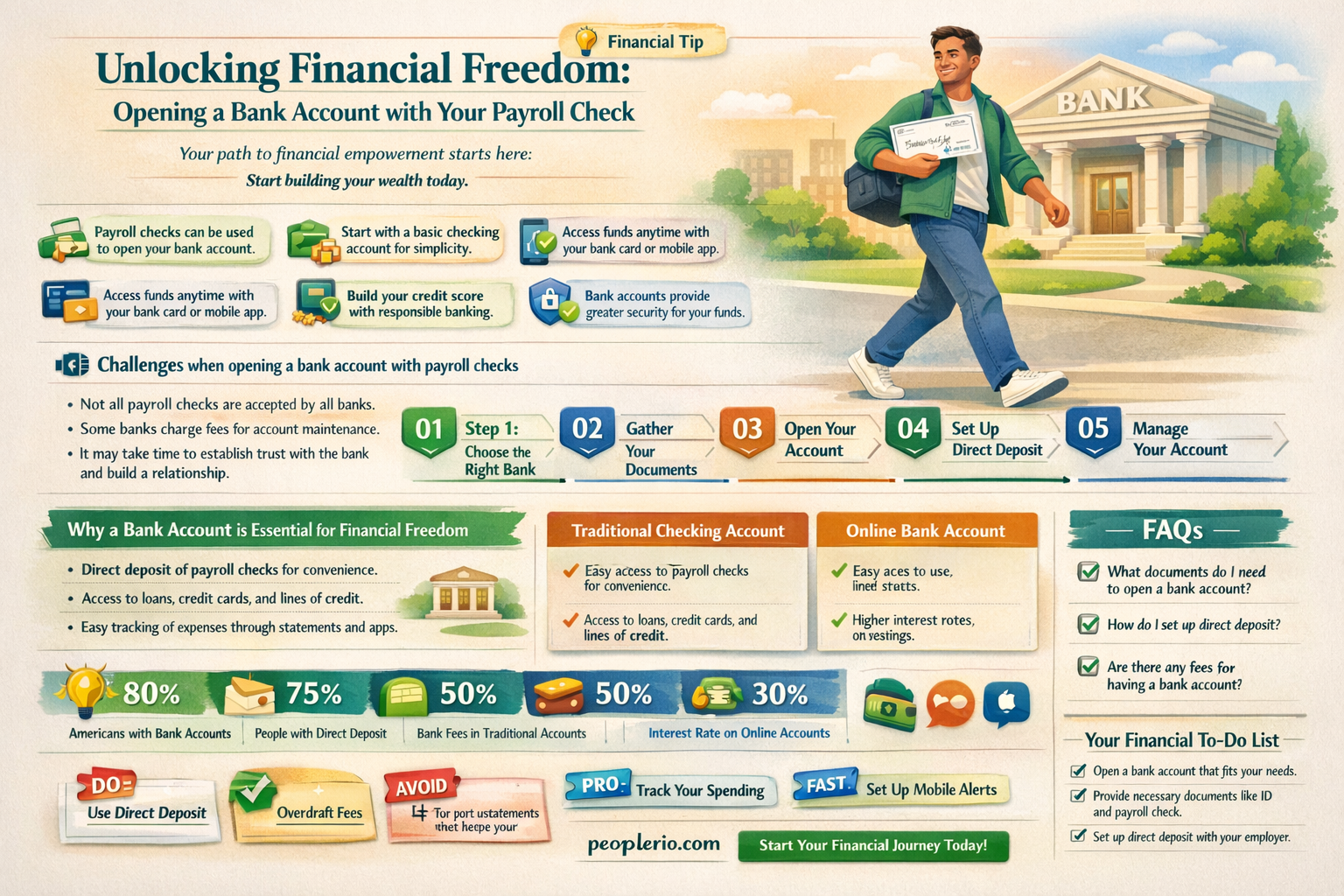

Opening a bank account with a payroll check is a common financial practice, especially for individuals who receive their wages via direct deposit. This process typically involves verifying your identity and employment status, as well as meeting the bank's specific requirements for account opening. In this guide, we'll explore the necessary steps, documentation, and considerations to successfully open a bank account using your payroll check, ensuring you have a clear understanding of the procedure and any potential challenges you may encounter.

| Characteristics | Values |

|---|---|

| Account Type | Checking or Savings |

| Required Documents | Payroll Check, Identification, Proof of Address |

| Minimum Deposit | Varies by Bank |

| Fees | Monthly Maintenance, Overdraft, ATM |

| Interest Rate | Varies by Bank and Account Type |

| Online Banking | Available with Most Banks |

| Mobile Banking | Available with Most Banks |

| Direct Deposit | Available with Most Banks |

| Bill Pay | Available with Most Banks |

| Minimum Balance | Varies by Bank and Account Type |

| Withdrawal Limits | Varies by Bank and Account Type |

| Deposit Limits | Varies by Bank and Account Type |

| Credit Score Requirement | None or Minimum Score Required |

| Residency Requirement | US Resident or Non-Resident with Valid Visa |

| Age Requirement | 18 Years or Older |

Explore related products

What You'll Learn

- Requirements for Opening a Bank Account: Identification, minimum age, and residency status needed to open an account

