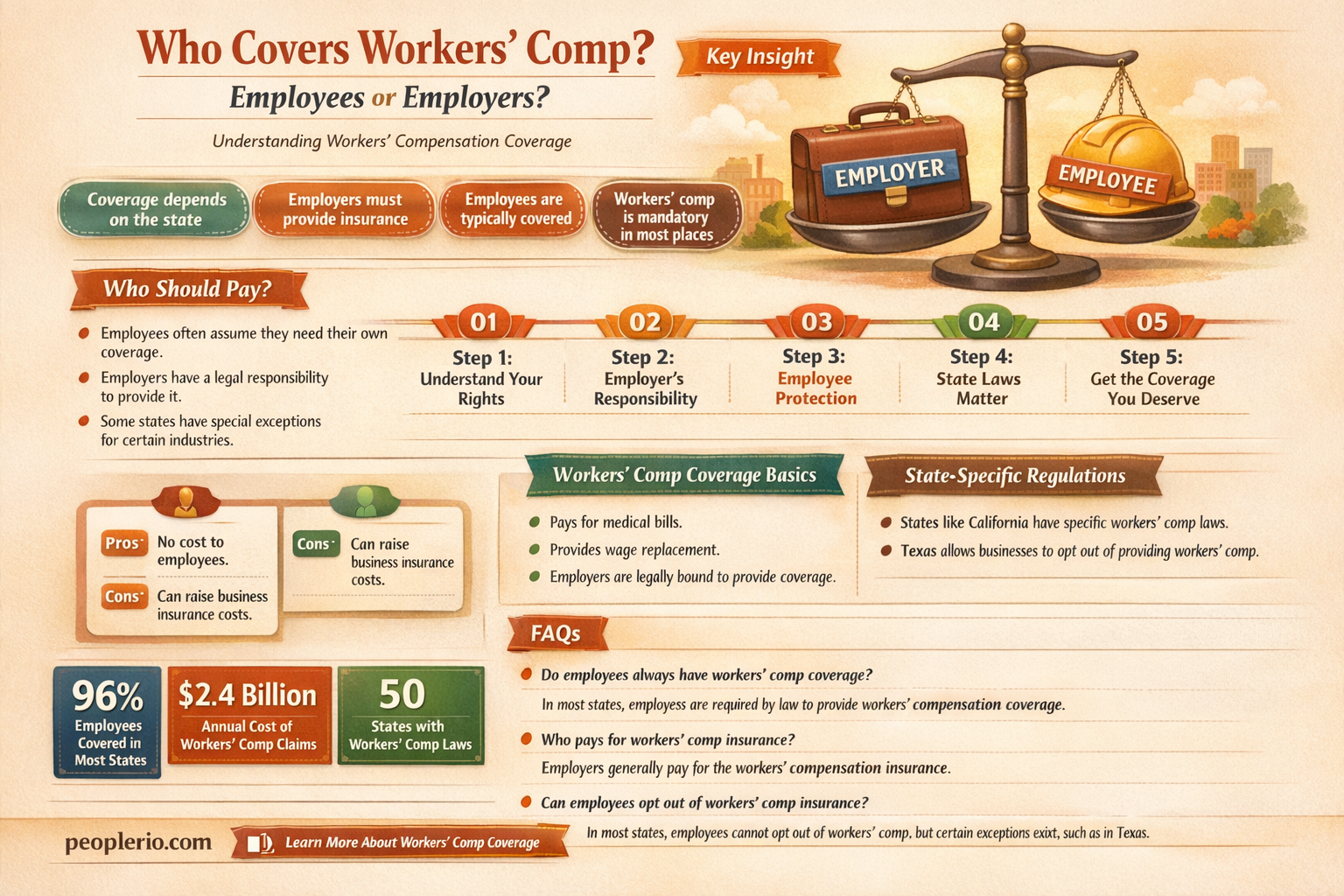

Workers' compensation is a crucial aspect of employment law that provides financial protection to employees who suffer work-related injuries or illnesses. In most jurisdictions, employers are legally obligated to carry workers' compensation insurance to cover the costs associated with such incidents. This includes medical expenses, lost wages, and rehabilitation costs. Employees generally do not have to pay for workers' compensation out of their own pockets, as the system is designed to shift the financial burden from the injured worker to the employer and, ultimately, to the insurance provider. However, there may be specific circumstances or requirements that could affect an employee's eligibility or the extent of coverage, making it essential for workers to understand their rights and responsibilities under workers' compensation laws.

| Characteristics | Values |

|---|---|

| Responsibility | Employer's responsibility |

| Coverage | Covers work-related injuries and illnesses |

| Employee Contribution | Generally not required to contribute |

| Cost | Paid by employer through insurance premiums |

| Legal Requirement | Mandated by law in most jurisdictions |

| Benefits | Provides medical care and wage replacement |

| Administration | Managed by employer or insurance carrier |

| Employee Action | Employees may need to report incidents and provide documentation |

Explore related products

What You'll Learn

![]()

Who Pays for Workers' Compensation?

