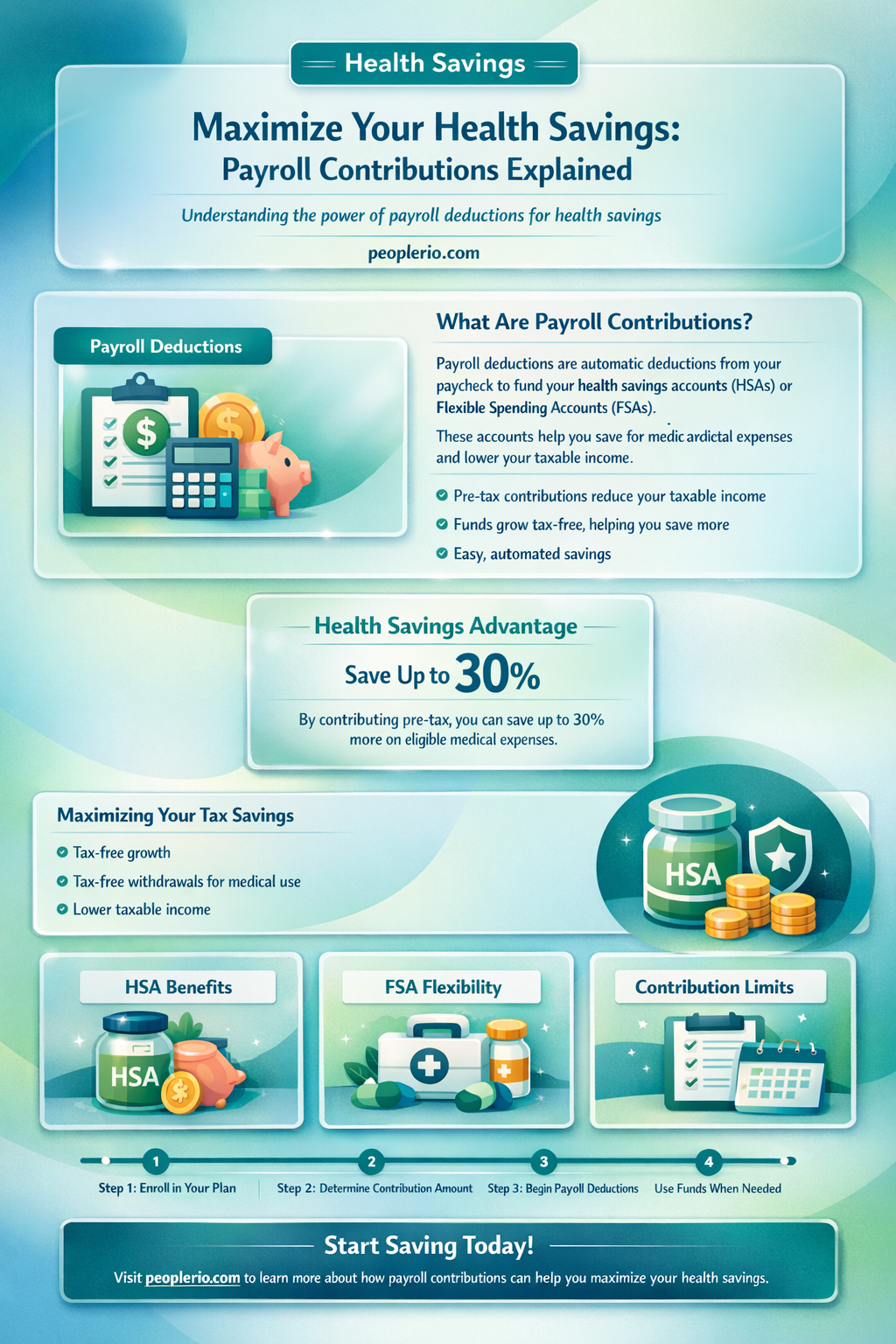

Health savings accounts (HSAs) are a valuable tool for individuals looking to save money on healthcare expenses. One common question is whether HSA contributions can be made through payroll deductions. The answer is yes, many employers offer the option for employees to contribute to their HSAs directly from their paychecks. This can be a convenient way to save for healthcare costs, as the contributions are typically made pre-tax, reducing the employee's taxable income. Additionally, some employers may even match a portion of the employee's HSA contributions, further incentivizing this savings method.

