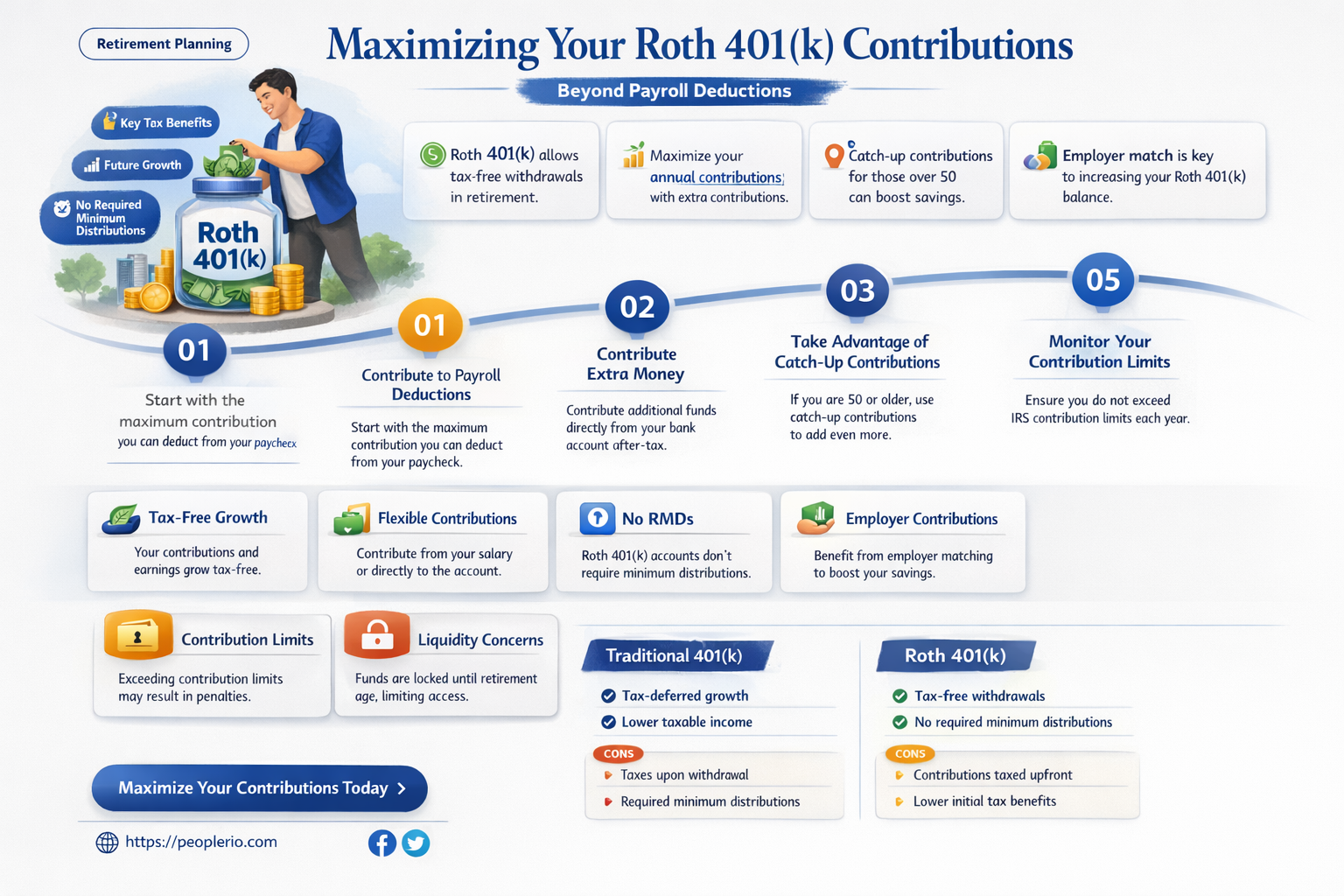

A Roth 401(k) is a retirement savings plan sponsored by an employer that allows workers to contribute a piece of their paycheck before taxes are taken out. The money grows tax-free and can be withdrawn tax-free in retirement. However, many people wonder if they can contribute to a Roth 401(k) outside of their regular payroll deductions. The answer is yes, but there are some limitations and considerations to keep in mind.

| Characteristics | Values |

|---|---|

| Contribution Type | Roth 401(k) |

| Contribution Source | Outside of payroll |

| Eligibility | Depends on plan rules |

| Contribution Limits | Subject to annual limits |

| Tax Treatment | Contributions are after-tax |

| Investment Options | Typically mutual funds or ETFs |

| Withdrawal Rules | Qualified distributions are tax-free |

| Required Minimum Distributions (RMDs) | Generally required after age 72 |

| Impact on Social Security Benefits | May increase taxable income |

| Employer Matching | Not applicable for Roth contributions |

Explore related products

What You'll Learn

- Eligibility: Understand the requirements to contribute to a Roth 401(k) outside of regular payroll deductions