In the realm of workers' compensation, a common question arises: Who bears the financial burden? Contrary to what some employees might believe, they are not typically responsible for paying for workers' compensation insurance. This responsibility usually falls on the shoulders of employers.

Employers are generally required by law to carry workers' compensation insurance to cover their employees in case of work-related injuries or illnesses. This insurance serves as a safety net, providing financial support to workers who are unable to perform their duties due to job-related health issues. The premiums for this insurance are paid by the employer, and in some cases, a portion may be deducted from the employees' wages, but this is not a direct payment by the employees for the insurance itself.

The cost of workers' compensation insurance can vary significantly depending on several factors, including the type of industry, the number of employees, and the claims history of the employer. High-risk industries, such as construction or manufacturing, may have higher premiums due to the increased likelihood of workplace accidents. Employers with a history of frequent claims may also face higher insurance costs.

It's important for employees to understand that while they may not be directly paying for workers' compensation insurance, they do have a role to play in maintaining a safe work environment. By following safety protocols and reporting potential hazards, employees can help reduce the risk of workplace accidents, which in turn can lead to lower insurance costs for their employer.

In some cases, employees may need to contribute to the cost of workers' compensation through wage deductions, but this is typically a small percentage of their overall compensation. This contribution is often seen as a minor trade-off for the security and protection provided by the insurance in case of a work-related injury or illness.

In conclusion, while employees may not be the primary payers of workers' compensation insurance, they do have a vested interest in maintaining a safe and healthy work environment. By understanding their role and the factors that influence insurance costs, employees can contribute to a more secure and stable workplace for themselves and their colleagues.

Navigating Workers' Compensation Payments to the Texas Government

You may want to see also

Explore related products

![]()

Employee Contributions

Employees often contribute to workers' compensation insurance through payroll deductions. These contributions are typically a percentage of the employee's wages and are mandated by state laws. The specific contribution rates can vary depending on the state, the employer's industry, and the employer's claims history.

One unique aspect of employee contributions is that they can sometimes choose to make additional voluntary contributions. These voluntary contributions might be used to cover the costs of specific medical treatments or to supplement the standard workers' compensation benefits. However, such voluntary contributions are not common and are usually only available through certain employers or unions.

It's important for employees to understand that their contributions to workers' compensation insurance do not affect their eligibility for benefits. Workers' compensation is a no-fault system, meaning that employees are entitled to benefits regardless of who was at fault for the injury or illness. The contributions are simply a way to fund the system and ensure that it remains available to all employees who need it.

Employees should also be aware that their contributions to workers' compensation insurance are not tax-deductible. This is because the contributions are considered a form of insurance premium, and insurance premiums are generally not tax-deductible. However, the benefits received from workers' compensation are typically tax-free, which can help offset the cost of the contributions.

In some states, employees may have the option to opt out of workers' compensation insurance if they choose to purchase their own private insurance. However, this is not always possible, and employees should carefully consider the risks and benefits before making such a decision. Opting out of workers' compensation insurance can leave employees vulnerable to financial losses if they are injured on the job and do not have adequate private insurance coverage.

Overall, employee contributions to workers' compensation insurance are an essential part of the system, helping to ensure that all employees have access to the benefits they need in the event of a workplace injury or illness. By understanding how these contributions work and what their rights are under the system, employees can make informed decisions about their own workers' compensation coverage.

Iran's Accountability: Compensation for US Ship Attacks Explored

You may want to see also

Explore related products

![]()

No-Fault System

In the context of workers' compensation, a no-fault system is a mechanism where employees are entitled to benefits regardless of who was at fault for the injury or illness. This system is designed to provide swift and certain compensation to workers, reducing the need for lengthy and costly litigation. Under a no-fault system, employees do not need to prove that their employer was negligent or that they were not at fault for the accident. Instead, they only need to demonstrate that the injury or illness is work-related.

One of the key advantages of a no-fault system is that it streamlines the claims process. Without the need to establish fault, claims can be processed more quickly, and employees can receive the medical care and financial support they need sooner. This can be particularly beneficial for workers who have suffered severe injuries and are unable to return to work immediately. Additionally, a no-fault system can help to reduce the administrative burden on employers, as they do not need to contest claims or engage in legal battles.

However, there are also some potential drawbacks to a no-fault system. One concern is that it may lead to an increase in fraudulent claims, as employees may be more likely to file claims knowing that they do not need to prove fault. Another issue is that a no-fault system may not provide adequate incentives for employers to maintain safe working conditions, as they are not held financially responsible for workplace accidents. To mitigate these risks, many no-fault systems include provisions for monitoring and auditing claims, as well as penalties for employers who fail to comply with safety regulations.

