The question of whether a government employee can claim insurance premiums on taxes is a common one, particularly in the United States. The answer, as with many tax-related inquiries, depends on several factors, including the type of insurance, the employee's tax filing status, and specific IRS regulations. Generally, health insurance premiums paid by an employer on behalf of an employee are considered tax-free benefits and are not taxable to the employee. However, if an employee pays for insurance premiums out-of-pocket, they may be able to deduct these expenses on their tax return, provided they meet certain criteria. For instance, the premiums must be for a qualified health plan, and the employee must itemize their deductions on Schedule A of Form 1040. It's also important to note that the Affordable Care Act (ACA) has introduced additional complexities, such as the requirement for individuals to maintain minimum essential coverage or face a penalty. Given these nuances, it's advisable for government employees to consult with a tax professional or refer to IRS publications for detailed guidance on this matter.

| Characteristics | Values |

|---|---|

| Country | United States |

| Tax Form | Form 1040, Schedule A |

| Deduction Type | Itemized deduction |

| Category | Medical and dental expenses |

| Eligibility | Government employees with health insurance |

| Conditions | Premiums must be for the employee, spouse, or dependents |

| Limitations | Only premiums paid out-of-pocket are deductible |

| Maximum Deduction | No specific maximum, subject to overall itemized deduction limits |

| Documentation Required | Proof of payment, insurance policy details |

| Impact on Tax Liability | Reduces taxable income, potentially lowering tax owed |

| Alternatives | Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs) |

| Additional Considerations | May affect eligibility for other tax credits or deductions |

| Recent Changes | Tax Cuts and Jobs Act (2017) modified the deduction rules |

| Future Outlook | Subject to legislative changes and IRS guidance |

| Professional Advice | Consultation with a tax professional recommended for complex situations |

