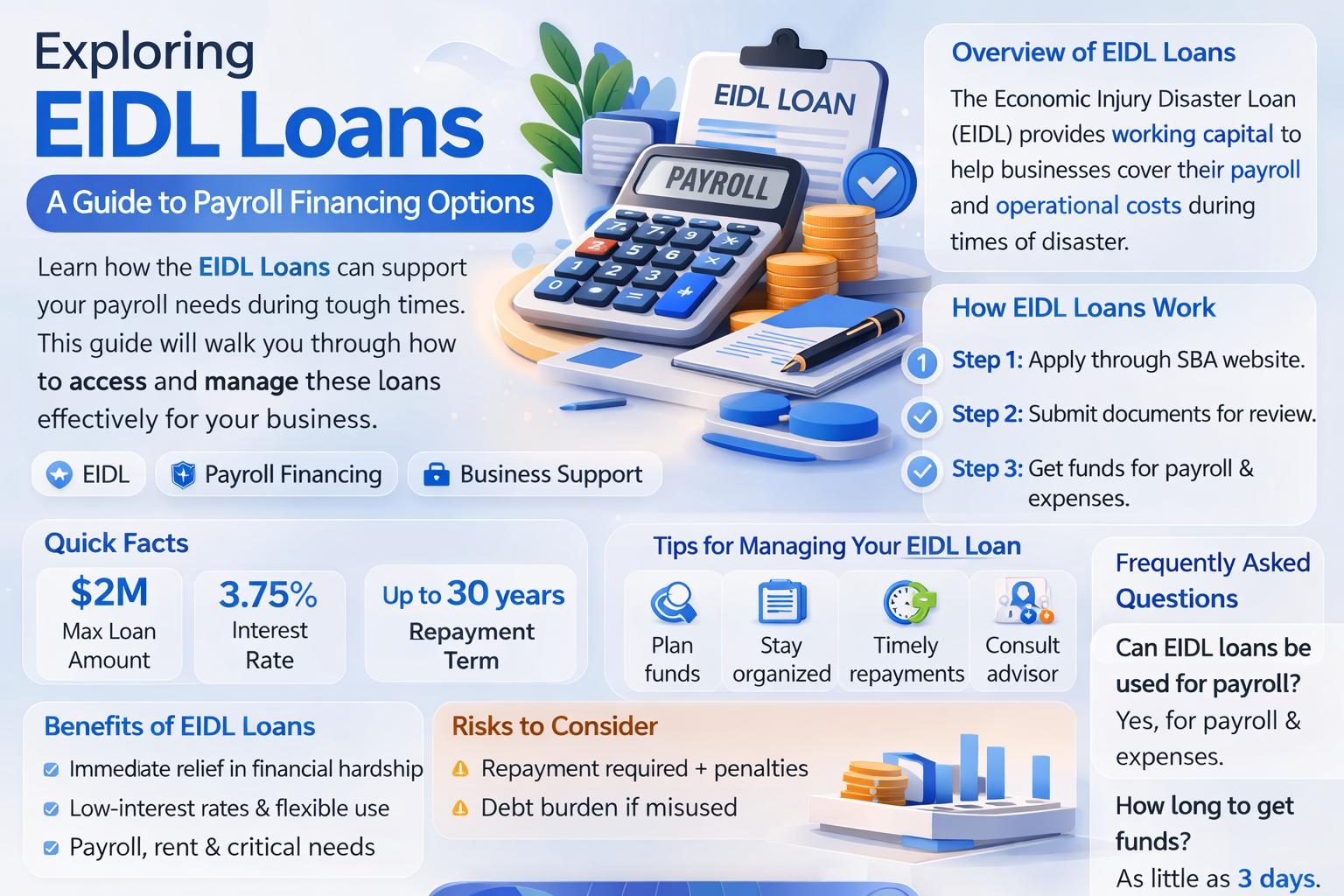

The Economic Injury Disaster Loan (EIDL) program, administered by the Small Business Administration (SBA), provides financial assistance to businesses affected by declared disasters. One common question among business owners is whether EIDL funds can be used for payroll purposes. The answer is yes; EIDL loans can indeed be used to cover payroll expenses. This flexibility allows businesses to maintain operations and support their employees during challenging times. However, it's essential to note that while payroll is an eligible expense, the SBA may have specific guidelines and restrictions on how the funds can be utilized. Business owners should carefully review the terms and conditions of the loan to ensure compliance and make the most of the financial support provided.

