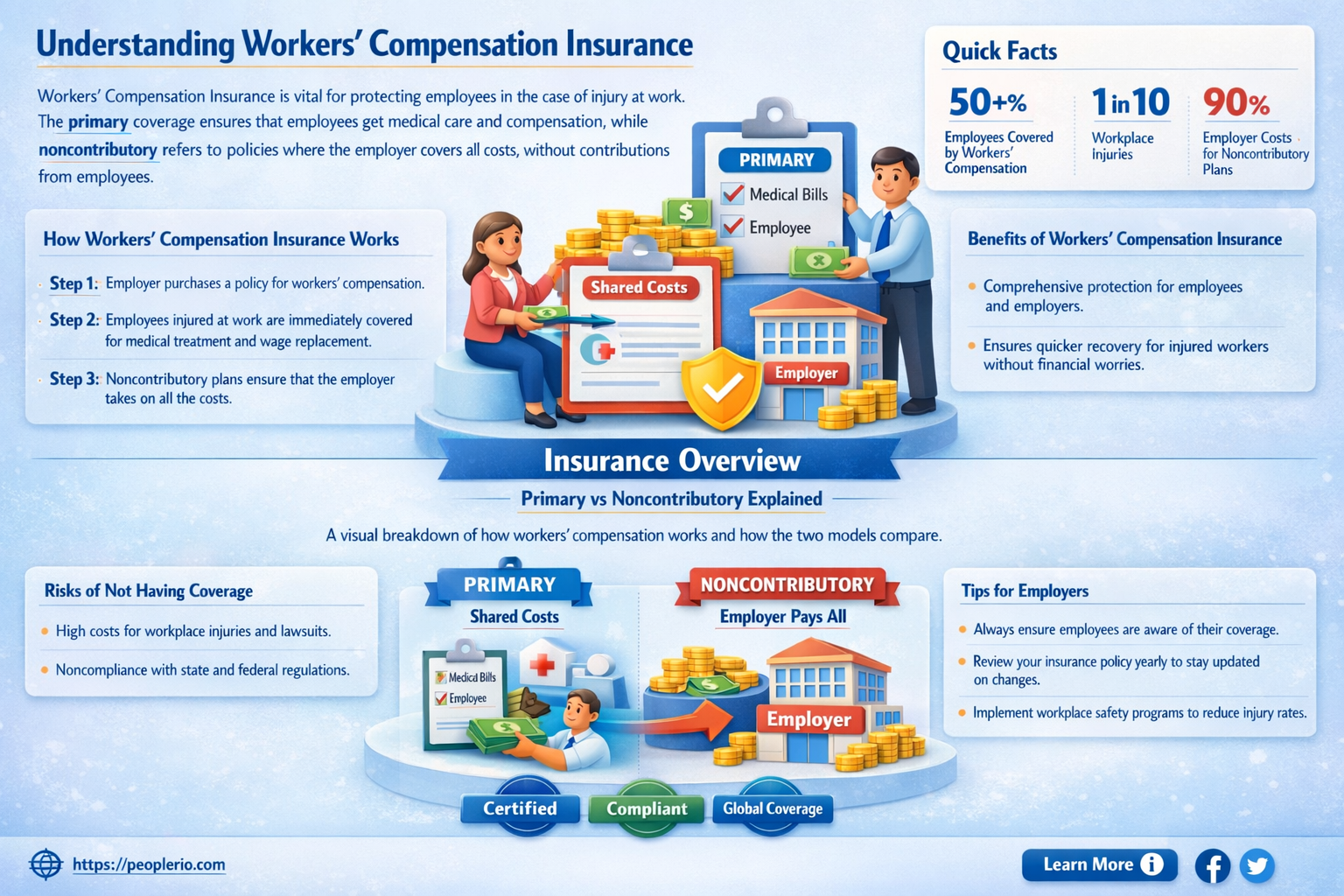

Workers' compensation insurance is a crucial aspect of employee benefits, designed to provide financial protection to workers who suffer job-related injuries or illnesses. In many jurisdictions, it is mandatory for employers to carry this type of insurance to ensure that employees receive necessary medical care and wage replacement without having to sue their employer. The question of whether workers' compensation insurance can be both primary and noncontributory is significant, as it pertains to the exclusivity of the benefits provided and the extent to which employees may seek additional compensation through other means, such as personal injury lawsuits. Primary insurance implies that it is the first line of coverage, while noncontributory means that the employee does not contribute to the cost of the insurance. Understanding the nuances of these terms is essential for both employers and employees to navigate the complexities of workers' compensation claims effectively.

