Cashing someone else's payroll check is a common scenario that may arise when an individual is unable to cash their own check due to various reasons such as being out of town, having an expired ID, or not having access to a bank account. In such cases, it is possible to cash the check by following certain legal procedures and providing the necessary documentation. However, it is important to note that there may be limitations and restrictions depending on the state or country where the check is being cashed, as well as the policies of the bank or financial institution involved.

| Characteristics | Values |

|---|---|

| Check Type | Payroll Check |

| Ownership | Someone Else's |

| Cashing Method | In-person, Mobile Deposit, ATM Deposit |

| Required Identification | Valid ID, Paycheck Stub |

| Potential Fees | Check Cashing Fees, ATM Fees |

| Legal Considerations | Endorsement Requirements, Fraud Prevention |

| Bank Policies | Varies by Bank, Check Amount Limits |

Explore related products

What You'll Learn

- Legal Requirements: Understand the laws and regulations surrounding the cashing of third-party checks

- Bank Policies: Familiarize yourself with specific bank rules and procedures for cashing someone else's payroll check

- Endorsement Process: Learn the correct way to endorse a check to ensure it's processed without issues

- Identification Needed: Discover what forms of ID are typically required to cash a payroll check on behalf of someone else

- Potential Fees: Be aware of any fees associated with cashing payroll checks that aren't your own

![]()

Legal Requirements: Understand the laws and regulations surrounding the cashing of third-party checks