- Contribution Limits: Learn about the maximum amounts you can contribute annually, including any catch-up contributions allowed

- Tax Implications: Discover how contributing to a Roth 401(k) affects your taxable income and potential tax liabilities

- Investment Options: Explore the types of investments available within a Roth 401(k) and how to choose wisely

- Withdrawal Rules: Familiarize yourself with the regulations governing withdrawals from a Roth 401(k), including any penalties or restrictions

![]()

Eligibility: Understand the requirements to contribute to a Roth 401(k) outside of regular payroll deductions

To contribute to a Roth 401(k) outside of regular payroll deductions, you must first understand the eligibility requirements. The IRS has specific guidelines that dictate who can make such contributions. Generally, you must have earned income to contribute to a Roth 401(k), and your income must fall below certain thresholds. For the tax year 2023, individuals can contribute up to $6,500 if their income is below $14,500, and married couples filing jointly can contribute up to $13,000 if their combined income is below $21,800.

However, there are exceptions to these income limits. If you are over the age of 50, you can make additional "catch-up" contributions of up to $1,000, regardless of your income level. This can be a valuable tool for those who are nearing retirement and want to maximize their retirement savings.

Another important factor to consider is the type of plan you are contributing to. Not all 401(k) plans allow for Roth contributions, so you should check with your plan administrator to ensure that your plan is eligible. Additionally, some plans may have their own contribution limits or restrictions, so it's important to be aware of these before making any contributions.

Once you have determined that you are eligible to contribute to a Roth 401(k) outside of regular payroll deductions, you will need to fill out the necessary paperwork with your plan administrator. This typically involves completing a contribution election form and specifying the amount you wish to contribute. You may also need to provide proof of your income and marital status.

It's important to note that contributing to a Roth 401(k) outside of regular payroll deductions can have tax implications. Since Roth contributions are made with after-tax dollars, you will not receive a tax deduction for your contributions. However, the earnings on your contributions will grow tax-free, and you will not have to pay taxes on your withdrawals in retirement, as long as you meet certain conditions.

In conclusion, understanding the eligibility requirements for contributing to a Roth 401(k) outside of regular payroll deductions is crucial for maximizing your retirement savings. By familiarizing yourself with the income limits, plan restrictions, and necessary paperwork, you can make informed decisions about your contributions and ensure that you are taking full advantage of this valuable retirement savings tool.

Can I Put My Child on Payroll? Legal and Tax Insights

You may want to see also

Explore related products

![]()

Contribution Limits: Learn about the maximum amounts you can contribute annually, including any catch-up contributions allowed

The IRS sets annual contribution limits for Roth 401(k) accounts, which are designed to help individuals save for retirement. As of 2023, the maximum contribution limit is $19,500 for those under age 50. For individuals aged 50 and older, an additional catch-up contribution of $6,500 is allowed, bringing the total limit to $26,000. These limits are subject to change based on inflation and other economic factors, so it's essential to stay informed about any updates.

Catch-up contributions are a valuable tool for older savers who may have fallen behind in their retirement savings or who want to maximize their contributions before reaching the age of required minimum distributions (RMDs). To take advantage of catch-up contributions, you must be at least 50 years old by the end of the calendar year. It's important to note that catch-up contributions are separate from the regular contribution limit and can only be made to Roth 401(k) accounts, not traditional 401(k) accounts.

When planning your contributions, it's crucial to consider your overall financial situation, including your income, expenses, and other savings goals. Contributing the maximum amount allowed can help you build a more substantial retirement nest egg, but it's also important to ensure that you're not sacrificing other financial priorities, such as paying off high-interest debt or maintaining an emergency fund.

If you're unsure about how to navigate the contribution limits or need assistance with your retirement planning, consider consulting with a financial advisor or tax professional. They can help you develop a personalized strategy that takes into account your unique circumstances and goals. Remember, the key to successful retirement savings is to start early, contribute consistently, and make informed decisions about your financial future.

DIY Payroll for Small Businesses: Is It Right for You?

You may want to see also

Explore related products

![]()

Tax Implications: Discover how contributing to a Roth 401(k) affects your taxable income and potential tax liabilities

Contributing to a Roth 401(k) can have significant tax implications, affecting both your taxable income and potential tax liabilities. Unlike traditional 401(k) contributions, which are made pre-tax, Roth 401(k) contributions are made after-tax. This means that the amount you contribute to a Roth 401(k) is deducted from your gross income, reducing your taxable income for the year. As a result, you may be able to lower your tax bracket and reduce your overall tax liability.

One of the key benefits of contributing to a Roth 401(k) is that the earnings on your contributions grow tax-free. This means that you won't have to pay taxes on the investment gains, dividends, or interest earned within the account. Additionally, qualified distributions from a Roth 401(k) are tax-free, allowing you to withdraw your contributions and earnings without incurring any additional tax liability.

