The question of whether an employer can compel an employee to continue paying for healthcare is a complex one, often governed by specific laws and regulations that vary by jurisdiction. Generally, if an employee has elected to participate in an employer-sponsored health plan, they may be required to contribute a portion of the premiums. However, the extent to which an employer can enforce this obligation, especially after an employee's termination or during a leave of absence, depends on the terms of the plan and applicable laws such as the Affordable Care Act (ACA) in the United States or similar legislation in other countries. Employers must also consider the potential implications of such policies on employee morale and retention, as well as the legal ramifications of non-compliance with healthcare regulations.

Explore related products

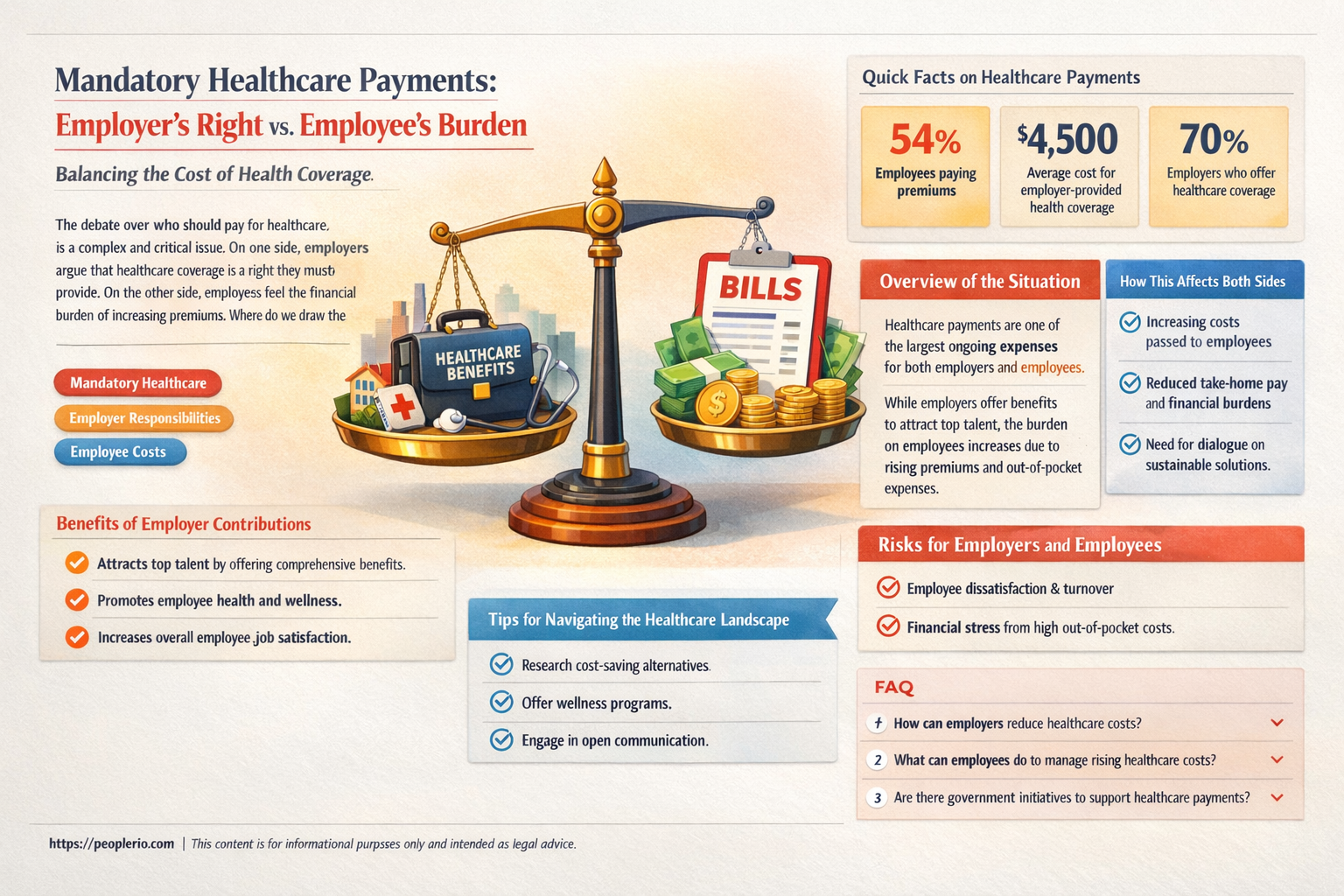

What You'll Learn

- Legal Requirements: Employers must comply with laws like the Affordable Care Act when offering health benefits

