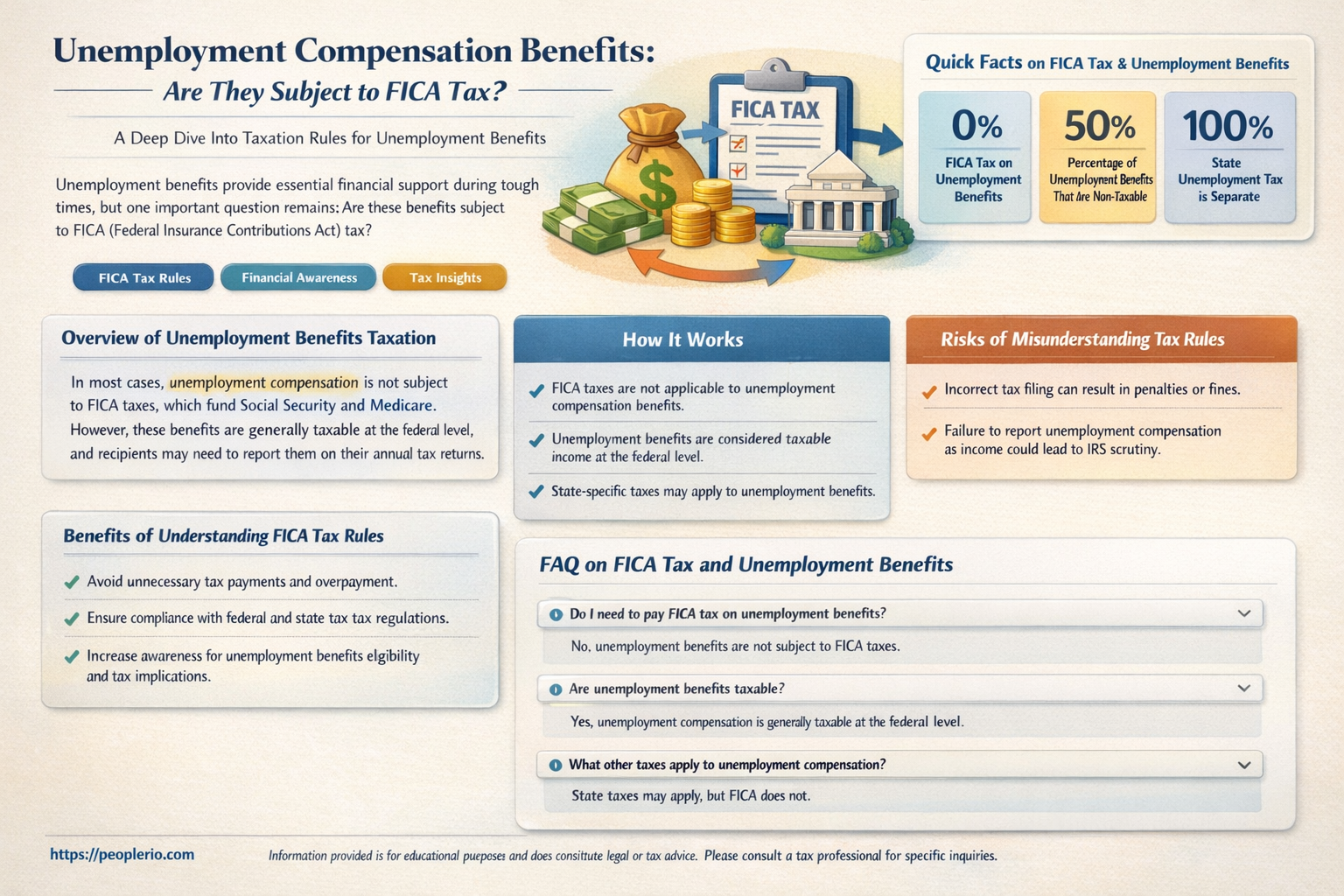

Unemployment compensation benefits are a crucial aspect of social safety nets, providing financial support to individuals who have lost their jobs through no fault of their own. However, a common question arises regarding the tax implications of these benefits: Are unemployment compensations benefits subject to FICA tax? FICA, which stands for Federal Insurance Contributions Act, is a federal payroll tax that funds Social Security and Medicare. Understanding whether unemployment benefits are taxable under FICA is essential for both recipients and policymakers to ensure compliance with tax laws and to plan for the financial sustainability of these programs.

| Characteristics | Values |

|---|---|

| Subject | Unemployment compensations benefits |

| Tax Applicability | Subject to FICA tax |

| FICA Tax Components | Social Security and Medicare taxes |

| Tax Rate | 6.2% for Social Security, 1.45% for Medicare |

| Tax Cap | No cap for Medicare, $137,700 cap for Social Security (2023) |

| Exemptions | None for unemployment benefits |

| Reporting Requirements | Reported on Form 1099-G |

Explore related products

What You'll Learn

- Definition of Unemployment Compensation: Understanding what constitutes unemployment compensation for FICA tax purposes

