Certainly! Here's a paragraph introducing the topic:

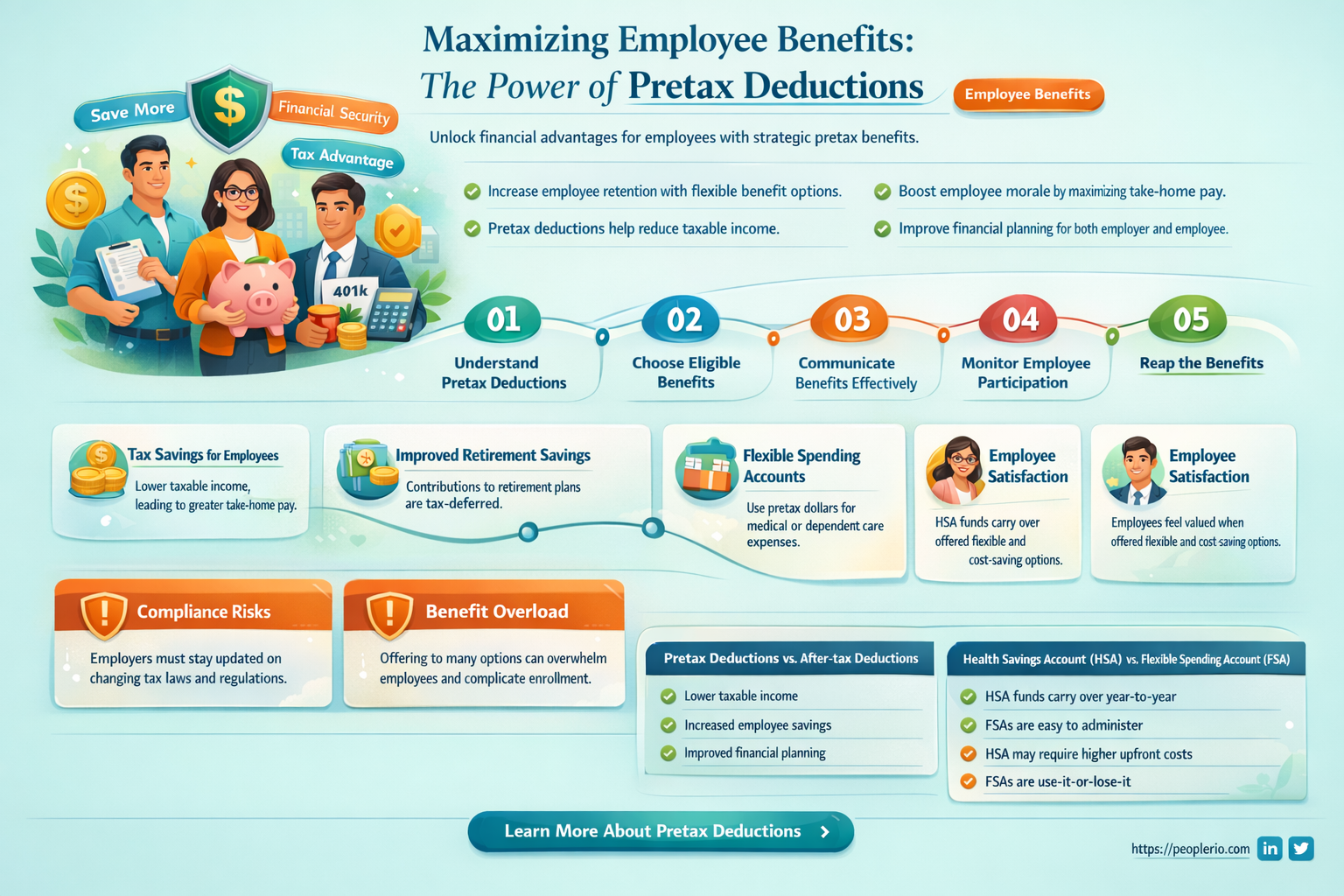

When it comes to managing payroll and employee benefits, one common question that arises is whether it's possible to add a pretax deduction for a single employee. Pretax deductions are amounts withheld from an employee's gross pay before taxes are calculated, which can include contributions to retirement plans, health insurance premiums, or other benefits. The ability to make such deductions can have significant implications for both the employer and the employee, affecting take-home pay, tax liabilities, and overall financial planning. In this discussion, we'll explore the considerations and potential steps involved in implementing a pretax deduction for one employee.

