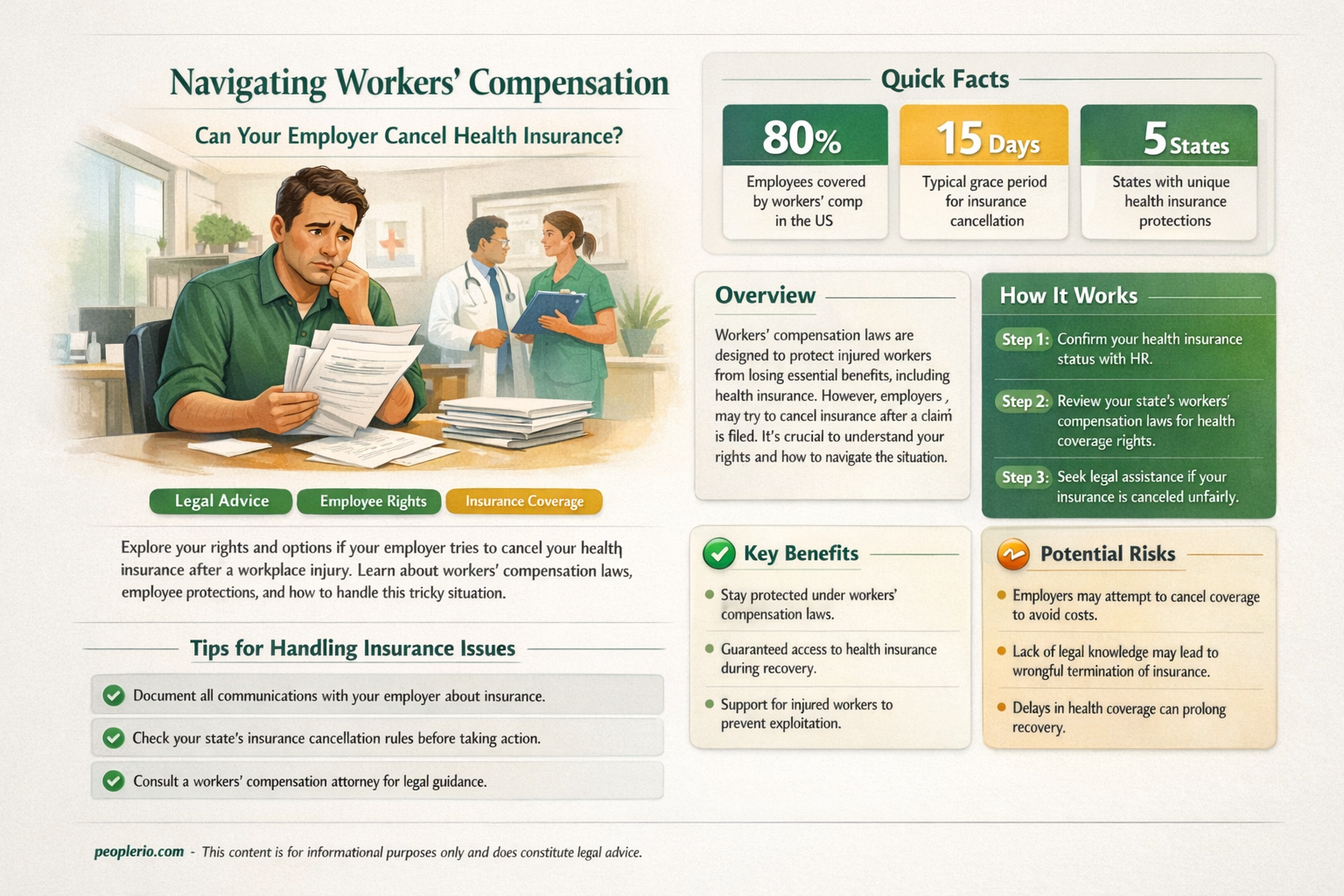

When an employee is injured on the job and requires medical attention, workers' compensation insurance typically covers their healthcare expenses. However, there may be situations where an employer wishes to cancel their employee's health insurance while they are receiving workers' compensation benefits. This could be due to various reasons, such as the employee's injury being deemed ineligible for workers' compensation, the employee's failure to comply with treatment recommendations, or the employer's financial constraints. It is essential to understand the legal implications and requirements surrounding the cancellation of health insurance in such cases, as well as the potential impact on the employee's access to necessary medical care.

