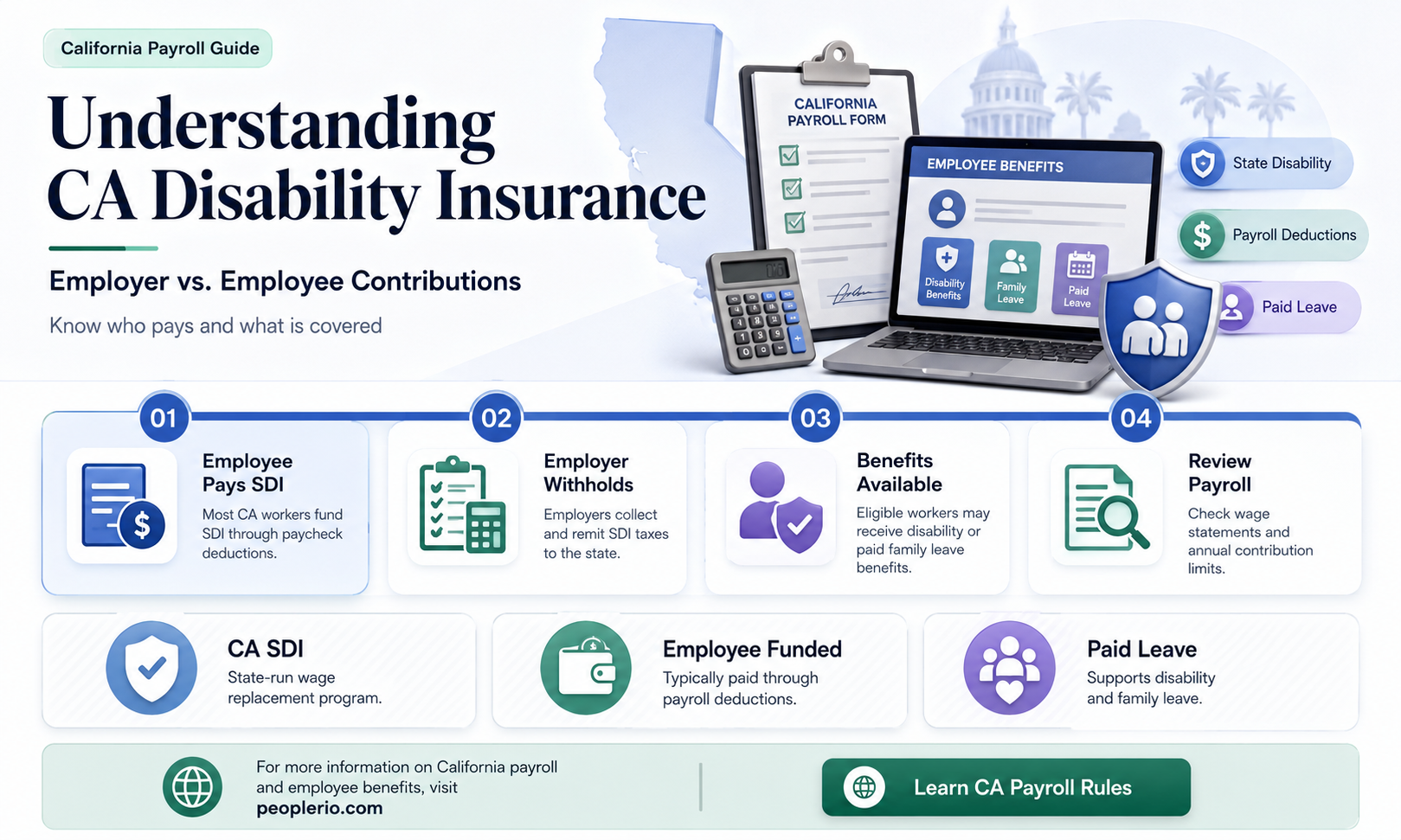

California Disability Insurance (CDI) is a state-mandated program that provides partial wage replacement to eligible employees who are unable to work due to a non-work-related illness or injury. While employers are required to pay for this insurance, there is often confusion about whether they can also pay the employee's portion. The short answer is yes, employers can pay the employee's portion of CA disability insurance, but it's important to understand the implications and potential benefits of doing so. By covering the employee's portion, employers can help ensure that their workers have adequate financial protection during times of disability, which can lead to increased job security and loyalty. Additionally, paying the employee's portion can be a valuable recruitment and retention tool, as it demonstrates a commitment to employee well-being. However, it's crucial for employers to carefully consider the financial impact of this decision and to communicate clearly with employees about the terms and conditions of the coverage.

