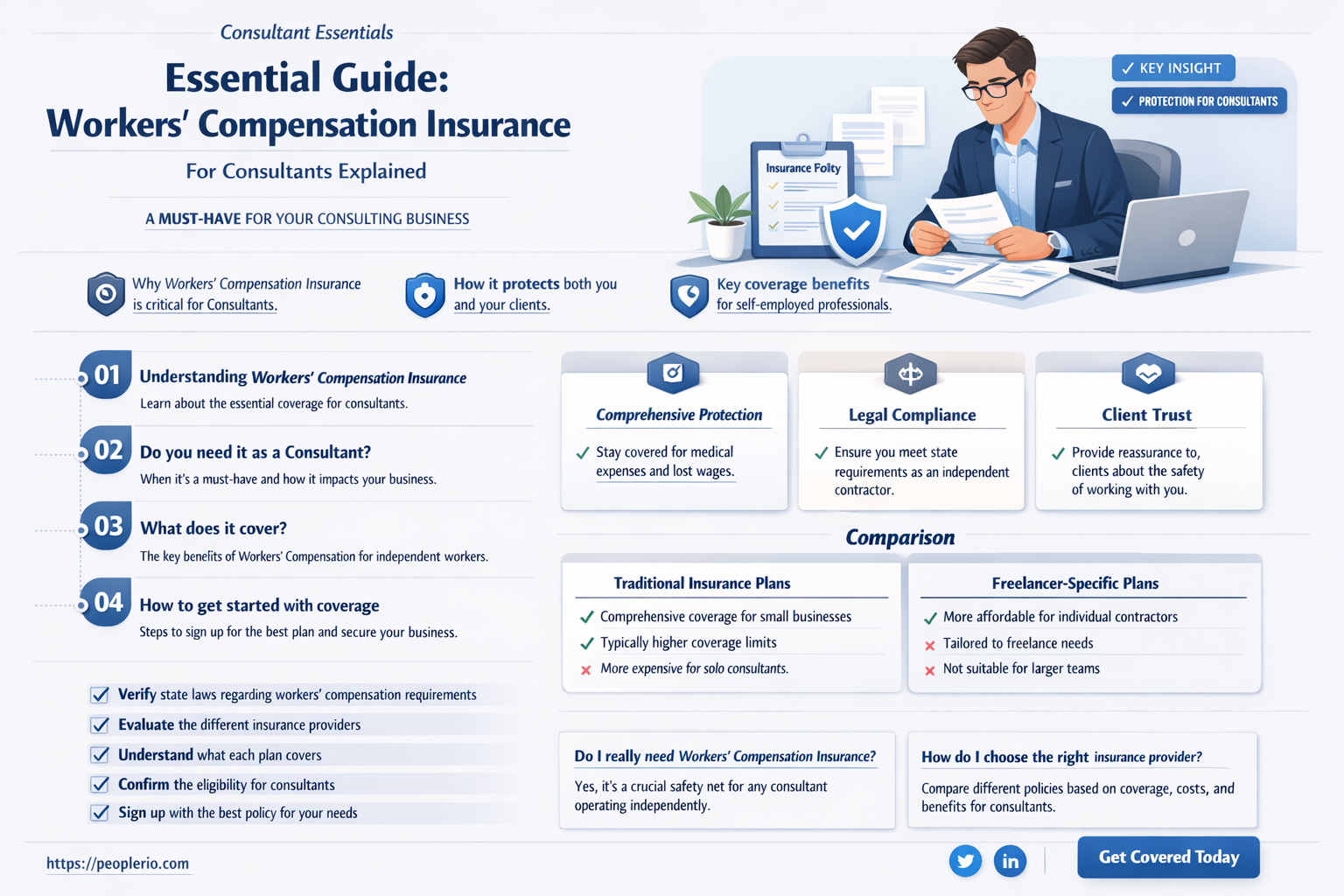

As a consultant, you might be wondering whether workers' compensation insurance is necessary for your business. This type of insurance is designed to protect employees who are injured or become ill as a result of their work. While consultants typically work independently or in small teams, there are still scenarios where workers' compensation insurance could be beneficial. For instance, if you hire subcontractors or temporary workers, you may be responsible for providing this coverage. Additionally, some clients may require you to have workers' compensation insurance as part of your contract. It's essential to understand the specific risks associated with your consulting business and the legal requirements in your state or country to determine if this insurance is necessary for you.