| Characteristics | Values |

|---|---|

| Employer's Right | Generally, an employer cannot cancel health insurance while an employee is on workers' compensation. |

| Legal Protection | Workers' compensation laws often protect employees from retaliation or adverse actions by employers. |

| Continuation of Benefits | Health insurance coverage typically continues while an employee is receiving workers' compensation benefits. |

| Exceptions | Certain circumstances, such as fraud or misrepresentation, may allow an employer to cancel health insurance. |

| Notice Requirements | Employers may be required to provide written notice to employees before canceling health insurance. |

| Impact on Workers' Compensation | Canceling health insurance may not affect the employee's eligibility for workers' compensation benefits. |

| State-Specific Regulations | Laws regarding the cancellation of health insurance while on workers' compensation vary by state. |

Explore related products

What You'll Learn

- Legal Protections: Employees on workers' compensation are protected by law from employer retaliation, including cancellation of health insurance

- Workers' Compensation Benefits: These benefits are designed to cover medical expenses and lost wages, and are separate from employer-provided health insurance

- Employer Obligations: Employers are required to maintain workers' compensation insurance, which is different from regular health insurance coverage

- Impact on Health Insurance: Workers' compensation claims can affect employer health insurance premiums, but employers cannot cancel health insurance in response to a claim

- Employee Rights: Employees have the right to continue their health insurance coverage under COBRA or similar state laws, regardless of their workers' compensation status

![]()

Legal Protections: Employees on workers' compensation are protected by law from employer retaliation, including cancellation of health insurance

Employees who are receiving workers' compensation benefits are afforded certain legal protections to ensure they are not unfairly penalized by their employers. One such protection is the prohibition against employer retaliation, which includes the cancellation of health insurance. This safeguard is crucial as it prevents employers from using health insurance as a tool to intimidate or coerce employees who are exercising their rights under workers' compensation laws.

The legal framework protecting employees from such retaliation varies by jurisdiction, but many states have specific statutes in place to address this issue. For instance, some states may have laws that explicitly prohibit employers from cancelling health insurance for employees who are on workers' compensation leave. In other cases, the protection may be implied under broader anti-retaliation laws or regulations.

In practice, this means that if an employer cancels an employee's health insurance while they are on workers' compensation, the employee may have legal recourse. This could include filing a complaint with a state labor agency or pursuing a lawsuit against the employer for retaliatory actions. The consequences for employers who violate these laws can be significant, including fines, reinstatement of benefits, and potentially even punitive damages.

It is important for employees to be aware of their rights under workers' compensation and to understand the legal protections available to them. If an employee believes their employer has retaliated against them by cancelling their health insurance, they should consult with an attorney or a workers' compensation advocate to discuss their options and to ensure they take the appropriate steps to protect their rights.

Overall, the legal protections against employer retaliation, including the cancellation of health insurance, are a critical component of workers' compensation laws. These protections help to ensure that employees are not unfairly penalized for exercising their rights and that they have access to the necessary medical care and benefits while they are recovering from work-related injuries or illnesses.

Arizona Workers' Compensation Insurance: Employer Requirements Explained

You may want to see also

Explore related products

![]()

Workers' Compensation Benefits: These benefits are designed to cover medical expenses and lost wages, and are separate from employer-provided health insurance

Workers' Compensation Benefits are a critical safety net for employees who suffer work-related injuries or illnesses. These benefits are designed to cover medical expenses and lost wages, ensuring that injured workers can focus on their recovery without the added stress of financial hardship. It's important to note that Workers' Compensation is a separate entity from employer-provided health insurance, which means that even if an employer decides to cancel health insurance coverage, Workers' Compensation benefits should remain unaffected.

