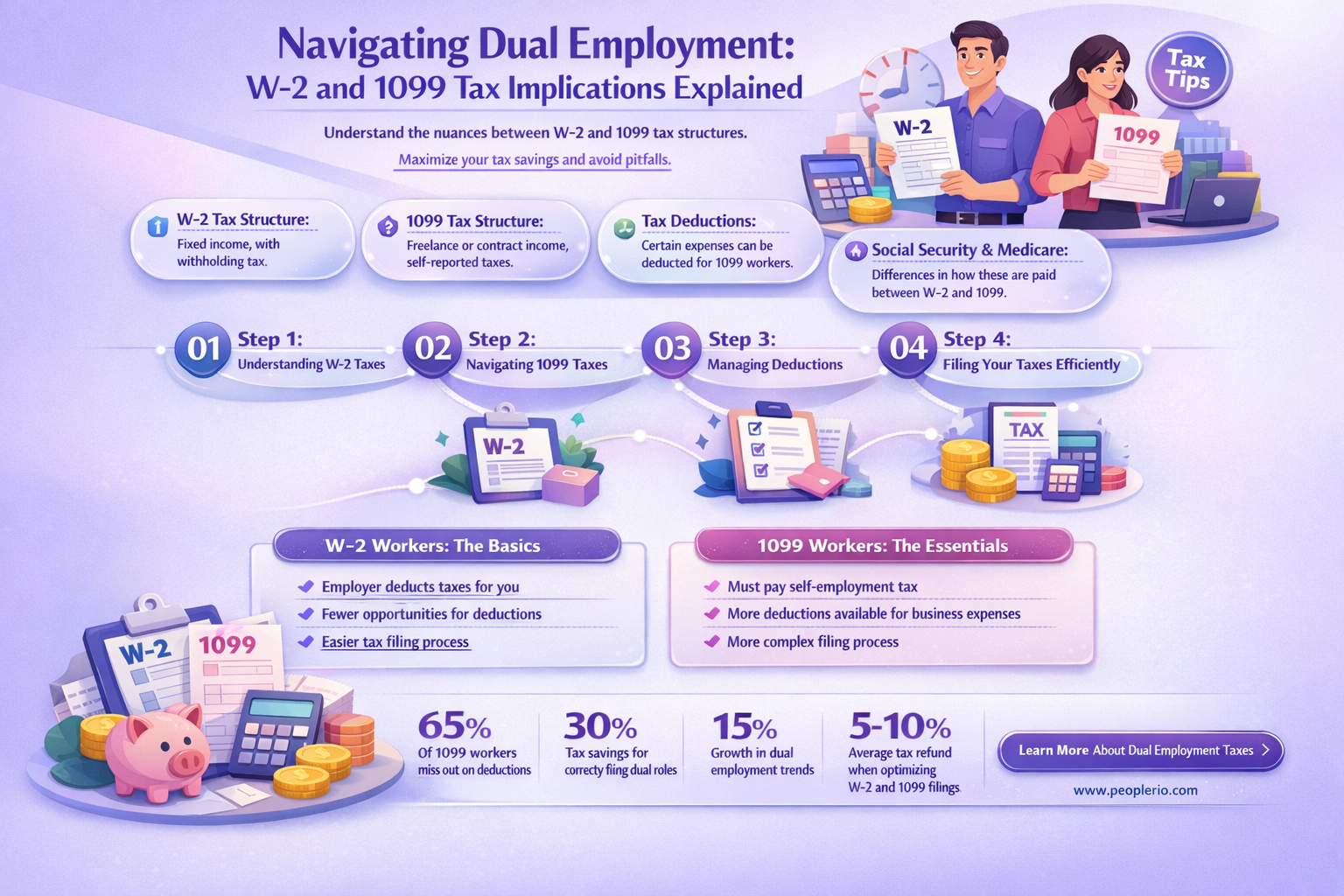

The question of whether an employee can receive both a 1099 and a W-2 form is a common one in the realm of tax and employment law. Generally, an employee is issued a W-2 form by their employer, which reports their wages and the amount of taxes withheld from their paycheck. On the other hand, a 1099 form is typically given to independent contractors or freelancers to report their earnings. However, there are situations where an employee might receive both forms, such as if they have a side gig or freelance work in addition to their regular employment. It's important to understand the implications of receiving both forms, as it can affect how one's taxes are calculated and reported to the IRS.

