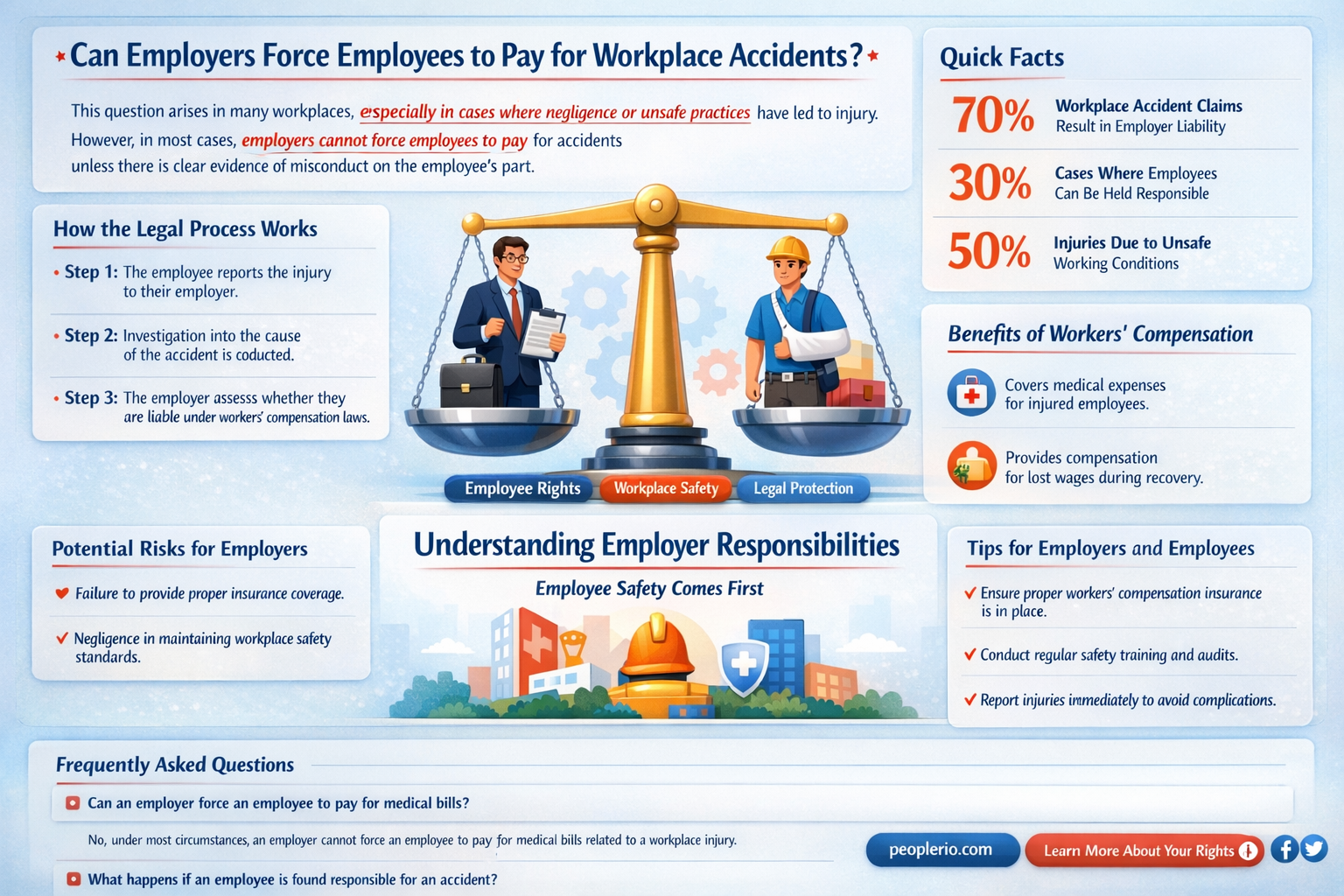

The question of whether an employer can legally require an employee to pay for damages resulting from a workplace accident is a complex and contentious issue, often governed by labor laws, employment contracts, and liability principles. Generally, employers are responsible for providing a safe working environment and may be held liable for accidents caused by negligence or unsafe conditions. However, in certain circumstances, such as employee misconduct or violation of company policies, employers might seek reimbursement for damages. The legality of such actions varies by jurisdiction, with many regions protecting employees from financial liability unless explicitly stated in a contract or proven gross negligence. Understanding the legal framework and contractual agreements is crucial for both employers and employees to navigate this delicate balance of responsibility and accountability.

