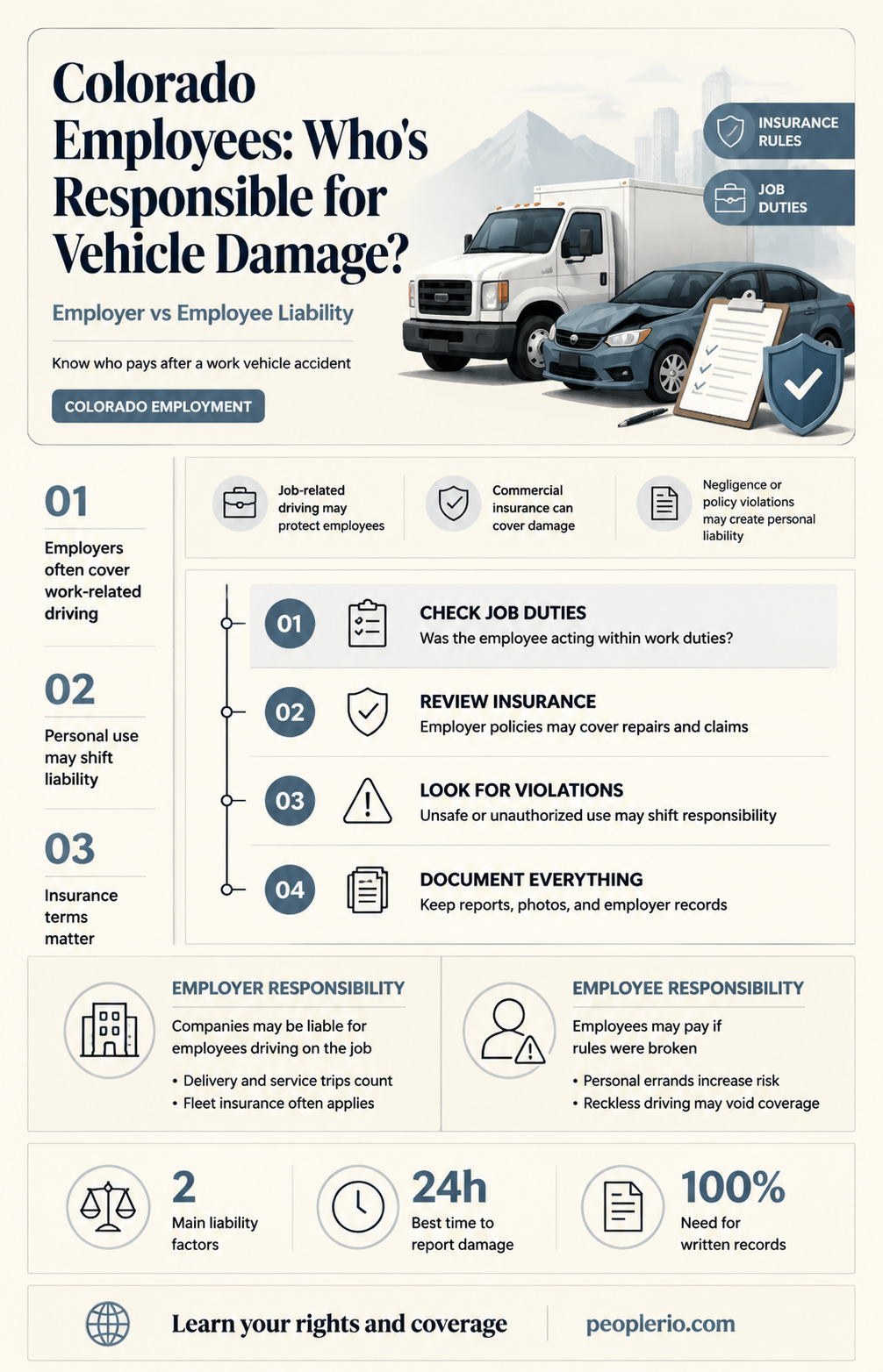

In Colorado, employees may be held responsible for vehicle damage incurred during the course of their employment. This liability can arise from various scenarios, such as accidents while driving a company car or damage to a personal vehicle used for work purposes. Understanding the legal framework and company policies surrounding this issue is crucial for both employers and employees. Employers must establish clear guidelines regarding vehicle use and maintenance, while employees should be aware of their rights and responsibilities in case of vehicle damage. This paragraph aims to provide an overview of the key considerations and potential implications involved in employee liability for vehicle damage in Colorado.

Explore related products

What You'll Learn

- Colorado Law Overview: Understand the legal framework governing vehicle damage compensation in Colorado

- Employee Responsibility: Define the scope of an employee's liability for vehicle damage during work use

- Insurance Coverage: Explore the types of insurance policies that may cover vehicle damage in Colorado

- Damage Assessment: Learn how to properly assess and document vehicle damage for insurance claims

- Claim Process: Navigate the step-by-step process of filing an insurance claim for vehicle damage in Colorado

![]()

Colorado Law Overview: Understand the legal framework governing vehicle damage compensation in Colorado

Colorado's legal framework regarding vehicle damage compensation is rooted in its status as a "fault" state for car insurance. This means that the driver who is deemed responsible for an accident is liable for the damages incurred by the other party. In the context of an employee causing vehicle damage, this could have significant implications for both the employee and the employer.