- FICA Tax Overview: Brief explanation of FICA tax, including its components and how it funds social programs

- Taxability of Benefits: Detailed analysis of whether unemployment benefits are taxable under FICA

- Exceptions and Exemptions: Exploring any exceptions or exemptions that might apply to unemployment benefits regarding FICA tax

- Reporting and Withholding: Guidelines on how to report and withhold FICA tax on unemployment compensation, if applicable

![]()

Definition of Unemployment Compensation: Understanding what constitutes unemployment compensation for FICA tax purposes

Unemployment compensation, for the purposes of FICA (Federal Insurance Contributions Act) tax, refers to any payments made to an individual due to their involuntary separation from employment. This includes traditional unemployment insurance benefits provided by state governments, as well as other forms of severance pay that are not based on the employee's prior earnings or length of service.

To qualify as unemployment compensation under FICA, the payments must be made pursuant to a governmental program or plan that provides for the payment of benefits to unemployed individuals. This means that private sector severance packages, even if they are substantial, do not typically qualify as unemployment compensation for FICA tax purposes. However, there are some exceptions to this rule, such as certain types of supplemental unemployment benefits provided by employers in conjunction with state unemployment insurance.

It is important to note that while unemployment compensation is generally exempt from FICA tax, there are some limitations to this exemption. For example, if an individual receives unemployment compensation in excess of the maximum benefit amount allowed by their state's unemployment insurance program, the excess amount may be subject to FICA tax. Additionally, certain types of unemployment compensation, such as benefits paid to individuals who are not actively seeking new employment, may also be subject to FICA tax.

Employers are responsible for withholding FICA tax from any unemployment compensation that is subject to tax. This includes both the employee's share of the tax, as well as the employer's share. Failure to properly withhold FICA tax from unemployment compensation can result in penalties and interest for the employer.

In conclusion, understanding what constitutes unemployment compensation for FICA tax purposes is crucial for both employers and employees. While most forms of unemployment compensation are exempt from FICA tax, there are some important exceptions and limitations to this exemption. Employers must be diligent in ensuring that they are properly withholding FICA tax from any unemployment compensation that is subject to tax, in order to avoid potential penalties and interest.

Navigating Job Loss: Your Guide to Unemployment Office Locations

You may want to see also

Explore related products

![]()

FICA Tax Overview: Brief explanation of FICA tax, including its components and how it funds social programs

FICA, which stands for Federal Insurance Contributions Act, is a U.S. federal payroll tax imposed on both employers and employees to fund Social Security and Medicare—two critical social insurance programs. The tax is calculated as a percentage of an employee's gross wages and is split between the employer and the employee. As of 2023, the Social Security tax rate is 6.2% for both employers and employees, while the Medicare tax rate is 1.45% for employees and 1.45% for employers, totaling 2.9% for Medicare.

Social Security benefits are funded through the Social Security Trust Fund, which is primarily financed by the payroll taxes collected under FICA. These benefits include retirement income, disability income, and survivor benefits for the dependents of deceased workers. Medicare, on the other hand, is funded through the Medicare Trust Fund, which also relies heavily on FICA taxes. Medicare provides health insurance coverage for individuals aged 65 and older, as well as for certain younger people with disabilities and those with End-Stage Renal Disease.

Regarding unemployment compensation benefits, they are generally not subject to FICA tax. This means that individuals receiving unemployment benefits do not have to pay Social Security or Medicare taxes on those benefits. However, it's important to note that while unemployment benefits are exempt from FICA tax, they may still be subject to federal income tax and state taxes, depending on the state's tax laws.

The exemption of unemployment benefits from FICA tax is designed to provide financial relief to individuals who are temporarily out of work. By not taxing these benefits, the government aims to ensure that unemployed individuals can maintain a basic level of financial stability while they search for new employment opportunities. This policy also helps to stimulate the economy by allowing unemployed individuals to spend more of their benefits on essential goods and services.

In summary, FICA tax plays a crucial role in funding Social Security and Medicare, two vital social insurance programs in the United States. While unemployment compensation benefits are not subject to FICA tax, they may still be taxable under federal income tax and state tax laws. This exemption is intended to support individuals during periods of unemployment and to contribute to economic stability.

Navigating Unemployment Compensation: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Taxability of Benefits: Detailed analysis of whether unemployment benefits are taxable under FICA

Unemployment benefits are a critical financial safety net for millions of Americans who find themselves out of work. However, understanding the tax implications of these benefits can be complex. Specifically, the question of whether unemployment benefits are taxable under the Federal Insurance Contributions Act (FICA) is an important one for both recipients and policymakers.

FICA taxes are typically applied to wages and salaries, funding Social Security and Medicare. Generally, unemployment benefits are not considered wages for FICA purposes. This means that recipients of unemployment benefits do not have to pay FICA taxes on those benefits. However, there are some nuances to this rule. For instance, if an individual receives unemployment benefits and also works part-time, their wages from that part-time job would be subject to FICA taxes.