Overall, a no-fault system can provide significant benefits to both employees and employers by simplifying the workers' compensation process and ensuring that injured workers receive the support they need. However, it is important to carefully design and implement such a system to minimize the potential for abuse and to maintain incentives for workplace safety.

Understanding VA Disability Back Pay: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Covered Injuries

In the realm of workers' compensation, the term "covered injuries" refers to the types of injuries that are eligible for benefits under the workers' compensation system. It's crucial to understand that not all injuries sustained by an employee are automatically covered. For an injury to be considered covered, it must meet specific criteria as outlined by the workers' compensation laws of the jurisdiction in question.

Typically, covered injuries are those that occur as a direct result of employment-related activities. This can include injuries sustained while performing job duties, traveling for work, or participating in work-related events. However, the injury must also be work-related in nature. For instance, an employee who slips and falls on a wet floor at the workplace may have a covered injury, whereas an employee who is injured in a car accident while commuting to work may not be covered, unless the accident occurred on the employer's premises or during work hours.

It's also important to note that certain types of injuries may be excluded from coverage. These can include injuries that are the result of the employee's own misconduct, such as being intoxicated on the job, or injuries that occur while the employee is engaged in illegal activities. Additionally, some jurisdictions may exclude injuries that are the result of repetitive stress or strain, unless they can be directly linked to a specific work-related incident.

The process of determining whether an injury is covered can be complex and may involve a thorough investigation. This can include reviewing medical records, interviewing witnesses, and examining the circumstances surrounding the injury. If an injury is deemed to be covered, the employee may be entitled to various benefits, such as medical expenses, lost wages, and rehabilitation costs.

In conclusion, understanding what constitutes a covered injury is essential for both employees and employers. It ensures that employees receive the necessary support and compensation for work-related injuries, while also protecting employers from frivolous claims. By adhering to the guidelines and criteria set forth by workers' compensation laws, both parties can navigate the complexities of workplace injuries with greater clarity and fairness.

Navigating VA Disability Pay: Your Comprehensive Guide to Benefits and Support

You may want to see also

Explore related products

![]()

Benefits Provided

Workers' compensation insurance is a crucial safety net for employees who suffer work-related injuries or illnesses. One of the primary benefits provided by this system is the coverage of medical expenses. This includes not only immediate emergency care but also ongoing treatment, rehabilitation, and any necessary medical devices or medications. Employees do not have to pay out-of-pocket for these expenses, which can be a significant financial relief, especially in cases of severe injuries requiring extensive medical intervention.

In addition to medical coverage, workers' compensation also provides wage replacement benefits. If an employee is unable to work due to their injury or illness, they may be eligible to receive a portion of their regular wages. This helps to ensure that they can continue to support themselves and their families while they are recovering. The amount and duration of these benefits can vary depending on the specific circumstances of the case and the laws of the state in which the employee works.

Another important benefit is the protection against retaliation. Employees who file for workers' compensation are legally protected from being fired or otherwise retaliated against by their employers. This safeguard is essential for ensuring that workers feel safe in coming forward to report their injuries and seek the benefits they are entitled to. It also helps to maintain a fair and just workplace environment, where employees are not penalized for circumstances beyond their control.

Furthermore, workers' compensation can also provide vocational rehabilitation services. These services are designed to help injured employees return to work by offering training, education, and job placement assistance. This can be particularly valuable for workers who have suffered permanent injuries that may limit their ability to perform their previous job duties. By providing these resources, workers' compensation helps to empower employees to regain their independence and contribute to the workforce.

Lastly, in cases where an employee's injury or illness results in permanent disability or death, workers' compensation can provide long-term financial support. This may include disability benefits, which offer ongoing financial assistance to employees who are unable to work due to their condition, or death benefits, which provide financial support to the dependents of an employee who has passed away as a result of a work-related injury or illness. These benefits are critical for ensuring that employees and their families are not left without financial security in the face of tragedy.

Understanding Workers' Compensation Benefits: A Comprehensive Guide

You may want to see also

Frequently asked questions

Generally, employees do not have to pay for workers' compensation. It is typically funded by employers through insurance premiums.

Employers are responsible for paying workers' compensation benefits, either directly or through an insurance carrier.

If an employee is injured at work, they may be eligible for workers' compensation benefits, which can include medical expenses and lost wages.

Workers' compensation requirements vary by jurisdiction, but in many places, it is mandatory for employers to carry workers' compensation insurance.

In some jurisdictions, employees may have the option to opt out of workers' compensation coverage, but this is not common and may have specific conditions or limitations.