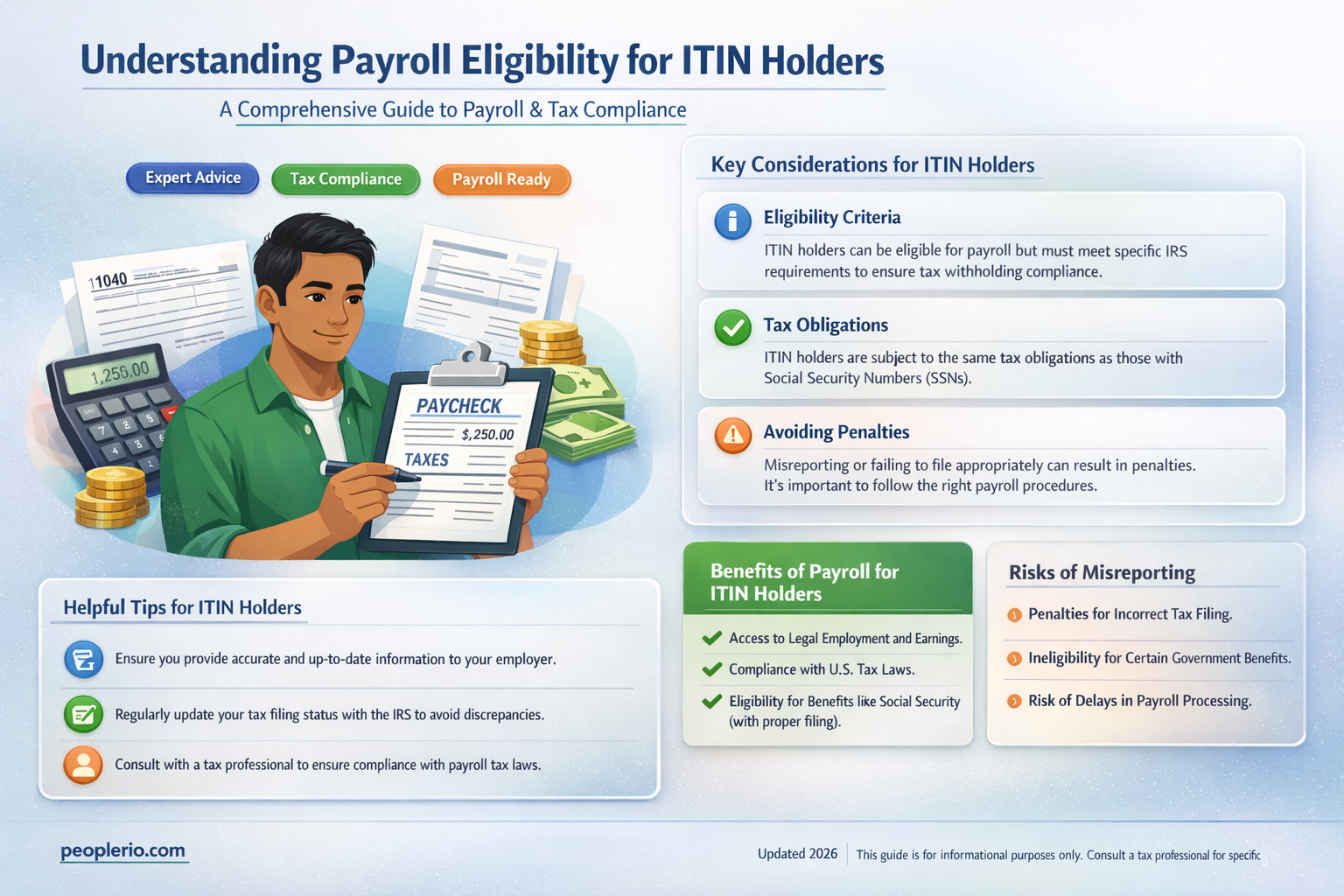

An Individual Taxpayer Identification Number (ITIN) is a unique tax processing number issued by the Internal Revenue Service (IRS) to individuals who are required to have a U.S. taxpayer identification number but who do not have, and are not eligible to obtain, a Social Security Number (SSN). This includes non-resident aliens, foreign nationals, and others who may need to file a U.S. tax return or be claimed as a dependent on one. A common question arises regarding whether a person with an ITIN can be on payroll. The answer is yes; individuals with ITINs can be employed and placed on payroll. However, there are specific guidelines and requirements that both the employer and the employee must follow to ensure compliance with U.S. tax laws. Employers must verify the ITIN and ensure that the individual is authorized to work in the United States. Additionally, the employee must provide the necessary documentation to support their ITIN and work authorization status. It is crucial for both parties to understand their responsibilities to avoid any legal or tax-related issues.

| Characteristics | Values |

|---|---|

| ITIN Definition | An Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the United States Internal Revenue Service (IRS) to individuals who are required to have a U.S. taxpayer identification number but who do not have, and are not eligible to obtain, a Social Security Number (SSN). |

| Purpose of ITIN | It is used for tax purposes, such as reporting income and claiming tax benefits. |

| Eligibility for Payroll | Yes, a person with an ITIN can be on payroll. Employers may hire individuals with ITINs and include them in their payroll systems. |

| Tax Withholding | Employers are required to withhold federal income tax from the wages of employees with ITINs, just as they would for employees with SSNs. |

| Benefits and Deductions | Individuals with ITINs may be eligible for certain tax benefits and deductions, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit (CTC), depending on their specific circumstances. |

| Legal Work Authorization | Having an ITIN does not necessarily mean that an individual is authorized to work in the United States. Employers should verify the work authorization status of all employees, regardless of whether they have an ITIN or an SSN. |

| Reporting Requirements | Employers must report wages and taxes withheld for employees with ITINs on Form W-2, Wage and Tax Statement, and file it with the IRS. |

Explore related products

What You'll Learn