Explore related products

![Social Security Disability Insurance Program worker experience by Tim Zayatz 1999 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

What You'll Learn

- Legal Requirements: Employers' obligations under California law to provide disability insurance to employees

- Cost Distribution: Breakdown of premium costs between employers and employees for CA disability insurance

- Benefit Structure: Overview of the benefits provided by CA disability insurance, including eligibility and coverage

- Employee Contributions: Details on how employee portions of CA disability insurance premiums are deducted and managed

- Compliance and Penalties: Consequences for employers who fail to comply with CA disability insurance regulations

![]()

Legal Requirements: Employers' obligations under California law to provide disability insurance to employees

Under California law, employers have specific obligations regarding disability insurance for their employees. One key requirement is that employers must provide disability insurance coverage to their employees. This coverage is designed to protect employees who are unable to work due to a disability, providing them with a portion of their wages while they are out of work. Employers are required to pay for this coverage, and they cannot pass the cost on to their employees.

The disability insurance provided by employers must meet certain standards set by California law. For example, the coverage must provide at least 50% of the employee's weekly wages, up to a maximum of $1,075 per week. The coverage must also begin within 30 days of the employee's disability and can last for up to 52 weeks. Employers are also required to provide their employees with a notice of their rights under the disability insurance program.

In addition to providing disability insurance coverage, employers must also comply with other legal requirements related to employee benefits. For example, employers must provide their employees with access to health insurance coverage, and they must also comply with the Family and Medical Leave Act (FMLA). Employers who fail to comply with these legal requirements can face penalties and legal action.

Overall, employers in California have a legal obligation to provide disability insurance coverage to their employees. This coverage is designed to protect employees who are unable to work due to a disability, and employers must meet certain standards when providing this coverage. Employers who fail to comply with these legal requirements can face serious consequences.

Can an Employer Cease COBRA Insurance Payments for an Employee?

You may want to see also

Explore related products

![]()

Cost Distribution: Breakdown of premium costs between employers and employees for CA disability insurance

In California, disability insurance is a crucial component of employee benefits, providing financial protection in the event of an employee's inability to work due to illness or injury. The cost of this insurance is typically shared between employers and employees, with each party contributing a portion of the premium. Employers are mandated to provide disability insurance to their employees, and they often absorb a significant portion of the cost to attract and retain talent.

The breakdown of premium costs between employers and employees can vary depending on the specific insurance plan and the employer's policies. Generally, employers may cover anywhere from 50% to 100% of the premium, with the remaining portion deducted from the employee's paycheck. Some employers may also offer the option for employees to purchase additional coverage at their own expense.

It's important for both employers and employees to understand the cost distribution of disability insurance premiums, as it can impact budgeting and financial planning. Employers need to consider the cost of providing this benefit when setting salaries and determining overall compensation packages, while employees should be aware of the portion of the premium they are responsible for and how it fits into their personal financial goals.

When evaluating disability insurance plans, employers should consider factors such as the level of coverage provided, the cost of the premiums, and the potential impact on employee morale and productivity. Employees, on the other hand, should review the terms of the plan carefully, including the waiting period before benefits are paid, the duration of benefits, and any exclusions or limitations.

In conclusion, the cost distribution of disability insurance premiums between employers and employees in California is a critical aspect of employee benefits that requires careful consideration from both parties. By understanding the breakdown of costs and the implications for financial planning, employers and employees can make informed decisions about disability insurance coverage.

Severance Pay Cessation: What Happens If an Employee Dies?

You may want to see also

Explore related products

![]()

Benefit Structure: Overview of the benefits provided by CA disability insurance, including eligibility and coverage

California disability insurance provides a range of benefits to eligible employees who are unable to work due to a disability. These benefits include partial wage replacement, which helps to cover lost income during the period of disability. The amount of wage replacement varies depending on the employee's earnings history and the extent of their disability. Additionally, CA disability insurance may offer benefits for medical expenses related to the disability, as well as vocational rehabilitation services to help employees return to work when possible.

Eligibility for CA disability insurance benefits typically requires that the employee has earned a minimum amount in wages prior to the disability and has paid into the state's disability insurance program. The coverage period for benefits can vary, but generally, employees may receive benefits for up to one year, depending on the severity of their disability and their ability to return to work.

It's important to note that CA disability insurance benefits are designed to provide temporary financial assistance and support during a period of disability, rather than long-term income replacement. Employees who are receiving benefits may also be required to participate in vocational rehabilitation programs to help them regain their ability to work and reduce their reliance on disability benefits.

