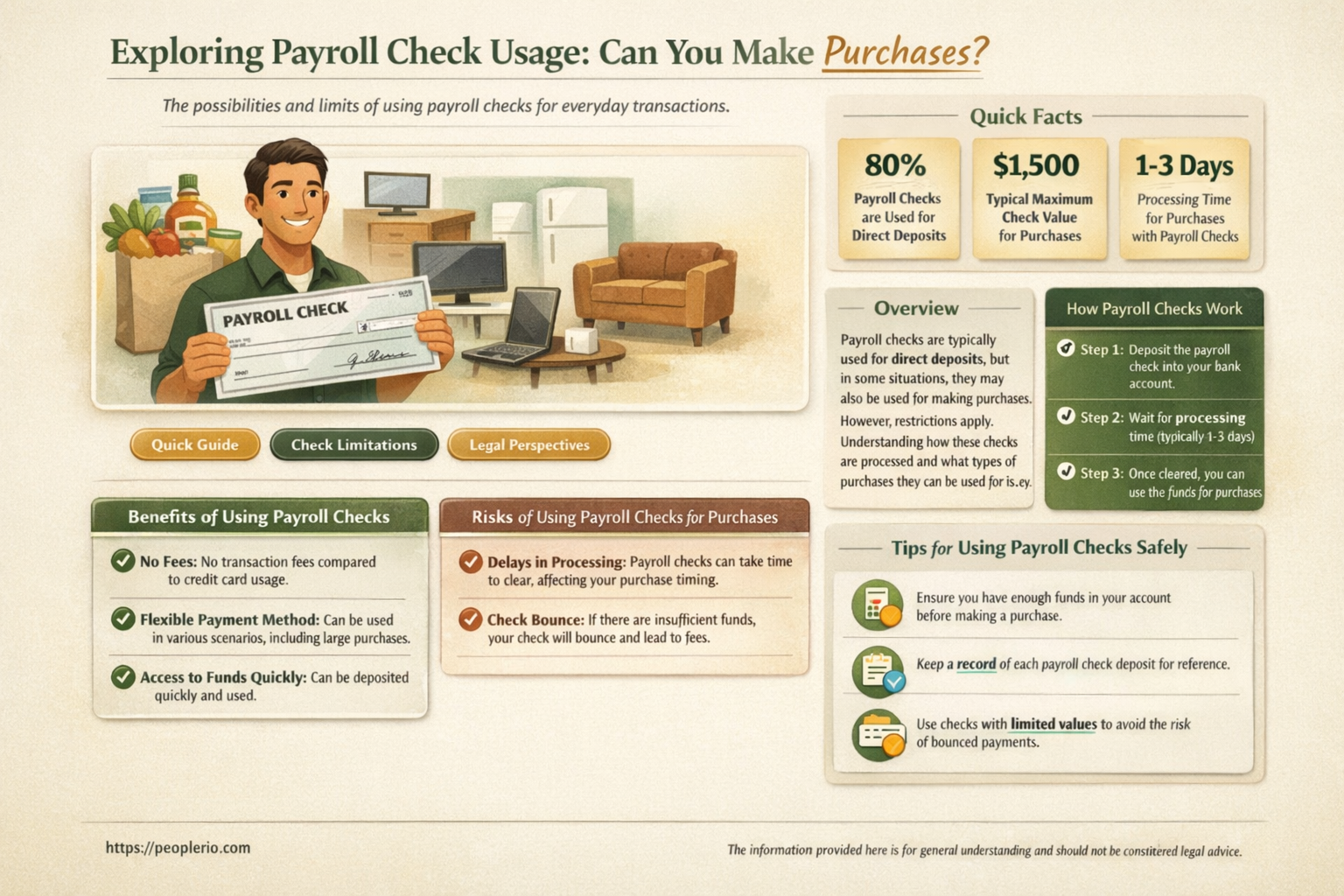

When it comes to using a payroll check for purchases, there are several factors to consider. Payroll checks are typically issued by employers to employees as compensation for work performed. These checks are drawn from the employer's bank account and are generally used for depositing into the employee's personal bank account. However, some employers may allow employees to use their payroll checks for direct purchases, depending on company policy and the nature of the transaction. It's important to note that using a payroll check for purchases may have implications for both the employee and the employer, including potential tax and accounting considerations. Additionally, the use of payroll checks for purchases may be subject to certain restrictions or limitations imposed by the employer or financial institution.

| Characteristics | Values |

|---|---|

| Type of Check | Payroll Check |

| Purpose | To buy something |

| Acceptability | Depends on the store/merchant |

| Legal Tender | Yes, in most cases |

| Security Features | Typically includes signature, routing number, account number, and check number |

| Processing Time | May take 1-3 business days to clear |

| Fees | Possible processing fees by the merchant |

| Record Keeping | Provides a paper trail for the transaction |

| Reversibility | Generally non-reversible once cashed or deposited |

| Alternatives | Cash, credit/debit cards, electronic transfers |

Explore related products

What You'll Learn

- Understanding Payroll Checks: Explanation of what a payroll check is and how it works