Let me know if you'd like me to elaborate on any specific aspect of this topic!

| Characteristics | Values |

|---|---|

| Employee Count | 1 |

| Deduction Type | Pretax |

| Purpose | To add |

Explore related products

What You'll Learn

- Eligibility Criteria: Define the conditions an employee must meet to qualify for a pretax deduction

- Types of Pretax Deductions: List common pretax deductions like 401(k), health insurance, and flexible spending accounts

- Contribution Limits: Specify the maximum amount an employee can contribute to each type of pretax deduction

- Enrollment Process: Outline the steps an employee needs to take to enroll in a pretax deduction plan

- Tax Implications: Explain how pretax deductions affect an employee's taxable income and potential tax savings

![]()

Eligibility Criteria: Define the conditions an employee must meet to qualify for a pretax deduction

To qualify for a pretax deduction, an employee must meet specific eligibility criteria set by the employer and governing tax laws. These criteria typically include being a full-time employee, as part-time or contract workers may not be eligible. The employee must also meet any age requirements, such as being at least 18 years old, and may need to have a certain level of income or job status to qualify.

In addition to these general requirements, the employee must also meet the specific criteria for the type of pretax deduction being offered. For example, if the deduction is for a 401(k) contribution, the employee must be enrolled in the plan and meet any vesting requirements. If the deduction is for a health savings account (HSA), the employee must be enrolled in a high-deductible health plan (HDHP) and not be enrolled in Medicare.

Employers may also set their own eligibility criteria, such as requiring employees to have been with the company for a certain period of time or to have a certain level of job performance. These criteria must be clearly communicated to employees and must be applied consistently to avoid discrimination or favoritism.

It is important for employers to carefully consider the eligibility criteria for pretax deductions, as these can have a significant impact on employee morale and retention. Offering pretax deductions can be a valuable benefit for employees, but it is essential to ensure that the criteria are fair and reasonable. Employers should also be aware of any legal requirements or restrictions on pretax deductions, such as those imposed by the IRS or other governing bodies.

In conclusion, the eligibility criteria for pretax deductions are an important aspect of employee benefits and must be carefully considered by employers. By setting clear and fair criteria, employers can offer valuable benefits to their employees while also ensuring compliance with legal requirements.

Can Wegmans Employees Accept Tips? Understanding the Policy and Etiquette

You may want to see also

Explore related products

![]()

Types of Pretax Deductions: List common pretax deductions like 401(k), health insurance, and flexible spending accounts

Pretax deductions are a crucial aspect of employee compensation, allowing individuals to reduce their taxable income and potentially lower their tax liability. Common pretax deductions include contributions to 401(k) retirement plans, health insurance premiums, and flexible spending accounts (FSAs). These deductions are typically made before federal, state, and local taxes are withheld from an employee's paycheck.

A 401(k) plan is a tax-advantaged retirement savings plan sponsored by an employer that allows workers to save and invest a piece of their paycheck before taxes are taken out. Contributions to a 401(k) plan can significantly reduce an employee's taxable income, and the earnings on the investments grow tax-deferred until withdrawal, typically in retirement.

Health insurance premiums are another common pretax deduction. When an employer provides health insurance as part of an employee's compensation package, the premiums paid by the employee are often deducted from their paycheck on a pretax basis. This can result in substantial tax savings, especially for employees in higher tax brackets.

Flexible spending accounts (FSAs) are also popular pretax deductions. An FSA is a tax-advantaged account that allows employees to set aside money on a pretax basis to pay for qualified medical expenses, such as deductibles, copayments, and prescription drugs. The money in an FSA can be used throughout the year to cover eligible expenses, and any unused funds at the end of the year may be forfeited.

In addition to these common pretax deductions, there are other types of deductions that may be available to employees, depending on their employer's policies and the applicable tax laws. For example, some employers may offer pretax deductions for dependent care expenses, transportation costs, or even student loan repayments.

Understanding the types of pretax deductions available can help employees make informed decisions about their compensation packages and potentially reduce their tax liability. It's essential for employees to review their employer's policies and consult with a tax professional to determine which deductions they may be eligible for and how to maximize their tax savings.

Can Navy Spouses Deliver at Walter Reed? Birth Options Explained

You may want to see also

Explore related products

![]()

Contribution Limits: Specify the maximum amount an employee can contribute to each type of pretax deduction

When setting up pretax deductions for employees, it's crucial to understand and specify the contribution limits for each type of deduction. This ensures compliance with tax regulations and helps employees make informed decisions about their contributions. For example, the IRS sets annual contribution limits for 401(k) plans, which employers must communicate to their employees.

To specify contribution limits, employers need to consider the type of pretax deduction and the applicable tax laws. For instance, the contribution limit for a 401(k) plan in 2023 is $22,500 for employees under 50 years old and $30,000 for those 50 and older. Employers must also be aware of any additional limits, such as the overall limit on contributions to all retirement plans, which is $66,000 in 2023.

In addition to retirement plans, employers may offer other pretax deductions, such as flexible spending accounts (FSAs) or health savings accounts (HSAs). Each of these deductions has its own contribution limits, which employers must clearly communicate to employees. For example, the maximum contribution to an FSA in 2023 is $5,000, while the maximum contribution to an HSA is $3,600 for individuals and $7,200 for families.