Explore related products

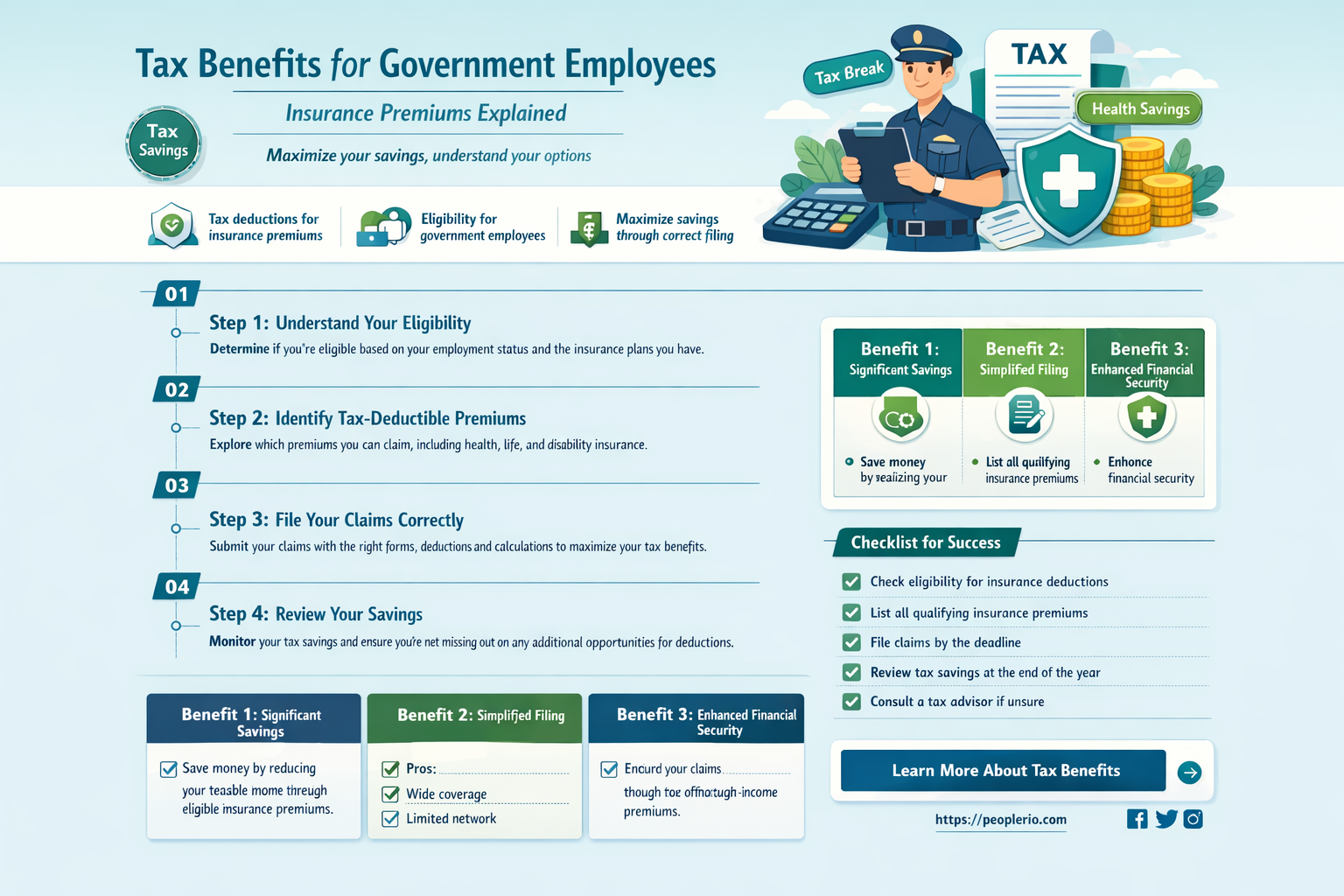

What You'll Learn

- Eligibility Criteria: Understand the conditions under which a government employee can claim insurance premiums on taxes

- Types of Insurance: Identify which insurance types (health, life, disability) are eligible for tax deductions

- Documentation Required: List the necessary documents and forms needed to claim insurance premiums on tax returns

- Tax Laws and Regulations: Overview of relevant tax laws and IRS regulations that pertain to insurance premium deductions

- Calculation of Deductions: How to calculate the amount of insurance premiums that can be deducted from taxable income

![]()

Eligibility Criteria: Understand the conditions under which a government employee can claim insurance premiums on taxes

To claim insurance premiums on taxes, a government employee must meet specific eligibility criteria. These criteria are designed to ensure that only those who are genuinely entitled to the benefit can claim it. The first and foremost condition is that the employee must have paid the insurance premiums out of their own pocket. This means that if the premiums were paid by the government or any other third party, the employee would not be eligible to claim them on their taxes.

Another important criterion is that the insurance policy must be a qualifying one. This typically means that the policy must provide coverage for medical expenses, hospitalization, or long-term care. The policy must also be in force for the entire tax year for which the employee is claiming the premiums. If the policy was only in force for part of the year, the employee would only be able to claim the premiums for that portion of the year.

The employee must also be able to provide proof of the premiums paid. This can be done by obtaining a statement from the insurance company detailing the premiums paid over the course of the year. The employee must keep this statement for their records and be prepared to provide it to the tax authorities if requested.

It is also important to note that there may be a cap on the amount of premiums that can be claimed. This cap is typically set by the tax authorities and may vary depending on the employee's income level or other factors. The employee should check with the tax authorities to determine the current cap and ensure that they are not claiming more than the allowed amount.

Finally, the employee must file the appropriate tax forms to claim the insurance premiums. This typically involves filling out a separate form for each type of insurance coverage being claimed. The forms must be filed with the employee's tax return for the year in which the premiums were paid. If the employee is unsure about how to file the forms or has any other questions about claiming insurance premiums on their taxes, they should consult with a tax professional for assistance.

