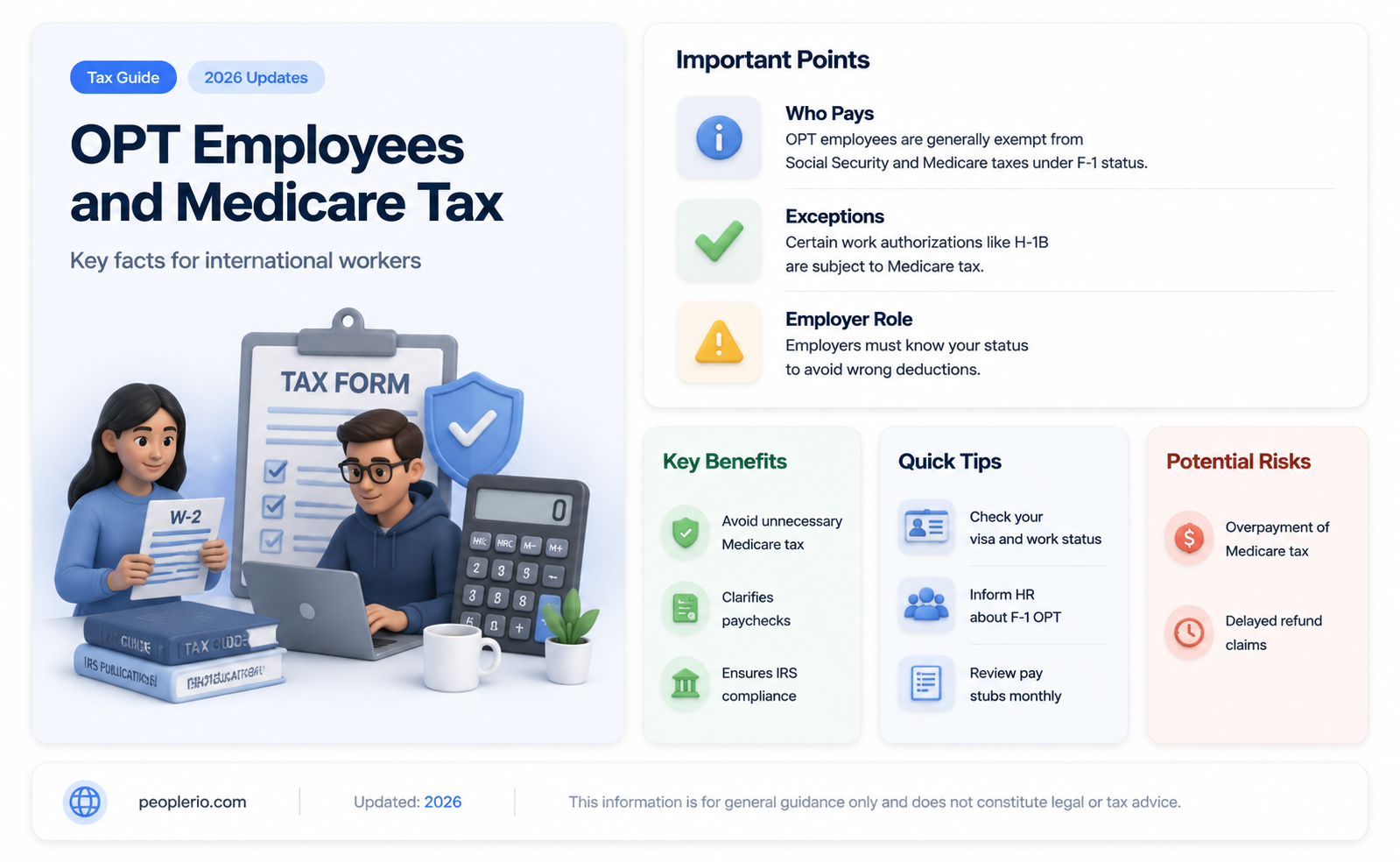

The question of whether an employee on Optional Practical Training (OPT) is required to pay Medicare tax is a nuanced one, often leading to confusion among international students and employers alike. OPT is a temporary employment opportunity available to international students who have completed their degree in the United States, allowing them to gain practical work experience in their field of study. However, the specifics of tax obligations, including Medicare tax, for these employees are not always straightforward. This paragraph aims to shed light on the general guidelines and considerations that apply to OPT employees regarding Medicare tax payments, helping to clarify this important aspect of employment for international students.

| Characteristics | Values |

|---|---|

| Employee Status | On OPT (Optional Practical Training) |

| Medicare Tax Exemption | Not applicable |

| OPT Duration | Typically 12 months, extendable to 36 months for STEM fields |

| Employment Type | Full-time or part-time |

| Employer Requirements | Must be registered with E-Verify |

| Employee Eligibility | F-1 visa holder, completed degree from an accredited U.S. institution |

| Application Process | Employer submits Form I-983 to USCIS |

| Reporting Requirements | Employer must report employee's OPT status to USCIS |

| Travel Restrictions | Limited to work-related travel within the U.S. |

| Benefits | No Medicare benefits, may have access to employer-sponsored health insurance |

| Tax Implications | Exempt from Medicare tax, but may be subject to other federal and state taxes |

| OPT Extension | Possible for STEM fields, requires employer sponsorship and additional paperwork |

| Employment Authorization | Limited to the specific employer and job listed on the OPT approval |

| OPT Termination | Ends upon completion of the authorized period or if employment is terminated |

| Future Employment | May transition to H-1B visa or other employment statuses upon OPT expiration |