Under Colorado law, if an employee is acting within the scope of their employment when they cause vehicle damage, the employer may be held vicariously liable. This is based on the legal principle of respondeat superior, which holds employers responsible for the actions of their employees when those actions are performed in the course of their employment duties. As such, it is crucial for employers to have adequate insurance coverage to protect against potential claims arising from employee-caused vehicle damage.

However, if the employee is not acting within the scope of their employment—for example, if they are using the vehicle for personal reasons or are off-duty—then the employer may not be liable. In such cases, the employee would be personally responsible for the damages, and their own insurance policy would be the primary source of compensation for the other party.

Colorado law also requires all drivers to carry minimum amounts of liability insurance. As of 2023, the minimum coverage is $25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $15,000 per accident for property damage. If an employee causes vehicle damage and their employer's insurance policy does not cover the full amount of the damages, the employee's personal insurance may be required to make up the difference.

In addition to liability insurance, Colorado law also mandates that all drivers carry uninsured/underinsured motorist coverage. This coverage protects drivers who are involved in accidents with uninsured or underinsured motorists. In the context of employee-caused vehicle damage, this coverage could be critical if the employee's personal insurance policy does not provide adequate compensation for the damages.

Ultimately, understanding Colorado's legal framework governing vehicle damage compensation is essential for both employers and employees. Employers must ensure that they have adequate insurance coverage to protect against potential claims, while employees must be aware of their personal liability and the importance of carrying sufficient insurance coverage. By being informed about these legal requirements, both parties can take steps to mitigate risks and ensure that they are prepared in the event of an accident.

Cash Compensation: Exploring the Pros and Cons for Employers and Employees

You may want to see also

Explore related products

![]()

Employee Responsibility: Define the scope of an employee's liability for vehicle damage during work use

In the context of employee responsibility for vehicle damage during work use in Colorado, it is essential to understand the scope of liability that employees may bear. This involves examining the specific circumstances under which an employee might be held responsible for damages incurred to a company vehicle.

Firstly, the nature of the employee's job and the extent to which vehicle use is integral to their duties play a significant role. For instance, if an employee is required to use a company vehicle for deliveries or client visits, the employer may have established clear guidelines regarding the acceptable use and maintenance of the vehicle. In such cases, if the employee fails to adhere to these guidelines and the vehicle is damaged as a result, the employee could be held liable for the costs associated with the damage.

Secondly, the concept of negligence is a crucial factor in determining employee liability. If an employee operates the vehicle in a reckless or careless manner, resulting in damage, they may be found negligent and thus responsible for the damages. This could include instances of speeding, driving under the influence, or failing to properly secure cargo, leading to accidents or damage to the vehicle.

Thirdly, the employee's adherence to traffic laws and regulations is also a critical consideration. If an employee violates traffic laws, such as running a red light or failing to yield, and this violation results in an accident causing damage to the vehicle, the employee may be held liable. In Colorado, as in many other states, employers may have policies in place that require employees to obey all traffic laws while operating company vehicles.

Lastly, it is important to note that the scope of an employee's liability may be influenced by the employer's insurance coverage and policies. If the employer has comprehensive insurance that covers vehicle damage, the employee's liability may be limited to the deductible or other out-of-pocket expenses. However, if the employer's insurance does not cover certain types of damage or if the employee's actions are deemed to be outside the scope of their employment, the employee could be held fully responsible for the damages.

In conclusion, the scope of an employee's liability for vehicle damage during work use in Colorado is multifaceted and depends on various factors, including the nature of their job, their adherence to company guidelines and traffic laws, and the extent of the employer's insurance coverage. Understanding these factors is crucial for both employers and employees to ensure that responsibilities are clear and that appropriate measures are taken to minimize the risk of vehicle damage.

Exploring the Ethics and Legality of Unpaid Work

You may want to see also

Explore related products

$16.69 $17.76

![]()

Insurance Coverage: Explore the types of insurance policies that may cover vehicle damage in Colorado

In Colorado, when an employee is involved in a vehicle accident resulting in damage, various types of insurance policies may come into play to cover the costs. Understanding these policies is crucial for both employers and employees to navigate the financial implications effectively.

One of the primary types of insurance that may cover vehicle damage is auto insurance. This can include comprehensive coverage, which protects against damage to the vehicle that is not caused by a collision, such as theft, vandalism, or natural disasters. Collision coverage, on the other hand, specifically covers damage to the vehicle resulting from an accident with another vehicle or object.

Another relevant type of insurance is liability insurance, which covers the costs associated with injuries or property damage that the employee may be responsible for. This can be particularly important in cases where the employee is at fault for the accident and may be held liable for the damages incurred.

Additionally, some employers may offer specialized insurance policies for company vehicles, known as fleet insurance. This type of policy can provide comprehensive coverage for all vehicles owned or leased by the company, offering a more cost-effective solution for businesses with multiple vehicles on the road.

