A payroll account and a savings account serve distinct purposes in personal finance. A payroll account is primarily used by employers to deposit employees' wages and salaries, ensuring a smooth and efficient payment process. On the other hand, a savings account is designed to help individuals save money, offering features like interest accrual and easy access to funds when needed. While both types of accounts are essential for managing finances, they cater to different needs and typically have unique characteristics.

| Characteristics | Values |

|---|---|

| Account Type | Payroll and Savings |

| Purpose | Payroll for employee payments, Savings for financial storage |

| Interest Rate | Typically lower for payroll, higher for savings |

| Minimum Balance | Often required for savings, not typically for payroll |

| Fees | May have fees for payroll processing, usually none for savings |

| Accessibility | Payroll may have restricted access, savings generally unrestricted |

| Tax Implications | Payroll subject to tax withholding, savings may have tax advantages |

| Withdrawal Limits | Payroll may have limits on withdrawals, savings generally do not |

| Deposit Limits | Payroll may have limits on deposits, savings generally do not |

| Statements | Payroll may have more frequent statements, savings typically monthly |

Explore related products

What You'll Learn

- Definition of Payroll and Savings Accounts: Understand the fundamental differences between payroll and savings accounts

- Interest Accrual: Explore whether payroll accounts can earn interest like savings accounts

- Withdrawal and Deposit Rules: Compare the withdrawal and deposit regulations for payroll versus savings accounts

- Tax Implications: Investigate the tax consequences of using a payroll account as a savings vehicle

- Employer Restrictions: Examine any employer-imposed limitations on using payroll accounts for savings purposes

![]()

Definition of Payroll and Savings Accounts: Understand the fundamental differences between payroll and savings accounts

