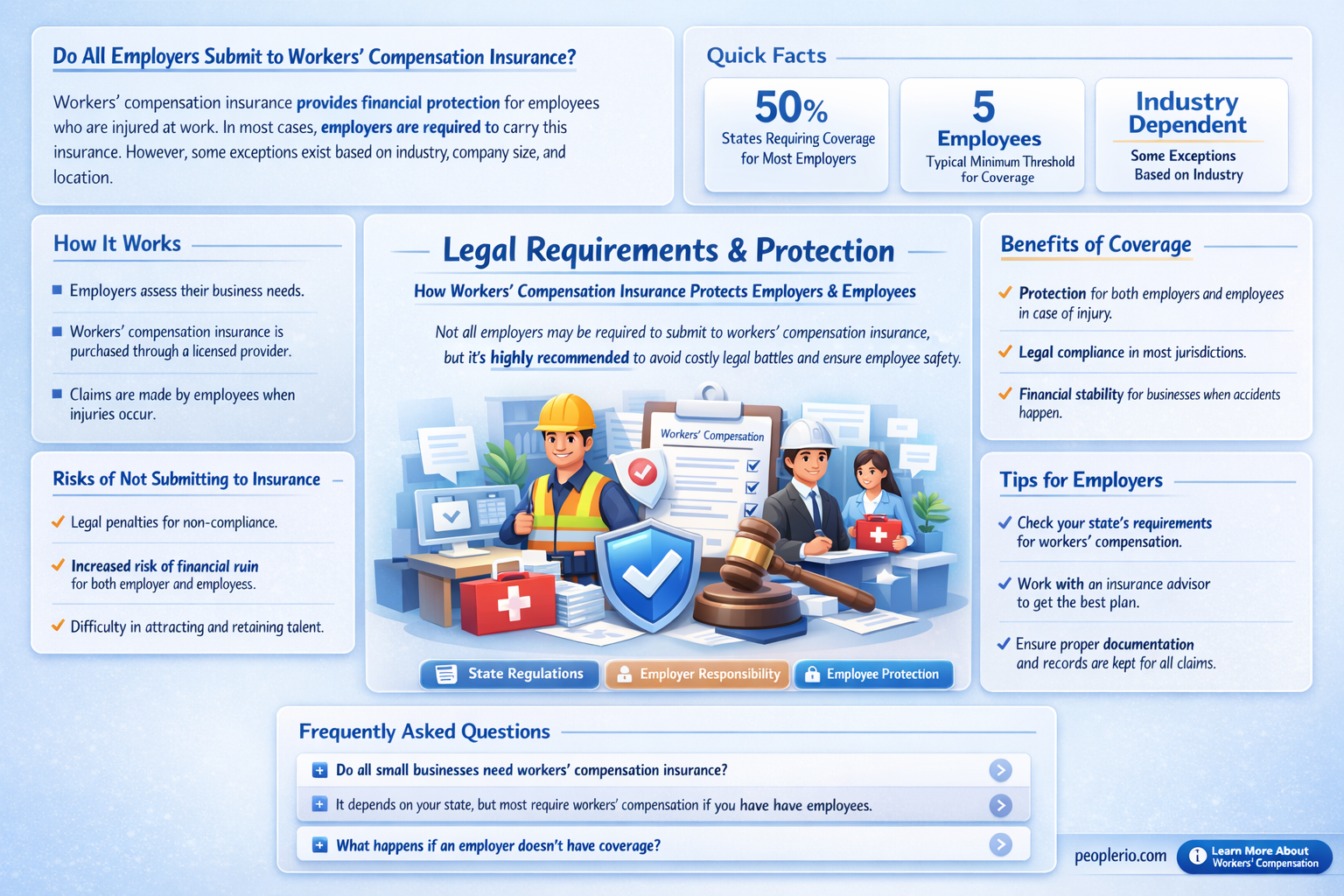

Workers' compensation insurance is a crucial aspect of employment that provides financial protection to workers who suffer job-related injuries or illnesses. While it is a common practice for many employers to carry this insurance, not all are legally required to do so. The necessity for employers to submit to workers' compensation insurance varies by jurisdiction and is typically governed by state or provincial laws. In some regions, only businesses with a certain number of employees or those in specific high-risk industries are mandated to have this coverage. Therefore, whether an employer is obligated to carry workers' compensation insurance depends on the legal framework of the area in which they operate.