However, it's important to note that contributing to a Roth 401(k) may not be the best option for everyone. If you expect to be in a lower tax bracket in retirement, you may be better off contributing to a traditional 401(k) or IRA. Additionally, if you have high-interest debt or other financial obligations, it may be more beneficial to focus on paying those off before contributing to a Roth 401(k).

When considering whether to contribute to a Roth 401(k), it's essential to evaluate your current tax situation, your expected tax bracket in retirement, and your overall financial goals. Consulting with a financial advisor or tax professional can help you make an informed decision that aligns with your specific circumstances and objectives.

In conclusion, contributing to a Roth 401(k) can offer several tax advantages, including reducing your taxable income, allowing your earnings to grow tax-free, and providing tax-free distributions in retirement. However, it's crucial to weigh these benefits against your individual financial situation and goals to determine if a Roth 401(k) is the right choice for you.

Can Payroll Companies Legally Withhold Your W-2? What You Need to Know

You may want to see also

Explore related products

![]()

Investment Options: Explore the types of investments available within a Roth 401(k) and how to choose wisely

Within a Roth 401(k), you have a variety of investment options to choose from, each with its own risk profile and potential for growth. Understanding these options is crucial to making informed decisions about your retirement savings.

One common investment option is mutual funds, which pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other securities. Roth 401(k)s often offer a selection of mutual funds with different investment strategies, such as growth, value, or balanced funds. Another option is exchange-traded funds (ETFs), which are similar to mutual funds but trade on stock exchanges like individual stocks. ETFs can offer lower fees and more flexibility than mutual funds.

Individual stocks and bonds are also typically available within a Roth 401(k). Investing in individual securities can provide more control over your portfolio, but it also requires more research and carries higher risks. You may also have the option to invest in real estate through real estate investment trusts (REITs) or other real estate-focused funds.

When choosing investments for your Roth 401(k), consider your risk tolerance, investment goals, and time horizon. A diversified portfolio that includes a mix of asset classes can help mitigate risk and maximize returns over the long term. It's also important to regularly review and rebalance your portfolio to ensure it remains aligned with your investment strategy.

Finally, be mindful of the fees associated with each investment option, as they can have a significant impact on your returns over time. Lower-cost index funds and ETFs can be more cost-effective than actively managed funds with higher expense ratios.

How to Locate Your W2 on Paylocity: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Withdrawal Rules: Familiarize yourself with the regulations governing withdrawals from a Roth 401(k), including any penalties or restrictions

Understanding the withdrawal rules for a Roth 401(k) is crucial for maximizing the benefits of this retirement savings vehicle. Unlike traditional 401(k)s, Roth 401(k)s are funded with after-tax dollars, which allows for tax-free growth and withdrawals in retirement. However, there are specific regulations that govern when and how you can withdraw funds from a Roth 401(k) without incurring penalties.

One key rule is the five-year requirement. To avoid penalties, you must wait at least five years from the year you first contributed to the Roth 401(k) before making any withdrawals. This five-year period is calculated from the first contribution made to any Roth 401(k) account you have, not just the specific account from which you are withdrawing. Additionally, you must be at least 59½ years old at the time of the withdrawal. If you meet both of these criteria, you can withdraw your contributions and earnings tax-free and penalty-free.

There are some exceptions to the five-year rule and age requirement. For example, if you become disabled or die, your beneficiaries can withdraw funds without penalty. You can also withdraw up to $10,000 for the purchase of a first home without incurring a penalty, although this exception only applies to earnings, not contributions. Furthermore, if you use the funds for qualified education expenses, such as tuition and fees for yourself, your spouse, or your dependents, you can avoid penalties.

It's important to note that while Roth 401(k) withdrawals are generally tax-free, they can still impact your taxable income. If you withdraw funds before meeting the five-year requirement or age 59½, the earnings portion of the withdrawal will be subject to income tax and a 10% penalty. This penalty can be waived in certain circumstances, such as if you are using the funds to pay for health insurance premiums while unemployed or if you are a reservist called to active duty.

To avoid any potential issues, it's essential to keep accurate records of your contributions and withdrawals. This will help you track your five-year period and ensure that you are meeting all the necessary requirements to avoid penalties. Consulting with a financial advisor or tax professional can also provide valuable guidance on navigating the withdrawal rules and making the most of your Roth 401(k) savings.

Exploring Intuit Payroll: Can You Purchase It Online?

You may want to see also

Frequently asked questions

Yes, you can make contributions to a Roth 401(k) outside of your regular payroll deductions. This can be done through additional payments directly to the plan, often referred to as "after-tax contributions."

Yes, there are contribution limits for Roth 401(k)s. As of 2023, the maximum contribution limit is $19,500 for individuals under 50 years old, and $26,000 for those 50 and older. These limits include both payroll deductions and additional after-tax contributions.

To set up additional contributions, you'll need to check with your plan administrator or human resources department. They can provide you with the necessary forms or online options to arrange for these contributions. You may need to specify the amount and frequency of these payments, and ensure that they are processed correctly by your plan provider.