Explore related products

What You'll Learn

- OPT Exemption: Employees on OPT may be exempt from Medicare tax under certain conditions

- FICA Tax Rules: Understanding FICA tax rules helps clarify when Medicare tax applies to OPT employees

- IRS Guidelines: The IRS provides specific guidelines on Medicare tax for non-citizens, including OPT holders

- State-Specific Laws: Some states have additional laws or exemptions related to Medicare tax for OPT employees

- Tax Filing Requirements: OPT employees must file tax returns and may need to include Medicare tax information

![]()

OPT Exemption: Employees on OPT may be exempt from Medicare tax under certain conditions

Employees on Optional Practical Training (OPT) may be exempt from paying Medicare tax under specific conditions. This exemption is based on the nature of their employment and the duration of their stay in the United States. To qualify for this exemption, employees must be non-resident aliens who are temporarily in the U.S. to pursue practical training related to their field of study.

The conditions for Medicare tax exemption include the requirement that the employee's primary purpose in the U.S. is to engage in OPT, rather than to work permanently. Additionally, the employee must not have been in the U.S. for more than five years. This five-year period is cumulative, meaning that any time spent in the U.S. on other visas or statuses counts towards this limit.

It is important to note that the exemption from Medicare tax does not apply to all employees on OPT. Those who are considered resident aliens for tax purposes, or who have been in the U.S. for more than five years, are not eligible for this exemption. Furthermore, the exemption only applies to Medicare tax and does not affect other taxes, such as Social Security or federal income tax.

Employers of OPT participants should carefully review the conditions for exemption to ensure compliance with tax laws. Failure to properly apply the exemption could result in penalties or fines. Employees on OPT should also be aware of their tax obligations and consult with a tax professional if they are unsure about their status.

In summary, the OPT exemption from Medicare tax is a specific provision that applies to non-resident alien employees who are in the U.S. on OPT and have not been in the country for more than five years. This exemption is an important consideration for both employers and employees to ensure proper tax compliance and avoid potential penalties.

Unpaid Work Requests: Legal and Ethical Considerations for Employers

You may want to see also

Explore related products

![]()

FICA Tax Rules: Understanding FICA tax rules helps clarify when Medicare tax applies to OPT employees

Understanding FICA tax rules is crucial for clarifying when Medicare tax applies to employees on Optional Practical Training (OPT). FICA, which stands for Federal Insurance Contributions Act, encompasses both Social Security and Medicare taxes. Generally, FICA taxes are withheld from an employee's wages to fund these federal programs. However, the application of these taxes to OPT employees can be nuanced and depends on several factors.

One key aspect to consider is the duration of the OPT. According to FICA tax rules, Medicare tax applies to OPT employees for the first 40 quarters of their employment in the United States. This means that if an employee has been working in the U.S. for less than 40 quarters, they may not be subject to Medicare tax. It's important to note that this exemption applies only to Medicare tax and not to Social Security tax, which has different rules and thresholds.

Another factor that can impact the application of Medicare tax to OPT employees is the type of employment. FICA tax rules distinguish between different types of employment, such as full-time, part-time, and seasonal work. For OPT employees, the determination of employment type can be complex, as their work authorization is tied to their student status and may involve multiple employers or varying work schedules.

Additionally, the FICA tax rules allow for certain exemptions and exceptions based on the employee's nationality and the nature of their work. For example, non-resident aliens employed by a foreign government or international organization may be exempt from FICA taxes, including Medicare tax. Similarly, employees working in certain industries, such as agriculture or domestic service, may be subject to different FICA tax rules.

In conclusion, navigating the FICA tax rules for OPT employees requires a thorough understanding of the specific circumstances and factors involved. By considering the duration of employment, type of work, and applicable exemptions, employers and employees can ensure compliance with federal tax laws and avoid potential penalties or legal issues.

Understanding Holiday Pay Deductions: What Employees Need to Know

You may want to see also

Explore related products

$14.99

![]()

IRS Guidelines: The IRS provides specific guidelines on Medicare tax for non-citizens, including OPT holders

The IRS has established clear guidelines regarding Medicare tax for non-citizens, including those holding Optional Practical Training (OPT) permits. According to these guidelines, non-citizens are generally exempt from Medicare tax if they meet certain criteria. One key criterion is that the individual must be a non-resident alien. This typically means that the person is not a U.S. citizen or permanent resident and does not meet the substantial presence test, which determines if an individual has spent a significant amount of time in the United States.