Explore related products

What You'll Learn

- Legal Requirements: Most states mandate workers' compensation insurance for employers to cover employee injuries

- Coverage Details: Policies typically cover medical expenses, lost wages, and rehabilitation costs for work-related injuries

- Exemptions: Some small businesses or specific industries may be exempt from carrying workers' compensation insurance

- Premiums: Employers pay premiums based on factors like the number of employees, industry risk, and claims history

- Claim Process: Employees must report injuries promptly, and employers must file claims with the insurance provider

![]()

Legal Requirements: Most states mandate workers' compensation insurance for employers to cover employee injuries

In the United States, the legal landscape surrounding workers' compensation insurance is complex and varies significantly from state to state. While most states do mandate that employers carry this type of insurance to cover employee injuries, there are notable exceptions and nuances that employers must be aware of. For instance, some states, like Texas, allow employers to opt out of workers' compensation insurance under certain conditions, which can include demonstrating financial responsibility through other means.

The requirements for workers' compensation insurance are typically governed by state statutes, which outline the specific conditions under which employers are obligated to provide coverage. These statutes often define the types of injuries that are covered, the benefits that employees are entitled to, and the procedures for filing claims. Employers who fail to comply with these legal requirements may face significant penalties, including fines and legal action from injured employees.

One of the key aspects of workers' compensation insurance is that it is a no-fault system, meaning that employees do not need to prove that their employer was negligent in order to receive benefits. This system is designed to provide quick and efficient compensation to injured workers while also protecting employers from costly lawsuits. However, this also means that employers must be proactive in managing workplace safety and preventing injuries, as they cannot rely on the legal system to absolve them of responsibility.

Employers should also be aware of the different types of workers' compensation insurance policies available. Some policies may offer additional coverage for things like occupational illnesses or repetitive stress injuries, which may not be covered under standard policies. Additionally, employers may need to consider the impact of workers' compensation insurance on their business operations, such as the potential for increased premiums following a workplace injury.

In conclusion, while most states do require employers to carry workers' compensation insurance, the specific legal requirements and implications can vary widely. Employers must stay informed about the laws in their state and take steps to ensure that they are in compliance with all relevant regulations. This includes not only carrying the required insurance but also maintaining a safe working environment and being prepared to manage claims effectively.

Unraveling the Confusion: State Unemployment Insurance vs. Unemployment Compensation

You may want to see also

Explore related products

![]()

Coverage Details: Policies typically cover medical expenses, lost wages, and rehabilitation costs for work-related injuries

Workers' compensation insurance is a critical safety net for employees who suffer work-related injuries or illnesses. While the specifics of coverage can vary by state and policy, most workers' compensation policies typically cover several key areas: medical expenses, lost wages, and rehabilitation costs.

Medical expenses are usually the most immediate and obvious costs associated with a work-related injury. Workers' compensation policies generally cover all necessary medical treatment, including doctor visits, hospital stays, surgeries, and prescription medications. This coverage is essential for ensuring that injured workers receive the care they need without incurring significant out-of-pocket expenses.

Lost wages are another significant concern for injured workers. If an employee is unable to work due to a work-related injury, workers' compensation policies typically provide wage replacement benefits. These benefits are designed to help workers maintain their financial stability while they are recovering and unable to earn their regular income. The amount and duration of these benefits can vary depending on the policy and the state's regulations.

Rehabilitation costs are also an important aspect of workers' compensation coverage. These costs can include physical therapy, occupational therapy, and other forms of rehabilitation that are necessary to help the injured worker recover and return to their job. In some cases, workers' compensation policies may also cover the costs of retraining or education if the injured worker is unable to return to their previous job and needs to learn new skills.

It's important to note that workers' compensation policies do not typically cover every type of injury or illness. For example, injuries that occur outside of the workplace or illnesses that are not directly related to the worker's job may not be covered. Additionally, workers' compensation policies often have specific requirements and procedures that must be followed in order to qualify for benefits.

In conclusion, workers' compensation insurance is a vital form of protection for employees, providing coverage for medical expenses, lost wages, and rehabilitation costs associated with work-related injuries. Understanding the specifics of this coverage can help workers navigate the claims process and ensure they receive the benefits they are entitled to.

Securing Your Future: A Guide to Obtaining Disability Insurance

You may want to see also

Explore related products

![]()

Exemptions: Some small businesses or specific industries may be exempt from carrying workers' compensation insurance

Certain small businesses or specific industries may be exempt from carrying workers' compensation insurance, depending on the jurisdiction. These exemptions are typically based on the size of the business, the nature of the work, or the level of risk involved. For example, in some states, businesses with fewer than a certain number of employees may not be required to carry workers' compensation insurance. Similarly, certain industries, such as agriculture or domestic work, may be exempt due to their unique characteristics or lower risk profiles.

It is important for business owners to understand the specific exemptions that apply to their operations, as failing to carry the required insurance can result in significant penalties or legal liabilities. Employers should consult with their state's workers' compensation department or an insurance professional to determine if they are exempt from carrying workers' compensation insurance.