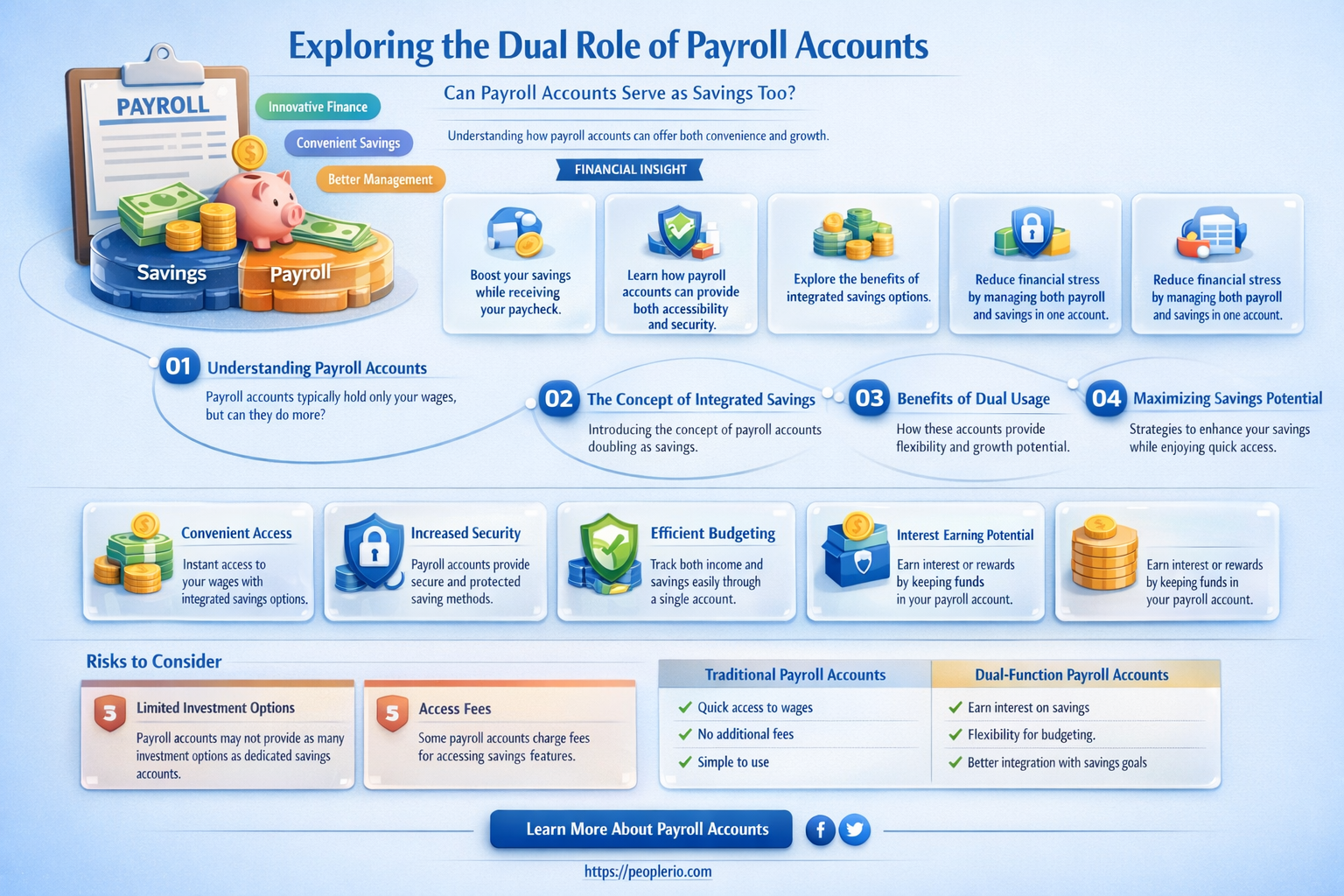

Payroll and savings accounts serve distinct purposes in personal finance, each designed to meet specific financial needs. A payroll account, also known as a checking account, is primarily used for managing day-to-day expenses and receiving direct deposits from employers. It typically offers features such as debit cards, online banking, and bill pay services, making it convenient for handling regular transactions. On the other hand, a savings account is intended for storing money over time, often earning interest on the deposited funds. Savings accounts usually have limitations on the number of withdrawals allowed per month and may require a minimum balance to avoid fees.

One fundamental difference between payroll and savings accounts lies in their liquidity. Payroll accounts provide easy access to funds, allowing individuals to withdraw or transfer money as needed to cover expenses. In contrast, savings accounts are designed to encourage saving by making it less convenient to access the funds frequently. This distinction is crucial for individuals looking to manage their finances effectively, as it helps in segregating funds for immediate use versus long-term goals.

Another key difference is the interest rate offered by each type of account. Payroll accounts typically do not earn interest or offer very low interest rates, as their primary function is to facilitate transactions rather than grow savings. Savings accounts, however, are designed to earn interest on the deposited funds, helping individuals grow their savings over time. The interest rates on savings accounts can vary depending on the financial institution and the specific type of savings account (e.g., high-yield savings, money market accounts).

In summary, while both payroll and savings accounts are essential components of personal finance, they serve different purposes and offer distinct features. Payroll accounts are geared towards managing daily expenses and receiving income, while savings accounts are intended for storing and growing funds over time. Understanding these fundamental differences can help individuals make informed decisions about how to allocate their funds and achieve their financial goals.

Flexibility in Payroll Dates: A Guide for Companies

You may want to see also

Explore related products

![]()

Interest Accrual: Explore whether payroll accounts can earn interest like savings accounts

Payroll accounts are typically used by employers to deposit employees' wages and are not traditionally designed to earn interest. However, some financial institutions offer payroll accounts with interest-earning capabilities, blurring the lines between payroll and savings accounts. This hybrid feature can be an attractive option for both employers and employees looking to maximize their financial benefits.