- ITIN Definition: An Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the IRS

- ITIN vs. SSN: ITINs are for tax purposes only and do not authorize work or payroll

- Payroll Requirements: Employers must verify work authorization and use valid identification numbers for payroll processing

- ITIN Use Cases: ITINs are used by non-citizens who need to file taxes but don't have a Social Security Number

- Legal Implications: Using an ITIN for payroll without proper work authorization can lead to legal and financial consequences

![]()

ITIN Definition: An Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the IRS

An Individual Taxpayer Identification Number (ITIN) is a unique identifier assigned by the Internal Revenue Service (IRS) to individuals who are required to have a U.S. taxpayer identification number but who do not have, and are not eligible to obtain, a Social Security Number (SSN). This includes non-resident aliens, foreign nationals, and others who may need to file a U.S. tax return or be claimed as a dependent on someone else's return.

One common question regarding ITINs is whether a person with an ITIN can be on payroll. The answer is yes, but there are specific conditions and requirements that must be met. Employers can use an ITIN to report wages and withhold taxes for employees who do not have an SSN. However, it's important to note that an ITIN is not a work permit and does not authorize an individual to work in the United States. It is solely for tax purposes.

To use an ITIN on payroll, the employer must first verify that the employee is eligible for an ITIN and has obtained one. The employee will need to provide the employer with their ITIN and certify that they are eligible to work in the United States. The employer should then use the ITIN to report the employee's wages on Form W-2 and withhold the appropriate taxes.

It's also important for employers to understand that they have certain responsibilities when using an ITIN on payroll. They must maintain accurate records of the employee's ITIN and ensure that it is used correctly on all tax documents. Employers should also be aware of the potential for identity theft and take steps to protect sensitive information.

In summary, a person with an ITIN can be on payroll, but there are specific requirements and responsibilities that must be met. Employers should verify the employee's eligibility for an ITIN, obtain the necessary certifications, and use the ITIN correctly on all tax documents. By following these guidelines, employers can ensure compliance with U.S. tax laws and protect sensitive information.