- Check Cashing Options: Overview of where and how you can cash a payroll check

- Using Payroll Checks for Purchases: Guidance on using payroll checks to make purchases directly

- Potential Fees and Limits: Information on any fees or limits associated with using payroll checks

- Alternatives to Payroll Checks: Discussion of alternative payment methods that might be more convenient

![]()

Understanding Payroll Checks: Explanation of what a payroll check is and how it works

A payroll check is a financial instrument issued by an employer to an employee as compensation for work performed. It serves as a written, dated, and signed instrument that directs a bank to pay a specific sum of money to the bearer. Payroll checks are typically issued on a regular basis, such as weekly, biweekly, or monthly, and are a common method of payment for employees in many industries.

To understand how a payroll check works, it's essential to familiarize yourself with the various components of the check. These typically include the employer's name and address, the employee's name and address, the check number, the date of issue, the amount of money being paid (both in numerical and written form), and the employer's signature or the signature of an authorized representative. Additionally, payroll checks may include information such as the employee's social security number, the tax year, and the amount of taxes withheld.

When an employee receives a payroll check, they can deposit it into their bank account or cash it at a bank or other financial institution. The funds are then made available for the employee to use as they see fit, whether that's to pay bills, make purchases, or save for the future. It's important to note that payroll checks are subject to various laws and regulations, including those related to minimum wage, overtime pay, and tax withholding.

One common question that employees may have is whether they can use a payroll check to make purchases directly. The answer to this question depends on the specific circumstances and the policies of the employer and the merchant. Some employers may issue payroll checks that are specifically designed for direct deposit or electronic payment, while others may issue checks that can be used for purchases at certain retailers or service providers.

In general, it's advisable to deposit or cash a payroll check before attempting to use it for purchases. This ensures that the funds are properly accounted for and that the employee has a clear record of their earnings and expenditures. Additionally, using a payroll check for purchases may be subject to fees or other restrictions, so it's important to check with the employer and the merchant before proceeding.

In conclusion, understanding payroll checks is an essential aspect of managing one's finances as an employee. By familiarizing oneself with the components of a payroll check and how it works, employees can make informed decisions about how to use their earnings and ensure that they are in compliance with relevant laws and regulations.

Navigating Finances After Loss: Can You Receive Your Deceased Husband's Payroll Check?

You may want to see also

Explore related products

![Customizable 3 to a Page Business Checks with Tear Off Stubs | White, Pink, Green, and Yellow Options | Compatible with 7 Ring Binders [Printed in The USA] (American Eagle, 54)](https://m.media-amazon.com/images/I/618e1m5EVoL._AC_UL320_.jpg)

![]()

Check Cashing Options: Overview of where and how you can cash a payroll check

If you've received a payroll check and are wondering where and how you can cash it, you have several options available. One of the most common places to cash a payroll check is at a bank or credit union. If you have an account with the financial institution, you can simply deposit the check into your account and access the funds once the check has cleared. Many banks also offer the option to cash checks at their branches, even if you don't have an account with them, though they may charge a fee for this service.

Another option for cashing a payroll check is at a check cashing store. These stores specialize in cashing checks and typically offer instant cash for a fee. The fees can vary depending on the amount of the check and the specific store, so it's important to shop around and compare rates before choosing a check cashing service.

Some employers also offer the option to have your payroll check directly deposited into your bank account. This can be a convenient and secure way to receive your pay, as the funds are automatically transferred and available for use on payday. If your employer offers this service, you can usually set it up by providing your bank account information to your payroll department.

In addition to traditional banking and check cashing services, there are also online options for cashing payroll checks. Some online services allow you to upload a photo of your check and receive the funds electronically, often within a day or two. These services can be convenient if you don't have easy access to a bank or check cashing store, but be sure to research the fees and security measures before using an online check cashing service.

When cashing a payroll check, it's important to consider the fees and convenience of each option. If you have a bank account, depositing the check is likely the most cost-effective and secure choice. However, if you need cash quickly or don't have a bank account, a check cashing store or online service may be a better option, despite the potential fees.

Cashing Michigan Payroll Checks in Ohio: What You Need to Know

You may want to see also

Explore related products

![]()

Using Payroll Checks for Purchases: Guidance on using payroll checks to make purchases directly

Payroll checks are typically used for depositing into a bank account or cashing to receive payment for work performed. However, in certain situations, you might consider using a payroll check to make direct purchases. This could be due to a lack of access to a bank account, a preference for not carrying cash, or simply for convenience.

Before using a payroll check for purchases, it's essential to understand the potential risks and limitations involved. Firstly, not all businesses or individuals will accept payroll checks as a form of payment. This is because payroll checks are not as widely recognized or trusted as personal checks or credit/debit cards. Additionally, there may be fees associated with cashing or depositing payroll checks, which could reduce the overall value of the check.