Unlocking the Truth: Can You Deduct Employee Wages on Taxes?

You may want to see also

Explore related products

![]()

Types of Insurance: Identify which insurance types (health, life, disability) are eligible for tax deductions

Government employees, like other taxpayers, may be able to claim certain insurance premiums as tax deductions, but the eligibility criteria can be complex. The types of insurance that may qualify for tax deductions include health, life, and disability insurance. However, not all premiums paid for these types of insurance will be deductible.

For health insurance, premiums paid for coverage under a high-deductible health plan (HDHP) may be eligible for deduction if the employee is not enrolled in Medicare and if the premiums are not paid or reimbursed by the employer. Additionally, premiums paid for long-term care insurance may also be deductible, subject to certain limits based on the employee's age.

Life insurance premiums are generally not deductible, but there are some exceptions. For example, if the life insurance policy is part of a group term life insurance plan provided by the employer, the premiums may be deductible if the employee pays them out of pocket. However, if the employer pays the premiums or reimburses the employee, the premiums are not deductible.

Disability insurance premiums may be deductible if the employee pays them out of pocket and if the policy provides coverage for the employee's own disability. However, if the employer pays the premiums or reimburses the employee, the premiums are not deductible. Additionally, premiums paid for disability insurance provided through a government-sponsored program, such as the Federal Employees Retirement System (FERS), are not deductible.

It is important to note that the rules for deducting insurance premiums can be complex and may change over time. Government employees should consult with a tax professional or refer to the latest IRS guidance to determine their eligibility for deducting insurance premiums on their taxes.

Maximizing Tax Benefits: Spouse Employee Health Insurance Deductions Explained

You may want to see also

Explore related products

![]()

Documentation Required: List the necessary documents and forms needed to claim insurance premiums on tax returns

To claim insurance premiums on tax returns, government employees must gather and submit several key documents. The primary form required is IRS Form 1040, which is the standard individual income tax return form. On this form, taxpayers will report their income, deductions, and credits, including the deduction for insurance premiums.

In addition to Form 1040, government employees may need to provide documentation of their insurance premiums paid during the tax year. This can include receipts, invoices, or statements from the insurance provider detailing the premiums paid and the type of insurance coverage. It's important to note that only premiums paid for health insurance, long-term care insurance, and certain other types of insurance may be deductible.

If the government employee is claiming the deduction for health insurance premiums, they may also need to provide documentation of their health insurance coverage. This can include a copy of their health insurance card, a statement from their employer confirming their health insurance coverage, or a Form 1095, which is a tax form that employers use to report health insurance coverage to the IRS.

For long-term care insurance premiums, government employees may need to provide additional documentation, such as a copy of their long-term care insurance policy and a statement from the insurance provider detailing the premiums paid. It's important to note that the deduction for long-term care insurance premiums is subject to certain limits and phase-outs based on the taxpayer's age and income.

Finally, government employees should also keep records of any other relevant documents, such as cancelled checks or credit card statements, that can help substantiate their insurance premium payments. By gathering and organizing these documents, government employees can ensure that they are able to claim the maximum deduction for insurance premiums on their tax returns.

Navigating Tax Season: A Guide for Contract Employees

You may want to see also

Explore related products

![]()

Tax Laws and Regulations: Overview of relevant tax laws and IRS regulations that pertain to insurance premium deductions

The U.S. tax code allows certain deductions for insurance premiums, but the specifics can be complex, especially for government employees. According to IRS regulations, premiums for health insurance, dental insurance, and long-term care insurance may be deductible if they meet certain criteria. However, the rules differ depending on whether the insurance is provided through an employer or purchased individually.

For government employees, the deduction of insurance premiums is often limited. If the insurance is provided as part of their employment benefits, the premiums are generally not deductible. This is because such premiums are considered tax-free benefits provided by the employer. However, if a government employee pays for additional insurance coverage out-of-pocket, they may be able to deduct these premiums, subject to certain limits and conditions.

