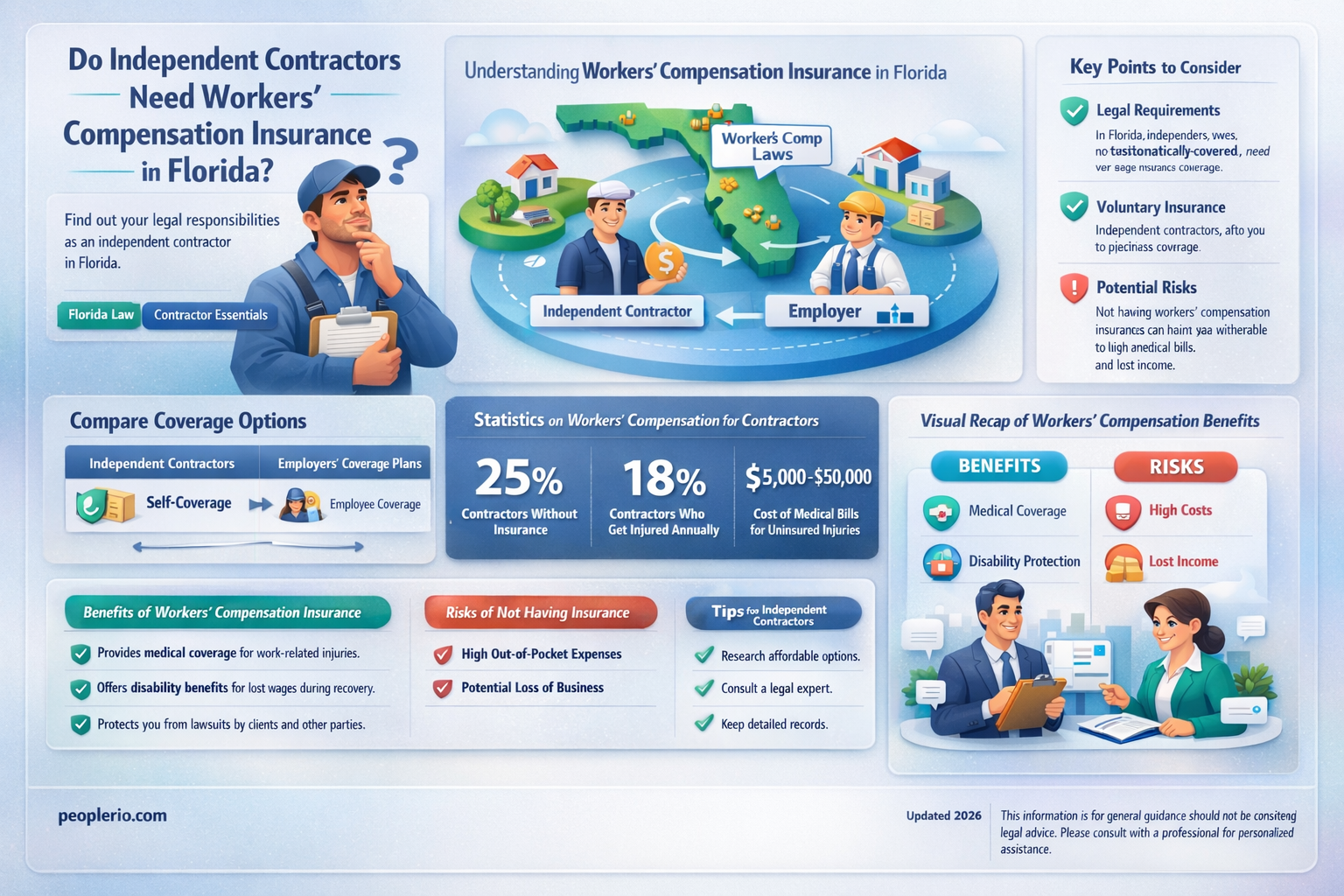

In Florida, the requirement for workers' compensation insurance varies depending on the nature of the business and the number of employees. For independent contractors, the rules can be particularly nuanced. Generally, independent contractors are not considered employees and therefore are not mandated to have workers' compensation insurance. However, there are exceptions and specific circumstances that might necessitate such coverage. For instance, if an independent contractor hires their own employees, they may be required to carry workers' compensation insurance to protect those workers. Additionally, certain industries or contracts may stipulate that independent contractors must have this insurance as a condition of their work agreements. Understanding these requirements is crucial for independent contractors in Florida to ensure compliance with state laws and to protect themselves and their workers from potential liabilities.