One of the key aspects of Workers' Compensation is that it provides coverage regardless of who is at fault for the injury. This no-fault system is designed to streamline the process of obtaining benefits and to reduce the potential for litigation. In most cases, Workers' Compensation will cover all necessary medical treatment related to the work injury, as well as a portion of the worker's lost wages. The specific amount of wage replacement varies by state, but it is typically a percentage of the worker's average weekly wage.

In addition to medical and wage benefits, Workers' Compensation may also provide vocational rehabilitation services to help injured workers return to their jobs or to find new employment if they are unable to perform their previous duties. These services can include job training, education, and assistance with job searches. Furthermore, in cases where a worker is permanently disabled due to a work injury, Workers' Compensation may provide long-term disability benefits or a lump-sum payment.

It's crucial for employees to understand their rights under Workers' Compensation and to know how to navigate the claims process. This includes reporting the injury to their employer in a timely manner, seeking appropriate medical treatment, and filing a claim with the state Workers' Compensation board. Employees should also be aware that they have the right to appeal a denial of benefits and to seek legal representation if necessary.

Overall, Workers' Compensation Benefits play a vital role in protecting the financial well-being of injured workers and their families. By providing a separate source of coverage for work-related injuries, Workers' Compensation helps to ensure that employees can recover from their injuries without the added burden of worrying about their finances or their health insurance coverage.

Understanding Workers' Compensation Insurance Costs for Small Businesses

You may want to see also

Explore related products

![]()

Employer Obligations: Employers are required to maintain workers' compensation insurance, which is different from regular health insurance coverage

Employers have a legal obligation to maintain workers' compensation insurance, which is distinct from regular health insurance coverage. This requirement ensures that employees who suffer work-related injuries or illnesses have access to necessary medical care and wage replacement. Workers' compensation insurance is a no-fault system, meaning that employees do not need to prove that their employer was at fault for their injury to receive benefits.

One key aspect of workers' compensation insurance is that it provides coverage for medical expenses related to work injuries, regardless of whether the employee's regular health insurance would cover such expenses. This can include hospital stays, doctor visits, physical therapy, and prescription medications. Additionally, workers' compensation insurance may provide wage replacement benefits if an employee is unable to work due to their injury.

Employers must also be aware of their obligations under the Family and Medical Leave Act (FMLA), which requires covered employers to provide eligible employees with up to 12 weeks of unpaid leave for certain family and medical reasons, including work-related injuries. This means that employers cannot cancel an employee's health insurance coverage while they are on workers' compensation leave, as doing so would violate the FMLA.

Furthermore, employers should be cautious about canceling an employee's health insurance coverage even if they are not on workers' compensation leave. Many states have laws that prohibit employers from retaliating against employees who file workers' compensation claims, and canceling health insurance coverage could be seen as a form of retaliation. Employers should consult with legal counsel before making any decisions about canceling an employee's health insurance coverage.

In summary, employers have a legal obligation to maintain workers' compensation insurance and must be aware of their obligations under the FMLA. Canceling an employee's health insurance coverage while they are on workers' compensation leave is prohibited, and employers should consult with legal counsel before making any decisions about canceling health insurance coverage.

Understanding Workers' Comp Insurance Coverage: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Impact on Health Insurance: Workers' compensation claims can affect employer health insurance premiums, but employers cannot cancel health insurance in response to a claim

Workers' compensation claims can indeed have an impact on employer health insurance premiums. When an employee files a workers' compensation claim, it may lead to an increase in the employer's insurance costs due to the perceived higher risk of workplace injuries. Insurance companies often view workplaces with frequent claims as hazardous environments, which can result in higher premiums to cover potential future claims.