It's also worth noting that in some cases, an employee's personal auto insurance policy may not cover damage to a company vehicle, or it may only provide limited coverage. Therefore, it's essential for employees to understand the specifics of their own insurance policies and how they interact with any company-provided coverage.

In conclusion, navigating the complexities of insurance coverage for vehicle damage in Colorado requires a thorough understanding of the various types of policies available and how they apply in different situations. By being informed about auto insurance, liability insurance, and fleet insurance options, both employers and employees can better protect themselves financially in the event of an accident.

Exploring the Benefits and Boundaries of Company-Sponsored Employee Meals

You may want to see also

Explore related products

![]()

Damage Assessment: Learn how to properly assess and document vehicle damage for insurance claims

In the event of a vehicle accident, one of the most critical steps is conducting a thorough damage assessment. This process involves carefully examining the vehicle to identify all areas of damage, both visible and hidden. It's essential to approach this task systematically, starting from the front of the vehicle and moving to the back, noting any dents, scratches, or structural damage. Don't overlook the undercarriage, as damage here can be particularly costly to repair.

Once the initial visual inspection is complete, it's time to document the findings. This documentation should include detailed notes, photographs, and diagrams if necessary. It's crucial to be as specific as possible, noting the exact location and extent of each piece of damage. This information will be invaluable when filing an insurance claim, as it provides a clear and accurate record of the vehicle's condition.

In addition to documenting the physical damage, it's also important to consider any potential mechanical issues that may have arisen as a result of the accident. This might include problems with the engine, transmission, or other critical systems. If there are any concerns about the vehicle's safety or drivability, it should be noted in the damage assessment.

When conducting a damage assessment, it's essential to remain objective and factual. Avoid making assumptions about the cause of the damage or the potential cost of repairs. Stick to the facts and let the insurance company make the necessary determinations. By providing a clear, accurate, and detailed damage assessment, you can help ensure that the insurance claim process goes smoothly and that you receive fair compensation for your vehicle's damage.

California Employers: Are You Obligated to Provide Employee Health Insurance?

You may want to see also

Explore related products

![]()

Claim Process: Navigate the step-by-step process of filing an insurance claim for vehicle damage in Colorado

To initiate the claim process for vehicle damage in Colorado, you must first ensure that you have the necessary documentation. This includes a copy of your insurance policy, the vehicle's registration, and any relevant photos or videos of the damage. Additionally, you should gather any witness statements or police reports if applicable. Once you have compiled all the required documents, you can proceed to file a claim with your insurance provider.

The next step in the process is to contact your insurance company and inform them of the incident. They will likely ask for details about the accident, the extent of the damage, and any other pertinent information. Be prepared to provide them with the documentation you have gathered. Your insurance company will then assign an adjuster to assess the damage and determine the appropriate course of action.

After the adjuster has evaluated the damage, they will provide you with an estimate for the repairs. If you agree with the estimate, you can proceed with the repairs. However, if you disagree with the estimate, you may need to negotiate with the insurance company or seek a second opinion from an independent adjuster. Once the repairs are completed, you will need to submit the final invoice to your insurance company for reimbursement.

Throughout the claim process, it is important to keep detailed records of all communications with your insurance company, including phone calls, emails, and letters. This will help ensure that you have a clear record of the claim process and can reference it if needed. Additionally, be aware of the statute of limitations for filing a claim in Colorado, which is typically three years from the date of the accident.

In conclusion, navigating the claim process for vehicle damage in Colorado can be a complex and time-consuming task. However, by following these steps and being prepared with the necessary documentation, you can help ensure a smooth and successful claim process. Remember to stay organized, communicate effectively with your insurance company, and seek professional assistance if needed.

Can Employees Withhold Company Property for Unpaid Wages?

You may want to see also

Frequently asked questions

Generally, if an employee is using a company-owned vehicle and the damage occurs during work hours, the company's insurance should cover the costs. However, if the employee is found to be at fault or if the company's insurance policy has specific exclusions, the employee might be held responsible for some or all of the damages.

If an employee is using their personal vehicle for work purposes and gets into an accident, their personal auto insurance policy will typically be the primary coverage. However, if the employee's personal policy does not cover business use or if the coverage is insufficient, the company's insurance may provide secondary coverage. It's important for employees to check their personal policies and understand their company's insurance coverage in such situations.

Colorado law requires all vehicles operated on public roads to have minimum levels of insurance coverage. For company vehicles, this includes liability insurance to cover damages to other vehicles or property in the event of an accident. While the law does not specifically mandate that employees pay for damages, companies often have internal policies that outline employee responsibilities in the case of vehicle damage.

Employees can protect themselves financially by ensuring they have adequate insurance coverage, both through their employer and their personal auto insurance policy. It's also advisable to review and understand the company's vehicle use policies and any clauses related to employee responsibility for damages. In some cases, employees may want to consider purchasing additional coverage or umbrella insurance to provide extra protection beyond the company's policy limits.