What You'll Learn

![]()

Legal Responsibility for Damages

Employers often seek to recover costs after workplace accidents, but the legal framework governing such actions is complex and varies by jurisdiction. In the United States, for instance, the general rule under workers' compensation laws is that employers cannot sue employees for damages resulting from workplace accidents, provided the employee’s actions were not willful or egregious. This principle, known as the "exclusive remedy rule," shields employees from personal liability while ensuring they receive benefits for work-related injuries. However, exceptions exist, particularly in cases of gross negligence, intoxication, or intentional misconduct. Understanding these nuances is critical for both employers and employees to navigate their rights and obligations effectively.

In contrast to the U.S., some countries allow employers to deduct costs from employee wages or seek reimbursement for damages under specific conditions. For example, in the United Kingdom, employers can deduct wages for accidental damage only if the employee agrees in writing, and the deduction is reasonable and does not reduce earnings below the National Minimum Wage. Such practices highlight the importance of contractual agreements and local labor laws in determining liability. Employees should carefully review employment contracts for clauses related to financial responsibility for accidents, as these can significantly impact their legal standing.

A comparative analysis reveals that the legal responsibility for damages often hinges on the concept of fault and the nature of the employment relationship. In at-will employment states in the U.S., employers may have more leeway to terminate or penalize employees for costly mistakes, even if they cannot recover damages directly. Conversely, in countries with stronger labor protections, such as Germany, employers are generally prohibited from holding employees financially liable for accidental damage unless it results from willful misconduct. This disparity underscores the need for employees to familiarize themselves with the legal protections afforded to them in their respective jurisdictions.

Practical tips for employees include documenting all workplace incidents thoroughly, seeking legal advice if an employer demands reimbursement, and ensuring that any agreements related to financial liability are fair and compliant with local laws. Employers, on the other hand, should focus on implementing robust safety protocols, providing adequate training, and obtaining appropriate insurance coverage to mitigate risks. By prioritizing prevention and compliance, both parties can reduce the likelihood of disputes arising from workplace accidents.

Ultimately, the legal responsibility for damages in workplace accidents is a delicate balance between protecting employees from undue financial burden and holding them accountable for reckless behavior. While employers may feel the financial strain of accidents, attempting to shift costs onto employees without legal justification can lead to costly litigation and damage workplace morale. A proactive approach, grounded in clear policies and mutual understanding, is the most effective way to manage risks and maintain a positive work environment.

Can Salaried Employees Face Pay Deductions? Understanding Wage Docking Rules

You may want to see also

![]()

Employer vs. Employee Liability

Employers often face the dilemma of whether they can hold employees financially responsible for workplace accidents, a question that hinges on the complex interplay of liability laws and employment contracts. In most jurisdictions, the general rule is that employers are liable for accidents occurring in the workplace, especially if they result from negligence or unsafe working conditions. However, there are exceptions and nuances that can shift the financial burden onto the employee under specific circumstances.

Consider the scenario of a delivery driver who damages a company vehicle due to reckless driving. While the employer’s insurance may cover the repairs, some companies attempt to recoup costs from the employee, particularly if gross negligence is proven. This practice, however, is legally precarious. In the U.S., for instance, the Fair Labor Standards Act (FLSA) prohibits employers from deducting wages for such damages if doing so reduces the employee’s pay below minimum wage. Similarly, in the UK, employers can only deduct wages for workplace damage if explicitly stated in the employment contract and the employee has agreed in writing.

The key to understanding liability lies in distinguishing between ordinary negligence and gross misconduct. Ordinary negligence, such as a minor mistake leading to equipment damage, typically falls under the employer’s responsibility. Gross misconduct, however, such as intentional damage or violation of clear safety protocols, may allow employers to seek reimbursement. For example, if an employee deliberately ignores safety training and causes an accident, the employer might have grounds to recover costs, though this varies by jurisdiction and requires robust evidence.

Practical steps for employers include clearly outlining liability terms in employment contracts, ensuring compliance with local labor laws, and maintaining comprehensive insurance coverage. Employees, on the other hand, should scrutinize their contracts for clauses related to financial liability and understand their rights under labor laws. In cases of disputes, both parties may benefit from mediation or legal consultation to avoid costly litigation.

