The question Can you 10-99 a standard employee? refers to the practice of classifying workers as independent contractors (1099) rather than as regular employees (W-2). This classification impacts various aspects of employment, including tax obligations, benefits, and labor rights. Typically, a standard employee is someone who works regular hours, follows a set schedule, and is subject to the employer's control and direction. In contrast, independent contractors generally have more autonomy over their work, set their own schedules, and are responsible for their own taxes and benefits. The distinction between these two classifications is crucial for both employers and workers, as misclassification can lead to legal and financial consequences.

Explore related products

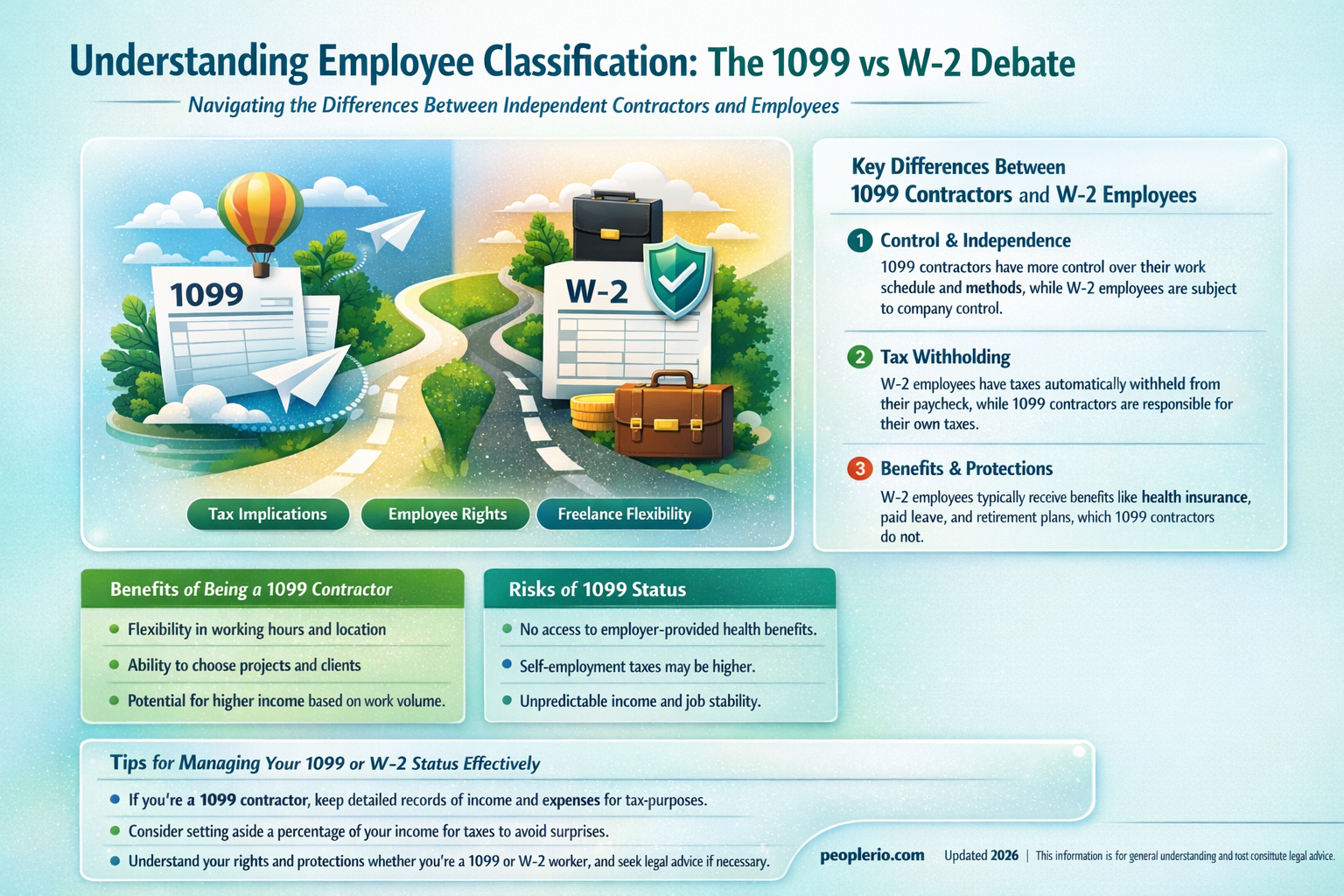

What You'll Learn

- Understanding 10-99 Forms: Explanation of what a 10-99 form is and its purpose

- Employee Classification: Criteria for classifying workers as employees or independent contractors

- Tax Implications: How issuing a 10-99 affects tax reporting and liabilities for both parties

- Legal Requirements: Overview of legal obligations when hiring and reporting independent contractors

- Common Mistakes: Frequent errors to avoid when completing and submitting 10-99 forms

![]()

Understanding 10-99 Forms: Explanation of what a 10-99 form is and its purpose

The 10-99 form, officially known as the Form 1099-MISC, is a tax document used in the United States to report miscellaneous income. It is typically issued by employers or businesses to independent contractors or freelancers who have provided services during the tax year. The form serves as a means to report non-employee compensation, which is crucial for both the payer and the recipient when filing their tax returns.