It's also important to note that while unemployment benefits may not be taxable under FICA, they could still be subject to federal income tax. Recipients of unemployment benefits should consult with a tax professional or refer to IRS guidelines to understand their specific tax obligations.

In summary, unemployment benefits are generally not taxable under FICA, but there are exceptions and other tax considerations that recipients should be aware of. This analysis provides a detailed look at the intersection of unemployment benefits and FICA taxes, helping to clarify this aspect of the tax code.

Understanding Unemployment Compensation: Are Taxes Withheld?

You may want to see also

Explore related products

![]()

Exceptions and Exemptions: Exploring any exceptions or exemptions that might apply to unemployment benefits regarding FICA tax

While unemployment benefits are generally subject to FICA tax, there are specific exceptions and exemptions that can apply in certain circumstances. One such exception is for individuals who receive unemployment benefits due to a federally declared disaster. In these cases, the benefits may be exempt from FICA tax, providing some financial relief to those affected by the disaster.

Another exemption applies to certain state-funded unemployment benefits programs. Some states have opted to provide unemployment benefits that are not subject to FICA tax, either in whole or in part. This can vary depending on the state and the specific program, so it's essential to check with the relevant state authorities to determine if this exemption applies.

Additionally, there are exemptions for certain types of unemployment benefits, such as those provided under the Federal Unemployment Compensation Law (FUCL). These benefits are typically exempt from FICA tax, as they are funded by federal taxes rather than state taxes. However, it's important to note that this exemption may not apply to all types of FUCL benefits, and further clarification may be needed.

In some cases, individuals may be eligible for unemployment benefits that are partially exempt from FICA tax. For example, if an individual receives unemployment benefits from a state-funded program that is partially funded by federal taxes, a portion of those benefits may be exempt from FICA tax. This can be a complex area, and it's advisable to consult with a tax professional to determine the exact implications.

It's also worth noting that while unemployment benefits may be exempt from FICA tax, they may still be subject to other taxes, such as federal income tax or state income tax. Therefore, it's crucial to understand the full tax implications of receiving unemployment benefits and to plan accordingly.

Understanding Unemployment Compensation Eligibility: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Reporting and Withholding: Guidelines on how to report and withhold FICA tax on unemployment compensation, if applicable

Unemployment compensation benefits are indeed subject to FICA tax, which comprises Social Security and Medicare taxes. When individuals receive unemployment benefits, they are required to report this income on their federal tax return. The FICA tax on unemployment benefits is typically withheld by the state unemployment insurance program, but in some cases, individuals may need to make estimated tax payments if the withholding is insufficient.

To report FICA tax on unemployment compensation, individuals should receive a Form 1099-G from their state unemployment insurance program, which details the total amount of benefits received and the amount of FICA tax withheld. This form should be used when filing their federal tax return to ensure accurate reporting of unemployment benefits and FICA tax withholding.

If an individual's unemployment benefits are not subject to FICA tax withholding by the state, they may need to make estimated tax payments to avoid underpayment penalties. Estimated tax payments can be made quarterly using Form 1040-ES, which is available on the IRS website. It is essential to accurately calculate the estimated tax payments to avoid owing additional taxes or penalties when filing the federal tax return.

In addition to federal FICA tax, some states also impose state income tax on unemployment benefits. Individuals should check with their state tax authority to determine if they need to report and pay state income tax on their unemployment benefits. Failure to report and pay FICA tax on unemployment benefits can result in penalties and interest, so it is crucial to understand and comply with the reporting and withholding guidelines.

When reporting FICA tax on unemployment compensation, it is essential to keep accurate records of all benefits received and tax payments made. This includes maintaining copies of Form 1099-G, estimated tax payment receipts, and any correspondence with the IRS or state tax authority. By following these guidelines, individuals can ensure they are in compliance with FICA tax reporting and withholding requirements, avoiding potential penalties and interest.

Unemployment Compensation and Social Security Tax: What You Need to Know

You may want to see also

Frequently asked questions

Yes, unemployment compensation benefits are subject to FICA tax. The Federal Insurance Contributions Act (FICA) requires that both employers and employees pay taxes on wages, which includes unemployment compensation benefits.

The amount of FICA tax withheld from unemployment benefits depends on the total amount of benefits received. The tax rate is 6.2% for Social Security and 1.45% for Medicare, totaling 7.65%. However, there may be additional state taxes withheld as well.

Yes, you need to report unemployment benefits on your tax return. The IRS considers unemployment benefits as taxable income, and you must report them on Form 1040 when filing your annual tax return.

No, you cannot deduct the FICA tax withheld from your unemployment benefits on your tax return. FICA taxes are not deductible as itemized deductions or as a reduction to your adjusted gross income.

![Taxation is Theft Sticker Tax Sticker Funny Sarcastic Political Bumper Sticker Tax Refund Return Vinyl Decals Gift Decoration Graphic Car Truck Van Windows Helmet Bumper [7.5x3.75]](https://m.media-amazon.com/images/I/41ZNx4CTckL._AC_UL320_.jpg)