| Characteristics | Values |

|---|---|

| Coverage Type | Primary and Noncontributory |

| Purpose | To provide medical and wage replacement benefits to employees injured on the job |

| Funding | Employer-funded through insurance premiums |

| Employee Contribution | None required |

| Benefit Coordination | Coordinates with other benefits like Social Security Disability Insurance (SSDI) |

| Legal Requirement | Mandated by state laws in most U.S. states |

| Policy Provisions | Typically includes medical expenses, lost wages, rehabilitation costs, and death benefits |

| Claim Process | Employee must report injury to employer and file a claim with the insurance provider |

| Appeals Process | Available if claim is denied, varies by state and policy |

Explore related products

What You'll Learn

- Definition of Primary and Noncontributory Insurance: Explains the basic concepts and how they apply to workers' compensation

- Legal Requirements by State: Discusses the varying state laws regarding primary and noncontributory workers' compensation insurance

- Benefits for Employers: Outlines the advantages for employers in opting for primary and noncontributory workers' compensation coverage

- Impact on Employee Claims: Examines how primary and noncontributory insurance affects the claims process and benefits for employees

- Comparison with Contributory Insurance: Contrasts primary and noncontributory insurance with contributory insurance, highlighting key differences

![]()

Definition of Primary and Noncontributory Insurance: Explains the basic concepts and how they apply to workers' compensation

Primary and noncontributory insurance are terms used in the context of workers' compensation to define the roles and responsibilities of different insurance carriers. Primary insurance refers to the main insurance policy that covers the majority of the risk. In workers' compensation, this is typically the policy held by the employer to cover their employees. Noncontributory insurance, on the other hand, is a secondary policy that provides additional coverage but does not contribute to the primary policy's premiums or benefits.

In the realm of workers' compensation, noncontributory insurance often comes into play when an employee is injured or becomes ill due to work-related activities. This type of insurance can help cover medical expenses, lost wages, and other costs associated with the employee's recovery. However, it's important to note that noncontributory insurance does not replace the primary policy; rather, it supplements it.

One key aspect of primary and noncontributory insurance in workers' compensation is the concept of subrogation. Subrogation allows the primary insurer to recover costs from the noncontributory insurer when the latter's policy covers some or all of the claim. This process helps ensure that the primary insurer is not unfairly burdened with the entire cost of the claim.

Another important consideration is the coordination of benefits between primary and noncontributory policies. This coordination ensures that the injured employee receives the appropriate level of coverage without duplication of benefits. For example, if the primary policy covers 80% of the employee's medical expenses, the noncontributory policy may cover the remaining 20%.

In conclusion, understanding the definitions and applications of primary and noncontributory insurance in workers' compensation is crucial for employers, employees, and insurance carriers alike. By clearly defining these terms and their roles, all parties can better navigate the complexities of workers' compensation claims and ensure that injured employees receive the appropriate level of coverage and support.

Georgia Workers' Compensation Insurance: Legal Requirements for Employers

You may want to see also

Explore related products

![]()

Legal Requirements by State: Discusses the varying state laws regarding primary and noncontributory workers' compensation insurance

Workers' compensation insurance can indeed be both primary and noncontributory, but the legal requirements for such insurance vary significantly by state. This section delves into the nuances of state laws that govern primary and noncontributory workers' compensation insurance, highlighting the key differences and similarities across jurisdictions.

Primary workers' compensation insurance is typically mandatory for employers, covering employees who suffer work-related injuries or illnesses. Noncontributory workers' compensation insurance, on the other hand, is often optional and covers employees who are not eligible for primary coverage, such as independent contractors or certain types of volunteers.

State laws play a crucial role in determining the specifics of primary and noncontributory workers' compensation insurance. For instance, some states require employers to carry both types of insurance, while others allow employers to choose between them. Additionally, the benefits and coverage limits for primary and noncontributory insurance can vary widely from state to state.

One key aspect of state laws regarding workers' compensation insurance is the concept of "exclusive remedy." In many states, workers' compensation insurance is considered the exclusive remedy for work-related injuries or illnesses, meaning that employees cannot sue their employers for damages beyond the benefits provided by the insurance. However, there are exceptions to this rule, and some states allow employees to pursue additional legal action in certain circumstances.

Another important consideration is the impact of state laws on the cost of workers' compensation insurance. Factors such as the state's regulatory environment, the prevalence of workplace injuries, and the average cost of medical care can all influence insurance premiums. Employers operating in states with more stringent workers' compensation laws may face higher insurance costs, while those in states with more lenient laws may enjoy lower premiums.

In conclusion, understanding the legal requirements for primary and noncontributory workers' compensation insurance is essential for employers and employees alike. By familiarizing themselves with the specific laws and regulations of their state, both parties can ensure compliance and make informed decisions about their insurance coverage.

Workplace Bullying: Can Insurance Companies Be Held Accountable?

You may want to see also

Explore related products

![]()

Benefits for Employers: Outlines the advantages for employers in opting for primary and noncontributory workers' compensation coverage

Employers who opt for primary and noncontributory workers' compensation coverage can benefit from a streamlined claims process. Since the employer is the sole contributor to the fund, there is no need for employees to contribute, which simplifies payroll deductions and reduces administrative burdens. This can lead to faster resolution of claims and quicker return to work for injured employees, ultimately saving employers time and resources.