One of the primary purposes of the 10-99 form is to ensure that independent contractors are properly reported to the Internal Revenue Service (IRS). This is important because it affects how the contractors report their income and calculate their tax liability. Unlike standard employees who receive a W-2 form, independent contractors are responsible for paying their own self-employment taxes, which include both the employer and employee portions of Social Security and Medicare taxes.

When a business issues a 10-99 form, it must include specific information such as the contractor's name, address, and taxpayer identification number (TIN). The form also details the total amount of compensation paid to the contractor during the year, as well as any federal income tax withheld. Contractors use this information to complete their Schedule C (Form 1040), which is used to calculate their net earnings from self-employment and determine their tax obligation.

It is essential for businesses to understand when to issue a 10-99 form. Generally, if a business pays an independent contractor more than $600 in a single tax year, they are required to file a 10-99 form with the IRS and provide a copy to the contractor. Failure to do so can result in penalties for the business. Contractors, on the other hand, should be aware that even if they do not receive a 10-99 form, they are still responsible for reporting their income and paying the appropriate taxes.

In summary, the 10-99 form is a critical document for both businesses and independent contractors. It ensures that miscellaneous income is properly reported to the IRS, allowing contractors to accurately calculate their tax liability and enabling the IRS to collect the necessary taxes. Understanding the purpose and requirements of the 10-99 form is essential for maintaining compliance with tax laws and avoiding potential penalties.

Withdrawing Employee Pension Funds: Rules, Options, and Considerations Explained

You may want to see also

Explore related products

![]()

Employee Classification: Criteria for classifying workers as employees or independent contractors

The classification of workers as employees or independent contractors is a critical aspect of human resource management and legal compliance. In the United States, the Internal Revenue Service (IRS) provides guidelines to help businesses determine the appropriate classification of their workers. The IRS uses a 20-factor test to evaluate the relationship between the worker and the employer, focusing on the degree of control the employer has over the worker's activities.

One key criterion is the level of behavioral control the employer exercises over the worker. This includes factors such as the employer's ability to direct the worker's tasks, set schedules, and determine the order in which tasks are performed. If the employer has significant control over these aspects of the worker's job, it is more likely that the worker will be classified as an employee.

Another important criterion is the degree of financial control the employer has over the worker. This includes factors such as the employer's responsibility for providing tools and equipment, reimbursing expenses, and setting payment terms. If the employer has a high degree of financial control, it is more likely that the worker will be classified as an employee.

The nature of the work relationship is also a critical factor. If the relationship is ongoing and the worker performs tasks that are integral to the employer's business, it is more likely that the worker will be classified as an employee. In contrast, if the relationship is temporary or project-based, and the worker performs tasks that are not integral to the employer's business, it is more likely that the worker will be classified as an independent contractor.

Misclassification of workers can have significant legal and financial consequences for employers. If an employer misclassifies a worker as an independent contractor, they may be liable for back taxes, penalties, and interest. Additionally, misclassification can lead to legal disputes and damage to the employer's reputation.

To avoid misclassification, employers should carefully evaluate the relationship between themselves and their workers, considering the factors outlined by the IRS. Employers should also consult with legal and tax professionals to ensure that they are complying with all applicable laws and regulations. By taking these steps, employers can minimize the risk of misclassification and ensure that they are treating their workers fairly and legally.

Addressing Poor Documentation: How to Write Up an Employee Effectively

You may want to see also

Explore related products

![]()

Tax Implications: How issuing a 10-99 affects tax reporting and liabilities for both parties

Issuing a 10-99 to a standard employee has significant tax implications for both the employer and the employee. The 10-99 form, officially known as the Form 10-99-MISC, is used to report miscellaneous income to the Internal Revenue Service (IRS). When an employer issues a 10-99, it indicates that the employee has received income that is not subject to payroll taxes, such as social security and Medicare. This can include payments for services rendered as an independent contractor, freelance work, or other non-employee compensation.

