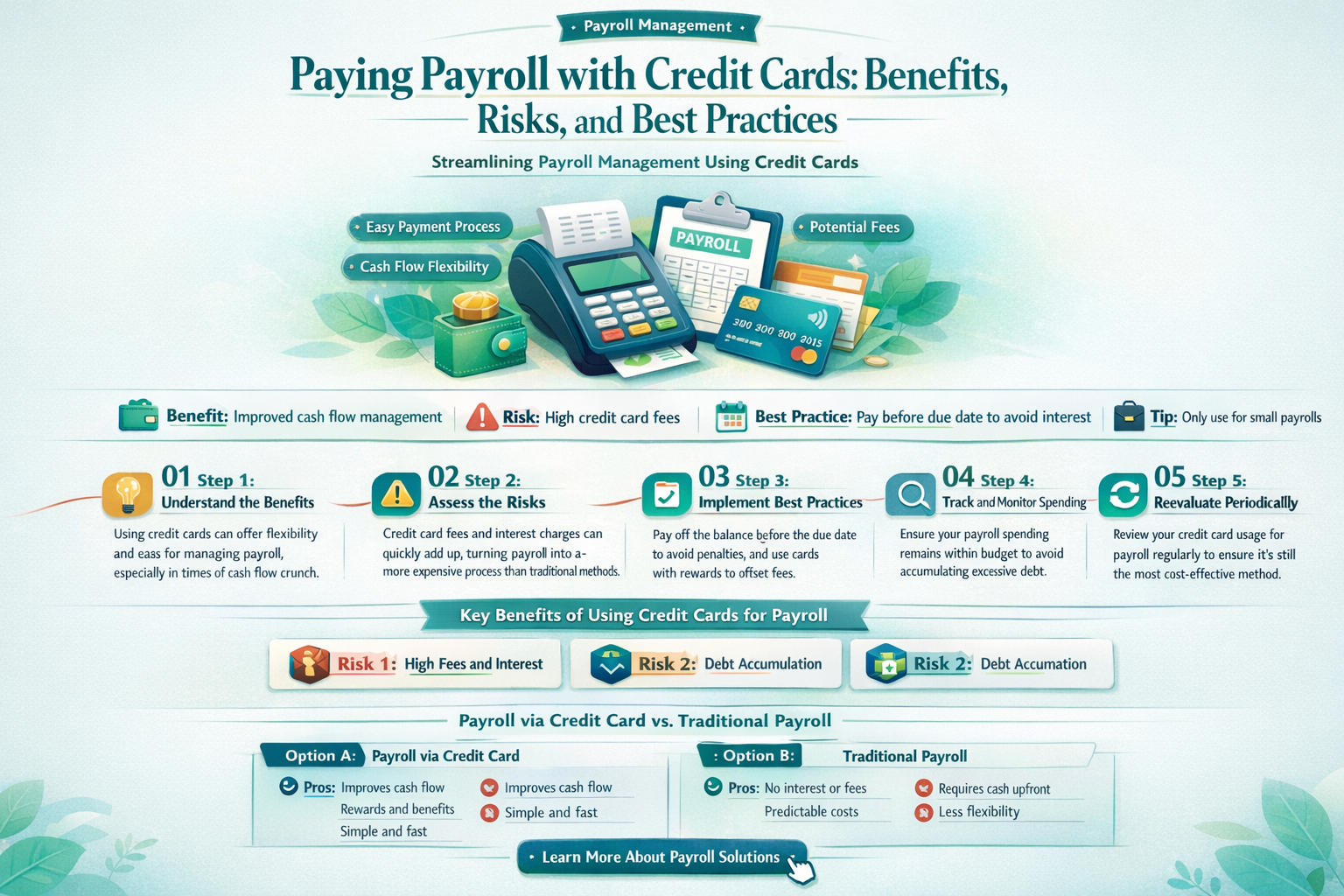

Paying payroll with a credit card is a topic that often arises among business owners seeking flexibility in managing cash flow. While it may seem like a convenient solution, especially during tight financial periods, there are important considerations to weigh. Using a credit card for payroll can help bridge temporary gaps in liquidity, but it also comes with potential drawbacks, such as high transaction fees, interest charges, and the risk of accumulating debt. Additionally, not all payroll processors accept credit card payments, and employees may prefer direct deposit or other traditional methods. Before opting for this approach, businesses should carefully evaluate their financial situation, explore alternative funding options, and ensure compliance with tax and labor regulations.

