Employee turnover is a critical metric for businesses to track, as it can significantly impact operational efficiency, morale, and financial health. QuickBooks, a popular accounting software, provides tools to help businesses manage their finances, including tracking employee-related expenses. While QuickBooks does not have a built-in feature specifically for calculating employee turnover, you can use the software to gather necessary data and perform the calculation manually. This involves determining the number of employees who have left the company within a specific period and comparing that to the average number of employees during the same period. By understanding how to utilize QuickBooks for this purpose, businesses can better monitor their workforce dynamics and make informed decisions to improve retention and overall performance.

Explore related products

What You'll Learn

- Setting up QuickBooks for Turnover Tracking: Configure QuickBooks to monitor employee turnover by creating relevant accounts and reports

- Recording Employee Data: Enter employee details, including hire and termination dates, to facilitate accurate turnover calculations

- Customizing Reports: Modify QuickBooks reports to include turnover metrics, such as average tenure and turnover rates by department

- Analyzing Turnover Costs: Use QuickBooks to estimate the financial impact of employee turnover, including recruitment and training expenses

- Turnover Trends and Insights: Regularly review QuickBooks data to identify turnover patterns and areas for improvement in employee retention strategies

![]()

Setting up QuickBooks for Turnover Tracking: Configure QuickBooks to monitor employee turnover by creating relevant accounts and reports

To set up QuickBooks for turnover tracking, you'll need to create specific accounts and reports that monitor employee turnover. Begin by opening your QuickBooks software and navigating to the 'Company' menu. From there, select 'Chart of Accounts' to create new accounts related to employee turnover. These might include accounts for tracking terminated employees, new hires, and the costs associated with recruitment and training.

Once you've established these accounts, you can create custom reports to monitor turnover rates. Go to the 'Reports' menu and choose 'Custom Report.' Select the accounts you created for turnover tracking and customize the report to show the data you need, such as the number of employees hired and terminated within a specific timeframe, and the associated costs.

To further streamline the process, consider setting up automated workflows within QuickBooks. This can help ensure that data is consistently tracked and reported without manual intervention. For example, you can automate the process of recording new hires and terminations, or set up alerts to notify you when turnover rates exceed certain thresholds.

When configuring QuickBooks for turnover tracking, it's important to ensure that your data is accurate and up-to-date. Regularly review your reports and reconcile any discrepancies. Additionally, consider integrating QuickBooks with other HR systems or software to streamline data collection and reduce the risk of errors.

By setting up QuickBooks to monitor employee turnover, you can gain valuable insights into your company's hiring and retention practices. This information can help you identify areas for improvement and make data-driven decisions to reduce turnover and improve employee satisfaction.

Retroactive Employee Dating: Navigating the Legal and Ethical Landscape

You may want to see also

Explore related products

![]()

Recording Employee Data: Enter employee details, including hire and termination dates, to facilitate accurate turnover calculations

To calculate employee turnover in QuickBooks, you must first ensure that you have accurately recorded all relevant employee data. This includes entering each employee's hire date and termination date, which are critical for determining the turnover rate. In QuickBooks, you can enter this information through the Employee Center. Click on the 'Employees' tab, then select 'Employee Center'. From here, you can add new employees or edit existing ones. Make sure to fill in the 'Hire Date' and 'Termination Date' fields for each employee.

Once you have entered the necessary data, QuickBooks can automatically calculate the employee turnover rate for you. To access this feature, navigate to the 'Reports' tab and select 'Employees & Payroll'. Then, choose the 'Employee Turnover' report. QuickBooks will generate a report that shows the turnover rate based on the employee data you have entered.

It's important to note that the accuracy of the turnover calculation depends on the accuracy of the data you have entered. Therefore, it's crucial to double-check all employee details to ensure that they are correct. Additionally, QuickBooks allows you to customize the report to fit your specific needs. For example, you can filter the report by date range or by individual employees.

In conclusion, recording employee data accurately is essential for calculating employee turnover in QuickBooks. By following the steps outlined above, you can ensure that your turnover calculations are precise and reliable. This information can be invaluable for making informed business decisions and improving your company's overall performance.

Navigating Workplace Safety: Requesting COVID-19 Vaccine Proof from Employees

You may want to see also

Explore related products

![]()

Customizing Reports: Modify QuickBooks reports to include turnover metrics, such as average tenure and turnover rates by department

To customize QuickBooks reports for turnover metrics, you'll need to delve into the software's reporting features. QuickBooks allows you to modify existing reports or create custom ones to suit your specific needs. Start by navigating to the 'Reports' tab and selecting 'Customize Report'. Choose the report you want to modify, such as the 'Employee Contact List' or 'Payroll Summary', and click 'Customize'.