Explore related products

What You'll Learn

- Understanding 1099 and W-2 Forms: Explanation of the differences and purposes of 1099 and W-2 tax forms

- Employee Classification: Criteria for classifying workers as employees or independent contractors affecting tax form issuance

- Tax Withholding: How tax withholding differs for W-2 employees compared to 1099 independent contractors

- Reporting Requirements: Employer obligations for reporting employee income and taxes to the IRS using 1099 and W-2 forms

- Filing Deadlines: Important deadlines for employers to file 1099 and W-2 forms with the IRS and state tax authorities

![]()

Understanding 1099 and W-2 Forms: Explanation of the differences and purposes of 1099 and W-2 tax forms

The 1099 and W-2 forms are both used for reporting income to the Internal Revenue Service (IRS), but they serve different purposes and are issued under different circumstances. The W-2 form is provided by an employer to an employee, detailing the employee's wages, salary, and tax withholdings for the year. It is a crucial document for employees to file their individual tax returns. On the other hand, the 1099 form is typically issued by a payer to an independent contractor or freelancer, reporting the amount of money paid to them for services rendered. This form is essential for independent contractors to calculate their tax liabilities and file their returns.

One key difference between the two forms is the nature of the income reported. The W-2 form reports employment income, which is subject to payroll taxes, including Social Security and Medicare. The 1099 form, however, reports non-employee compensation, which is not subject to these payroll taxes. Instead, independent contractors are responsible for paying their own self-employment taxes.

Another important distinction is the filing requirements. Employers must file W-2 forms with the IRS and provide copies to their employees by the end of January each year. Independent contractors, on the other hand, must file their own tax returns using the information provided on the 1099 forms they receive from their clients.

In summary, the W-2 form is used for reporting employee wages and tax withholdings, while the 1099 form is used for reporting non-employee compensation. Understanding the differences between these two forms is crucial for both employers and independent contractors to ensure accurate tax reporting and compliance with IRS regulations.

Navigating Taxes: Can You Issue a 1099 to a Household Employee?

You may want to see also

Explore related products

$9.49 $18.99

![]()

Employee Classification: Criteria for classifying workers as employees or independent contractors affecting tax form issuance

The classification of workers as employees or independent contractors is a critical aspect of tax form issuance, as it determines which forms are required and who is responsible for issuing them. Generally, employees receive a Form W-2, which reports their wages and tax withholdings, while independent contractors receive a Form 1099-MISC, which reports non-employee compensation.

To classify a worker, the IRS considers several factors, including the level of control the employer has over the worker's activities, the worker's economic dependence on the employer, and the degree to which the worker's services are integrated into the employer's business. If an employer has significant control over a worker's schedule, tasks, and methods of work, that worker is likely to be classified as an employee. Conversely, if a worker has more autonomy and independence in their work, they may be classified as an independent contractor.

Misclassification of workers can have serious consequences for both employers and workers. Employers may face penalties and back taxes if they misclassify employees as independent contractors, while workers may miss out on important benefits and protections if they are misclassified as employees. Therefore, it is essential for employers to carefully consider the criteria for classification and to consult with a tax professional if they are unsure.

In some cases, a worker may be considered an "employee" for some purposes but an "independent contractor" for others. For example, a worker may be considered an employee for federal tax purposes but an independent contractor for state tax purposes. This can create confusion and complexity for both employers and workers, highlighting the importance of understanding the specific criteria for classification in different contexts.

Ultimately, the key to proper classification is to focus on the substance of the relationship between the employer and the worker, rather than on labels or formalities. By carefully analyzing the factors that influence classification, employers can ensure that they are issuing the correct tax forms and complying with their legal obligations.

Can Navy Spouses Deliver at Walter Reed? Birth Options Explained

You may want to see also

Explore related products

![]()

Tax Withholding: How tax withholding differs for W-2 employees compared to 1099 independent contractors

Tax withholding is a critical aspect of employment that differs significantly between W-2 employees and 1099 independent contractors. For W-2 employees, tax withholding is typically handled by their employer, who deducts federal, state, and local taxes from each paycheck. This process is relatively straightforward, as the employer is responsible for calculating the correct amount of tax to withhold based on the employee's earnings and tax filing status.

In contrast, 1099 independent contractors are responsible for their own tax withholding. This means that they must set aside a portion of their earnings to cover their tax liability, which can be a more complex and challenging task. Independent contractors must estimate their tax liability based on their income and expenses, and then make quarterly estimated tax payments to the IRS and any applicable state and local tax authorities.

One key difference between W-2 employees and 1099 independent contractors is the amount of tax that is withheld. For W-2 employees, the employer is required to withhold a specific percentage of their earnings for federal income tax, as well as any applicable state and local taxes. This percentage is based on the employee's tax filing status and the amount of their earnings. For 1099 independent contractors, the amount of tax that is withheld is typically lower, as they are only required to make estimated tax payments based on their net income after expenses.

Another important difference is the timing of tax payments. For W-2 employees, tax withholding is typically done on a bi-weekly or monthly basis, with the employer remitting the withheld taxes to the IRS and any applicable state and local tax authorities. For 1099 independent contractors, estimated tax payments are typically made on a quarterly basis, with the contractor remitting the payments directly to the IRS and any applicable state and local tax authorities.

In summary, tax withholding is a critical aspect of employment that differs significantly between W-2 employees and 1099 independent contractors. While W-2 employees rely on their employer to handle tax withholding, 1099 independent contractors are responsible for their own tax withholding, which can be a more complex and challenging task. Understanding these differences is essential for both employers and independent contractors to ensure compliance with tax laws and regulations.