Explore related products

What You'll Learn

- EIDL Loan Purpose: Understand the primary uses of EIDL loans, including payroll, rent, and operating expenses

- Payroll Coverage: Learn which employees and payroll-related expenses are eligible for EIDL loan funds

- Loan Limits: Discover the maximum loan amount available and how it can be allocated for payroll costs

- Interest Rates and Terms: Explore the interest rates and repayment terms specific to EIDL loans used for payroll

- Application Process: Get guidance on how to apply for an EIDL loan, including required documentation and eligibility criteria

![]()

EIDL Loan Purpose: Understand the primary uses of EIDL loans, including payroll, rent, and operating expenses

The Economic Injury Disaster Loan (EIDL) program, administered by the Small Business Administration (SBA), provides crucial financial support to businesses affected by declared disasters. One of the primary uses of EIDL loans is to cover payroll expenses, ensuring that employees continue to receive their wages despite the economic challenges posed by the disaster. This is particularly important for small businesses, which often operate on thin profit margins and may not have the financial reserves to maintain payroll without assistance.

In addition to payroll, EIDL loans can also be used to cover rent and operating expenses. This flexibility allows businesses to allocate funds where they are most needed, whether it's to keep the lights on, maintain inventory levels, or cover other essential costs. By providing a source of long-term, low-interest financing, EIDL loans help businesses to recover and rebuild in the aftermath of a disaster.

To be eligible for an EIDL loan, businesses must be located in a declared disaster area and demonstrate that they have suffered substantial economic injury as a result of the disaster. The loan amount is based on the business's actual economic injury, up to a maximum of $2 million. The SBA determines the interest rate for each loan, which is typically lower than rates offered by private lenders.

When applying for an EIDL loan, businesses should be prepared to provide detailed financial information, including tax returns, profit and loss statements, and balance sheets. They should also be able to demonstrate their ability to repay the loan, which may require providing collateral or a personal guarantee from the business owner.

In conclusion, EIDL loans serve as a vital lifeline for businesses facing economic hardship due to disasters. By providing funds for payroll, rent, and operating expenses, these loans help businesses to maintain their operations and support their employees during difficult times. With favorable terms and flexible usage, EIDL loans are an essential tool for disaster recovery and resilience.

Understanding Payroll Adjustments: Can Employers Dock Your Pay?

You may want to see also

Explore related products

![]()

Payroll Coverage: Learn which employees and payroll-related expenses are eligible for EIDL loan funds

The Economic Injury Disaster Loan (EIDL) program provides crucial financial support to businesses affected by disasters, including the COVID-19 pandemic. One of the key uses of EIDL funds is for payroll coverage, ensuring that employees continue to receive their wages despite the economic challenges faced by their employers. To effectively utilize these funds, it is essential to understand which employees and payroll-related expenses are eligible for EIDL loan funds.

Eligibility for EIDL payroll coverage extends to a broad range of employees, including full-time, part-time, and seasonal workers. This inclusivity ensures that businesses can maintain their workforce and avoid layoffs during difficult times. Additionally, EIDL funds can be used to cover various payroll-related expenses, such as salaries, wages, sick leave, and payroll taxes. This comprehensive coverage helps businesses manage their financial obligations and maintain operational stability.

When applying for EIDL payroll coverage, businesses must provide detailed documentation to support their application. This includes payroll records, tax filings, and other relevant financial documents. The Small Business Administration (SBA) uses this information to assess the business's eligibility and determine the appropriate loan amount. It is crucial for businesses to maintain accurate and up-to-date records to facilitate a smooth application process and ensure timely disbursement of funds.

EIDL payroll coverage is particularly beneficial for small businesses and non-profit organizations that may not have the financial reserves to sustain their operations during a disaster. By providing a reliable source of funding, the EIDL program helps these entities maintain their workforce and continue serving their communities. Furthermore, EIDL funds can be used in conjunction with other disaster relief programs, such as the Paycheck Protection Program (PPP), to maximize financial support and minimize the economic impact of disasters.

In conclusion, understanding the payroll coverage options available through the EIDL program is essential for businesses seeking to mitigate the financial effects of disasters. By familiarizing themselves with the eligibility criteria and application process, businesses can effectively leverage EIDL funds to maintain their operations and support their employees during challenging times.

Can LLC Member Distributions Be Reclassified as Payroll?

You may want to see also

Explore related products

![]()

Loan Limits: Discover the maximum loan amount available and how it can be allocated for payroll costs

The Economic Injury Disaster Loan (EIDL) program, administered by the Small Business Administration (SBA), provides financial assistance to businesses affected by declared disasters. One of the key aspects of the EIDL program is understanding the loan limits and how they can be allocated for various business expenses, including payroll costs.

The maximum loan amount available through the EIDL program is currently set at $2 million. This limit applies to the total amount a business can borrow, not just for payroll costs. It's important to note that the actual loan amount a business may qualify for will depend on several factors, including the extent of the economic injury, the business's financial health, and its ability to repay the loan.

