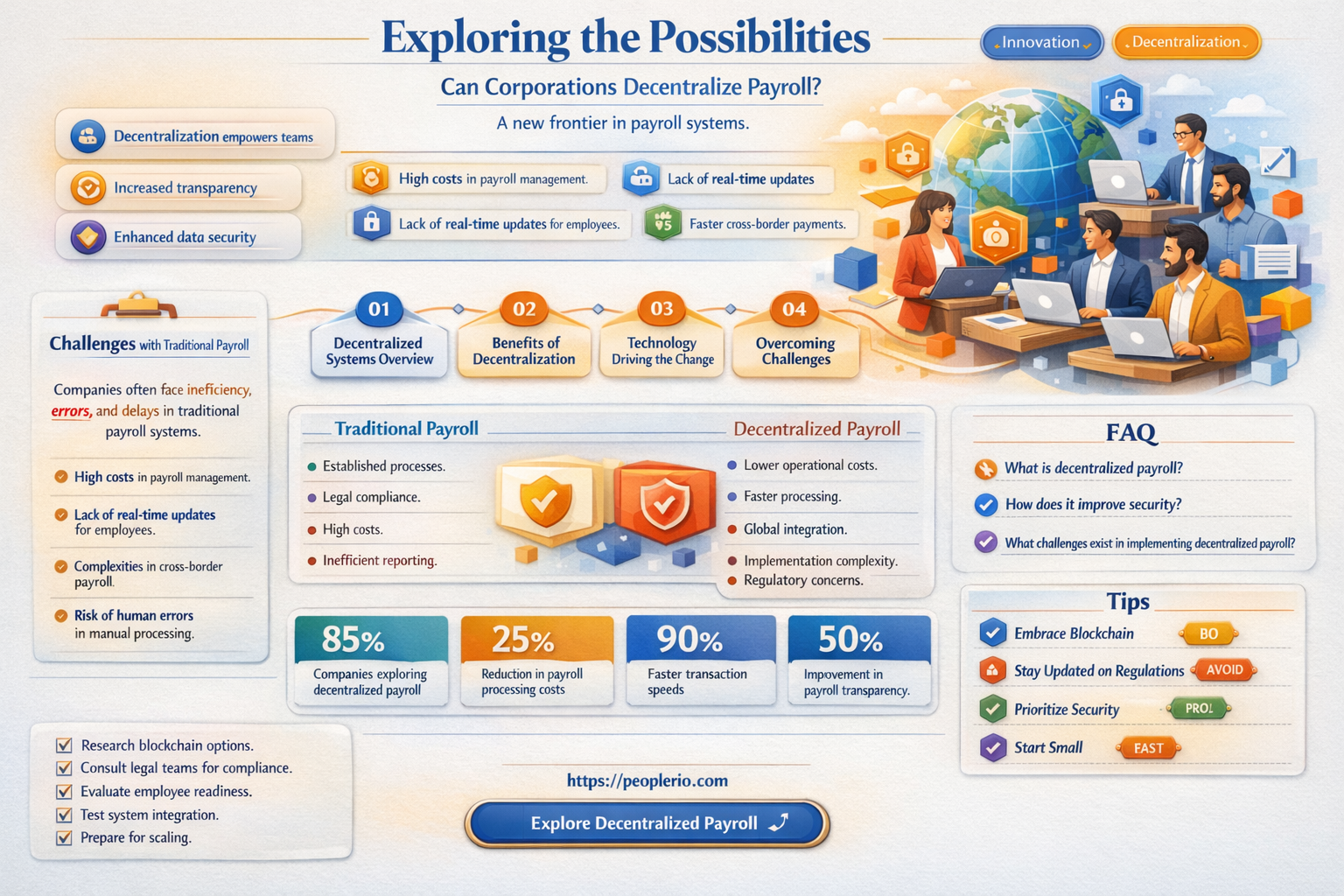

Decentralizing payroll is a concept that has gained traction in recent years, particularly with the rise of blockchain technology and remote workforces. At its core, decentralized payroll refers to the process of distributing payroll responsibilities and functions across multiple entities or locations, rather than centralizing them within a single corporate headquarters. This approach can offer several benefits, including increased efficiency, reduced costs, and improved compliance with local regulations. However, it also presents unique challenges, such as ensuring data security and maintaining consistent payroll processes across different jurisdictions. In this article, we will explore the feasibility and implications of decentralizing payroll for corporations, examining both the advantages and disadvantages of this emerging trend.