- Types of Bank Accounts: Overview of checking, savings, and other account types suitable for payroll deposits

- Payroll Check Deposit Process: Steps to deposit a payroll check into a new or existing bank account

- Bank Account Fees: Explanation of potential fees associated with bank accounts, such as maintenance or overdraft charges

- Direct Deposit Options: Information on setting up direct deposit for payroll, including benefits and how to enroll

![]()

Requirements for Opening a Bank Account: Identification, minimum age, and residency status needed to open an account

To open a bank account, individuals must meet specific requirements regarding identification, minimum age, and residency status. These criteria are essential for banks to verify the identity of the account holder, ensure compliance with legal regulations, and assess the potential risks associated with the account.

Identification requirements typically include presenting a valid government-issued ID, such as a driver's license, passport, or state ID card. Some banks may also accept other forms of identification, such as a military ID or a foreign passport, depending on their policies and the individual's circumstances. It is crucial to ensure that the identification provided is up-to-date and matches the name and address listed on the account application.

The minimum age requirement for opening a bank account varies depending on the bank and the type of account being opened. Generally, individuals must be at least 18 years old to open a bank account independently. However, some banks offer accounts for minors, often referred to as youth or student accounts, which can be opened with parental consent and supervision. These accounts are designed to help young people learn about banking and financial management.

Residency status is another important factor in determining eligibility for a bank account. Banks typically require account holders to have a valid address within the country where the bank operates. This is to ensure that the bank can communicate with the account holder and comply with local laws and regulations. Some banks may also have specific requirements for non-resident aliens, such as obtaining a Taxpayer Identification Number (TIN) or providing additional documentation to verify their immigration status.

In conclusion, meeting the identification, minimum age, and residency status requirements is crucial for individuals looking to open a bank account. By understanding and fulfilling these criteria, potential account holders can increase their chances of successfully opening an account and enjoying the benefits of banking services.

Handwritten Payroll Checks: A Guide to Printing Stubs

You may want to see also

Explore related products

![Customizable 3 to a Page Business Checks with Tear Off Stubs | White, Pink, Green, and Yellow Options | Compatible with 7 Ring Binders [Printed in The USA] (Pink, 54)](https://m.media-amazon.com/images/I/61TqSM9fpgL._AC_UL320_.jpg)

![]()

Types of Bank Accounts: Overview of checking, savings, and other account types suitable for payroll deposits

When considering where to deposit your payroll check, it's essential to understand the different types of bank accounts available. Each account type serves a unique purpose and offers distinct features that may align better with your financial needs.

Checking Accounts:

Checking accounts are the most common type of bank account and are designed for everyday transactions. They typically come with a debit card and checks, making them ideal for paying bills, purchasing groceries, and other regular expenses. Many checking accounts also offer online banking and mobile deposit features, allowing you to manage your finances conveniently. However, checking accounts often have lower interest rates compared to savings accounts, and some may charge monthly maintenance fees unless you meet certain requirements, such as maintaining a minimum balance or setting up direct deposits.

Savings Accounts:

Savings accounts are intended for storing money you don't need immediate access to, such as emergency funds or money you're saving for a specific goal. These accounts typically earn higher interest rates than checking accounts, helping your money grow over time. Savings accounts often have restrictions on the number of withdrawals you can make per month, and some may require a minimum balance to avoid fees. They are an excellent choice for payroll deposits if you want to set aside a portion of your income for savings or emergencies.

Money Market Accounts:

Money market accounts combine features of both checking and savings accounts. They offer higher interest rates than traditional checking accounts and provide more liquidity than savings accounts. Money market accounts often come with a debit card and checks, allowing you to make purchases and pay bills directly from the account. However, they may have higher minimum balance requirements and limit the number of transactions you can make per month.

Certificates of Deposit (CDs):

Certificates of Deposit (CDs) are time deposits that offer a fixed interest rate for a specific term, typically ranging from a few months to several years. CDs are a good option if you have a lump sum of money you want to invest for a longer period, as they generally offer higher interest rates than savings accounts. However, CDs are less liquid, and you may face penalties if you need to withdraw your money before the term expires.

When deciding which type of bank account is best for your payroll deposits, consider your financial goals, spending habits, and the features that are most important to you. It may be beneficial to consult with a bank representative to discuss your options and find the account that best suits your needs.