Explore related products

What You'll Learn

- Legal Requirements: Understand if your consulting business is legally required to carry workers' compensation insurance

- Client Mandates: Check if your clients demand you have workers' compensation insurance before engaging your services

- Risk Assessment: Evaluate the risks associated with your consulting work to determine the necessity of insurance

- Cost Considerations: Weigh the costs of workers' compensation insurance against the potential risks and liabilities

- Alternative Coverage: Explore alternative insurance options that might better suit your consulting business needs

![]()

Legal Requirements: Understand if your consulting business is legally required to carry workers' compensation insurance

As a consultant, understanding the legal requirements regarding workers' compensation insurance is crucial to ensure compliance and mitigate potential risks. The necessity of carrying such insurance largely depends on the nature of your consulting business, the number of employees you have, and the specific regulations in your state or country.

In many jurisdictions, workers' compensation insurance is mandatory for businesses with a certain number of employees. For instance, in the United States, the threshold varies by state, with some states requiring coverage for all businesses with one or more employees, while others may exempt small businesses or those in certain industries. It is essential to consult your local labor laws to determine if your consulting business falls under the mandatory coverage requirements.

Even if your business is not legally required to carry workers' compensation insurance, it may still be advisable to obtain coverage. Consulting work can involve various risks, such as workplace accidents, injuries, or illnesses that could result in costly medical bills and potential lawsuits. Having workers' compensation insurance can provide financial protection and help cover the costs of medical treatment, lost wages, and other expenses related to work-related injuries or illnesses.

When evaluating the need for workers' compensation insurance, consider the nature of the work performed by your consulting business. If your consultants work in hazardous environments, operate heavy machinery, or engage in physically demanding tasks, the risk of injury is higher, and insurance coverage becomes more critical. On the other hand, if your consulting work primarily involves office-based tasks with minimal physical risks, the need for workers' compensation insurance may be less pressing.

To determine if your consulting business is legally required to carry workers' compensation insurance, follow these steps:

- Research your local labor laws and regulations to understand the requirements for workers' compensation insurance in your jurisdiction.

- Assess the number of employees in your business, as this is a key factor in determining mandatory coverage.

- Evaluate the nature of the work performed by your consultants to identify potential risks and hazards.

- Consult with a legal professional or an insurance advisor to discuss your specific situation and obtain guidance on compliance with legal requirements.

By taking these steps, you can ensure that your consulting business is in compliance with legal requirements and adequately protected against potential risks associated with workplace injuries or illnesses.

Top-Rated Employers Compensation Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Client Mandates: Check if your clients demand you have workers' compensation insurance before engaging your services

As a consultant, it's crucial to understand the specific requirements and mandates set by your clients. One such mandate that you may encounter is the demand for workers' compensation insurance. This requirement is not just a formality; it's a critical aspect of ensuring that both you and your client are protected in case of work-related injuries or illnesses.

When engaging with a new client, it's essential to review their contractual requirements carefully. Look for clauses that specify the need for workers' compensation insurance. If such a clause is present, it typically means that the client wants to ensure that you, as a consultant, are covered under this insurance. This is particularly important if you will be working on-site or if your work involves physical labor or exposure to potential hazards.

The demand for workers' compensation insurance can also be a reflection of the client's risk management strategy. By requiring this insurance, the client is mitigating the risk of being held liable for any work-related injuries or illnesses that may occur during the course of your consultancy. This is especially relevant in industries where the risk of accidents is higher, such as construction, manufacturing, or healthcare.

If you find that a client does indeed require you to have workers' compensation insurance, it's important to obtain the necessary coverage promptly. Failure to do so could result in the termination of your contract or legal repercussions. Moreover, having this insurance in place can provide you with peace of mind, knowing that you are protected in the event of an unforeseen incident.

In conclusion, always check your client's mandates regarding workers' compensation insurance. This not only ensures compliance with their requirements but also demonstrates your commitment to maintaining a safe and responsible working environment. By understanding and adhering to these mandates, you can foster stronger relationships with your clients and protect yourself from potential liabilities.

Do I Really Need Workers' Comp Insurance for My Small Business?

You may want to see also

Explore related products

![]()

Risk Assessment: Evaluate the risks associated with your consulting work to determine the necessity of insurance

As a consultant, it's crucial to conduct a thorough risk assessment to determine whether you need workers' compensation insurance. This involves evaluating the potential hazards and liabilities associated with your consulting work. Start by identifying the nature of your consulting services and the environments in which you operate. Consider factors such as the physical demands of your work, the use of equipment or machinery, and the potential for accidents or injuries.

Next, assess the likelihood and potential impact of these risks. For example, if you're a construction consultant, you may face a higher risk of physical injury compared to a marketing consultant. Evaluate the severity of potential injuries and the associated medical costs, as well as the impact on your ability to work. Additionally, consider the legal and financial implications of not having adequate insurance coverage.

Once you've identified and assessed the risks, determine the appropriate level of insurance coverage. This may involve consulting with an insurance professional to understand the different types of workers' compensation insurance policies available and their specific benefits and limitations. Consider factors such as the cost of premiums, the coverage limits, and the deductibles when selecting a policy.