| Characteristics | Values |

|---|---|

| Decentralization | Yes, a corporation can decentralize payroll |

| Benefits | Increased efficiency, reduced costs, improved employee satisfaction |

| Challenges | Requires robust technology, potential security risks, need for clear communication |

| Implementation | Involves transitioning from centralized to decentralized systems, training staff, and setting up new processes |

| Cost Savings | Can be significant, as decentralized payroll reduces the need for intermediaries and streamlines operations |

| Employee Access | Employees can have more direct access to their payroll information and manage their own data |

| Compliance | Must ensure compliance with local and international payroll regulations |

| Scalability | Decentralized payroll can be more scalable and adaptable to changing business needs |

| Integration | Can be integrated with other HR and financial systems for a seamless experience |

| Security | Requires strong cybersecurity measures to protect sensitive employee data |

Explore related products

What You'll Learn

- Blockchain Integration: Utilizing blockchain technology to ensure transparent and secure payroll transactions

- Smart Contracts: Implementing smart contracts to automate payroll processes and reduce human error

- Tokenization of Compensation: Exploring the concept of tokenizing employee compensation for easier management and trading

- Decentralized Finance (DeFi) Solutions: Leveraging DeFi platforms to facilitate payroll operations without traditional banking intermediaries

- Regulatory Compliance: Navigating the legal and regulatory landscape to ensure decentralized payroll systems meet all necessary standards

![]()

Blockchain Integration: Utilizing blockchain technology to ensure transparent and secure payroll transactions

Blockchain technology offers a revolutionary approach to payroll management by ensuring transparency and security in transactions. Unlike traditional centralized payroll systems, which rely on a single authority to manage and distribute funds, blockchain integration decentralizes the process, making it more resistant to fraud and errors.

One of the key benefits of blockchain integration in payroll is the immutable nature of the ledger. Once a transaction is recorded on the blockchain, it cannot be altered or deleted, providing a permanent and transparent record of all payroll transactions. This feature is particularly useful for auditing purposes, as it allows for easy tracking and verification of payments.

Another advantage of blockchain integration is the enhanced security it provides. Payroll data is highly sensitive, and traditional systems are often vulnerable to cyber attacks and data breaches. By using blockchain technology, payroll data is encrypted and distributed across a network of computers, making it much more difficult for hackers to gain access.

Blockchain integration can also streamline the payroll process by automating certain tasks, such as calculating wages and deductions. Smart contracts, which are self-executing contracts with the terms of the agreement directly written into code, can be used to automate these calculations, reducing the need for manual intervention and minimizing the risk of human error.

However, implementing blockchain integration in payroll systems is not without its challenges. One of the main obstacles is the need for widespread adoption of blockchain technology. In order for blockchain integration to be effective, all parties involved in the payroll process, including employees, employers, and payroll service providers, must be using the same blockchain platform.

Another challenge is the regulatory environment surrounding blockchain technology. Payroll systems must comply with a variety of laws and regulations, and the use of blockchain technology may raise new legal and compliance issues. For example, the decentralized nature of blockchain technology may conflict with existing data protection laws, which require centralized control over personal data.

In conclusion, blockchain integration has the potential to revolutionize payroll management by providing a transparent, secure, and efficient way to manage and distribute funds. However, widespread adoption and regulatory compliance are key challenges that must be addressed in order for blockchain integration to become a mainstream solution in the payroll industry.

Can I Put My Child on Payroll? Legal and Tax Insights

You may want to see also

Explore related products

$13.52 $15.95

![]()

Smart Contracts: Implementing smart contracts to automate payroll processes and reduce human error

Smart contracts offer a revolutionary approach to automating payroll processes, significantly reducing the potential for human error. These self-executing contracts with the terms of the agreement directly written into code can streamline payroll operations, ensuring timely and accurate payments to employees. By leveraging blockchain technology, smart contracts provide a secure, transparent, and immutable record of transactions, which is particularly beneficial in a decentralized payroll system.

Implementing smart contracts for payroll automation involves several key steps. First, the payroll process must be thoroughly analyzed to identify the specific tasks that can be automated. This typically includes calculating wages, deductions, and bonuses, as well as generating payment receipts. Once the automatable tasks are identified, the smart contract code can be developed using a blockchain platform such as Ethereum. The code should include all the necessary logic to execute the payroll process, such as conditional statements for calculating different types of payments and triggers for initiating the payment process.