Does Meijer Cash Payroll Checks? A Complete Guide for Employees

You may want to see also

Explore related products

![]()

Payroll Check Deposit Process: Steps to deposit a payroll check into a new or existing bank account

To deposit a payroll check into a new or existing bank account, you'll need to follow a specific process. First, ensure you have all the necessary information and materials. This includes your check, a valid form of identification, and your bank account details. If you're opening a new account, you may also need additional documents such as proof of address or social security number.

Next, locate a bank branch or ATM that accepts check deposits. Many banks have mobile apps that allow you to deposit checks remotely, but for larger amounts or new accounts, it's often safer to visit a branch in person. When depositing at a branch, you'll typically need to fill out a deposit slip, listing the amount of the check and any other relevant details.

If you're depositing into an existing account, the process is relatively straightforward. Endorsed the back of the check with your signature and the words "For Deposit Only" to ensure it can only be deposited into your account. Then, either hand the check and deposit slip to a bank teller or insert it into an ATM following the on-screen instructions.

For new accounts, the process may take longer as the bank will need to verify your identity and set up your account. Be prepared to wait a few days for the account to be fully active and for the funds to clear. Some banks may also have specific requirements or restrictions for depositing payroll checks into new accounts, so it's best to check with them beforehand.

Finally, keep track of your deposit and ensure the funds are credited to your account correctly. If there are any issues or delays, don't hesitate to contact the bank for assistance. By following these steps, you can ensure a smooth and secure payroll check deposit process.

Exploring Payroll Check Deposits onto Prepaid Cards at 7-Eleven

You may want to see also

Explore related products

![]()

Bank Account Fees: Explanation of potential fees associated with bank accounts, such as maintenance or overdraft charges

Bank account fees can vary widely depending on the type of account and the bank's policies. One common fee is the maintenance fee, which is charged for the upkeep of the account. This fee can be waived if certain conditions are met, such as maintaining a minimum balance or setting up direct deposit.

Another potential fee is the overdraft fee, which is charged when an account holder spends more money than they have available in their account. This fee can be quite high and is often charged multiple times if the account remains overdrawn for an extended period.

Some banks also charge fees for services such as wire transfers, bounced checks, and ATM withdrawals. It's important to carefully review the fee schedule when opening a bank account to understand all potential charges.

To avoid these fees, account holders can take steps such as monitoring their account balance regularly, setting up overdraft protection, and using in-network ATMs. Additionally, some banks offer fee-free accounts or waive fees for certain groups, such as students or seniors.

In conclusion, understanding and managing bank account fees is an important part of maintaining a healthy financial relationship with a bank. By being aware of potential fees and taking steps to avoid them, account holders can save money and ensure that their banking experience is as smooth as possible.

Streamline Your Payroll: FreshBooks' Check Printing and Processing Capabilities

You may want to see also

Explore related products

![]()

Direct Deposit Options: Information on setting up direct deposit for payroll, including benefits and how to enroll

Setting up direct deposit for payroll is a convenient and efficient way to receive your earnings. To enroll in direct deposit, you'll typically need to provide your employer with your bank account information, including the routing number and account number. This information can usually be found on the bottom of your checks or by logging into your online banking account.

One of the main benefits of direct deposit is the speed at which you receive your funds. Unlike traditional paper checks, which can take several days to clear, direct deposit allows your earnings to be available in your account on the same day your employer processes payroll. This can be especially helpful for those who need to pay bills or make purchases quickly.

Another advantage of direct deposit is the reduced risk of lost or stolen checks. Since your earnings are deposited directly into your account, there's no need to worry about a physical check being misplaced or taken by someone else. Additionally, direct deposit can help reduce the amount of paper waste generated by traditional payroll checks, making it a more environmentally friendly option.

To set up direct deposit, you'll need to follow your employer's specific enrollment process. This may involve filling out a form, providing documentation, or completing an online application. Your employer may also require you to have a certain type of bank account or meet other eligibility criteria. It's important to note that some employers may charge a fee for direct deposit, so be sure to check with your employer before enrolling.

Once you've enrolled in direct deposit, it's important to monitor your account regularly to ensure that your earnings are being deposited correctly. If you notice any discrepancies or issues, be sure to contact your employer or bank immediately to resolve the problem. By taking advantage of direct deposit, you can enjoy faster access to your earnings, reduced risk of lost or stolen checks, and a more environmentally friendly payroll process.

Can Your Employer Garnish Your Entire Paycheck? Know Your Rights

You may want to see also

Frequently asked questions

Yes, you can open a bank account with a payroll check. Most banks accept payroll checks as a form of identification and proof of income when opening a new account.

In addition to a payroll check, you may need to provide a valid government-issued ID, such as a driver's license or passport, and possibly proof of address, like a utility bill or lease agreement.

Requirements can vary by bank, but generally, the payroll check must be recent (usually within 30-60 days) and drawn from an account at a different bank. Some banks may also have minimum deposit requirements or specific account types that are eligible for opening with a payroll check.