| Characteristics | Values |

|---|---|

| Feasibility | Possible, but not directly through most payroll providers. Requires third-party services or workarounds. |

| Third-Party Services | Platforms like Plastiq, Melio, or Bill.com allow payroll payments via credit card for a fee (typically 2.5-3% of the transaction). |

| Fees | Transaction fees range from 2.5% to 3% of the payroll amount, depending on the service used. |

| Credit Card Rewards | Potential to earn rewards (points, cashback) on payroll payments, but may be offset by fees. |

| Payroll Providers | Most major payroll providers (e.g., ADP, Gusto, Paychex) do not accept credit cards directly. |

| Employee Impact | Employees receive payments as usual; no direct impact on their compensation method. |

| Cash Flow Benefits | Can improve cash flow by delaying payroll expenses until the credit card bill is due. |

| Tax Implications | Fees may be tax-deductible as a business expense, but consult a tax professional. |

| Risks | High fees can negate benefits; risk of accumulating credit card debt if not managed properly. |

| Alternatives | ACH transfers, debit cards, or payroll financing options are often more cost-effective. |

Explore related products

What You'll Learn

![]()

Fees and Processing Costs

Payroll processing via credit card isn’t free—fees can quickly erode the benefits. Most credit card processors charge a percentage of each transaction (typically 1.5% to 3.5%) plus a flat fee (around $0.10 to $0.30 per transaction). For a small business with a $10,000 payroll, this could mean $150 to $350 in fees per pay run. Multiply that by monthly or biweekly cycles, and the costs become unsustainable without careful planning.

Example: A company with 10 employees paid biweekly at $2,000 each would face $300 to $700 in fees per cycle using a 1.5% to 3.5% rate. Annually, that’s $7,800 to $18,200—a significant expense. Some payroll processors or credit card companies may cap fees or offer tiered rates, but these are rare and often come with strings attached, like minimum processing volumes or long-term contracts.

Analyzing the cost-benefit ratio is critical. If using a credit card for payroll earns rewards (e.g., 2% cashback), the net cost might be manageable. However, rewards programs often exclude payroll transactions or cap earnings. Additionally, credit card interest rates (averaging 20% to 25% APR) can compound if balances aren’t paid in full, turning a short-term solution into long-term debt.

Practical tip: Compare total fees against alternatives like ACH transfers (typically $0.50 to $1.50 per transaction) or payroll services with flat monthly fees. For instance, Gusto charges $40/month plus $6/employee, while Square Payroll starts at $35/month with no per-employee fee. If credit card fees exceed $200/month, traditional methods are often cheaper.

Caution: Some processors charge additional fees for "card-not-present" transactions, which payroll payments often fall under. Others may impose penalties for high-volume or high-risk transactions, categorizing payroll as such due to its recurring nature. Always review the fine print to avoid hidden costs.

Consequences of Payroll Shortfalls: What Happens When Companies Can't Pay Employees?

You may want to see also

Explore related products

![]()

Employee Payment Methods

Paying employees with a credit card is possible but comes with significant caveats. Many payroll processors and platforms now offer credit card payment options, often through integrations with services like Square, Stripe, or PayPal. However, this method is typically reserved for contractors or freelancers rather than full-time employees due to legal and financial complexities. For instance, Gusto allows credit card payments for contractors but not W-2 employees, while ADP requires employers to use direct deposit or paper checks for traditional payroll. Understanding these limitations is crucial before considering credit card payments as a viable option.

From a financial perspective, using a credit card for payroll can be a double-edged sword. On one hand, it allows employers to earn rewards or points on large transactions, potentially offsetting processing fees. For example, a business spending $50,000 monthly on payroll could earn 2% cashback, totaling $1,000. However, processing fees for credit card transactions typically range from 2.5% to 3.5%, which could negate any rewards earned. Additionally, carrying a balance on a credit card incurs high interest rates, often exceeding 20% APR, making this method unsustainable for long-term use. Employers must weigh these financial implications carefully.

Legally, paying employees with a credit card raises compliance issues. The Fair Labor Standards Act (FLSA) requires employers to pay employees in cash or its equivalent, such as a check or direct deposit. Credit card payments may not meet this standard, especially if employees are charged fees to access their funds. Furthermore, state laws often dictate acceptable payment methods, with some explicitly prohibiting credit card payments for W-2 employees. For example, California requires employers to pay wages by check, direct deposit, or payroll debit card, with no mention of credit cards. Ignoring these regulations can result in penalties or lawsuits.