Explore related products

What You'll Learn

- Legal Requirements: Florida law mandates workers' compensation insurance for businesses with four or more employees

- Independent Contractor Status: Misclassification of employees as independent contractors can lead to legal and financial repercussions

- Insurance Coverage Options: Independent contractors may opt for personal liability insurance or workers' compensation coverage

- Cost Factors: Premiums vary based on the nature of work, employee count, and claims history

- Consequences of Non-Compliance: Failure to secure required insurance can result in penalties, fines, and potential legal action

![]()

Legal Requirements: Florida law mandates workers' compensation insurance for businesses with four or more employees

Florida law requires businesses with four or more employees to carry workers' compensation insurance. This mandate is designed to protect workers who suffer job-related injuries or illnesses, ensuring they receive necessary medical care and wage replacement. For businesses, this insurance helps mitigate the financial risks associated with workplace accidents.

Independent contractors in Florida are generally not considered employees and therefore are not covered under an employer's workers' compensation policy. However, there are exceptions and nuances to this rule. For instance, if an independent contractor is injured while working on a project for a business that is required to have workers' compensation insurance, they may still be eligible for coverage if they can prove that the business had control over their work and that the injury occurred within the scope of their employment.

It's important for independent contractors to understand their rights and options regarding workers' compensation insurance. They may choose to purchase their own workers' compensation policy to protect themselves in case of an injury. Additionally, independent contractors should be aware of the potential risks and liabilities associated with not having workers' compensation coverage, such as being personally responsible for medical expenses and lost wages.

In conclusion, while Florida law mandates workers' compensation insurance for businesses with four or more employees, independent contractors are typically not covered under these policies. Independent contractors should consider purchasing their own coverage to protect themselves from the financial risks associated with workplace injuries.

Suing Workers' Comp Insurance for Malpractice: What You Need to Know

You may want to see also

Explore related products

![]()

Independent Contractor Status: Misclassification of employees as independent contractors can lead to legal and financial repercussions

Misclassifying employees as independent contractors can have significant legal and financial consequences for businesses. In Florida, this misclassification can lead to penalties, fines, and even criminal charges. The Florida Department of Economic Opportunity (DEO) and the Internal Revenue Service (IRS) are vigilant in identifying and addressing such misclassifications. Businesses found guilty of misclassifying employees may be required to pay back wages, taxes, and benefits, along with substantial fines.

One of the key factors in determining whether a worker is an employee or an independent contractor is the level of control the business has over the worker. If a business controls the worker's schedule, tasks, and methods of work, the worker is likely considered an employee. Independent contractors, on the other hand, typically have more autonomy and control over their work. They often set their own schedules, choose their own projects, and determine their own methods of work.

Another important factor is the financial relationship between the business and the worker. Employees are typically paid a salary or hourly wage, while independent contractors are paid on a project-by-project basis or by the hour. Independent contractors are also responsible for their own taxes and benefits, whereas employees have these taken care of by their employer.

In Florida, independent contractors are not required to have workers' compensation insurance. However, businesses that misclassify employees as independent contractors may still be held liable for workers' compensation claims. This is because the misclassification does not change the nature of the work being performed or the risks associated with it. If an employee is injured on the job, the business may be required to provide workers' compensation benefits, regardless of how the employee was classified.

To avoid misclassification and the associated legal and financial repercussions, businesses should carefully evaluate their relationships with workers. They should consider factors such as the level of control they have over the worker, the financial relationship, and the nature of the work being performed. If there is any uncertainty, businesses should consult with legal and financial professionals to ensure they are in compliance with Florida law.

Do Contractors Need Workers' Compensation Insurance?

You may want to see also

Explore related products

![]()

Insurance Coverage Options: Independent contractors may opt for personal liability insurance or workers' compensation coverage

Independent contractors in Florida have several insurance coverage options to consider, each tailored to different needs and risks. Personal liability insurance is one such option, providing protection against claims of bodily injury or property damage for which the contractor may be held responsible. This type of insurance is crucial for contractors who work in environments where accidents could occur, such as construction sites or clients' homes.

Another important coverage option is workers' compensation insurance. While not always mandatory for independent contractors in Florida, it can be a vital safeguard. Workers' compensation covers medical expenses and lost wages if a contractor is injured on the job. This insurance is particularly beneficial for those who work in high-risk industries or perform physically demanding tasks.

When deciding between these coverage options, contractors should carefully assess their specific risks and the nature of their work. Factors such as the type of projects they undertake, the environments in which they work, and their financial situation should all be considered. It's also advisable for contractors to consult with an insurance professional who can provide tailored advice based on their unique circumstances.

