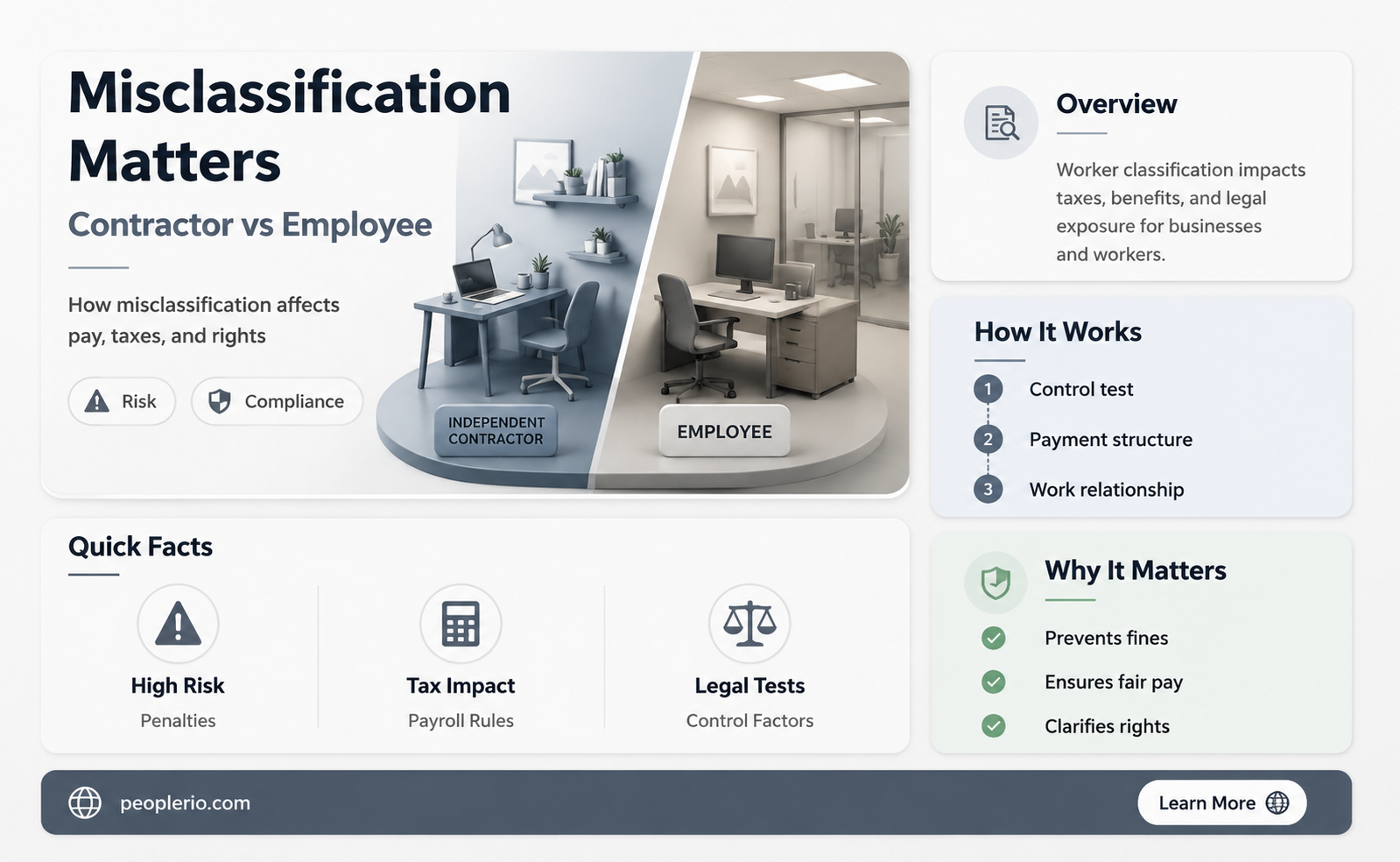

The question of whether an independent contractor can be classified as an employee is a complex and nuanced one, often arising in the context of labor law and employment regulations. Independent contractors are typically individuals or entities that provide services to a business on a project-by-project basis, without the traditional employer-employee relationship. They are generally responsible for their own taxes, insurance, and work-related expenses. However, there are situations where the line between independent contractor and employee can become blurred, leading to potential legal and financial implications for both parties involved.

Explore related products

What You'll Learn

- Legal Definitions: Understand the distinct legal definitions of independent contractors and employees

- Control and Direction: Analyze the level of control and direction exerted over the worker

- Economic Realities: Consider the economic realities of the relationship, including payment and benefits

- Work Integration: Evaluate how integrated the worker is into the company's operations

- Misclassification Risks: Be aware of the risks and consequences of misclassifying an independent contractor as an employee

![]()

Legal Definitions: Understand the distinct legal definitions of independent contractors and employees

Understanding the legal distinctions between independent contractors and employees is crucial for businesses and individuals alike. The classification of a worker as an independent contractor or an employee has significant implications for tax purposes, benefits, and legal liabilities. An independent contractor is typically defined as a person who performs work for another under a contract, has control over the manner and means of performing the work, and is not subject to the same level of control as an employee. In contrast, an employee is generally considered someone who works for an employer under a more permanent arrangement, is subject to the employer's control and direction, and is entitled to certain benefits and protections.