When it comes to allocating the loan funds for payroll costs, businesses have some flexibility. The SBA allows EIDL funds to be used for payroll and operating expenses, as well as to purchase equipment and inventory. However, the SBA does have some restrictions on how the funds can be used. For example, EIDL funds cannot be used to refinance existing debt or to pay off federal taxes.

To ensure that EIDL funds are used appropriately, businesses should carefully review the SBA's guidelines and restrictions. They should also consult with a financial advisor or accountant to determine the best way to allocate the loan funds for their specific business needs. By understanding the loan limits and allocation guidelines, businesses can make the most of the EIDL program and get the financial assistance they need to recover from a disaster.

S Corp Payroll: Can All Employees Be Paid Through Payroll?

You may want to see also

Explore related products

![]()

Interest Rates and Terms: Explore the interest rates and repayment terms specific to EIDL loans used for payroll

EIDL loans, provided by the Small Business Administration (SBA), offer a lifeline to businesses facing financial difficulties, especially in times of economic uncertainty. One of the key advantages of these loans is their flexibility in usage, including covering payroll expenses. However, understanding the interest rates and repayment terms is crucial for businesses to make informed decisions and ensure they can manage the loan effectively.

The interest rates for EIDL loans are typically lower than those of traditional bank loans, making them an attractive option for small businesses. As of my last update in June 2024, the SBA had set the interest rates for EIDL loans at 3.75% for businesses and 2.75% for non-profit organizations. These rates are fixed, providing borrowers with predictable monthly payments and helping them budget more effectively.

Repayment terms for EIDL loans can vary depending on the specific circumstances of the borrower and the purpose of the loan. Generally, these loans have a maximum repayment term of 30 years, which allows businesses to spread out their payments over a longer period, reducing the immediate financial burden. The SBA also offers a grace period of up to 4 years, during which borrowers are not required to make payments on the principal, although interest payments are still due.

For businesses using EIDL loans specifically for payroll, it's important to note that the loan amount can cover up to 6 months of payroll expenses. This can be a significant relief for businesses experiencing cash flow issues or those that have been impacted by external factors such as economic downturns or natural disasters.

To ensure successful repayment, businesses should carefully review the loan agreement and understand all the terms and conditions. They should also consider creating a detailed repayment plan that aligns with their cash flow projections. Additionally, businesses may want to explore options for loan forgiveness or other forms of assistance that could further alleviate their financial burden.

In conclusion, EIDL loans can be a valuable tool for businesses needing to cover payroll expenses, but it's essential to understand the interest rates and repayment terms to make the most of this financial resource. By doing so, businesses can better manage their finances and position themselves for long-term success.

Can Employees Cancel Square Payroll? Understanding Your Options

You may want to see also

Explore related products

![]()

Application Process: Get guidance on how to apply for an EIDL loan, including required documentation and eligibility criteria

To apply for an EIDL loan, businesses must meet specific eligibility criteria and provide required documentation. The application process involves several steps, starting with determining eligibility. Businesses must have been in operation for at least one year and have a credit score of 650 or higher. They must also meet the SBA's size standards for their industry.

Once eligibility is confirmed, businesses can begin the application process. This involves providing detailed financial information, including tax returns, financial statements, and a list of debts. Businesses must also provide a business plan and a description of how the loan funds will be used. It's important to note that EIDL loans cannot be used for payroll, but can be used for other operating expenses such as rent, utilities, and supplies.

After submitting the application, businesses may be required to provide additional documentation or information. The SBA will review the application and make a decision within a few weeks. If approved, the loan funds will be disbursed directly to the business.

It's important to carefully review the eligibility criteria and required documentation before applying for an EIDL loan. This will help ensure a smooth application process and increase the chances of approval. Businesses should also consider consulting with a financial advisor or SBA representative to get guidance on the application process and loan terms.

Reversing Direct Deposits: What Payroll Companies Can and Can't Do

You may want to see also

Frequently asked questions

Yes, an EIDL loan can be used for payroll. The Economic Injury Disaster Loan (EIDL) program provides financial assistance to businesses affected by disasters, including the COVID-19 pandemic. Payroll is considered a normal operating expense, and EIDL funds can be used to cover such expenses.

EIDL loans have favorable terms, including a low-interest rate of 3.75% for businesses and 2.75% for non-profit organizations. The repayment term is typically 30 years, and there are no prepayment penalties. Interest payments are deferred for the first two years, and principal payments are deferred for the first year.

The maximum loan amount for the EIDL program is $2 million. However, the actual loan amount a business can borrow will depend on its financial situation, creditworthiness, and the extent of the economic injury suffered.

Businesses can apply for an EIDL loan directly through the Small Business Administration (SBA) website. The application process typically involves providing basic business information, financial statements, and documentation of the economic injury suffered. It is recommended to consult with a financial advisor or accountant before applying to ensure all necessary documentation is prepared.