive the necessary medical attention without incurring significant out-of-pocket costs. Lost wages coverage is equally important, as it helps to replace income lost due to the inability to work following an injury or illness. The amount and duration of this coverage can vary, so it's crucial for subcontractors to carefully review their policies.

Rehabilitation costs are another key component of workers' compensation coverage. This can include physical therapy, occupational therapy, and other forms of rehabilitation aimed at helping the subcontractor recover and return to work. In some cases, policies may also cover vocational rehabilitation, which assists workers in retraining for a new job if they are unable to return to their previous role.

Beyond these core coverage types, some policies may offer additional benefits, such as death benefits for the worker's dependents or coverage for home modifications necessary due to a work-related injury. Subcontractors should also be aware of any exclusions or limitations in their policies, such as pre-existing conditions or injuries that occur outside of the workplace.

Ultimately, the specific coverage types and details will depend on the subcontractor's policy and the laws of their state or country. It's essential for subcontractors to carefully review their policies, understand their rights and responsibilities, and ensure they have adequate coverage to protect themselves and their families in the event of a work-related injury or illness.

Understanding Military Disability Insurance: Coverage and Benefits Explained

You may want to see also

Explore related products

![]()

Cost Factors: Premiums depend on industry risk, number of employees, claims history

Workers' compensation insurance premiums are influenced by several key cost factors that businesses must consider. Industry risk is a primary determinant, as certain sectors inherently carry higher risks of workplace injuries. For instance, construction or manufacturing industries typically face more hazardous conditions compared to office-based jobs, leading to higher premium rates.

The number of employees also plays a significant role in calculating premiums. Larger companies with more workers will generally pay more in premiums due to the increased likelihood of claims. Conversely, smaller businesses with fewer employees may benefit from lower rates, reflecting the reduced risk pool.

Claims history is another critical factor impacting premium costs. A business with a history of frequent or severe claims will likely face higher premiums, as insurers view this as an indicator of potential future claims. Maintaining a safe work environment and implementing effective risk management strategies can help mitigate this factor and lead to more favorable premium rates.

In addition to these primary factors, other elements such as geographic location, business experience, and the type of coverage selected can also influence premium costs. For example, businesses operating in states with higher workers' compensation rates will pay more in premiums. Similarly, new businesses may face higher rates due to a lack of claims history, while those with a proven track record of safety and risk management may qualify for discounts.

Understanding these cost factors is essential for businesses to make informed decisions about their workers' compensation insurance. By assessing their industry risk, employee count, and claims history, companies can better anticipate their premium costs and take steps to manage these expenses effectively. This might include implementing safety training programs, investing in ergonomic equipment, or exploring different insurance providers to find the most competitive rates.

Ultimately, the key to controlling workers' compensation insurance premiums lies in proactive risk management and a commitment to maintaining a safe work environment. By addressing potential hazards and fostering a culture of safety, businesses can not only reduce their premium costs but also protect their most valuable asset – their employees.

Understanding Workers' Compensation Insurance Requirements for Nonprofits

You may want to see also

Explore related products

$6.99 $6.99

![]()

Compliance Verification: Contractors should ensure subcontractors provide proof of adequate coverage

Contractors have a critical responsibility to ensure that their subcontractors maintain adequate workers' compensation insurance coverage. This is not merely a formality but a crucial safeguard that protects both the subcontractors' employees and the contractors themselves from potential legal and financial liabilities. Without proper verification, contractors may unknowingly expose themselves to risks that could have been mitigated through due diligence.

To effectively verify compliance, contractors should implement a systematic approach. This begins with clearly stating the insurance requirements in the subcontractor agreement, including the minimum coverage limits and the types of risks that must be covered. Contractors should then request proof of insurance from subcontractors before work commences and ensure that the policies are current and in good standing. Regular audits and checks throughout the project lifecycle can help maintain ongoing compliance.

One common mistake contractors make is assuming that a subcontractor's general liability insurance will cover workers' compensation claims. This is often not the case, as workers' compensation insurance is designed to cover work-related injuries and illnesses specifically. Contractors must be vigilant in confirming that subcontractors have the appropriate workers' compensation coverage in place.

In addition to protecting against legal liabilities, ensuring adequate workers' compensation coverage can also foster a safer work environment. When subcontractors know that their employees are protected, they are more likely to prioritize safety measures and best practices. This, in turn, can lead to fewer accidents and injuries on the job site, ultimately benefiting everyone involved in the project.

In conclusion, compliance verification is a critical aspect of contractor-subcontractor relationships. By taking the necessary steps to ensure that subcontractors have adequate workers' compensation insurance, contractors can mitigate risks, protect their employees and themselves, and promote a safer work environment. This process requires diligence, clear communication, and ongoing monitoring to be effective.

Exploring State Farm's Workers' Compensation Insurance Options

You may want to see also

Explore related products

![]()

Consequences of Non-Compliance: Failure to carry required insurance can lead to legal penalties, financial liability

Failure to carry required insurance, such as workers' compensation, can have severe consequences for subcontractors. Legal penalties are a significant risk, as many jurisdictions mandate this type of insurance to protect workers in the event of injury or illness. Without proper coverage, subcontractors may face fines, lawsuits, or even criminal charges, depending on the severity and frequency of non-compliance.

Financial liability is another critical concern. In the absence of workers' compensation insurance, subcontractors may be held personally responsible for medical expenses, lost wages, and other damages incurred by injured workers. This can lead to substantial out-of-pocket costs and potentially bankrupt a small business. Moreover, uninsured subcontractors may struggle to secure future contracts, as clients and general contractors often require proof of adequate insurance coverage as a condition of doing business.

Beyond the direct financial and legal repercussions, non-compliance with insurance requirements can also damage a subcontractor's reputation. Word of uninsured operations can spread quickly within the industry, leading to a loss of trust and credibility among potential clients and partners. This can have long-term effects on a subcontractor's ability to secure work and maintain a stable business.

To mitigate these risks, it is essential for subcontractors to understand and comply with all applicable insurance requirements. This may involve consulting with an insurance professional to determine the appropriate types and levels of coverage, as well as staying informed about changes in local laws and regulations. By prioritizing proper insurance, subcontractors can protect themselves, their workers, and their businesses from the potentially devastating consequences of non-compliance.

Mandatory Workers' Compensation Insurance: What Companies Need to Know

You may want to see also

Frequently asked questions

Yes, subcontractors are generally required to have workers' compensation insurance to cover their employees in case of work-related injuries or illnesses.

If a subcontractor does not have workers' compensation insurance, they may be held liable for any work-related injuries or illnesses that occur to their employees. This can result in significant financial penalties and legal consequences.

The general contractor or the employer who hires the subcontractor is responsible for ensuring that the subcontractor has workers' compensation insurance. They may need to verify the subcontractor's insurance coverage before hiring them.

Workers' compensation insurance protects the subcontractor by providing coverage for their employees' medical expenses and lost wages in case of work-related injuries or illnesses. It also protects the general contractor by limiting their liability in case a subcontractor's employee is injured on the job.

If a general contractor fails to verify a subcontractor's workers' compensation insurance, they may be held liable for any work-related injuries or illnesses that occur to the subcontractor's employees. This can result in significant financial penalties and legal consequences.