Ultimately, while employers may seek to hold employees accountable for accidents, the legal framework often limits their ability to do so. The balance of liability rests on factors such as negligence type, contractual agreements, and statutory protections. Both employers and employees must navigate this terrain carefully, prioritizing clarity, fairness, and adherence to the law.

Can Employers Legally Charge Employees for Workplace Damages?

You may want to see also

![]()

Workplace Accident Policies

Employers often grapple with the question of financial responsibility when workplace accidents occur. While it’s tempting to shift costs to employees, labor laws in most jurisdictions explicitly prohibit this practice. For instance, in the United States, the Occupational Safety and Health Administration (OSHA) mandates that employers are responsible for providing a safe workplace and cannot penalize employees for accidents, including through wage deductions or reimbursement demands. Similarly, in the UK, the Health and Safety at Work Act 1974 places the onus on employers to ensure employee safety, leaving no legal ground for cost recovery from workers. These laws underscore a fundamental principle: workplace safety is a non-negotiable employer obligation.

Crafting a robust workplace accident policy is essential for clarity and compliance. Start by defining the scope of coverage, including medical expenses, lost wages, and rehabilitation costs. Explicitly state that employees will not bear financial liability for accidents, unless gross negligence or intentional misconduct is proven. Incorporate a reporting procedure that encourages timely documentation of incidents, as this not only aids in claims processing but also helps identify systemic safety issues. For example, a policy might require employees to report accidents within 24 hours and provide a detailed incident report within 48 hours. Such specificity minimizes ambiguity and fosters trust.

A common misconception is that workers’ compensation insurance absolves employers of all responsibilities. While this insurance covers medical costs and wage replacement, it does not exempt employers from maintaining a safe work environment or from potential OSHA fines for violations. Moreover, workers’ compensation does not cover all accident-related costs, such as property damage or increased insurance premiums. Employers should therefore view insurance as a safety net, not a substitute for proactive safety measures. Regular safety audits, employee training, and equipment maintenance are critical components of a comprehensive accident prevention strategy.

Finally, consider the human element in workplace accident policies. Employees who feel supported after an accident are more likely to remain loyal and engaged. A policy that includes provisions for counseling, temporary reassignment, or phased return-to-work programs can significantly aid recovery. For instance, offering access to an Employee Assistance Program (EAP) can provide mental health support, while a gradual return schedule might allow an injured worker to ease back into full duties. Such measures not only benefit the employee but also reduce long-term costs associated with turnover and lost productivity. A compassionate policy is not just ethical—it’s good business.

Employer-Paid Medicare Premiums: Legal, Tax, and Benefits Overview

You may want to see also

![]()

Insurance Coverage Limits

Employers often carry insurance policies to mitigate financial risks associated with workplace accidents, but coverage limits can leave gaps that may indirectly affect employees. For instance, a standard general liability policy might cap payouts at $1 million per occurrence, which could be insufficient for accidents involving severe injuries or multiple parties. If damages exceed this limit, the employer might face a shortfall, potentially leading to legal actions or cost-shifting measures that could impact employees, such as increased premiums or reduced benefits. Understanding these limits is crucial for both employers and employees to assess potential financial exposure.

Analyzing insurance coverage limits requires a proactive approach. Employers should conduct regular policy reviews to ensure limits align with operational risks. For example, a construction company with high-risk activities might need umbrella coverage extending beyond the base policy’s $2 million limit. Employees, meanwhile, should inquire about workers’ compensation coverage, which typically covers medical expenses and lost wages but may have state-specific caps. In California, for instance, temporary disability benefits are capped at $1,540 per week as of 2023, leaving high earners vulnerable to income gaps post-accident.

A persuasive argument for addressing coverage limits lies in the shared interest of employers and employees to avoid financial strain. Employers can invest in higher coverage limits or supplemental policies to protect their workforce and reputation, while employees can advocate for transparent communication about existing policies. For example, a company with a $500,000 auto liability limit for company vehicles might face significant out-of-pocket costs if an employee causes a multi-vehicle accident, potentially leading to lawsuits or wage garnishments. Expanding coverage to $1 million or more could prevent such scenarios.