After the smart contract code is developed, it must be tested and audited to ensure its accuracy and security. This involves simulating various payroll scenarios to verify that the contract behaves as expected under different conditions. Additionally, the contract should be reviewed by security experts to identify and address any potential vulnerabilities. Once the contract has passed testing and auditing, it can be deployed to the blockchain network, where it will run autonomously, executing the payroll process according to the predefined rules.

One of the significant advantages of using smart contracts for payroll automation is the reduction in human error. By removing the need for manual intervention in the payroll process, the risk of mistakes such as miscalculations, late payments, or incorrect deductions is greatly minimized. Furthermore, smart contracts can improve the efficiency of payroll processing, as they can execute tasks much faster than human payroll administrators. This can lead to cost savings for corporations and improve employee satisfaction by ensuring timely and accurate payments.

However, there are also challenges associated with implementing smart contracts for payroll automation. One major challenge is the need for integration with existing payroll systems and data sources. This can be a complex process, requiring careful planning and coordination to ensure a seamless transition to the new automated system. Additionally, there may be regulatory and compliance considerations that need to be addressed, as payroll processing is subject to various laws and regulations. Corporations must ensure that their smart contract-based payroll system complies with all relevant legal requirements.

In conclusion, smart contracts have the potential to transform payroll processes by automating tasks, reducing human error, and improving efficiency. While there are challenges to implementation, the benefits of using smart contracts for payroll automation are significant, making it an attractive option for corporations looking to decentralize and streamline their payroll operations.

Exploring Payroll Deductions for Cash Basis Taxpayers: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Tokenization of Compensation: Exploring the concept of tokenizing employee compensation for easier management and trading

Tokenization of compensation involves converting traditional forms of employee remuneration, such as salaries and bonuses, into digital tokens that can be easily managed and traded on blockchain platforms. This innovative approach offers several potential benefits for corporations looking to decentralize their payroll systems. Firstly, tokenization can enhance transparency and accountability in compensation management, as all transactions are recorded on an immutable ledger. This can help to build trust among employees and stakeholders, as well as reduce the risk of fraud and errors.

Moreover, tokenization can facilitate more efficient and cost-effective payroll processing. By automating the conversion of fiat currencies into digital tokens, corporations can streamline their payroll operations and reduce the need for manual intervention. This can lead to significant savings in terms of time and resources, as well as minimize the risk of human error. Additionally, tokenization can enable employees to access their compensation more quickly and easily, as digital tokens can be transferred instantly and securely.

Another key advantage of tokenization is that it can provide employees with greater flexibility and control over their compensation. By allowing employees to trade their tokens on open markets, corporations can empower their workforce to make informed decisions about their financial future. This can lead to increased employee satisfaction and retention, as well as attract top talent to the organization. Furthermore, tokenization can enable corporations to offer more competitive compensation packages, as they can provide employees with a wider range of financial options and incentives.

However, it is important to note that tokenization also presents several challenges and risks. For instance, the volatility of digital tokens can make it difficult for employees to predict their earnings, which can lead to financial uncertainty and insecurity. Additionally, the regulatory landscape surrounding digital tokens is still evolving, which can create legal and compliance risks for corporations. To mitigate these risks, corporations must carefully consider the implications of tokenization and develop robust strategies for managing and mitigating potential issues.

In conclusion, tokenization of compensation offers a promising approach for corporations looking to decentralize their payroll systems. By leveraging blockchain technology, corporations can enhance transparency, efficiency, and flexibility in their compensation management, while also providing employees with greater control over their financial future. However, it is crucial for corporations to carefully evaluate the risks and challenges associated with tokenization and develop comprehensive strategies for addressing these issues.

Accessing Payroll Records: A Guide for California Employees

You may want to see also

Explore related products

![]()

Decentralized Finance (DeFi) Solutions: Leveraging DeFi platforms to facilitate payroll operations without traditional banking intermediaries

Decentralized Finance (DeFi) solutions offer a promising avenue for corporations to streamline payroll operations without relying on traditional banking intermediaries. By leveraging DeFi platforms, companies can potentially reduce transaction costs, increase efficiency, and provide employees with more flexible and accessible payment options.

One key advantage of DeFi solutions is the ability to facilitate cross-border payments with greater ease and lower fees compared to traditional banking systems. This is particularly beneficial for corporations with a global workforce, as it can help to simplify the process of managing payroll across different countries and currencies.