It's also important to implement risk mitigation strategies to reduce the likelihood and impact of potential hazards. This may include developing safety protocols, providing training to employees or clients, and maintaining a safe work environment. By taking proactive steps to manage risks, you can not only protect yourself and your business but also potentially reduce your insurance premiums.

In conclusion, conducting a comprehensive risk assessment is essential for consultants to determine the necessity of workers' compensation insurance. By carefully evaluating the risks associated with your work and implementing appropriate risk management strategies, you can make informed decisions about insurance coverage and protect your business from potential liabilities.

Understanding the Tax Implications of Insurance Compensation

You may want to see also

Explore related products

![]()

Cost Considerations: Weigh the costs of workers' compensation insurance against the potential risks and liabilities

As a consultant, you may be inclined to focus on the immediate costs of workers' compensation insurance, but it's crucial to consider the long-term implications of potential risks and liabilities. While the premiums may seem high, the cost of not having adequate coverage can be far more detrimental to your business.

For instance, if one of your consultants is injured on the job, without workers' compensation insurance, you could be held personally liable for their medical expenses and lost wages. This could lead to significant financial strain, potentially even bankruptcy. On the other hand, with proper insurance in place, you can mitigate these risks and protect your business from such devastating consequences.

Moreover, workers' compensation insurance can also provide coverage for legal fees and settlements, which can be substantial in the event of a lawsuit. By weighing the costs of insurance against the potential risks and liabilities, you can make an informed decision that safeguards your business and your consultants.

It's also important to consider the potential impact on your reputation. If you're found to be negligent in providing a safe working environment or adequate insurance coverage, it could damage your professional image and make it difficult to attract future clients. In contrast, demonstrating a commitment to safety and responsible business practices can enhance your reputation and build trust with potential clients.

Ultimately, the decision to purchase workers' compensation insurance as a consultant should be based on a careful evaluation of the costs and benefits. By considering the potential risks and liabilities, you can make a well-informed decision that protects your business and your consultants.

Securing Workers' Compensation Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Alternative Coverage: Explore alternative insurance options that might better suit your consulting business needs

As a consultant, you may find that traditional workers' compensation insurance isn't the best fit for your business model. Perhaps you work alone, subcontract work, or have a unique risk profile that isn't adequately covered by standard policies. In such cases, exploring alternative insurance options can be crucial to ensure you're protected without overpaying or underinsuring.

One alternative to consider is professional liability insurance, also known as errors and omissions (E&O) insurance. This type of coverage protects you against claims arising from professional mistakes or negligence, which can be a significant risk for consultants. While it doesn't cover workplace injuries like workers' compensation does, it can provide essential protection for your business reputation and financial stability.

Another option is business owners' policy (BOP) insurance, which bundles general liability and property insurance into a single, cost-effective package. This can be particularly useful for consultants who work from home or have a small office, as it covers both your business operations and your property. However, it's important to note that BOPs typically don't include workers' compensation coverage, so you may need to purchase this separately if you have employees.

If you frequently travel for work, you might also consider travel insurance that includes coverage for business-related activities. This can protect you against a range of risks, from trip cancellations to equipment loss or theft. Some policies even offer coverage for political risks or natural disasters, which can be valuable for consultants working in volatile or disaster-prone areas.

Ultimately, the key to finding the right alternative coverage is to carefully assess your business needs and risks. Consider factors such as the nature of your work, your business structure, and the potential liabilities you face. By doing so, you can identify the insurance options that will provide the most comprehensive and cost-effective protection for your consulting business.

Understanding Workers' Compensation Insurance: A Guide for Employers

You may want to see also

Frequently asked questions

As a consultant, you may not need workers' compensation insurance if you are working as an independent contractor and not hiring any employees. However, it's essential to check the specific laws and regulations in your state or country, as requirements can vary.

Workers' compensation insurance is a type of insurance that provides wage replacement and medical benefits to employees who are injured or become ill as a result of their work. It covers medical expenses, lost wages, and rehabilitation costs, among other things.

The determination of whether you are an employee or an independent contractor depends on various factors, including the level of control your employer has over your work, how you are paid, and whether you have the ability to work for multiple clients. It's crucial to review the specific laws and guidelines in your jurisdiction to make this determination.

If you are required to have workers' compensation insurance and do not have it, you may face legal penalties, fines, or even criminal charges. Additionally, you may be held personally liable for any work-related injuries or illnesses that occur without proper insurance coverage.

To obtain workers' compensation insurance, you can contact an insurance agent or broker who specializes in this type of coverage. They will be able to guide you through the process and help you find a policy that meets your specific needs and budget.