Comparatively, industries with inherently higher risks, such as manufacturing or transportation, often face stricter insurance requirements but may still encounter limits that fall short in catastrophic events. A trucking company with a $750,000 cargo insurance limit could face substantial losses if a shipment worth $1.5 million is damaged in an accident. Employees in these sectors should explore personal liability policies to fill gaps, while employers can negotiate industry-specific endorsements to extend coverage. For instance, a hazardous materials endorsement might increase limits for chemical spills but at a higher premium.

Practically, employees can take steps to protect themselves by reviewing their employer’s insurance certificates and understanding exclusions. For example, if a policy excludes coverage for accidents caused by employee negligence, individuals might consider legal liability insurance. Employers, on the other hand, can implement risk management programs to reduce claim frequency, thereby lowering premiums and justifying higher coverage limits. A company that reduces workplace accidents by 30% through safety training might negotiate a 15% premium discount, allowing them to allocate savings to increased coverage limits.

![]()

State-Specific Labor Laws

In the United States, the question of whether an employer can make an employee pay for damages resulting from a workplace accident is governed by a complex interplay of federal and state-specific labor laws. While federal laws like the Fair Labor Standards Act (FLSA) provide a baseline, individual states often enact their own regulations that can either reinforce or diverge from federal standards. This patchwork of laws means that the answer to this question varies significantly depending on where the accident occurs. For instance, some states explicitly prohibit employers from deducting wages for accidental damage to company property, while others allow it under specific conditions, such as employee negligence or written agreements.

Consider California, a state with some of the most employee-protective labor laws in the country. Under California Labor Code Section 221, employers are generally prohibited from deducting wages for losses incurred by the employer unless the employee is found to have willful misconduct. This means that if an employee accidentally damages company property, the employer cannot typically withhold wages to cover the cost. However, if the employee intentionally or recklessly caused the damage, the employer might have grounds to recover the losses. This distinction highlights the importance of understanding the specific language and intent of state laws, as they often hinge on terms like "negligence" or "willful misconduct."

In contrast, states like Texas take a more employer-friendly approach. Texas labor laws do not explicitly prohibit employers from requiring employees to pay for accidental damages, provided the deduction does not reduce the employee’s wages below minimum wage. Additionally, Texas allows employers to implement policies requiring employees to reimburse for damages, especially if the employee signs an agreement acknowledging this responsibility. This flexibility underscores the need for employees to carefully review employment contracts and understand their rights under state law. For example, if an employee in Texas signs a document agreeing to reimburse the employer for accidental damage, they may be legally obligated to do so, even if the accident was unintentional.

Another critical factor in state-specific labor laws is the role of workers’ compensation insurance. In states like New York, where workers’ compensation is mandatory for most employers, employees are generally protected from personal liability for workplace accidents, regardless of fault. This means that if an employee causes damage while performing their job duties, the employer’s insurance should cover the losses, and the employee cannot be held financially responsible. However, this protection does not extend to cases of intoxication, intentional misconduct, or violations of company policy, which may still result in employee liability depending on state law.

To navigate these state-specific nuances, employees and employers alike should take proactive steps. First, employees should familiarize themselves with their state’s labor laws and review their employment contracts for clauses related to liability for damages. Employers, on the other hand, should ensure their policies comply with state regulations and clearly communicate expectations to employees. For instance, if an employer in a state like Florida wishes to implement a policy requiring employees to pay for accidental damages, they should consult legal counsel to ensure the policy aligns with Florida’s wage deduction laws and does not violate employee protections. By understanding and adhering to state-specific labor laws, both parties can avoid legal disputes and foster a fair working environment.

Frequently asked questions

In most cases, employers cannot legally force employees to pay for damages caused by workplace accidents, especially if the employee was acting within the scope of their job duties and following company policies.

Employees may be held responsible if the accident was caused by gross negligence, intentional misconduct, or violation of company policies, though this varies by jurisdiction and employment laws.

Wage deductions for accident-related costs are generally illegal unless the employee voluntarily agrees in writing, and even then, it must comply with labor laws and not violate minimum wage requirements.

Employees are typically protected by workers’ compensation laws, which generally prevent employers from holding employees financially liable for accidents occurring in the course of their employment.

Terminating an employee for refusing to pay for a workplace accident may be considered retaliatory and illegal, especially if the employee was not at fault or was protected by workers’ compensation laws.