One unique angle to explore is the potential for payroll accounts to serve as a tool for financial wellness programs. Employers could leverage interest-earning payroll accounts to incentivize employees to save more, offering a higher interest rate for larger balances or for employees who meet certain savings goals. This approach could help employees build emergency funds and improve their overall financial health, while also benefiting employers through increased employee satisfaction and retention.

Another aspect to consider is the regulatory environment surrounding payroll accounts. Unlike savings accounts, payroll accounts are subject to specific laws and regulations governing wage payments and deductions. Employers must ensure that any interest earned on payroll accounts is properly reported and withheld for tax purposes, and that employees are aware of their rights and responsibilities regarding the account.

From a practical standpoint, implementing an interest-earning payroll account requires careful consideration of the account's terms and conditions. Employers should compare interest rates, fees, and minimum balance requirements across different financial institutions to find the best option for their business and employees. Additionally, employers should establish clear guidelines for account usage and management, including how interest will be distributed and how employees can access their funds.

In conclusion, while payroll accounts are not typically designed to earn interest, some financial institutions offer hybrid options that can provide both employers and employees with additional financial benefits. By exploring the unique features and regulatory considerations of interest-earning payroll accounts, employers can make informed decisions about whether this type of account is right for their business and employees.

Contributing to Your HSA Outside Payroll: What You Need to Know

You may want to see also

Explore related products

![]()

Withdrawal and Deposit Rules: Compare the withdrawal and deposit regulations for payroll versus savings accounts

Payroll and savings accounts serve distinct purposes, and their withdrawal and deposit rules reflect these differences. Payroll accounts are primarily designed to receive and disburse funds for employee compensation, while savings accounts are intended for storing and growing money over time.

One key difference in withdrawal rules is that payroll accounts often have more frequent and regular withdrawals, corresponding to pay periods, whereas savings accounts typically have less frequent withdrawals. Payroll accounts may also have restrictions on the amount that can be withdrawn in a single transaction or within a certain timeframe to prevent overdrafts and ensure funds are available for payroll processing. In contrast, savings accounts usually offer more flexibility in withdrawal amounts and frequency, although some accounts may have minimum balance requirements or withdrawal limits to encourage saving.

Deposit rules also vary between payroll and savings accounts. Payroll accounts are generally set up to receive regular, recurring deposits from an employer, and these deposits are often automated. Savings accounts, on the other hand, may receive deposits from various sources, including direct deposits, transfers from other accounts, or cash deposits. Some savings accounts offer features like automatic transfers from checking accounts or employer contributions to encourage saving, while payroll accounts typically do not have these features.

Another important consideration is the interest rates and fees associated with each type of account. Payroll accounts often have lower interest rates and may charge fees for certain transactions, such as overdrafts or account maintenance. Savings accounts, particularly high-yield savings accounts, typically offer higher interest rates to encourage saving and may have fewer fees, although some accounts may charge fees for excessive withdrawals or account maintenance.

In summary, while both payroll and savings accounts involve depositing and withdrawing funds, their rules and regulations are tailored to their specific purposes. Payroll accounts are designed for regular, automated transactions related to employee compensation, while savings accounts offer more flexibility and features to encourage saving and growing money over time. Understanding these differences can help individuals make informed decisions about managing their finances and choosing the right type of account for their needs.

Can LLC Member Distributions Be Reclassified as Payroll?

You may want to see also

Explore related products

![]()

Tax Implications: Investigate the tax consequences of using a payroll account as a savings vehicle

Using a payroll account as a savings vehicle can have significant tax implications. One of the primary concerns is that payroll accounts are typically considered taxable income. This means that any money deposited into the account may be subject to income tax, depending on the jurisdiction. Additionally, if the account earns interest, that interest may also be taxable. It's important to note that the tax treatment of payroll accounts can vary depending on the country and specific tax laws in place.

Another consideration is the potential for penalties and fines. If the payroll account is not properly reported to the relevant tax authorities, there may be penalties for non-compliance. Furthermore, if the account is used to avoid paying taxes, there may be additional fines and legal consequences. It's crucial to ensure that all tax obligations are met and that the account is used in accordance with local tax laws.