In the customization window, you can add columns for turnover metrics like average tenure and turnover rates by department. To do this, click on the 'Columns' tab and select the desired metrics from the list. You can also create custom calculations using the 'Calculations' tab. For instance, you could calculate the average tenure by subtracting the hire date from the current date and averaging the result across employees in each department.

Once you've added the necessary columns and calculations, click 'OK' to save your changes. You can then run the report to see the turnover metrics for each department. QuickBooks also allows you to export the report to Excel for further analysis or to create custom visualizations.

When customizing reports, it's essential to ensure that the data is accurate and up-to-date. Regularly review and update employee information, including hire dates and department assignments, to maintain the integrity of your turnover metrics. Additionally, consider setting up automated reminders to run these reports periodically, so you can track turnover trends over time and make informed decisions about your workforce.

The Unseen Side of Employment: Navigating Without Benefits

You may want to see also

Explore related products

![Quickbooks Online For Beginners [10 In 1]: The Complete Visual Guide to Mastering QuickBooks Fast. Automate Your Finances, Stay Tax-Ready, and Take Control of Your Business in 30 Days or Less.](https://m.media-amazon.com/images/I/617U3Y-cutL._AC_UL320_.jpg)

![]()

Analyzing Turnover Costs: Use QuickBooks to estimate the financial impact of employee turnover, including recruitment and training expenses

To analyze turnover costs using QuickBooks, you'll need to categorize and track various expenses associated with employee turnover. Begin by setting up accounts specifically for recruitment and training costs. This could include job posting fees, recruiter commissions, training materials, and instructor fees. Once these accounts are established, you can start recording transactions as they occur.

Next, identify the direct costs of turnover, such as the loss of productivity during the recruitment period and any severance packages paid to departing employees. These costs can be more challenging to quantify but are essential for a comprehensive analysis. Consider using QuickBooks' budgeting tools to estimate these costs based on historical data or industry benchmarks.

QuickBooks also allows you to track indirect costs, such as the impact of turnover on team morale and the time spent by existing employees on additional tasks. While these costs are harder to measure, they can be significant and should not be overlooked. Use QuickBooks' reporting features to generate regular turnover cost reports, which can help you identify trends and areas for improvement.

To take your analysis to the next level, consider integrating QuickBooks with other HR tools and systems. This can provide a more holistic view of your turnover costs and help you identify the root causes of employee turnover. By leveraging QuickBooks' powerful financial analysis capabilities, you can gain valuable insights into the financial impact of employee turnover and make data-driven decisions to reduce these costs.

Addressing Poor Documentation: How to Write Up an Employee Effectively

You may want to see also

Explore related products

![]()