Exploring Payroll Options for Non-Profit Organizations

You may want to see also

![]()

ITIN vs. SSN: ITINs are for tax purposes only and do not authorize work or payroll

An Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the Internal Revenue Service (IRS) to individuals who are required to have a U.S. taxpayer identification number but who do not have, and are not eligible to obtain, a Social Security Number (SSN). ITINs are used solely for tax purposes and do not confer any rights or benefits beyond tax processing.

One of the key distinctions between an ITIN and an SSN is that an ITIN does not authorize an individual to work or be on payroll in the United States. An SSN, on the other hand, is required for employment and payroll purposes. Employers are legally obligated to verify an employee's eligibility to work in the U.S. and to use their SSN for payroll tax reporting.

Individuals with ITINs may still be required to file tax returns and pay taxes on income earned in the U.S., but they cannot use their ITIN to obtain employment or be paid through a payroll system. This distinction is crucial for both employers and employees to understand, as it affects hiring practices, payroll administration, and tax compliance.

In summary, while ITINs serve an important role in the U.S. tax system, they do not provide the same rights and benefits as an SSN, particularly when it comes to employment and payroll. Employers must ensure they are using the correct identification numbers for tax reporting and compliance purposes, and individuals with ITINs should be aware of the limitations associated with their tax identification number.

Navigating Payroll Errors: Can Collection Agencies Pursue You?

You may want to see also

![]()

Payroll Requirements: Employers must verify work authorization and use valid identification numbers for payroll processing

Employers have a legal obligation to verify the work authorization of their employees and use valid identification numbers for payroll processing. This requirement is crucial for maintaining compliance with immigration and tax laws. When hiring an individual, employers must ensure that the person is authorized to work in the United States by checking their documentation, such as a Social Security card or an Employment Authorization Document (EAD).

For payroll purposes, employers must use the employee's valid identification number, which is typically their Social Security number (SSN). However, in cases where an individual does not have an SSN, they may be issued an Individual Taxpayer Identification Number (ITIN) by the Internal Revenue Service (IRS). An ITIN is a unique tax processing number issued to individuals who are required to have a U.S. taxpayer identification number but who do not have, or are not eligible to obtain, an SSN.

It is important to note that an ITIN is not a substitute for an SSN and cannot be used for payroll processing. Employers must ensure that they are using the correct identification number for each employee to avoid any legal or financial repercussions. Failure to comply with these requirements can result in penalties, fines, and even criminal charges.

To ensure compliance, employers should establish a thorough onboarding process that includes verifying work authorization and identification numbers. This process should be consistent and applied to all employees, regardless of their immigration status. Additionally, employers should stay up-to-date on any changes to immigration and tax laws that may affect their payroll processing procedures.

In summary, employers must take the necessary steps to verify work authorization and use valid identification numbers for payroll processing. This includes checking documentation, using the correct identification number, and staying informed about any legal changes. By doing so, employers can maintain compliance with the law and avoid potential penalties.

Navigating Payroll for Loan-Out Employees: A Comprehensive Guide

You may want to see also

![]()

ITIN Use Cases: ITINs are used by non-citizens who need to file taxes but don't have a Social Security Number

ITINs, or Individual Taxpayer Identification Numbers, serve a critical function in the U.S. tax system, particularly for non-citizens who are required to file tax returns but do not have a Social Security Number (SSN). This unique nine-digit number is issued by the Internal Revenue Service (IRS) to ensure that individuals without SSNs can meet their tax obligations and comply with U.S. tax laws.

One common use case for ITINs is for non-resident aliens who earn income in the United States. This could include international students, temporary workers, or investors. Without an ITIN, these individuals would be unable to file tax returns, which is a legal requirement for anyone earning income in the U.S., regardless of their citizenship status.