Despite the challenges, credit card payments can be a temporary solution in emergencies. For instance, if a business faces a cash flow shortage, using a credit card to cover payroll ensures employees are paid on time, avoiding morale and legal issues. However, this should be a last resort, with a clear plan to repay the balance immediately. Employers can also explore alternatives like payroll financing or short-term loans, which offer lower interest rates and fewer compliance risks. In such cases, transparency with employees is key—communicating the situation and assuring them of timely payment builds trust.

In conclusion, while paying payroll with a credit card is technically feasible, it is rarely the best option for traditional employees. Employers should prioritize direct deposit or checks for W-2 workers, reserving credit card payments for contractors when necessary. For businesses considering this method, consulting with a payroll expert or attorney is essential to ensure compliance and avoid financial pitfalls. Ultimately, the goal is to balance convenience with legal and financial responsibility, ensuring employees are paid accurately and on time.

Explore related products

![]()

Credit Card Rewards Benefits

Paying payroll with a credit card can unlock a treasure trove of rewards, but only if you strategize carefully. Many business credit cards offer lucrative cashback, points, or miles on everyday spending, including payroll. For instance, the Chase Ink Business Preferred card provides 3x points on the first $150,000 spent annually on categories like shipping, advertising, and travel, but payroll processing fees could still qualify as eligible spending. By leveraging such rewards, businesses can effectively offset a portion of their payroll costs, turning a necessary expense into an opportunity for financial gain.

However, not all credit card rewards are created equal, and maximizing benefits requires a tailored approach. Start by evaluating your payroll frequency and total costs to determine the potential rewards value. For example, if your monthly payroll is $50,000 and your card offers 2% cashback, you could earn $1,000 annually. Next, factor in processing fees, typically 2-4% of the transaction amount. If the rewards outweigh the fees, proceed, but always ensure the card’s rewards structure aligns with your business’s spending patterns. A card that rewards payroll-related expenses, like the American Express Blue Business Plus with 2x Membership Rewards points on all purchases up to $50,000 annually, could be ideal.

One often-overlooked benefit of using credit cards for payroll is the ability to consolidate expenses and streamline financial tracking. By charging payroll to a single card, businesses can simplify record-keeping and gain clearer insights into cash flow. Additionally, many business credit cards offer expense management tools, such as QuickBooks integration, which can save time and reduce administrative burdens. This efficiency, combined with rewards, makes credit card payroll payments a compelling option for businesses seeking to optimize their financial operations.

Despite the advantages, caution is essential. High processing fees can erode rewards if not managed properly. To mitigate this, negotiate lower fees with your payroll processor or explore platforms like Gusto or Square Payroll, which often partner with credit card companies to offer reduced rates. Another strategy is to use a card with a sign-up bonus that offsets initial fees. For example, the Capital One Spark Miles for Business card offers 50,000 miles after spending $4,500 in the first three months, which can cover several months of payroll processing fees.

In conclusion, paying payroll with a credit card can be a rewarding strategy if executed thoughtfully. By selecting a card with a robust rewards program, factoring in processing fees, and leveraging additional benefits like expense management tools, businesses can turn payroll into a profitable endeavor. Always monitor your spending and rewards to ensure the strategy remains cost-effective, and remember that the key to success lies in aligning your card’s benefits with your business’s unique financial needs.

Explore related products

![[10 Rolls] Thermal Paper Receipt Rolls 2 1/4 x 50, Premium Quality Paper fits all Credit Card Terminals, 48g Weight, POS Cash Register Paper](https://m.media-amazon.com/images/I/613tfSQFCrL._AC_UL320_.jpg)

![]()

Cash Flow Management Tips

Paying payroll with a credit card can be a double-edged sword for businesses, particularly small ones. While it offers a temporary cash flow solution, it introduces risks like high interest rates and potential debt accumulation. To navigate this strategy effectively, consider these cash flow management tips tailored to this scenario.

Strategic Timing and Rewards Maximization: If you decide to pay payroll with a credit card, time it strategically. Aim to pay off the balance before the grace period ends to avoid accruing interest. Additionally, choose a credit card with rewards that align with your business needs, such as cashback or travel points. For instance, a 2% cashback card on a $10,000 payroll could yield $200 in rewards, offsetting some processing fees. However, ensure the rewards value exceeds the fees, typically 2-4% of the transaction amount.