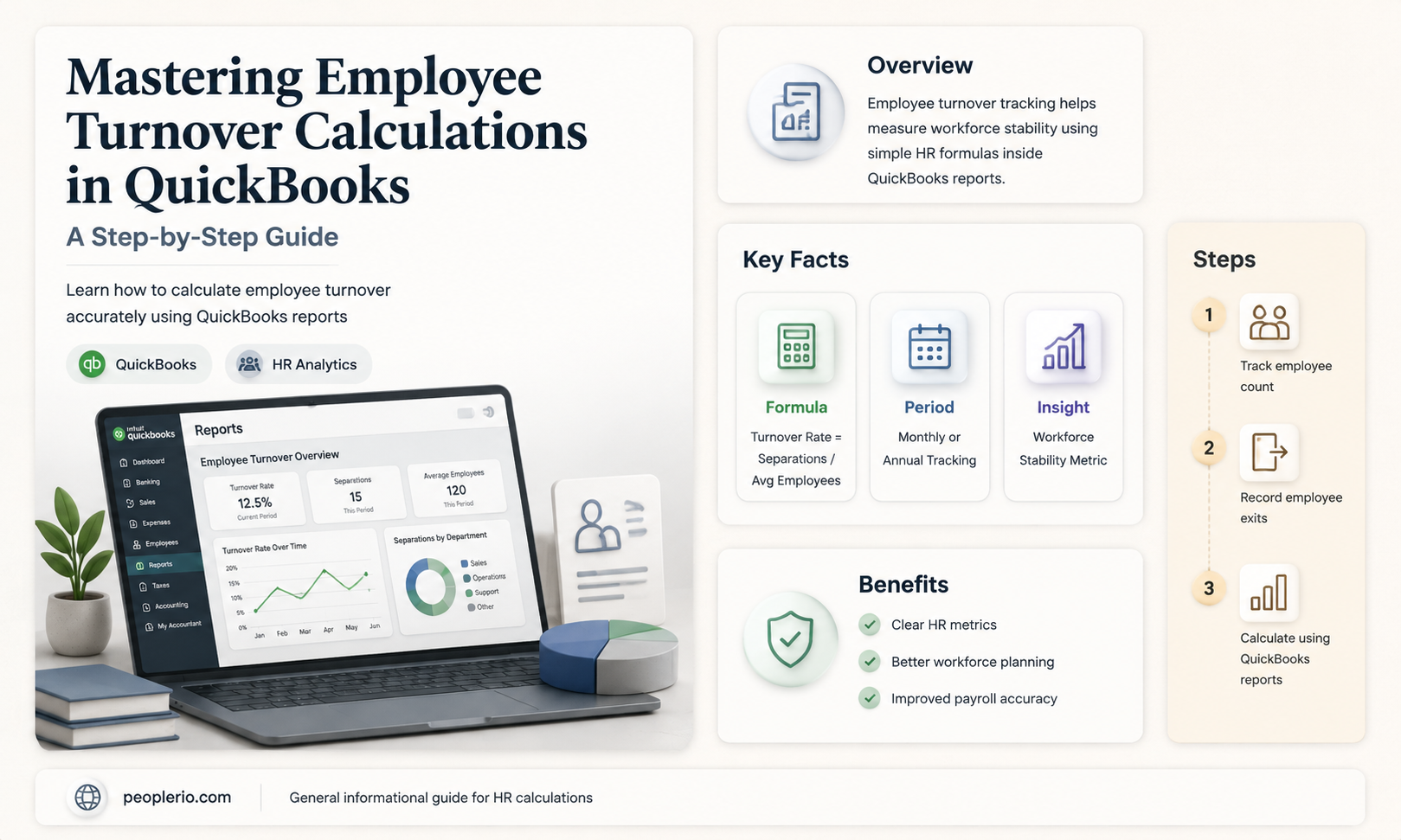

Turnover Trends and Insights: Regularly review QuickBooks data to identify turnover patterns and areas for improvement in employee retention strategies

Analyzing turnover trends within QuickBooks data can reveal critical insights into employee retention and potential areas for improvement. By regularly reviewing this data, businesses can identify patterns that may indicate underlying issues contributing to employee turnover. For instance, a noticeable increase in turnover during specific periods could suggest seasonal fluctuations or project-based hiring practices that lead to temporary employment. Conversely, a consistent turnover rate might point to more systemic issues, such as inadequate compensation, poor management, or lack of career advancement opportunities.

To effectively identify these patterns, businesses should segment their QuickBooks data by various criteria, including department, job role, tenure, and reason for departure. This segmentation allows for a more granular analysis, enabling companies to pinpoint specific areas where turnover is higher than average. For example, if the data shows that turnover is particularly high among employees in the customer service department, it may be worth investigating whether this is due to the nature of the work, the management style, or other factors unique to that department.

Once turnover patterns have been identified, businesses can begin to develop targeted strategies to address the root causes. This might involve implementing more robust training programs, offering competitive compensation packages, or creating clear career paths to encourage employee retention. Regularly reviewing and acting upon QuickBooks data can help businesses stay proactive in their retention efforts, ultimately leading to a more stable and productive workforce.

In addition to identifying turnover patterns, QuickBooks data can also be used to track the effectiveness of retention strategies over time. By monitoring changes in turnover rates following the implementation of new initiatives, businesses can determine which strategies are most effective and make data-driven decisions about where to allocate their resources. This continuous cycle of analysis and improvement is essential for maintaining a healthy and engaged workforce.

Overall, leveraging QuickBooks data to analyze turnover trends and inform retention strategies can provide businesses with a competitive edge in today's labor market. By understanding the factors that contribute to employee turnover and taking proactive steps to address them, companies can create a more positive work environment that fosters long-term employee satisfaction and loyalty.

Exploring Career Shifts: Why Employees Change Positions

You may want to see also

Frequently asked questions

Yes, QuickBooks allows you to track employee turnover through its payroll and HR features. You can generate reports that provide insights into employee retention and turnover rates.

To set up employee turnover tracking in QuickBooks, you need to enable the payroll feature and configure it to track employee start and end dates. This will allow you to generate turnover reports.

QuickBooks offers several report templates that can help you analyze employee turnover, including the 'Employee Turnover Rate' report and the 'Employee Retention Rate' report. These reports provide visual representations of turnover trends over time.

Yes, QuickBooks can integrate with various HR systems and software, allowing you to consolidate employee data and gain a more comprehensive view of turnover rates and trends.