Another scenario where ITINs are essential is for non-citizen spouses of U.S. citizens or permanent residents. In many cases, these spouses may not be eligible for an SSN but still need to file tax returns if they have income of their own or if they are required to report income jointly with their spouse.

ITINs are also used by non-citizens who are victims of identity theft. In these cases, the IRS may issue an ITIN to help the individual protect their identity and prevent further fraud.

It's important to note that ITINs are not a pathway to citizenship or legal residency. They are strictly for tax purposes and do not confer any rights or benefits beyond the ability to file tax returns.

In conclusion, ITINs play a vital role in ensuring that non-citizens can comply with U.S. tax laws and fulfill their tax obligations. They are a practical solution for individuals who are required to file tax returns but do not have a Social Security Number.

Navigating Payroll Returns: Can a CPA Sign Off on Client Documents?

You may want to see also

![]()

Legal Implications: Using an ITIN for payroll without proper work authorization can lead to legal and financial consequences

Using an Individual Taxpayer Identification Number (ITIN) for payroll purposes without proper work authorization can have serious legal and financial repercussions. This practice is often associated with undocumented immigrants who may not have a Social Security Number (SSN) but still need to file taxes or receive payments. However, it's crucial to understand that an ITIN is not a substitute for a SSN and does not confer legal work status.

From a legal standpoint, employers who knowingly use an ITIN for payroll without verifying proper work authorization may face penalties and fines. The U.S. Immigration and Customs Enforcement (ICE) agency has been known to conduct audits and raids on businesses suspected of employing undocumented workers. These actions can result in significant financial losses for employers, as well as potential criminal charges.

Furthermore, individuals who use an ITIN for payroll without proper work authorization may also face legal consequences. They may be subject to deportation proceedings and could be barred from re-entering the United States. Additionally, they may be required to pay back taxes and penalties, which can be a substantial financial burden.

It's important to note that the use of an ITIN for payroll purposes is not inherently illegal. In fact, the IRS issues ITINs to individuals who are required to have a U.S. taxpayer identification number but who do not have, and are not eligible to obtain, a SSN. However, the key distinction lies in the individual's legal status and the employer's responsibility to verify that status.

To avoid legal and financial consequences, both employers and individuals should ensure that they are in compliance with U.S. immigration and tax laws. Employers should verify the work authorization status of their employees using the E-Verify system, and individuals should consult with an immigration attorney to determine their eligibility for work authorization.

In conclusion, while an ITIN can be a useful tool for tax purposes, its misuse for payroll without proper work authorization can lead to severe legal and financial repercussions. It's essential for both employers and individuals to understand their rights and responsibilities under U.S. law to avoid potential pitfalls.

Exploring Weekly Payroll Options for Nonprofit Organizations

You may want to see also

Frequently asked questions

Yes, a person with an Individual Taxpayer Identification Number (ITIN) can be on payroll. An ITIN is issued by the IRS to individuals who are required to have a U.S. taxpayer identification number but who do not have, and are not eligible to obtain, a Social Security Number (SSN). Employers can use an ITIN to report wages and withhold taxes for employees who do not have an SSN.

Employers hiring someone with an ITIN must follow the same payroll tax rules as for any other employee. This includes withholding federal income tax, Social Security tax, and Medicare tax from the employee's wages. However, the employer should be aware that the employee may not be eligible for certain tax benefits or credits that are available to employees with SSNs. Additionally, the employer may need to provide the employee with a Form 1099-MISC instead of a Form W-2 at the end of the year, depending on the employee's immigration status and the nature of the work performed.

An individual can apply for an ITIN by submitting Form W-7, Application for IRS Individual Taxpayer Identification Number, to the IRS. The form can be downloaded from the IRS website or ordered by phone or mail. Along with the form, the individual must provide proof of identity and foreign status, such as a passport, visa, or other documentation. The IRS will review the application and issue an ITIN if the individual meets the eligibility criteria.