One way to mitigate the tax implications is to use a payroll account that is specifically designed for savings. These accounts may offer tax-advantaged status, allowing individuals to save money on taxes. For example, some countries offer tax-free savings accounts or accounts with preferential tax treatment. It's important to research and understand the specific tax benefits and limitations of these accounts before using them as a savings vehicle.

It's also worth considering the impact of using a payroll account as a savings vehicle on overall financial planning. While it may be convenient to use a payroll account for savings, it may not be the most effective strategy in terms of tax efficiency. It may be beneficial to consult with a financial advisor or tax professional to determine the best approach for individual circumstances.

In conclusion, using a payroll account as a savings vehicle can have significant tax implications. It's important to understand the tax treatment of these accounts, potential penalties and fines, and to consider alternative tax-advantaged savings options. Proper planning and consultation with a financial advisor or tax professional can help mitigate the tax consequences and ensure compliance with local tax laws.

Payroll Partnerships: Exploring the Possibilities and Pitfalls

You may want to see also

Explore related products

![]()

Employer Restrictions: Examine any employer-imposed limitations on using payroll accounts for savings purposes

Employers may impose various restrictions on using payroll accounts for savings purposes, which can significantly impact an employee's ability to save money effectively. One common limitation is the requirement to maintain a minimum balance in the payroll account. This ensures that there are sufficient funds available to cover any unexpected expenses or payroll discrepancies. Employees should be aware of this minimum balance requirement and ensure they do not fall below it, as doing so could result in penalties or restrictions on their savings activities.

Another restriction that employers may impose is a limit on the number of payroll deductions that can be made for savings purposes. This could include restrictions on the number of automatic transfers to a savings account or the total amount that can be deducted from each paycheck. Employees should review their employer's policies on payroll deductions to understand any limitations and plan their savings strategy accordingly.

Employers may also have specific rules regarding the timing of payroll deductions for savings. For example, they may require that savings deductions be taken out of the paycheck before other deductions, such as taxes or retirement contributions. This could affect the overall take-home pay and the amount available for savings. Employees should be aware of these timing restrictions and consider how they might impact their overall financial planning.

In some cases, employers may offer their own savings programs or incentives, such as matching contributions to a savings account or offering a separate savings plan. Employees should carefully review these programs to understand any eligibility requirements, contribution limits, or withdrawal restrictions. By taking advantage of employer-sponsored savings programs, employees can potentially increase their savings more effectively.

It is important for employees to carefully review their employer's policies and restrictions on using payroll accounts for savings purposes. By understanding these limitations, employees can develop a savings strategy that complies with their employer's requirements while still helping them achieve their financial goals.

Retroactive 401(k) Contributions: Can Payroll Deductions Be Credited to Previous Year?

You may want to see also

Frequently asked questions

Typically, a payroll account is designed to receive and manage direct deposits of an employee's wages and may not have the same features as a traditional savings account, such as interest accrual or withdrawal limitations. However, some financial institutions may offer hybrid accounts that combine payroll and savings features.

Payroll accounts offer several benefits, including the convenience of having wages deposited directly, reducing the risk of lost or stolen checks, and often providing access to funds a day or two earlier than with a paper check. Additionally, they can help with budgeting and financial management by allowing for automatic transfers to other accounts.

A payroll account is specifically designed to receive and manage direct deposits of wages, while a checking account is a more general-purpose account used for depositing checks, cash, and other funds, as well as making withdrawals and payments. Payroll accounts may have fewer fees and restrictions compared to checking accounts, but they might also lack some of the features and flexibility.

While traditional payroll accounts may not earn interest, some financial institutions offer interest-bearing payroll accounts or hybrid accounts that combine payroll and savings features. These accounts can earn interest on the balance, similar to a savings account, providing an additional incentive for employees to use direct deposit.