One key aspect of distinguishing between independent contractors and employees is the level of control exerted by the employer. Independent contractors have more autonomy and are responsible for determining how to complete their tasks, whereas employees are expected to follow the employer's instructions and procedures. Additionally, independent contractors are usually paid on a project-by-project basis or by the hour, while employees receive a regular salary or wages.

Another important factor is the nature of the work relationship. Independent contractors often have a more temporary and flexible relationship with their clients, while employees typically have a more stable and ongoing relationship with their employer. Independent contractors may work for multiple clients simultaneously, whereas employees are generally expected to be exclusive to their employer.

Misclassifying a worker as an independent contractor when they should be considered an employee can lead to legal and financial consequences. Employers may be held liable for unpaid taxes, benefits, and other obligations if they misclassify workers. Similarly, workers who are misclassified as independent contractors may miss out on important benefits and protections, such as health insurance, retirement plans, and workers' compensation.

To avoid misclassification, businesses should carefully evaluate the nature of their relationships with workers and consider factors such as the level of control, the permanence of the relationship, and the method of payment. Consulting with legal and tax professionals can also help ensure that workers are properly classified and that businesses comply with relevant laws and regulations.

In conclusion, understanding the legal definitions of independent contractors and employees is essential for maintaining compliance with the law and ensuring fair treatment of workers. By carefully considering the factors that distinguish between these two classifications, businesses can avoid costly mistakes and foster positive relationships with their workers.

Navigating Health Conversations with Employees: A Guide for Managers

You may want to see also

Explore related products

![]()

Control and Direction: Analyze the level of control and direction exerted over the worker

The level of control and direction exerted over a worker is a critical factor in determining whether they can be classified as an employee or an independent contractor. In the context of employment law, control and direction refer to the degree to which an employer dictates the manner, method, and timing of work performed by a worker. If an employer has significant control and direction over a worker's activities, it is more likely that the worker will be considered an employee. Conversely, if a worker has a high degree of autonomy and independence in performing their work, they are more likely to be classified as an independent contractor.

To analyze the level of control and direction, it is essential to consider various factors, including the employer's right to assign tasks, the worker's discretion in choosing their work schedule, and the extent to which the employer provides training and supervision. For example, if an employer requires a worker to follow a specific schedule, provides detailed instructions on how to perform tasks, and regularly monitors and evaluates the worker's performance, this suggests a high level of control and direction, which may indicate an employment relationship.

On the other hand, if a worker has the freedom to choose their own schedule, determine the methods and techniques used to complete tasks, and is responsible for their own training and development, this suggests a lower level of control and direction, which may indicate an independent contractor relationship. It is important to note that the level of control and direction is not the only factor in determining employee status, and other factors such as the nature of the work, the worker's economic dependence on the employer, and the degree of integration into the employer's business operations must also be considered.

In practice, the analysis of control and direction can be complex, and it is often necessary to examine the specific facts and circumstances of each case to make a determination. Employers and workers should carefully consider the level of control and direction in their working relationship to ensure compliance with employment laws and regulations. By understanding the nuances of control and direction, employers can make informed decisions about how to structure their relationships with workers, and workers can better understand their rights and obligations in the workplace.

Legal Risks at Work: Can You Be Sued as an Employee?

You may want to see also

Explore related products

![]()

Economic Realities: Consider the economic realities of the relationship, including payment and benefits

The economic realities of the relationship between a business and an independent contractor are multifaceted and must be carefully considered. One key aspect is the method of payment. Independent contractors are typically paid on a project-by-project basis or by the hour, rather than receiving a regular salary. This payment structure can provide flexibility for both parties, but it also means that contractors may not receive the same benefits as employees, such as health insurance, retirement plans, or paid time off.

Another important economic reality is the potential for cost savings for businesses that hire independent contractors. By not having to provide benefits or pay for office space and equipment, businesses can reduce their overhead costs. However, this cost savings must be weighed against the potential risks and liabilities associated with misclassifying an employee as an independent contractor.

Independent contractors are also responsible for paying their own taxes, which can be a significant burden. This is in contrast to employees, whose taxes are typically withheld by their employer. Contractors must be diligent in setting aside funds for taxes and ensuring that they are properly filed.