For OPT holders, the situation can be more complex. While OPT holders are not considered U.S. citizens or permanent residents, they are authorized to work in the United States for a specific period. The IRS considers OPT holders to be non-resident aliens for tax purposes, which generally means they are exempt from Medicare tax. However, there are some exceptions and nuances that OPT holders need to be aware of. For instance, if an OPT holder is employed by a U.S. employer and is subject to U.S. tax withholding, they may be required to pay Medicare tax.

It's important for OPT holders to understand their tax obligations and exemptions. They should consult with a tax professional or refer to IRS publications for detailed information on their specific situation. The IRS provides resources such as Publication 519, "U.S. Tax Guide for Aliens," which can help non-citizens, including OPT holders, navigate their tax responsibilities.

In summary, while OPT holders are generally considered non-resident aliens and exempt from Medicare tax, there are specific circumstances under which they may be required to pay this tax. It's crucial for individuals in this situation to seek professional advice and stay informed about the latest IRS guidelines to ensure compliance with U.S. tax laws.

Unpaid Leave: When Can an Employer Send an Employee Home?

You may want to see also

Explore related products

![]()

State-Specific Laws: Some states have additional laws or exemptions related to Medicare tax for OPT employees

Certain states have enacted their own legislation that either supplements or supersedes federal guidelines regarding Medicare tax for OPT employees. For instance, California has specific provisions that exempt certain OPT participants from state disability insurance and unemployment insurance taxes, which can indirectly affect their Medicare tax liabilities. Similarly, New York has laws that provide additional protections and benefits to OPT employees, which may influence their overall tax burden, including Medicare taxes.

In Texas, there are specific exemptions for OPT participants working in certain industries, such as technology and healthcare, which can impact their Medicare tax obligations. These state-specific laws often aim to attract and retain international talent by reducing their tax liabilities and providing additional benefits. However, it is crucial for OPT employees to understand that these laws may not necessarily exempt them from federal Medicare tax obligations, and they should consult with a tax professional to ensure compliance with both state and federal regulations.

Furthermore, some states have implemented programs that provide financial assistance or tax credits to OPT employees, which can help offset the cost of Medicare taxes. For example, Illinois offers a program that provides financial assistance to OPT participants working in certain industries, which can help reduce their overall tax burden. These state-specific initiatives highlight the importance of understanding the unique laws and regulations that apply to OPT employees in different states.

OPT employees should also be aware that state-specific laws and exemptions may change over time, and it is essential to stay informed about any updates or modifications. Failure to comply with state-specific laws can result in penalties, fines, or even deportation, so it is crucial for OPT participants to prioritize understanding and adhering to these regulations. By doing so, they can ensure that they are taking advantage of any available benefits and exemptions while remaining compliant with the law.

Understanding UK Salary Deductions: Employer's Rights and Employee Protections

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Tax Filing Requirements: OPT employees must file tax returns and may need to include Medicare tax information

Employees on Optional Practical Training (OPT) are required to file tax returns in the United States. This is a critical aspect of maintaining legal status and complying with IRS regulations. The tax filing process can be complex, especially for international students who may not be familiar with U.S. tax laws. It is essential to understand that even if an individual does not earn enough to owe federal income tax, they may still need to file a tax return to report their income and claim any applicable tax credits or deductions.

One of the key considerations for OPT employees is the inclusion of Medicare tax information on their tax returns. Medicare is a federal health insurance program primarily for individuals aged 65 and older, but it also covers certain younger people with disabilities and those with End-Stage Renal Disease. As an OPT employee, you are required to pay Medicare taxes, which are typically withheld from your paycheck by your employer. However, if you are self-employed or your employer does not withhold Medicare taxes, you may need to pay these taxes when you file your tax return.

To ensure compliance with tax filing requirements, OPT employees should gather all necessary documents, including their W-2 form (if applicable), 1099 forms (if self-employed), and any other relevant income statements. They should also be aware of the filing deadline, which is typically April 15th of each year. Failure to file a tax return or pay any owed taxes can result in penalties and interest, as well as potential issues with maintaining legal status in the United States.

In summary, OPT employees must file tax returns and include Medicare tax information as part of their compliance with U.S. tax laws. This process requires careful attention to detail and an understanding of the specific requirements and deadlines. By staying informed and following the necessary steps, OPT employees can ensure they meet their tax obligations and avoid potential legal and financial consequences.

Navigating Legal Fee Clauses in Employment Contracts: What You Need to Know

You may want to see also

Frequently asked questions

Generally, employees on OPT are required to pay Medicare tax. However, there may be specific circumstances or exemptions that apply.

OPT stands for Optional Practical Training, which is a work authorization for international students in the United States. Medicare tax is a federal tax that funds the Medicare program, and it is typically withheld from an employee's wages.

Yes, there are some exceptions. For example, if an employee on OPT is working for a tax-exempt organization or if they are a non-resident alien, they may be exempt from paying Medicare tax.

To determine if they are exempt from paying Medicare tax, an employee on OPT should consult with their employer's human resources department or a tax professional. They may need to provide documentation to support their exemption status.