Emergency-Only Approach: Treat credit card payroll payments as a last-resort option, not a regular practice. Analyze your cash flow patterns to identify recurring shortfalls and address them through cost-cutting, invoicing improvements, or financing alternatives like a line of credit. For example, if late-paying clients are the issue, implement stricter payment terms or offer early payment discounts to improve liquidity. Reserve credit card payroll payments for unforeseen emergencies, such as a sudden drop in revenue or unexpected expenses.

Fee Mitigation and Alternative Solutions: Credit card processing fees can erode your margins, especially on large payroll transactions. Explore alternatives like payroll financing or employee payment platforms that offer lower fees. For instance, some platforms charge a flat 1% fee compared to credit card rates. If you must use a credit card, negotiate with processors for lower rates or consider cards with no processing fees for the first year. Additionally, evaluate the tax implications, as credit card interest may not be tax-deductible in all jurisdictions.

Cash Flow Forecasting and Buffer Building: Implement robust cash flow forecasting to anticipate payroll needs and avoid last-minute credit card reliance. Tools like QuickBooks or Xero can help project cash positions weeks in advance. Aim to maintain a cash buffer equivalent to 1-2 months of payroll expenses in a high-yield savings account. For a $50,000 monthly payroll, this means saving $50,000-$100,000. While building this buffer, prioritize reducing non-essential expenses and accelerating receivables to free up cash.

Employee Communication and Contingency Planning: Transparency is key when considering credit card payroll payments. Communicate with employees about potential delays or alternative payment methods in case of cash flow disruptions. Develop a contingency plan that includes prioritizing critical payments, such as payroll taxes and employee wages, over discretionary expenses. For example, if using a credit card for payroll, ensure tax obligations are still met on time to avoid penalties. Regularly review and update this plan as your cash flow situation evolves.

Explore related products

![]()

Tax and Compliance Issues

Payroll taxes are a non-negotiable obligation, and using a credit card to pay wages doesn't alter this fact. Employers remain responsible for withholding and remitting federal, state, and local payroll taxes, regardless of the payment method. The IRS and state tax agencies require timely deposits of these taxes, typically through the Electronic Federal Tax Payment System (EFTPS) or state-specific systems. Using a credit card for payroll doesn't automatically integrate with these systems, so employers must manually ensure compliance. Failure to do so can result in penalties, interest, and even legal action.

From a tax perspective, paying payroll with a credit card introduces complexities in expense categorization. Credit card transactions are often treated as purchases rather than payroll expenses, which can muddy the waters during tax reporting. For instance, if payroll expenses are mistakenly categorized as general business expenses, it could lead to discrepancies in tax deductions or trigger audits. To avoid this, employers must meticulously track and classify these transactions, ensuring they align with IRS guidelines for payroll tax reporting.

Compliance with labor laws is another critical consideration. Many states have specific regulations regarding wage payments, including acceptable methods. While some states permit credit card payments for wages, others explicitly prohibit it or require written consent from employees. Employers must verify state-specific laws to avoid violating labor regulations. For example, California requires employers to pay wages in cash, check, or direct deposit unless the employee voluntarily agrees to another method. Ignoring such rules can result in fines, lawsuits, or damage to the employer’s reputation.

Finally, the use of credit cards for payroll can inadvertently create a paper trail that raises red flags during audits. Tax authorities scrutinize unusual payment methods, and credit card transactions for payroll may prompt closer examination. To mitigate this risk, employers should maintain detailed records, including employee consent forms (if required), transaction receipts, and clear documentation linking the credit card payments to specific payroll periods. Proactive documentation not only ensures compliance but also provides a defense in case of an audit.

In summary, while paying payroll with a credit card may seem convenient, it demands rigorous attention to tax and compliance issues. Employers must navigate payroll tax obligations, accurately categorize expenses, adhere to state labor laws, and prepare for potential audits. By addressing these challenges systematically, businesses can use this payment method without compromising their legal or financial standing.

Frequently asked questions

Yes, you can pay payroll with a credit card, but it’s not a common or recommended practice due to potential fees, interest charges, and cash flow implications.

Yes, using a credit card for payroll may incur processing fees, cash advance fees, or higher interest rates, depending on your card issuer and payroll provider.

While it’s technically legal, most payroll systems and employers prefer direct deposit or checks. Employees may also prefer traditional payment methods for consistency and reliability.

Potential benefits include earning rewards or points on the transaction, delaying payment until the credit card bill is due, and temporarily improving cash flow for businesses with tight finances.

Risks include high fees, accruing interest if the balance isn’t paid in full, potential damage to credit scores, and the possibility of exceeding credit limits, which could disrupt payroll processing.