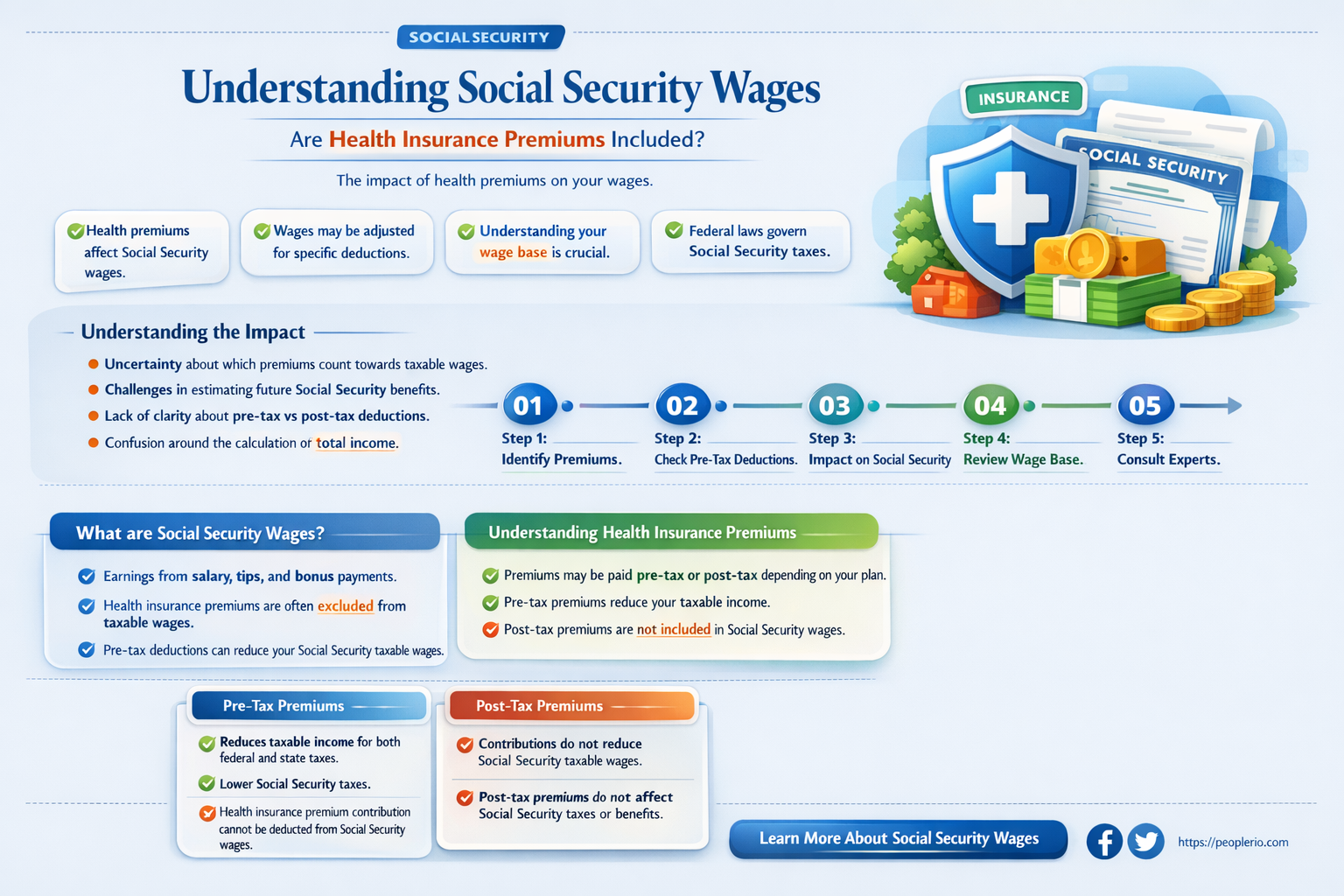

Social Security wages are a crucial aspect of an employee's compensation, impacting their future retirement benefits. These wages include not only the hourly or salaried pay but also certain other forms of compensation. One common question that arises is whether employee health insurance premiums are included in Social Security wages. To answer this, it's essential to understand the specifics of how Social Security wages are calculated and what types of compensation are considered taxable for this purpose.