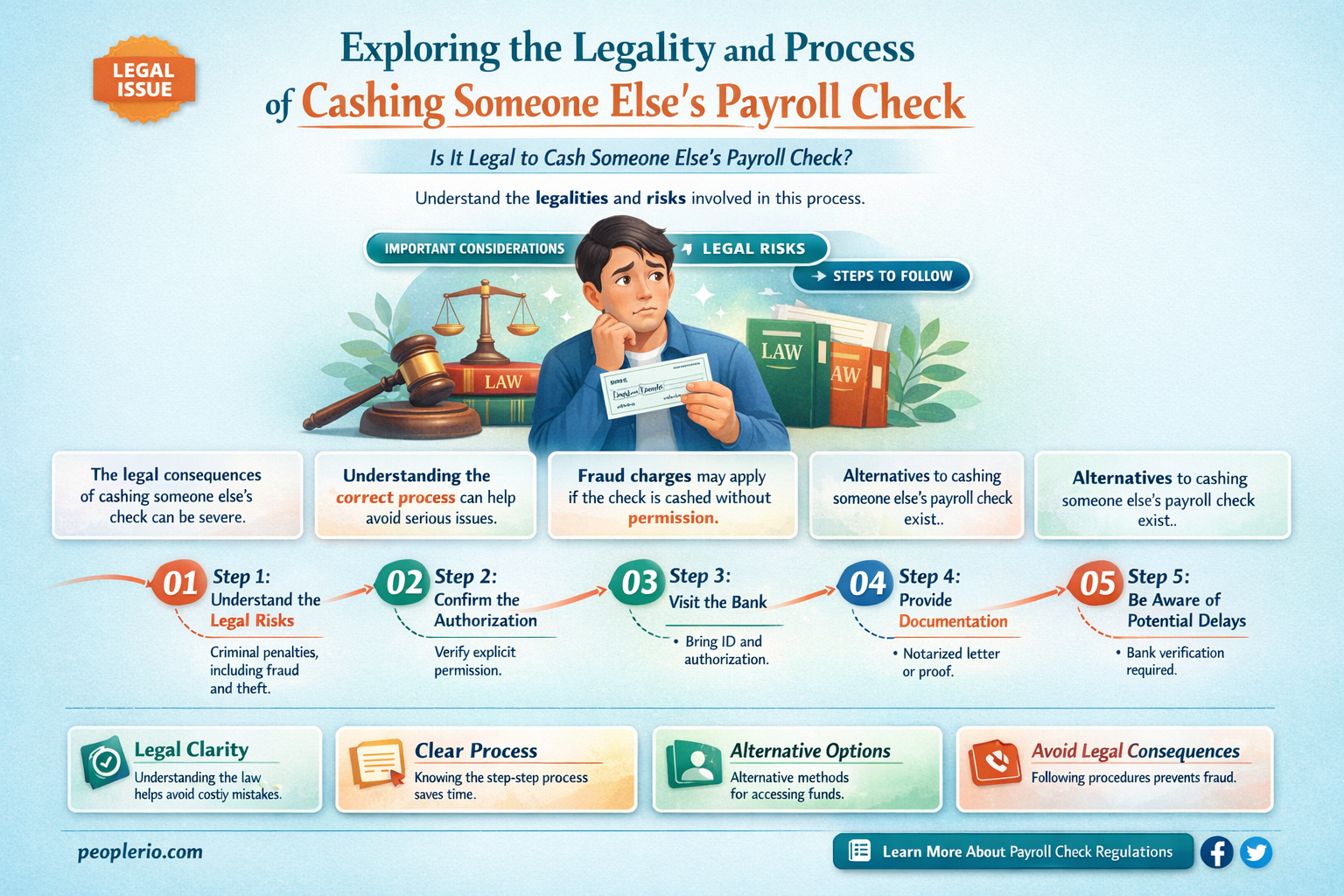

Understanding the legal requirements for cashing third-party checks is crucial to avoid potential legal issues. The laws and regulations surrounding this process vary by jurisdiction, but there are some general principles to keep in mind. First, it's important to note that cashing someone else's payroll check without their permission is generally illegal and can result in criminal charges. However, if you have been authorized to cash the check on someone's behalf, you must ensure that you follow the proper procedures.

One key legal requirement is to have proper identification. You will typically need to present a valid government-issued ID, such as a driver's license or passport, to verify your identity. Additionally, you may need to provide documentation to prove your relationship to the check issuer, such as a power of attorney or a signed authorization letter.

Another important consideration is the endorsement. The check must be properly endorsed by the payee, and in some cases, you may need to sign the endorsement as well. It's also essential to ensure that the check is not post-dated or stale-dated, as this can affect its validity.

Furthermore, you should be aware of any specific state or federal laws that may apply to your situation. For example, some states have laws that limit the amount of a third-party check that can be cashed, while others may require additional documentation or verification.

In conclusion, cashing a third-party check requires careful attention to legal details and proper authorization. By understanding the laws and regulations surrounding this process, you can avoid potential legal issues and ensure that the transaction is conducted smoothly and safely.

Exploring Payroll Check Cashing Options for Small Businesses

You may want to see also

Explore related products

![]()

Bank Policies: Familiarize yourself with specific bank rules and procedures for cashing someone else's payroll check

Familiarizing yourself with specific bank rules and procedures for cashing someone else's payroll check is crucial to avoid any complications or delays. Each bank has its own set of policies regarding third-party checks, and understanding these can save you time and effort. For instance, some banks may require the person cashing the check to have an account with them, while others might allow non-account holders to cash checks for a fee. Additionally, banks often have limits on the amount of money they will cash for non-account holders, and exceeding these limits may result in the check being rejected.

Before attempting to cash someone else's payroll check, it's essential to gather all necessary information and documentation. This typically includes the check itself, a valid form of identification for both the person who wrote the check and the person cashing it, and potentially proof of relationship or authorization to cash the check. Some banks may also require additional documentation, such as a utility bill or lease agreement, to verify the address of the person cashing the check.

One common mistake people make when trying to cash someone else's payroll check is not endorsing the check properly. The person cashing the check should endorse it on the back with their signature, and the person who wrote the check should also sign the back if required by the bank. Another mistake is not bringing sufficient identification or documentation, which can lead to the bank refusing to cash the check.

To avoid these issues, it's a good idea to call the bank ahead of time and ask about their specific requirements for cashing third-party checks. This can help you prepare all necessary documents and ensure a smooth process. Additionally, consider using mobile banking or online deposit options if available, as these can often streamline the process and reduce the need for in-person visits to the bank.

In conclusion, understanding and following bank policies when cashing someone else's payroll check is essential to avoid complications and ensure a successful transaction. By gathering all necessary information and documentation, endorsing the check properly, and being aware of any fees or limits, you can help make the process as smooth and efficient as possible.

Understanding Payroll Check Clearing Times: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Endorsement Process: Learn the correct way to endorse a check to ensure it's processed without issues

To endorse a check correctly, you must follow a specific process to ensure it is processed without issues. Start by examining the back of the check for any existing endorsements or instructions. If the check is endorsed with a signature only, you may need to add additional information to ensure it is processed correctly.

Next, locate the endorsement area on the back of the check. This is typically a designated space where you can write your endorsement. If there is no designated space, you can endorse the check by writing your name and the words "for deposit only" on the back.