Even if a business is exempt from carrying workers' compensation insurance, it may still be beneficial to carry other types of insurance, such as general liability insurance or business interruption insurance. These policies can help protect the business from other types of risks and liabilities that may not be covered by workers' compensation insurance.

In conclusion, while some small businesses or specific industries may be exempt from carrying workers' compensation insurance, it is crucial for employers to understand the specific exemptions that apply to their operations and to consider carrying other types of insurance to protect their business from potential risks and liabilities.

Understanding Workers' Compensation Insurance Funding: A State Fund Overview

You may want to see also

Explore related products

![]()

Premiums: Employers pay premiums based on factors like the number of employees, industry risk, and claims history

Employers' premiums for workers' compensation insurance are calculated based on several key factors. The number of employees is a primary determinant, as more workers generally mean a higher risk of workplace injuries and thus higher insurance costs. Industry risk is another significant factor; employers in industries with inherently higher risks, such as construction or manufacturing, will typically face higher premiums compared to those in lower-risk sectors like office administration.

Claims history also plays a crucial role in premium calculations. Employers with a history of frequent or severe claims will likely see higher premiums, as insurers view them as higher-risk clients. Conversely, employers with a clean claims history may benefit from lower premiums as a reward for maintaining a safer work environment.

In addition to these factors, insurers may also consider the employer's safety measures and risk management practices. Employers who invest in comprehensive safety training, equipment, and protocols may be able to demonstrate a lower risk profile, potentially leading to reduced premiums.

It's important for employers to understand these factors and how they impact their insurance costs. By actively managing risks and maintaining a safe work environment, employers can potentially reduce their premiums and improve their overall financial stability.

Mandatory Workers' Compensation Insurance for New Jersey Employers: What You Need to Know

You may want to see also

Explore related products

![]()

Claim Process: Employees must report injuries promptly, and employers must file claims with the insurance provider

Employees who suffer work-related injuries or illnesses are required to report them to their employer immediately. This prompt reporting is crucial as it sets the wheels in motion for the workers' compensation claim process. Employers, in turn, must file claims with their insurance provider within a specified timeframe, which varies by jurisdiction. Failure to report injuries promptly or file claims in a timely manner can result in delays in receiving benefits or even denial of the claim.

The claim process typically involves several steps. First, the employee must notify their employer of the injury or illness, either verbally or in writing. The employer then has a certain number of days to report the claim to their insurance provider. This report usually includes details about the employee's injury, their job duties, and the incident that led to the injury. The insurance provider will then investigate the claim and determine whether it is compensable.

During the investigation, the insurance provider may request additional information from the employee, such as medical records or a statement about the incident. The employee may also be required to undergo a medical examination by a doctor chosen by the insurance provider. Once the investigation is complete, the insurance provider will make a decision on the claim and notify the employee and employer of their findings.

If the claim is approved, the employee will begin receiving workers' compensation benefits, which may include medical expenses, lost wages, and rehabilitation costs. If the claim is denied, the employee may have the option to appeal the decision. This appeal process can be complex and may require the assistance of a workers' compensation attorney.

Employers must also be aware of their responsibilities under workers' compensation laws. In addition to reporting claims promptly, employers must maintain accurate records of all work-related injuries and illnesses. They must also provide employees with information about their rights under workers' compensation laws and post notices in the workplace about the claim process. Employers who fail to comply with these requirements may face penalties or fines.

In conclusion, the workers' compensation claim process is a critical component of ensuring that injured employees receive the benefits they are entitled to. By reporting injuries promptly and filing claims in a timely manner, employers can help ensure that their employees receive the necessary medical care and financial support to recover from work-related injuries or illnesses.

Indiana Churches and Workers' Compensation Insurance: What You Need to Know

You may want to see also

Frequently asked questions

In most jurisdictions, employers are required to carry workers' compensation insurance if they have a certain number of employees. This number varies by state or country, but it's typically mandatory for businesses with more than a few employees.

If an employer fails to carry the required workers' compensation insurance, they may face legal penalties, fines, or even criminal charges. Additionally, uninsured employers may be held personally liable for any work-related injuries or illnesses that occur.

Workers' compensation insurance provides financial protection to employees who are injured or become ill as a result of their work. It covers medical expenses, lost wages, and may also provide benefits for permanent disabilities or death.

Yes, there are some exceptions. For example, certain types of businesses, such as sole proprietorships or partnerships, may not be required to carry workers' compensation insurance. Additionally, some states or countries may have specific exemptions for certain industries or types of workers.

Employers usually pay for workers' compensation insurance through premiums, which are calculated based on factors such as the number of employees, the type of work they do, and the employer's claims history. Premiums can be paid annually, quarterly, or monthly, depending on the insurance provider and the employer's preference.