- Benefit Design: Employers can choose plans that require employee contributions, but must clearly communicate terms

- Employee Consent: Employees typically agree to benefit terms when enrolling, which may include premium payments

- Payment Methods: Employers can deduct premiums from wages or require direct payments, depending on company policy

- Consequences of Non-Payment: Failure to pay premiums can lead to loss of coverage or financial penalties for employees

![]()

Legal Requirements: Employers must comply with laws like the Affordable Care Act when offering health benefits

Under the Affordable Care Act (ACA), employers are mandated to provide health insurance to their employees if they meet certain criteria. This includes having 50 or more full-time employees. The ACA also sets standards for the coverage that must be offered, ensuring that it is affordable and covers essential health benefits. Employers must contribute at least 50% of the premium cost for employee-only coverage.

One of the key aspects of the ACA is that it prohibits employers from discriminating against employees based on their health status. This means that employers cannot deny coverage or charge higher premiums to employees with pre-existing conditions. Additionally, the ACA requires employers to provide a Summary of Benefits and Coverage (SBC) to employees, which outlines the key features of the health plan in an easy-to-understand format.

Employers must also comply with the ACA's reporting requirements. This includes filing annual reports with the IRS and providing employees with a Form 1095-C, which details the health coverage offered to them. Failure to comply with these requirements can result in penalties for employers.

In terms of the specific question of whether an employer can make an employee finish paying for healthcare, the ACA does not directly address this issue. However, it does provide employees with protections against unfair billing practices. For example, the ACA requires health plans to provide an explanation of benefits (EOB) to employees, which details the amount charged for healthcare services and the amount paid by the plan. This can help employees understand their financial responsibilities and identify any potential errors in billing.

Overall, the ACA sets important legal requirements for employers when it comes to offering health benefits. These requirements are designed to ensure that employees have access to affordable, quality healthcare and are protected from unfair practices. Employers must take steps to comply with these requirements in order to avoid penalties and provide the best possible benefits to their employees.

Understanding Holiday Pay Deductions: What Employees Need to Know

You may want to see also

Explore related products

![]()

Benefit Design: Employers can choose plans that require employee contributions, but must clearly communicate terms

Employers have the flexibility to design benefit plans that include employee contributions, but this flexibility comes with a critical responsibility: clear communication. The terms of these plans must be explicitly stated to avoid confusion and ensure that employees understand their financial obligations. This includes detailing the amount of the contributions, how they will be deducted, and any conditions under which they might change.

One effective way to communicate these terms is through a comprehensive benefits package that outlines all aspects of the plan. This package should be provided to employees during the onboarding process and should be easily accessible for reference at any time. Additionally, employers should consider holding informational sessions to explain the benefits and answer any questions employees may have.

It's also important for employers to be aware of the legal requirements surrounding benefit plan communications. The Employee Retirement Income Security Act (ERISA) mandates that employers provide certain information to employees, including a summary plan description (SPD) and a summary of benefits and coverage (SBC). These documents must be accurate and up-to-date, and employers must ensure that employees receive them in a timely manner.

In addition to meeting legal requirements, clear communication about benefit plans can also help to build trust and transparency between employers and employees. When employees understand the terms of their benefits, they are more likely to feel secure and satisfied with their employment. This, in turn, can lead to increased productivity and retention.

To ensure that benefit plan communications are effective, employers should consider the following best practices:

- Use clear and concise language

- Provide examples or scenarios to illustrate how the plan works

- Make sure the information is easily accessible

- Regularly review and update the plan documents

- Solicit feedback from employees to ensure that the communications are meeting their needs

By following these best practices, employers can create benefit plans that not only meet their business needs but also support the well-being of their employees.

Understanding Lactation Breaks: Employer Obligations and Employee Rights

You may want to see also

Explore related products

![]()

Employee Consent: Employees typically agree to benefit terms when enrolling, which may include premium payments

Employees typically agree to benefit terms when enrolling, which may include premium payments. This consent is often obtained through a benefits enrollment process where employees select their preferred health insurance plans and agree to the associated costs. Employers usually provide a range of options to cater to different employee needs and budgets.

The specifics of employee consent can vary depending on the employer's policies and the health insurance provider. Some employers may require employees to pay a portion of the premium, while others may cover the full cost. It's essential for employees to carefully review the terms and conditions of their selected plan to understand their financial obligations.

In some cases, employers may offer a grace period during which employees can change their minds about their benefit selections. This allows employees to make informed decisions without feeling rushed. However, once the grace period ends, employees are typically locked into their chosen plan for the duration of the plan year.