Another advantage is the potential for cost savings. By taking on the full responsibility for funding workers' compensation claims, employers can negotiate better rates with insurance providers. This is because the risk is concentrated on the employer, and insurance companies may offer more competitive pricing to secure the business. Additionally, employers have more control over the management of claims, which can help to prevent fraudulent or exaggerated claims that could drive up costs.

Primary and noncontributory workers' compensation coverage can also enhance an employer's reputation. By demonstrating a commitment to employee safety and well-being, employers can attract and retain top talent. This type of coverage can be seen as a sign of a responsible and caring employer, which can be a valuable asset in a competitive job market.

Furthermore, this type of coverage can provide employers with greater flexibility in managing their workforce. Since the employer is not reliant on employee contributions, they have more freedom to adjust their workers' compensation policies to meet the specific needs of their business. This can include tailoring coverage to high-risk occupations or implementing return-to-work programs that are customized to the employer's operations.

In conclusion, primary and noncontributory workers' compensation coverage offers several benefits to employers, including a simplified claims process, potential cost savings, enhanced reputation, and greater flexibility in managing their workforce. By taking on the full responsibility for funding workers' compensation claims, employers can gain more control over the management of claims and demonstrate a commitment to employee safety and well-being.

Seeking Compensation: Health Insurance Broker Negligence Explained

You may want to see also

![]()

Impact on Employee Claims: Examines how primary and noncontributory insurance affects the claims process and benefits for employees

The impact of primary and noncontributory insurance on employee claims is a critical aspect of workers' compensation. Primary insurance is the first line of coverage, meaning it pays out benefits first in the event of a claim. Noncontributory insurance, on the other hand, is secondary coverage that kicks in only after the primary insurance has been exhausted. This distinction has significant implications for the claims process and the benefits employees receive.

In a primary insurance scenario, the claims process is typically more straightforward. The employee files a claim with their employer's primary insurer, which then assesses the claim and disburses benefits according to the policy terms. This can result in quicker access to medical care and wage replacement for the injured employee. However, the benefits paid out by primary insurance may be limited by the policy's coverage limits, which could leave the employee with unpaid medical bills or lost wages if the claim exceeds these limits.

Noncontributory insurance comes into play when the primary insurance coverage is insufficient to cover the full extent of the employee's claim. In this case, the noncontributory insurer steps in to cover the remaining costs. This can provide a safety net for employees, ensuring they receive the full benefits they are entitled to under workers' compensation law. However, the claims process can become more complex when noncontributory insurance is involved, as it may require additional paperwork and coordination between the primary and secondary insurers.

The interplay between primary and noncontributory insurance can also affect the overall cost of workers' compensation for employers. While primary insurance premiums are typically higher due to the increased risk of paying out claims, noncontributory insurance can help mitigate these costs by covering excess claims. This can lead to lower overall premiums for employers, but it also means they need to carefully manage their insurance policies to ensure they have adequate coverage.

In conclusion, the distinction between primary and noncontributory insurance has a significant impact on the claims process and benefits for employees under workers' compensation. Understanding this difference is crucial for both employees and employers to navigate the complexities of workers' compensation insurance effectively.

Navigating California Workers' Comp: Employer's Guide to Insurance Options

You may want to see also

![]()

Comparison with Contributory Insurance: Contrasts primary and noncontributory insurance with contributory insurance, highlighting key differences

Primary and noncontributory insurance, such as workers' compensation, stands in stark contrast to contributory insurance models. The key difference lies in the funding mechanism. In a contributory insurance system, both employers and employees pay into the insurance fund, often through payroll deductions. This shared financial responsibility is intended to ensure that the insurance remains solvent and capable of covering claims.

In contrast, primary and noncontributory insurance models do not require employee contributions. Instead, the entire financial burden falls on the employer. This can be advantageous for employees, as it means they do not have to worry about losing a portion of their wages to insurance premiums. However, it also places a greater financial strain on employers, who must budget for the full cost of the insurance.

Another significant difference is in the administration of the insurance. Contributory insurance models often involve more complex administrative processes, as they require tracking and managing contributions from both employers and employees. Primary and noncontributory models, on the other hand, are typically simpler to administer, as the employer is the sole contributor and can more easily manage the insurance costs.

The impact on workplace culture can also vary between the two models. In a contributory system, employees may feel more invested in the insurance program, as they are contributing to it directly. This could lead to a greater sense of ownership and responsibility among employees. In contrast, primary and noncontributory models may not foster the same level of employee engagement, as the financial burden is solely on the employer.

Ultimately, the choice between primary and noncontributory insurance and contributory insurance depends on a variety of factors, including the size and financial stability of the employer, the nature of the work being performed, and the regulatory environment in which the business operates. Employers must carefully consider these factors when deciding which insurance model is most appropriate for their organization.

Navigating Ethical Boundaries: Insurance Agents and Attorney Compensation Sharing

You may want to see also