Employers play a crucial role in the CA disability insurance system, as they are responsible for withholding employee contributions and submitting them to the state. Employers may also choose to provide additional disability insurance coverage to their employees, either through a private insurance carrier or by offering a supplemental state disability insurance program. This additional coverage can help to fill gaps in the state's disability insurance benefits and provide employees with more comprehensive financial protection in the event of a disability.

In summary, the benefit structure of CA disability insurance provides essential financial support and resources to eligible employees who are unable to work due to a disability. Understanding the eligibility requirements, coverage options, and benefit limitations is crucial for both employees and employers to ensure that they are adequately prepared for the financial challenges that can arise from a disability.

Exploring the Option: Can Employees Choose No Pay Over PTO?

You may want to see also

Explore related products

![]()

Employee Contributions: Details on how employee portions of CA disability insurance premiums are deducted and managed

In the state of California, disability insurance is a crucial aspect of employee benefits, providing financial protection in the event of an inability to work due to illness or injury. While employers are mandated to provide this coverage, the specifics of how the employee portion of the premiums is handled can vary. Typically, the employee's contribution is deducted directly from their paycheck, ensuring that the insurance remains active and the employee is covered continuously.

The process of deducting these premiums is usually outlined in the employee's benefits package, detailing the percentage or fixed amount that will be withheld each pay period. Employers must ensure that these deductions are made accurately and consistently to avoid any lapses in coverage or discrepancies in payroll. Additionally, employers are responsible for managing these funds appropriately, often by setting up a separate account to hold the employee contributions until they are needed to pay the insurance premiums.

One important consideration for employers is the tax implications of these deductions. In California, disability insurance premiums paid by employees are generally considered taxable income. Employers must therefore report these amounts on the employee's W-2 form at the end of the year. This can have an impact on the employee's overall tax liability, so it is essential for employers to provide clear communication about the tax treatment of these contributions.

Another aspect to consider is the potential for disputes or questions regarding the deductions. Employers should have a clear policy in place for addressing employee concerns about their disability insurance contributions. This may include providing detailed breakdowns of the deductions, offering explanations of how the premiums are calculated, and outlining the appeals process if an employee believes there has been an error.

Overall, managing employee contributions to California disability insurance premiums requires careful attention to detail, compliance with state regulations, and effective communication with employees. By handling these aspects properly, employers can ensure that their employees have the necessary protection while also maintaining a smooth and efficient payroll process.

Understanding Minimum Salary Requirements for Salaried Employees: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Compliance and Penalties: Consequences for employers who fail to comply with CA disability insurance regulations

Employers in California are required to provide disability insurance to their employees, and failure to comply with these regulations can result in significant consequences. The California Employment Development Department (EDD) is responsible for enforcing these regulations, and they have the authority to impose penalties on employers who do not meet their obligations. These penalties can include fines, interest, and even criminal charges in severe cases.

One of the most common penalties for non-compliance is the imposition of fines. These fines can be substantial, and they are designed to encourage employers to take their obligations seriously. In addition to fines, employers may also be required to pay interest on any unpaid premiums or contributions. This interest can add up quickly, further increasing the cost of non-compliance.

In some cases, employers may face criminal charges for failing to comply with California disability insurance regulations. These charges can result in fines, imprisonment, or both. Criminal charges are typically reserved for the most egregious cases of non-compliance, such as those involving fraud or intentional misrepresentation.

To avoid these penalties, employers should ensure that they are in full compliance with California disability insurance regulations. This includes providing the required coverage, paying premiums on time, and maintaining accurate records. Employers should also be aware of any changes to the regulations, as failure to adapt to these changes can also result in penalties.

In conclusion, the consequences for employers who fail to comply with California disability insurance regulations can be severe. By understanding these regulations and taking steps to ensure compliance, employers can avoid costly penalties and protect their employees' rights to disability insurance.

Opting Out of Social Security Taxes: A Guide for Employees

You may want to see also

Frequently asked questions

Yes, employers are required to pay the employee portion of California disability insurance. This is mandated by California law, and it is typically deducted from the employee's wages.

The employee portion of California disability insurance is a percentage of the employee's wages, up to a certain maximum amount per year. The exact percentage and maximum amount can vary, so it's best to check with the California Employment Development Department for the most current figures.

If an employer does not pay the employee portion of California disability insurance, they may be subject to penalties and fines. Additionally, the employee may not be eligible for disability benefits if the employer has not paid their portion of the insurance.