The economic realities of the relationship between a business and an independent contractor also include the potential for unequal bargaining power. Businesses may have more leverage in negotiations, which can lead to contractors accepting lower pay or less favorable terms. This power imbalance can be mitigated by contractors banding together to form unions or associations that can negotiate on their behalf.

In conclusion, the economic realities of the relationship between a business and an independent contractor are complex and must be carefully considered by both parties. Understanding the payment structures, cost savings, tax responsibilities, and potential power imbalances can help ensure that the relationship is fair and mutually beneficial.

Is It Appropriate to Inquire About an Employee's Driving Record?

You may want to see also

Explore related products

![]()

Work Integration: Evaluate how integrated the worker is into the company's operations

To evaluate how integrated a worker is into a company's operations, it's essential to consider several key factors. First, assess the level of control the company has over the worker's tasks and schedule. If the company dictates the worker's hours, tasks, and methods of work, this indicates a higher level of integration. Second, examine the worker's involvement in company meetings and decision-making processes. Regular participation in team meetings and contributing to strategic decisions suggests that the worker is more integrated into the company's operations.

Another important aspect to consider is the worker's access to company resources and tools. If the worker has access to the company's internal systems, software, and equipment, this is a sign of integration. Additionally, evaluate the worker's interactions with other employees. Frequent collaboration and communication with other team members indicate that the worker is well-integrated into the company's culture and operations.

It's also crucial to look at the worker's role in the company's workflow. If the worker is responsible for critical tasks that are essential to the company's operations, this suggests a higher level of integration. Furthermore, consider the worker's level of commitment and loyalty to the company. If the worker demonstrates a strong commitment to the company's goals and values, this is another indicator of integration.

In conclusion, evaluating a worker's integration into a company's operations involves assessing control, involvement in decision-making, access to resources, interactions with other employees, role in the workflow, and level of commitment. By considering these factors, companies can determine how well-integrated their workers are and take steps to improve integration if necessary.

Exploring the Ethics of Bartering with Paid Employees

You may want to see also

Explore related products

![]()

Misclassification Risks: Be aware of the risks and consequences of misclassifying an independent contractor as an employee

Misclassifying an independent contractor as an employee can lead to significant legal and financial repercussions for businesses. One of the primary risks is the potential for lawsuits and penalties from government agencies, such as the Internal Revenue Service (IRS) in the United States. These penalties can include back taxes, fines, and interest, which can quickly add up to substantial amounts. Additionally, misclassification can result in the business being held liable for unpaid wages, benefits, and overtime, which can further exacerbate the financial impact.

Another consequence of misclassification is the potential damage to the business's reputation. If the misclassification is discovered, it can lead to negative publicity and a loss of trust among customers, partners, and potential employees. This can have long-term effects on the business's ability to attract and retain talent, as well as its overall success in the market.

To mitigate these risks, it is essential for businesses to understand the key differences between independent contractors and employees. Independent contractors are typically hired on a project-by-project basis and have more control over their work, including the ability to set their own schedules and choose their own projects. Employees, on the other hand, are typically hired for a specific role within the company and are subject to the company's policies and procedures.

Businesses should also be aware of the various factors that can contribute to misclassification, such as the level of control exerted over the worker, the nature of the work being performed, and the worker's level of independence. By carefully considering these factors and ensuring that workers are classified correctly, businesses can avoid the significant risks and consequences associated with misclassification.

In conclusion, misclassifying an independent contractor as an employee can have serious legal and financial implications for businesses. By understanding the differences between independent contractors and employees, and by carefully considering the factors that contribute to misclassification, businesses can minimize these risks and ensure that they are in compliance with the law.

Navigating Financial Wellness: A Guide for Employers and Employees

You may want to see also

Frequently asked questions

No, you cannot call an independent contractor an employee. An independent contractor is a self-employed individual who provides services to clients under a contract, while an employee is someone who is hired by an employer and works for them in exchange for wages or a salary.

The key differences between an independent contractor and an employee include the level of control the employer has over the worker, the worker's ability to set their own schedule and work independently, and the way in which the worker is paid. Independent contractors have more autonomy and are typically paid by the project or hour, while employees are subject to the employer's direction and are usually paid a regular wage or salary.

Misclassifying an independent contractor as an employee can have serious legal implications, including back taxes, penalties, and fines. Employers may also be liable for unpaid wages, benefits, and overtime if the misclassification is found to be intentional.

To determine whether a worker is an independent contractor or an employee, you need to consider several factors, including the level of control you have over the worker, the worker's ability to set their own schedule and work independently, and the way in which the worker is paid. If the worker has a high degree of autonomy and is paid by the project or hour, they are likely an independent contractor. If the worker is subject to your direction and is paid a regular wage or salary, they are likely an employee.

Some common industries that use independent contractors include construction, consulting, freelance writing and design, IT and technology, and healthcare. Independent contractors are often used in these industries to provide specialized services or to supplement a company's existing workforce.