DeFi platforms also enable the use of smart contracts, which can automate various aspects of payroll processing, such as calculating wages, deducting taxes, and distributing payments. This automation can help to reduce the risk of human error and increase the speed and accuracy of payroll operations.

Furthermore, DeFi solutions can provide employees with more control over their financial assets by allowing them to access their wages in real-time and choose from a variety of payment methods, including cryptocurrencies. This can be particularly appealing to employees who are looking for more flexible and innovative ways to manage their finances.

However, it is important to note that DeFi solutions are still in their early stages of development and adoption, and there are potential risks and challenges associated with their use. For example, the lack of regulatory oversight and the volatility of cryptocurrency markets can pose significant risks to both corporations and employees.

In conclusion, while DeFi solutions offer a range of potential benefits for payroll operations, it is crucial for corporations to carefully consider the risks and challenges involved before implementing these solutions. By doing so, they can ensure that they are making informed decisions that align with their business goals and values.

Canceling an ADP Payroll Run: Possibilities and Procedures

You may want to see also

Explore related products

![FlexiStation Employee Management Business Edition [PC Download]](https://m.media-amazon.com/images/I/51jDUHmoT1L._AC_UL320_.jpg)

![]()

Regulatory Compliance: Navigating the legal and regulatory landscape to ensure decentralized payroll systems meet all necessary standards

Navigating the regulatory landscape is a critical aspect of implementing decentralized payroll systems. Corporations must ensure that their decentralized payroll solutions comply with all relevant laws and regulations, which can vary significantly by jurisdiction. This involves a thorough understanding of local labor laws, tax regulations, and data protection requirements.

One of the key challenges in achieving regulatory compliance for decentralized payroll systems is the need to adapt to different legal frameworks across various countries and regions. For instance, in the European Union, companies must adhere to the General Data Protection Regulation (GDPR) when handling employee data, while in the United States, they must comply with the Fair Labor Standards Act (FLSA) and other state-specific laws.

To ensure compliance, corporations should conduct a comprehensive risk assessment to identify potential legal and regulatory pitfalls. This assessment should include a review of the payroll system's architecture, data storage and processing practices, and security measures. Based on the findings, companies can implement necessary safeguards, such as encryption, access controls, and regular audits, to mitigate risks and ensure adherence to legal standards.

Another important consideration is the need to maintain accurate and transparent records of all payroll transactions. Decentralized systems should be designed to provide clear audit trails and reporting capabilities, enabling companies to demonstrate compliance with financial and labor regulations. This may involve integrating blockchain technology or other immutable ledger solutions to ensure the integrity and traceability of payroll data.

Ultimately, achieving regulatory compliance for decentralized payroll systems requires a proactive and ongoing effort. Corporations must stay abreast of changing laws and regulations, continuously monitor their systems for compliance, and be prepared to adapt to new requirements as they emerge. By taking a strategic and comprehensive approach to regulatory compliance, companies can minimize legal risks and ensure the successful implementation of decentralized payroll solutions.

Understanding 1099 Forms: Can They Be Included in Payroll?

You may want to see also

Frequently asked questions

Yes, a corporation can decentralize its payroll system. Decentralization involves distributing payroll processing across multiple locations or departments rather than centralizing it in one place. This can be achieved through the use of payroll software that allows for multiple users and departments to manage payroll tasks.

Decentralizing payroll can offer several benefits, including increased efficiency, reduced processing time, and improved accuracy. By allowing multiple departments to handle payroll tasks, the workload is distributed more evenly, which can lead to faster processing and fewer errors. Additionally, decentralizing payroll can provide better visibility and control over payroll data, as well as improve compliance with local regulations.

One of the main challenges a corporation might face when decentralizing its payroll system is ensuring consistency and accuracy across all departments. With multiple users handling payroll tasks, there is a risk of discrepancies and errors. To mitigate this, it is important to have robust payroll software in place that can track and reconcile payroll data across different departments. Additionally, training and support may be needed to ensure that all users are familiar with the payroll system and processes.

Ensuring data security is crucial when decentralizing payroll, as sensitive employee information is involved. To maintain data security, a corporation should implement strong access controls, such as requiring multi-factor authentication and limiting access to payroll data based on user roles and permissions. Additionally, data encryption should be used to protect payroll data both in transit and at rest. Regular security audits and training on data security best practices can also help to minimize the risk of data breaches.