Employee consent is a crucial aspect of employer-sponsored health insurance. By agreeing to the benefit terms, employees acknowledge their understanding of the plan's features and costs. This helps to ensure that both the employer and the employee are on the same page regarding health insurance coverage and financial responsibilities.

Double COVID Pay for Employees: Is It Possible?

You may want to see also

Explore related products

![]()

Payment Methods: Employers can deduct premiums from wages or require direct payments, depending on company policy

Employers have several options when it comes to collecting health insurance premiums from their employees. One common method is to deduct the premiums directly from the employees' wages. This approach is often seen as convenient for both parties, as it automates the payment process and ensures that premiums are paid on time. However, it's important to note that wage deductions for health insurance premiums are subject to certain legal requirements and restrictions. For example, under the Fair Labor Standards Act (FLSA), employers must ensure that the deductions do not bring the employee's pay below the minimum wage.

Alternatively, employers may require employees to make direct payments for their health insurance premiums. This method can be more administratively burdensome, as it requires employees to submit payments manually, either through payroll deductions or other means. However, it can also provide employees with more flexibility in terms of when and how they pay their premiums. Employers who opt for this approach should establish clear policies and procedures for collecting payments, including deadlines and consequences for late payments.

In some cases, employers may choose to offer a combination of both wage deductions and direct payments. This hybrid approach can help to accommodate the needs and preferences of different employees. For example, an employer might allow employees to opt for wage deductions for a portion of their premiums, while requiring direct payments for the remainder. This can provide employees with greater control over their cash flow while still ensuring that premiums are paid in a timely manner.

Regardless of the payment method chosen, it's crucial for employers to communicate their policies clearly to employees. This includes providing information about the payment schedule, the amount of premiums to be paid, and any consequences for missed payments. Employers should also ensure that their policies comply with all applicable laws and regulations, including those related to wage deductions, employee benefits, and health insurance.

In conclusion, employers have multiple options for collecting health insurance premiums from their employees, including wage deductions, direct payments, and hybrid approaches. Each method has its own advantages and disadvantages, and employers should carefully consider their options before establishing a payment policy. By communicating their policies clearly and ensuring compliance with legal requirements, employers can help to ensure a smooth and efficient payment process for both themselves and their employees.

Deceptive Pay Practices: Understanding Employer-Employee Legal Rights

You may want to see also

Explore related products

![]()

Consequences of Non-Payment: Failure to pay premiums can lead to loss of coverage or financial penalties for employees

If an employer fails to pay the required premiums for employee healthcare, the consequences can be severe. Loss of coverage is a primary concern, leaving employees vulnerable to high medical costs and potential health risks. This can occur when the employer neglects to remit payments to the insurance provider, resulting in the policy lapsing. Employees may then face difficulties in obtaining necessary medical treatments or prescriptions, leading to potential health complications.

Financial penalties can also be imposed on employees if the employer does not fulfill their premium payment obligations. These penalties may include increased deductibles, higher co-payments, or even retroactive charges for services already rendered. In some cases, employees may be required to pay the full cost of their healthcare out-of-pocket if the employer's non-payment results in the cancellation of the insurance policy.

Furthermore, the employer's failure to pay premiums can lead to legal repercussions. Employees may have grounds to sue their employer for breach of contract or negligence, particularly if the non-payment results in significant financial losses or health issues. This can result in costly legal battles and potential settlements or judgments against the employer.

To mitigate these risks, it is essential for employers to prioritize timely premium payments and maintain open communication with their employees regarding any changes or issues with the healthcare plan. Employees, on the other hand, should stay informed about their rights and options under their employer-sponsored healthcare plan and seek legal advice if necessary.

Understanding Your Rights: Can You Legally Refuse Overtime Pay?

You may want to see also

Frequently asked questions

Generally, an employer cannot force an employee to continue paying for healthcare once their employment has ended. However, there may be specific circumstances or contractual agreements that could influence this.

When an employee is terminated, their healthcare coverage typically ends on the last day of their employment. Some employers may offer continuation of coverage under COBRA (Consolidated Omnibus Budget Reconciliation Act) or similar state laws, but this is not mandatory.

An employer is generally not responsible for an employee's healthcare costs after termination, unless there is a specific contractual agreement or legal requirement in place.

An employer may be able to deduct healthcare costs from an employee's final paycheck if the employee has agreed to this in writing or if it is permitted by state law. However, this practice is not common and may be subject to legal restrictions.

After termination, an employee may have several options for healthcare coverage, including purchasing individual insurance, enrolling in a spouse's or partner's employer-sponsored plan, or applying for Medicaid or other government-assisted programs. COBRA or state-specific continuation laws may also provide temporary coverage options.