In addition to personal liability and workers' compensation insurance, independent contractors may also want to explore other coverage options such as business auto insurance, equipment insurance, and professional liability insurance. These additional coverages can provide comprehensive protection against a wide range of potential risks and liabilities.

Ultimately, the decision of which insurance coverage options to choose depends on the individual contractor's needs and preferences. By carefully evaluating their risks and consulting with an insurance expert, contractors can ensure they have the appropriate coverage to protect themselves and their businesses.

Navigating Dental Coverage During Workers' Compensation: What You Need to Know

You may want to see also

Explore related products

![]()

Cost Factors: Premiums vary based on the nature of work, employee count, and claims history

The cost of workers' compensation insurance for independent contractors in Florida can vary significantly based on several key factors. One of the primary determinants of premium rates is the nature of the work being performed. Jobs that are considered high-risk, such as construction or manufacturing, will typically incur higher premiums due to the increased likelihood of workplace injuries. Conversely, professions that are deemed lower-risk, such as administrative or clerical work, may benefit from lower premium rates.

Another crucial factor influencing premium costs is the employee count. Even though independent contractors may not have traditional employees, the number of subcontractors or other workers they engage with can impact their insurance rates. More workers generally mean higher premiums, as the potential for workplace accidents increases with the size of the workforce.

Claims history is also a significant consideration in determining workers' compensation insurance premiums. Contractors with a history of frequent or severe claims may face higher premiums, as insurers view them as higher-risk clients. On the other hand, those with a clean claims history or who have implemented effective safety measures may be rewarded with lower premium rates.

In addition to these factors, insurers may also consider the contractor's payroll and the overall economic conditions of the industry when setting premium rates. It's essential for independent contractors to shop around and compare quotes from different insurers to find the most competitive rates that adequately cover their specific needs.

To mitigate the impact of these cost factors, independent contractors can take proactive steps to improve their risk profile. This may include implementing comprehensive safety training programs, maintaining a safe work environment, and regularly reviewing and updating their safety protocols. By demonstrating a commitment to workplace safety, contractors can potentially reduce their premium costs and improve their overall insurability.

Understanding Tax Deductions for Medical Insurance Premiums and Workers' Compensation

You may want to see also

Explore related products

![]()

Consequences of Non-Compliance: Failure to secure required insurance can result in penalties, fines, and potential legal action

In the state of Florida, independent contractors are generally not required to carry workers' compensation insurance if they do not have employees. However, there are specific circumstances and industries where this requirement may apply, such as in construction or for certain types of subcontractors. It is crucial for independent contractors to understand these nuances to avoid non-compliance, which can lead to severe consequences.

One of the primary consequences of failing to secure required insurance is financial penalties. These can include fines imposed by state regulatory agencies, which can vary depending on the severity and duration of the non-compliance. For instance, a first-time offense might result in a warning or a small fine, while repeated or willful violations could lead to significantly higher penalties.

Beyond financial penalties, non-compliance can also result in legal action. This might include lawsuits from injured workers who were not properly covered, or from regulatory bodies seeking to enforce compliance through the courts. Legal action can be costly and time-consuming, and may also result in further financial damages if the contractor is found liable.

Moreover, failure to comply with insurance requirements can damage an independent contractor's reputation and business prospects. Clients may be hesitant to hire a contractor who is not properly insured, as it could expose them to potential liabilities. This can lead to a loss of income and opportunities for the contractor.

To mitigate these risks, independent contractors should carefully review Florida's workers' compensation laws and consult with an insurance professional to determine their specific coverage needs. They should also stay informed about any changes to the law or industry regulations that could impact their insurance requirements. By taking these steps, contractors can protect themselves from the consequences of non-compliance and ensure that they are operating their businesses legally and responsibly.

Understanding Workers' Compensation Insurance Requirements in Arizona

You may want to see also

Frequently asked questions

In Florida, independent contractors are not required to carry workers' compensation insurance unless they have employees. However, it's often recommended to have such insurance to protect oneself from potential work-related injuries or illnesses.

Exceptions include independent contractors who work in the construction industry or who have employees. These individuals are required to carry workers' compensation insurance to cover themselves and their workers.

Yes, independent contractors can choose to carry workers' compensation insurance even if it's not mandatory. This can provide them with financial protection in case of work-related accidents or health issues.

Without workers' compensation insurance, independent contractors may be personally liable for medical expenses and lost wages if they are injured or become ill due to their work. This can lead to significant financial burdens.

Independent contractors can obtain workers' compensation insurance through various insurance providers. They should shop around for policies that suit their specific needs and budget, ensuring they understand the terms and coverage provided.