Employers should also consider any state-specific contribution limits, as some states have their own tax laws and regulations that may affect pretax deductions. For instance, California has its own retirement savings program, CalSavers, which has different contribution limits than federal programs.

To ensure compliance and help employees make informed decisions, employers should provide clear and concise information about contribution limits for each type of pretax deduction. This can be done through employee handbooks, benefit summaries, or online resources. Employers should also regularly review and update their contribution limits to reflect changes in tax laws and regulations.

Maximizing Deductions: Writing Off Unreimbursed Employee Travel Expenses

You may want to see also

![]()

Enrollment Process: Outline the steps an employee needs to take to enroll in a pretax deduction plan

To enroll in a pretax deduction plan, an employee must follow a series of steps that ensure they are properly registered and their contributions are correctly deducted. The first step is to obtain the necessary enrollment forms from their employer's human resources department. These forms typically include information about the available pretax deduction plans, such as a 401(k) or a health savings account (HSA).

Once the employee has the enrollment forms, they should carefully review the options available and select the plan that best suits their needs. This may involve considering factors such as the type of deductions allowed, the contribution limits, and any employer matching contributions. After selecting a plan, the employee must complete the enrollment forms, providing all required information such as their name, social security number, and the amount they wish to contribute.

The completed enrollment forms should be submitted to the employer's human resources department, which will then process the enrollment and notify the employee once it has been approved. The employee should also receive information about how their pretax deductions will be taken from their paycheck and how they can monitor their contributions.

It is important for employees to understand that pretax deductions can have a significant impact on their take-home pay and their tax liability. By enrolling in a pretax deduction plan, employees can reduce their taxable income, which can lead to lower federal and state taxes. However, it is also important to note that pretax deductions are subject to certain rules and limitations, and employees should consult with a tax professional or their employer's human resources department if they have any questions or concerns.

In summary, the enrollment process for a pretax deduction plan involves obtaining the necessary forms, selecting a plan, completing the forms, and submitting them to the employer's human resources department. Employees should carefully consider their options and understand the potential impact of pretax deductions on their finances before enrolling in a plan.

Withdrawing Employee Shares from PF: Rules, Process, and Eligibility Explained

You may want to see also

![]()

Tax Implications: Explain how pretax deductions affect an employee's taxable income and potential tax savings

Pretax deductions play a crucial role in reducing an employee's taxable income, which in turn can lead to significant tax savings. When an employer offers pretax deductions, such as for health insurance premiums or retirement contributions, these amounts are subtracted from the employee's gross income before taxes are calculated. This reduces the overall taxable income, resulting in a lower tax liability.

For example, if an employee earns $50,000 per year and contributes $5,000 to a pretax retirement plan, their taxable income would be reduced to $45,000. This could potentially lower their tax bracket and reduce their overall tax burden. The exact impact on tax savings would depend on the employee's tax rate and other factors, but generally, pretax deductions are a valuable tool for minimizing taxes owed.

It's important to note that not all pretax deductions are created equal. Some deductions, like those for health insurance, are only available to employees who meet certain criteria, such as being enrolled in a qualified plan. Additionally, there may be limits on the amount that can be deducted pretax for certain expenses. Employers should carefully review the rules and regulations surrounding pretax deductions to ensure compliance and maximize the benefits for their employees.

From an employer's perspective, offering pretax deductions can be a cost-effective way to provide additional benefits to employees without increasing the company's tax liability. By allowing employees to save money on taxes, employers can potentially attract and retain top talent while also promoting financial wellness among their workforce.

In conclusion, pretax deductions can have a significant impact on an employee's taxable income and potential tax savings. Employers who offer these deductions can provide valuable benefits to their employees while also potentially reducing their own tax burden. However, it's crucial to understand the rules and limitations surrounding pretax deductions to ensure compliance and maximize the benefits for all parties involved.

Navigating 1099 Forms for Full-Time Employees: A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, you can add a pretax deduction for one employee. Pretax deductions are amounts subtracted from an employee's gross pay before taxes are calculated. Common pretax deductions include contributions to retirement plans, health insurance premiums, and flexible spending accounts. To add a pretax deduction, you'll need to set up the deduction in your payroll system and ensure that the employee has elected to participate in the pretax deduction program.

There are several types of pretax deductions available, including:

- 401(k) contributions

- Health insurance premiums

- Dental insurance premiums

- Vision insurance premiums

- Flexible spending accounts (FSAs)

- Health savings accounts (HSAs)

- Commuter benefits

- Dependent care flexible spending accounts

- Adoption assistance

- Employee stock purchase plans

Pretax deductions reduce an employee's gross pay before taxes are calculated, which in turn reduces the amount of taxes withheld from their paycheck. This can result in a higher take-home pay for the employee. For example, if an employee contributes $100 per paycheck to a 401(k) plan, their gross pay will be reduced by $100, and the taxes withheld from their paycheck will be calculated based on the lower gross pay. This can lead to an increase in the employee's take-home pay, as they will have less tax withheld.