If you do decide to use a payroll check for purchases, there are a few steps you should follow to ensure a smooth transaction. Firstly, make sure the check is properly endorsed with your signature and any required identification information. Secondly, verify that the business or individual you are making the purchase from accepts payroll checks. You may want to call ahead or check their website to confirm this information.

When making the purchase, be prepared to provide any necessary identification or documentation to verify that you are the rightful owner of the check. This could include a driver's license, social security card, or other forms of identification. It's also a good idea to have a backup plan in case the business or individual does not accept payroll checks, such as having cash or a credit/debit card on hand.

In conclusion, while using a payroll check for purchases is possible, it's important to weigh the potential risks and limitations before proceeding. By following the proper steps and being prepared for any challenges, you can increase the likelihood of a successful transaction.

Cashing Payroll Checks at Western Union: A Convenient Option?

You may want to see also

Explore related products

![]()

Potential Fees and Limits: Information on any fees or limits associated with using payroll checks

Payroll checks, while a common method of payment for employees, do come with certain fees and limits that users should be aware of. One of the primary fees associated with payroll checks is the check cashing fee. This fee is typically charged by banks or check cashing services and can vary depending on the institution and the amount of the check. For example, some banks may charge a flat fee of $5 to $10 for cashing a payroll check, while others may charge a percentage of the check amount, usually around 1% to 3%.

In addition to check cashing fees, there may also be limits on the amount of money that can be cashed or deposited using a payroll check. These limits can vary depending on the bank or financial institution and may be based on factors such as the account holder's history, the amount of the check, and the type of account being used. For instance, some banks may have a daily deposit limit of $5,000 to $10,000 for payroll checks, while others may have no specific limit but may require additional documentation or verification for larger amounts.

Another potential fee associated with payroll checks is the overdraft fee. If a payroll check is cashed or deposited and the account does not have sufficient funds to cover the amount, the bank may charge an overdraft fee. This fee can be quite high, often ranging from $25 to $35 per occurrence. To avoid overdraft fees, it is important for users to keep track of their account balance and ensure that there are sufficient funds available to cover the payroll check.

Furthermore, some employers may impose limits on the use of payroll checks. For example, an employer may only allow payroll checks to be used for certain types of purchases or may require employees to use direct deposit for their paychecks. It is important for employees to be aware of their employer's policies regarding payroll checks to avoid any potential issues or penalties.

In conclusion, while payroll checks are a convenient way to receive payment, they do come with certain fees and limits that users should be aware of. By understanding these potential costs and restrictions, users can make informed decisions about how to best use their payroll checks and avoid any unnecessary fees or complications.

Does Food Lion Cash Payroll Checks? Your Payment Options Explained

You may want to see also

Explore related products

![]()

Alternatives to Payroll Checks: Discussion of alternative payment methods that might be more convenient

Direct deposit stands out as a prevalent alternative to traditional payroll checks, offering both employers and employees a streamlined payment process. This method eliminates the need for physical checks, reducing the risk of loss or theft and ensuring funds are available immediately on payday. Employees can typically access their pay stubs electronically, providing a convenient record-keeping solution.

Another option gaining traction is the use of prepaid debit cards. These cards function similarly to direct deposit but provide the added flexibility of a physical card for purchases and ATM withdrawals. Prepaid debit cards can be particularly beneficial for employees who prefer cash transactions or lack access to traditional banking services. Employers may also find this method cost-effective, as it can reduce the administrative burden associated with check issuance.

Mobile payment apps have also emerged as a viable alternative, allowing employees to receive and manage their pay directly through their smartphones. These apps often integrate with existing payroll systems, enabling seamless fund transfers and real-time notifications. Additionally, mobile payment apps may offer features such as budgeting tools and financial tracking, empowering employees to take greater control of their finances.

In some cases, employers may opt to issue payroll cards, which function similarly to prepaid debit cards but are specifically designed for payroll purposes. Payroll cards can be loaded with funds directly from the employer's account, providing a secure and efficient means of payment. This method can be particularly advantageous for businesses with a large number of employees or those operating in industries where cash transactions are common.

When considering alternatives to payroll checks, it's essential for employers to weigh the benefits and drawbacks of each method. Factors such as cost, convenience, security, and employee preferences should all be taken into account. By exploring these options, businesses can find a payment solution that best suits their needs and enhances the overall payroll experience for their employees.

Who Bears Responsibility When a Payroll Check Bounces? Key Insights

You may want to see also

Frequently asked questions

Yes, you can use a payroll check to make purchases, just like any other check. Ensure the check is properly endorsed and the funds are available in your account.

Generally, there are no specific restrictions on using a payroll check for purchases. However, some retailers may have policies against accepting payroll checks, so it's best to confirm with the seller beforehand.

To endorse a payroll check, sign the back of the check in the designated endorsement area. You may also need to include your account number or other identifying information, depending on the check issuer's requirements.

If a retailer refuses to accept your payroll check, you can try to negotiate with them or offer to provide additional identification or verification. Alternatively, you can use a different form of payment or visit another retailer that accepts payroll checks.