However, it's important to note that employers cannot cancel health insurance in response to a workers' compensation claim. Canceling health insurance as a retaliatory measure against an employee for filing a claim is illegal and can lead to serious legal consequences for the employer. Employees are entitled to maintain their health insurance coverage regardless of whether they have filed a workers' compensation claim.

The impact on health insurance premiums can vary depending on several factors, including the severity and frequency of claims, the size of the employer's workforce, and the employer's claims history. Employers with a history of frequent or severe workers' compensation claims may see a more significant increase in their health insurance premiums compared to those with fewer or less severe claims.

To mitigate the impact of workers' compensation claims on health insurance premiums, employers can take proactive steps to create a safer work environment. This may include implementing safety training programs, conducting regular safety audits, and addressing potential hazards promptly. By reducing the risk of workplace injuries, employers can potentially lower their workers' compensation claims and, in turn, their health insurance premiums.

In conclusion, while workers' compensation claims can affect employer health insurance premiums, employers must remember that they cannot cancel health insurance in response to a claim. Instead, they should focus on creating a safer work environment to reduce the likelihood of claims and the associated costs.

Exploring Workers' Compensation Insurance Requirements for Churches

You may want to see also

Explore related products

![]()

Employee Rights: Employees have the right to continue their health insurance coverage under COBRA or similar state laws, regardless of their workers' compensation status

Under the Consolidated Omnibus Budget Reconciliation Act (COBRA), employees who are covered by a group health plan have the right to continue their health insurance coverage if they experience a qualifying event, such as a reduction in work hours or termination of employment. This right to continuation applies regardless of whether the employee is receiving workers' compensation benefits. COBRA requires employers to provide written notice to employees about their rights under the law, and employees must elect continuation coverage within a specified time frame.

Similar state laws, often referred to as "mini-COBRA" laws, provide additional protections for employees in certain states. These laws may extend the duration of continuation coverage or apply to smaller employers that are not subject to federal COBRA requirements. For example, California's mini-COBRA law, known as the California Continuation Benefits Law, requires employers with 10 or more employees to offer continuation coverage for up to 36 months.

Employers are prohibited from retaliating against employees who exercise their rights under COBRA or similar state laws. This means that an employer cannot cancel an employee's health insurance coverage in retaliation for filing a workers' compensation claim or for electing continuation coverage under COBRA. Such actions would be considered unlawful and could result in legal consequences for the employer.

Employees who are on workers' compensation leave may also be eligible for disability benefits, which can help cover their health insurance premiums while they are unable to work. In some cases, employees may be able to use their accrued paid time off or vacation leave to maintain their health insurance coverage while on workers' compensation leave. It is important for employees to review their employer's policies and consult with a human resources representative or legal advisor to understand their rights and options.

In summary, employees have the right to continue their health insurance coverage under COBRA or similar state laws, regardless of their workers' compensation status. Employers are required to provide notice of these rights and cannot retaliate against employees who exercise them. Employees should be aware of their rights and options for maintaining health insurance coverage while on workers' compensation leave.

Understanding Workers' Compensation Insurance Requirements for Nonprofits

You may want to see also

Frequently asked questions

Generally, an employer cannot cancel health insurance while an employee is on workers' compensation. This is because workers' compensation is a separate system designed to cover work-related injuries and illnesses, and it typically does not affect an employee's health insurance coverage.

While an employee is on workers' compensation, their health insurance premiums are usually still paid by the employer. This is because the employee is still considered an active employee, even though they may not be working due to their injury or illness.

An employer cannot reduce an employee's health insurance coverage while they are on workers' compensation. The employee's health insurance coverage remains the same as it was before they went on workers' compensation.

If an employee's workers' compensation claim is denied, their health insurance coverage may be affected. The employee may need to pay for their own health insurance premiums, or they may be able to get coverage through a government program or a private insurance company.