Balancing Kroger Employment and Instacart: Is It Possible to Do Both?

You may want to see also

Explore related products

![]()

Reporting Requirements: Employer obligations for reporting employee income and taxes to the IRS using 1099 and W-2 forms

Employers have specific obligations when it comes to reporting employee income and taxes to the IRS. This includes using the correct forms, such as 1099 and W-2, to report different types of income and tax withholdings. The 1099 form is typically used for independent contractors and freelancers, while the W-2 form is used for traditional employees. Employers must ensure that they are using the correct form for each type of worker and that they are reporting all income and taxes accurately.

One of the key reporting requirements for employers is to provide employees with a copy of their W-2 form by the end of January each year. This form includes information about the employee's wages, tips, and other compensation, as well as the amount of federal, state, and local taxes withheld from their paycheck. Employers must also file a copy of the W-2 form with the IRS and the appropriate state and local tax authorities.

For independent contractors and freelancers, employers must provide a 1099 form by the end of January if the contractor earned $600 or more during the tax year. The 1099 form reports the amount of non-employee compensation paid to the contractor, as well as any federal, state, and local taxes withheld. Contractors are responsible for paying their own taxes, so the 1099 form is essential for them to prepare their tax returns.

Employers must also be aware of the penalties for failing to report employee income and taxes accurately. These penalties can include fines and interest, as well as potential criminal charges in severe cases. To avoid these penalties, employers should ensure that they are following all reporting requirements and deadlines, and that they are using the correct forms for each type of worker.

In addition to reporting income and taxes, employers may also need to report other information to the IRS, such as employee benefits and stock options. Employers should consult with a tax professional to ensure that they are meeting all of their reporting obligations and to avoid any potential penalties.

Overall, employers have a responsibility to report employee income and taxes accurately and on time using the correct forms. This includes providing employees and contractors with the necessary information to prepare their tax returns and filing the appropriate forms with the IRS and state and local tax authorities. By following these reporting requirements, employers can avoid penalties and ensure that they are in compliance with tax laws.

Understanding 1099 Forms for Hourly Employees: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Filing Deadlines: Important deadlines for employers to file 1099 and W-2 forms with the IRS and state tax authorities

Employers must adhere to strict filing deadlines when submitting 1099 and W-2 forms to the IRS and state tax authorities. These deadlines are crucial to avoid penalties and ensure compliance with tax regulations. For W-2 forms, employers must generally file by the end of January following the tax year. This deadline applies to both federal and state filings, although some states may have slightly different due dates. Employers should check with their state tax authorities to confirm the specific deadline for their location.

For 1099 forms, the filing deadline is typically by the end of February following the tax year. This deadline also applies to both federal and state filings, but similar to W-2 forms, state deadlines may vary. Employers should ensure they are aware of the deadlines for each state where they have employees or contractors.

In addition to the deadlines for filing with the IRS and state tax authorities, employers must also provide copies of the 1099 and W-2 forms to the employees and contractors by the end of January. This allows individuals to review their tax information and prepare their own tax returns. Employers should take care to ensure that the information on these forms is accurate and complete to avoid any issues or delays in tax processing.

Failure to meet these filing deadlines can result in significant penalties for employers. The IRS and state tax authorities may impose fines for late filings, and these penalties can increase over time if the forms are not submitted. Employers should make every effort to meet these deadlines to avoid unnecessary financial burdens and potential legal issues.

To ensure timely filing, employers should maintain accurate records of employee and contractor information throughout the year. This includes keeping track of wages, salaries, and other payments made to individuals. Employers should also stay informed about any changes to tax laws or filing requirements that may affect their obligations. By staying organized and up-to-date, employers can minimize the risk of missing important filing deadlines and maintain compliance with tax regulations.

Maximizing Deductions: Writing Off Unreimbursed Employee Travel Expenses

You may want to see also

Frequently asked questions

Yes, an employee can receive both a W-2 and a 1099 form. The W-2 form reports the employee's wages and tax withholdings from their primary job, while the 1099 form reports miscellaneous income, such as freelance work or side gigs, that is not subject to tax withholding.

A W-2 employee is a regular employee who receives a salary or hourly wage and has taxes withheld from their paycheck. A 1099 contractor, on the other hand, is an independent contractor or freelancer who is paid for their services and is responsible for paying their own taxes.

If you are a regular employee who receives a salary or hourly wage and has taxes withheld from your paycheck, you should receive a W-2 form. If you are an independent contractor or freelancer who is paid for your services and is responsible for paying your own taxes, you should receive a 1099 form.

Receiving both a W-2 and a 1099 form can have tax implications. The income reported on the W-2 form is subject to tax withholding, while the income reported on the 1099 form is not. This means that you may need to pay additional taxes on the income reported on the 1099 form when you file your tax return.