Explore related products

What You'll Learn

- Contribution Limits: Maximum amounts allowed annually, varies by plan and IRS regulations

- Tax Advantages: Contributions are pre-tax, reducing taxable income; earnings grow tax-free

- Eligibility: Requirements to qualify for an HSA, including having a high-deductible health plan

- Withdrawals: Rules for tax-free withdrawals, typically for qualified medical expenses

- Rollovers: Transferring funds from other accounts or plans into an HSA

![]()

Contribution Limits: Maximum amounts allowed annually, varies by plan and IRS regulations

The IRS sets annual contribution limits for Health Savings Accounts (HSAs), which vary based on the type of plan and the individual's age. For 2023, the maximum contribution limit for an individual with self-only coverage is $3,850, while for family coverage, it's $7,750. These limits include both employee and employer contributions. It's crucial to note that these figures are subject to change annually, reflecting adjustments for inflation and other economic factors.

Employers often contribute to HSAs as part of their employee benefits package. These contributions are tax-deductible for the employer and tax-free for the employee, making them a valuable component of an overall compensation strategy. However, employer contributions count towards the annual limit, so employees need to be mindful of how much their employer is contributing to avoid exceeding the IRS cap.

Individuals aged 55 and older are eligible to make additional "catch-up" contributions to their HSAs. For 2023, this catch-up contribution limit is $1,000. This provision allows older workers to save more for healthcare expenses in retirement, recognizing that healthcare costs tend to increase with age.

It's important for HSA holders to monitor their contributions throughout the year to ensure they do not surpass the annual limit. Exceeding the contribution limit can result in tax penalties and may require the individual to withdraw excess funds from the account. To avoid this, many HSA holders choose to contribute a fixed amount each paycheck, ensuring they stay within the annual cap.

In summary, understanding and adhering to HSA contribution limits is essential for maximizing the tax advantages of these accounts while avoiding potential penalties. By staying informed about the current limits and adjusting contributions accordingly, individuals can effectively manage their healthcare savings.

Exploring PPP Eligibility for LLCs Without Payroll: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Tax Advantages: Contributions are pre-tax, reducing taxable income; earnings grow tax-free

Contributions to a Health Savings Account (HSA) offer significant tax advantages that can enhance your financial well-being. Unlike other types of accounts, HSA contributions are made on a pre-tax basis, which means they are deducted from your gross income before taxes are calculated. This reduces your taxable income, leading to a lower tax bill. For instance, if you contribute $3,000 to your HSA and your marginal tax rate is 25%, you would save $750 in taxes.

Moreover, the earnings in your HSA grow tax-free, compounding the benefits over time. This means that any interest, dividends, or capital gains generated within the account are not subject to taxation. As a result, your HSA can serve as a powerful tool for long-term wealth accumulation, especially if you invest the funds wisely.

To maximize these tax advantages, it's essential to understand the contribution limits and eligibility requirements. For 2023, individuals can contribute up to $3,850, while families can contribute up to $7,750. Additionally, individuals aged 55 and older can make catch-up contributions of up to $1,000. It's also important to note that you must be enrolled in a high-deductible health plan (HDHP) and not be enrolled in Medicare to be eligible for HSA contributions.

When it comes to payroll, HSA contributions can be made through payroll deductions, which makes it easy to contribute regularly. Many employers also offer matching contributions, which can further boost your savings. However, it's crucial to ensure that your employer's HSA plan aligns with your financial goals and that you're taking full advantage of any matching funds offered.

In summary, the tax advantages of HSA contributions make them an attractive option for individuals looking to reduce their taxable income and grow their savings tax-free. By understanding the contribution limits, eligibility requirements, and payroll options, you can leverage these benefits to enhance your financial future.

Understanding Your Rights: Can a Company Withhold Your Payroll Records?

You may want to see also

Explore related products

![]()

Eligibility: Requirements to qualify for an HSA, including having a high-deductible health plan

To qualify for a Health Savings Account (HSA), individuals must meet specific eligibility requirements. One of the primary criteria is having a high-deductible health plan (HDHP). This type of plan typically has lower premiums but higher out-of-pocket costs, which the HSA can help cover. The IRS sets the minimum deductible amounts annually; for 2023, the minimum deductible for an individual is $1,350, and for a family, it's $2,700.

In addition to having an HDHP, individuals must not be enrolled in Medicare. This is because Medicare provides comprehensive health coverage that is not compatible with the purpose of an HSA, which is to provide a tax-advantaged way to save for qualified medical expenses. Furthermore, individuals cannot be claimed as dependents on someone else's tax return. This ensures that the HSA benefits are directed towards those who are responsible for their own healthcare costs.

Another important requirement is that the individual must have earned income. This is necessary because HSA contributions are tax-deductible, and having earned income is a prerequisite for taking advantage of this tax benefit. The amount an individual can contribute to their HSA is based on their earned income, with higher earners able to contribute more.

It's also crucial to note that individuals cannot have any other health coverage that provides significant benefits for the same expenses covered by the HDHP. This includes supplemental insurance policies or employer-provided health reimbursement arrangements (HRAs). The purpose of this rule is to prevent individuals from using multiple sources of coverage to reduce their out-of-pocket expenses, which would undermine the intent of the HSA.