For the employer, issuing a 10-99 can affect their tax reporting and liabilities in several ways. First, it relieves the employer of the responsibility to withhold payroll taxes from the employee's income. This can be beneficial for the employer, as it reduces the administrative burden of managing payroll taxes. However, it also means that the employer must ensure that the employee is properly classified as an independent contractor and not an employee, as misclassification can lead to penalties and back taxes.

For the employee, receiving a 10-99 can have both positive and negative tax implications. On the positive side, the employee may be able to deduct business expenses related to their work, which can reduce their taxable income. Additionally, the employee may be able to take advantage of tax credits and deductions available to self-employed individuals. However, the employee is also responsible for paying self-employment taxes, which can be a significant financial burden. Furthermore, the employee may face challenges in obtaining financing or insurance, as lenders and insurers often require proof of regular employment.

In conclusion, issuing a 10-99 to a standard employee can have complex tax implications for both parties. Employers must carefully consider the classification of their workers and ensure that they are complying with IRS regulations. Employees must be aware of their tax responsibilities and take steps to manage their finances effectively. By understanding the tax implications of a 10-99, both employers and employees can make informed decisions about their financial situations.

Withdrawing Employee Shares from PF: Rules, Process, and Eligibility Explained

You may want to see also

Explore related products

![]()

Legal Requirements: Overview of legal obligations when hiring and reporting independent contractors

When hiring independent contractors, it's crucial to understand the legal obligations that come with reporting their income to the IRS. One common question is whether you can issue a 1099 form to a standard employee. The answer is no; 1099 forms are specifically for independent contractors, freelancers, and other non-employees.

The IRS has strict guidelines on who qualifies as an independent contractor. Generally, if you have control over how and when the work is done, the worker is considered an employee and should receive a W-2 form. If the worker has more autonomy and you only have control over the final product or result, they may be classified as an independent contractor.

Misclassifying an employee as an independent contractor can lead to serious legal consequences, including penalties and back taxes. It's essential to carefully evaluate the working relationship and consult with a tax professional if you're unsure about the classification.

In addition to correctly classifying workers, you must also report their income accurately. For independent contractors, this means issuing a 1099 form by January 31st of the year following the tax year in which the income was earned. The form must include the contractor's name, address, social security number or employer identification number, and the total amount of income earned.

Failure to issue a 1099 form or misreporting income can result in penalties and fines. It's important to keep accurate records and consult with a tax professional to ensure compliance with all legal requirements when hiring and reporting independent contractors.

Using Employee Class as Key in HashMap: Best Practices and Pitfalls

You may want to see also

Explore related products

![]()

Common Mistakes: Frequent errors to avoid when completing and submitting 10-99 forms

One common mistake when completing 10-99 forms is failing to accurately classify the worker as an independent contractor. Misclassification can lead to legal and financial repercussions for both the employer and the worker. To avoid this error, employers should carefully review the criteria set by the IRS for determining independent contractor status, which includes factors such as the level of control over the work, the worker's investment in the business, and the permanence of the relationship.

Another frequent error is neglecting to report all payments made to the independent contractor, including non-cash payments and reimbursements. Employers must ensure that they provide a complete and accurate record of all payments on the 10-99 form to avoid penalties and ensure the worker's proper tax reporting.

Additionally, employers often fail to obtain the correct taxpayer identification number (TIN) from the independent contractor. This can result in backup withholding and additional paperwork. To prevent this, employers should request the worker's TIN using Form W-9 and verify the information with the IRS before issuing the 10-99 form.

Lastly, some employers mistakenly issue 10-99 forms to workers who should be classified as employees. This can lead to issues with payroll taxes and workers' compensation. Employers should carefully consider the nature of the work relationship and consult with a tax professional if they are unsure about the classification of a worker.

Maximizing Deductions: Writing Off Unreimbursed Employee Travel Expenses

You may want to see also

Frequently asked questions

To "10-99" a standard employee refers to issuing them a Form 1099 instead of a W-2 at the end of the year. This typically indicates that the employee is considered an independent contractor rather than a traditional employee.

Receiving a 1099 instead of a W-2 means that the individual is responsible for paying their own self-employment taxes, including Social Security and Medicare. They may also need to make estimated tax payments throughout the year and file their taxes differently.

Employees classified as 1099 contractors are generally not eligible for employer-provided benefits such as health insurance, retirement plans, or paid time off. They also lack certain legal protections afforded to traditional employees, such as those under the Fair Labor Standards Act (FLSA).

The classification of an employee as a 1099 contractor or a W-2 employee is based on several factors, including the level of control the employer has over the employee's work, the employee's economic dependence on the employer, and the nature of the work being performed. The IRS has specific guidelines to help determine the appropriate classification.