One important consideration is the type of insurance policy. For example, premiums for life insurance policies are not deductible, while premiums for long-term care insurance may be deductible if they meet certain requirements. Additionally, the IRS has specific rules regarding the deduction of premiums for health savings accounts (HSAs) and flexible spending accounts (FSAs), which are often used by government employees to cover medical expenses.

To claim insurance premiums on their taxes, government employees must itemize their deductions on Schedule A of Form 1040. This requires keeping detailed records of all insurance premiums paid during the year, as well as any other deductible expenses. It's also important to note that the deduction for insurance premiums is subject to the overall limit on itemized deductions, which can vary depending on the taxpayer's income and filing status.

In conclusion, while government employees may be able to deduct certain insurance premiums on their taxes, the rules are complex and require careful attention to detail. It's essential to understand the specific requirements and limitations set forth by the IRS to ensure compliance and maximize potential deductions.

Unlocking Tax Benefits: Key Employee Premiums Explained

You may want to see also

Explore related products

![]()

Calculation of Deductions: How to calculate the amount of insurance premiums that can be deducted from taxable income

To calculate the amount of insurance premiums that can be deducted from taxable income, government employees must follow a specific set of guidelines. First, it's essential to identify the type of insurance premiums eligible for deduction. Typically, these include health insurance, dental insurance, and long-term care insurance premiums. Once the eligible premiums are determined, the employee must gather the necessary documentation, such as insurance premium statements or receipts, to substantiate the deduction.

The calculation process involves determining the total amount of eligible premiums paid during the tax year. This total is then used to calculate the deduction, which is limited to the amount of premiums that exceed 10% of the employee's adjusted gross income (AGI). For example, if an employee's AGI is $50,000 and they paid $6,000 in eligible insurance premiums, they can deduct $1,000 from their taxable income ($6,000 - $5,000 = $1,000).

It's important to note that the deduction for insurance premiums is an above-the-line deduction, meaning it can be taken even if the employee does not itemize their deductions. This makes it a valuable tax benefit for government employees who may not have enough itemized deductions to exceed the standard deduction.

When calculating the deduction, government employees should also be aware of any employer-provided insurance benefits. If the employer pays for any portion of the insurance premiums, that amount is not deductible by the employee. Additionally, if the employee receives a tax credit for health insurance premiums through the Affordable Care Act (ACA), they cannot also deduct those premiums from their taxable income.

To maximize the deduction, government employees should consider contributing to a Health Savings Account (HSA) or a Flexible Spending Account (FSA). These accounts allow employees to set aside pre-tax dollars to pay for eligible medical expenses, including insurance premiums. By using these accounts, employees can reduce their taxable income and potentially increase their insurance premium deduction.

In conclusion, calculating the deduction for insurance premiums requires careful attention to detail and an understanding of the specific rules and limitations. By following these guidelines and taking advantage of available tax benefits, government employees can minimize their tax liability and maximize their savings.

Unlocking the Tax Benefits of Employee Bonuses: A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, government employees can claim insurance premiums on their taxes under certain conditions. This typically includes health insurance premiums, and sometimes other types of insurance depending on the country's tax laws.

Government employees can usually claim health insurance premiums on their taxes. In some jurisdictions, they may also be able to claim premiums for other types of insurance, such as life insurance or disability insurance, if these are required as part of their employment.

To claim insurance premiums on their taxes, government employees typically need to itemize their deductions on their tax return. They should keep records of their insurance payments throughout the year and consult with a tax professional or refer to their country's tax guidelines to ensure they are claiming the correct amounts.

Yes, there are often limitations and conditions. For example, the premiums must usually be for the employee themselves, their spouse, or their dependents. Additionally, the employee may need to meet certain income thresholds or other criteria set by their country's tax authority. It's important for government employees to review their country's specific tax laws to understand any restrictions that may apply.