Finally, individuals should be aware that they can open an HSA at any time during the year, but the contributions are prorated based on the number of months they have the qualifying HDHP. This means that if someone opens an HSA midway through the year, they can only contribute a portion of the annual maximum. It's important to consider this timing when planning for HSA contributions.

Navigating Payroll Without an SSN: What Companies Need to Know

You may want to see also

Explore related products

![]()

Withdrawals: Rules for tax-free withdrawals, typically for qualified medical expenses

To withdraw funds from a Health Savings Account (HSA) tax-free, you must use the money for qualified medical expenses. These expenses include doctor visits, hospital stays, prescription medications, and other healthcare costs not covered by your insurance plan. It's important to keep detailed records of all medical expenses to ensure you can substantiate your withdrawals.

One key rule is that you cannot use HSA funds to pay for health insurance premiums, except in certain circumstances, such as when you are receiving unemployment benefits. Additionally, you cannot use HSA funds for non-medical expenses, such as gym memberships or cosmetic procedures, unless they are specifically prescribed by a doctor for medical reasons.

When making a withdrawal, you should carefully consider the amount you need to avoid taking out more than necessary. Excessive withdrawals can lead to tax penalties and reduce the overall balance of your HSA. It's also important to be aware of any fees associated with withdrawals, as these can vary depending on your HSA provider.

In terms of documentation, you should keep all receipts and invoices related to your medical expenses. This will help you easily track your spending and ensure you have the necessary proof in case of an audit. Some HSA providers may also require you to submit documentation before processing a withdrawal request.

Finally, it's worth noting that HSA funds are portable, meaning you can use them even if you change jobs or retire. This flexibility makes HSAs a valuable tool for saving on healthcare costs throughout your life. However, it's crucial to understand and follow the rules for tax-free withdrawals to maximize the benefits of your HSA.

Understanding Wage Garnishment: Can a Visa Payroll Card Be Garnished?

You may want to see also

Explore related products

![]()

Rollovers: Transferring funds from other accounts or plans into an HSA

One effective strategy for maximizing the benefits of a Health Savings Account (HSA) is through rollovers, which involve transferring funds from other accounts or plans into the HSA. This can be particularly advantageous for individuals looking to consolidate their health-related savings or those who have unused funds in other accounts that could be better utilized within an HSA. Rollovers allow for the tax-free movement of funds, which can help in avoiding penalties and maximizing the growth potential of the savings.

To execute a rollover, it's essential to follow specific steps and adhere to IRS guidelines. First, ensure that the funds being rolled over are eligible for transfer into an HSA. Typically, funds from FSAs (Flexible Spending Accounts) and HRAs (Health Reimbursement Accounts) can be rolled over, but there may be limitations or specific conditions that need to be met. Next, contact the administrator of the account from which the funds are being transferred to initiate the rollover process. This may involve filling out specific forms or providing documentation to verify the eligibility of the funds.

Once the rollover is initiated, the funds will be transferred directly into the HSA, usually within a few weeks. It's crucial to monitor the transfer to ensure that it is completed correctly and that there are no issues or delays. After the rollover, review the HSA's investment options to determine the best strategy for growing the funds. HSAs often offer a range of investment choices, from conservative to aggressive, allowing individuals to tailor their savings strategy to their financial goals and risk tolerance.

One key consideration when planning rollovers is the timing. It's generally advisable to initiate rollovers at the beginning of the year to maximize the tax advantages and allow the funds to grow throughout the year. Additionally, be aware of any contribution limits or restrictions that may apply to the HSA, as exceeding these limits can result in penalties.

In conclusion, rollovers can be a valuable tool for enhancing the benefits of an HSA, but it's essential to understand the process and adhere to the relevant guidelines. By following the proper steps and considering the timing and eligibility of the funds, individuals can effectively consolidate their health savings and make the most of their HSA.

Exploring the Possibilities: Can GE Make Payroll?

You may want to see also

Frequently asked questions

Yes, many employers offer the option to contribute to your HSA through payroll deductions. This allows you to set aside money for medical expenses on a pre-tax basis, reducing your taxable income.

To set up HSA contributions through payroll deductions, you typically need to contact your employer's human resources or benefits department. They will provide you with the necessary forms or online portals to enroll in this benefit.

Contributing to an HSA through payroll deductions offers several benefits. Firstly, it allows you to save money on taxes since the contributions are made pre-tax. Secondly, it provides a convenient way to save for medical expenses, as the money is automatically deducted from your paycheck. Lastly, HSAs often earn interest, allowing your savings to grow over time.