When endorsing the check, be sure to use your full name and include any additional information required by the bank or financial institution. This may include your account number or the name of the account holder. If you are endorsing the check for deposit into a joint account, be sure to include the names of all account holders.

Once you have endorsed the check, be sure to review it carefully for any errors or omissions. If you notice any mistakes, correct them immediately to avoid any issues with processing. Finally, take the endorsed check to the bank or financial institution to deposit it into the designated account.

Remember, it is important to follow the specific endorsement instructions provided by the bank or financial institution to ensure the check is processed correctly. Failure to do so may result in delays or issues with the deposit.

Does Tops Cash Payroll Checks on Sundays? Your Weekend Guide

You may want to see also

Explore related products

![]()

Identification Needed: Discover what forms of ID are typically required to cash a payroll check on behalf of someone else

To cash a payroll check on behalf of someone else, you will typically need to provide identification that proves your identity and your relationship to the check's issuer. This is to prevent fraud and ensure that the check is being cashed by an authorized person. The specific forms of ID required may vary depending on the bank or financial institution, but generally, you will need to provide at least one form of government-issued ID, such as a driver's license, state ID, or passport. Additionally, you may need to provide proof of your relationship to the check's issuer, such as a power of attorney or a letter of authorization.

It's important to note that some banks may have additional requirements, such as a minimum age or residency status. For example, some banks may require that you be at least 18 years old to cash a check, while others may require that you have a local address. It's also possible that the bank may require additional documentation, such as a copy of the check issuer's ID or a proof of employment.

In some cases, you may be able to cash a payroll check without the person's physical presence, but this will typically require additional steps and documentation. For example, you may need to provide a notarized power of attorney or a letter of authorization that specifically states that you are allowed to cash the check on the person's behalf.

If you are unsure about the specific requirements for cashing a payroll check on behalf of someone else, it's best to contact the bank or financial institution directly. They will be able to provide you with the most up-to-date information and guide you through the process.

Remember, it's always important to be cautious when handling financial transactions, especially when they involve someone else's money. Make sure to follow all of the bank's requirements and guidelines to ensure that the transaction is processed smoothly and securely.

Understanding Payroll: Operating Accounts and Check Writing

You may want to see also

Explore related products

![]()

Potential Fees: Be aware of any fees associated with cashing payroll checks that aren't your own

Cashing someone else's payroll check can come with unexpected costs. One of the most common fees associated with this process is the check cashing fee. This fee is typically a percentage of the check amount and can vary depending on the financial institution or check cashing service used. For example, a bank may charge 1% of the check amount, while a check cashing store might charge up to 5%. These fees can quickly add up, especially if you're cashing multiple checks or if the checks are for large amounts.

In addition to check cashing fees, there may be other costs involved. Some financial institutions charge a deposit fee if you deposit the check into your account instead of cashing it directly. This fee is usually a flat rate, such as $5 or $10, but can sometimes be a percentage of the check amount. If you're depositing the check into your account, you may also need to consider the time it takes for the check to clear. This can vary depending on the bank and the amount of the check, but it's typically 1-3 business days. During this time, you may not have access to the funds, which could lead to additional fees if you need to access the money quickly.

Another potential cost to consider is the risk of fraud. If the check is fraudulent, you may be held responsible for the amount of the check, plus any fees associated with cashing or depositing it. This is why it's important to verify the authenticity of the check before cashing it. You can do this by contacting the issuer of the check or by using a check verification service. These services typically charge a small fee, but it's worth it to avoid the risk of fraud.

To minimize the fees associated with cashing someone else's payroll check, it's important to shop around and compare the fees charged by different financial institutions and check cashing services. You may also want to consider opening a bank account if you don't already have one, as this can provide you with more options for depositing and accessing the funds. Finally, always be cautious when cashing checks that aren't your own, and take steps to verify their authenticity before proceeding.

Free Payroll Check Creation: A Step-by-Step Guide for Small Businesses

You may want to see also

Frequently asked questions

Generally, you cannot cash someone else's payroll check as it is issued specifically to the employee named on the check.

Even with permission, most banks will not allow you to cash a check made out to someone else due to security and fraud prevention policies.

Some banks may allow you to deposit the check into your account if you have a power of attorney or a similar legal arrangement with the person named on the check.

Attempting to cash someone else's check without proper authorization can lead to legal issues, including potential charges of fraud or theft.

If you need to handle someone else's payroll check legitimately, you should discuss the situation with the person named on the check and explore options such as power of attorney or having the check reissued in your name if applicable.