| Characteristics | Values |

|---|---|

| Inclusion of Employee Health Insurance Premiums | Not included |

| What is Included in Social Security Wages | Gross wages, salaries, tips, bonuses, overtime pay, and certain other compensation |

| Purpose of Social Security Wages | To calculate Social Security tax liability and determine benefit eligibility |

| Impact on Employees | Employees pay Social Security tax on their wages, which funds retirement, disability, and survivor benefits |

| Impact on Employers | Employers also pay Social Security tax on employee wages and may need to withhold and report these taxes |

| Exceptions | Certain types of compensation, such as severance pay, may be exempt from Social Security wages |

| Reporting Requirements | Employers must report Social Security wages on Form W-2 and pay the associated taxes |

Explore related products

What You'll Learn

![]()

Definition of social security wages

Social Security wages are defined as the earnings an employee receives from their employer, which are subject to Social Security tax. This includes salaries, wages, bonuses, and other forms of compensation. However, not all forms of compensation are considered Social Security wages. For example, certain types of fringe benefits, such as health insurance premiums paid by the employer, are generally not included in the calculation of Social Security wages.

The distinction between what is and is not considered Social Security wages is important for both employers and employees. Employers are responsible for withholding Social Security taxes from their employees' wages and paying their own share of these taxes. Employees, on the other hand, need to understand what forms of compensation are subject to Social Security tax in order to accurately report their earnings and pay the correct amount of taxes.

In the case of health insurance premiums, the general rule is that if the employer pays the premiums directly to the insurance company, these payments are not considered Social Security wages. However, if the employer reimburses the employee for health insurance premiums they have paid out-of-pocket, this reimbursement may be considered taxable wages. This is because the reimbursement is essentially a form of compensation for the employee's expenses, and therefore subject to Social Security tax.

It's also worth noting that there are some exceptions to the general rule regarding health insurance premiums. For example, if an employer provides health insurance coverage to its employees through a self-insured plan, the premiums paid by the employer may be considered Social Security wages. Additionally, if an employer offers health insurance coverage to its employees through a health reimbursement arrangement (HRA), the amounts reimbursed to employees for health insurance premiums may also be considered taxable wages.

In conclusion, while health insurance premiums paid by an employer are generally not considered Social Security wages, there are some exceptions to this rule. Employers and employees should consult with a tax professional or refer to IRS publications for more information on the specific circumstances under which health insurance premiums may be considered taxable wages.

Understanding Florida's Employee Health Care Act: Key Requirements Explained

You may want to see also

Explore related products

![]()

Exclusion of health insurance premiums

The exclusion of health insurance premiums from social security wages is a critical aspect of payroll management that employers must understand to ensure compliance with tax regulations. Social security wages are the earnings on which social security taxes are paid, and they generally include most forms of compensation an employee receives. However, certain types of compensation, such as health insurance premiums paid by the employer, are excluded from this calculation. This exclusion is based on the premise that health insurance is a fringe benefit provided to employees, rather than a form of taxable income.

Employers must accurately determine which health insurance premiums are excluded from social security wages. Typically, premiums for employer-sponsored health insurance plans are excluded, as long as they are paid directly by the employer and not deducted from the employee's wages. This exclusion applies to both the employee's and employer's portions of the premiums. However, if an employee pays for health insurance premiums through a cafeteria plan or other arrangement where the premiums are deducted from their wages, these amounts are generally included in social security wages.

It's important to note that the exclusion of health insurance premiums from social security wages does not affect the calculation of Medicare wages, which are subject to a separate tax. Medicare wages include all forms of compensation, including health insurance premiums, regardless of whether they are paid by the employer or deducted from the employee's wages. This distinction between social security and Medicare wages can be complex, and employers should consult with a tax professional to ensure they are accurately calculating and reporting both types of wages.

In addition to the tax implications, the exclusion of health insurance premiums from social security wages can also impact employee benefits. For example, social security benefits are calculated based on an individual's earnings history, and excluding health insurance premiums from this calculation could potentially result in lower benefits for employees. Employers should consider this when designing their compensation and benefits packages to ensure they are providing the best possible support for their employees.

To summarize, the exclusion of health insurance premiums from social security wages is a nuanced aspect of payroll management that requires careful consideration. Employers must understand the specific rules and regulations governing this exclusion to ensure compliance with tax laws and to provide accurate information to their employees. By doing so, they can help their employees maximize their social security benefits while also maintaining a competitive compensation and benefits package.

Exploring the Legality of Health Screenings for Hospital Staff

You may want to see also

Explore related products

$28.24 $45

![]()

Impact on taxable income

Employee health insurance premiums can have a significant impact on taxable income. When an employer provides health insurance to its employees, the premiums paid by the employer are generally considered a tax-deductible business expense. This means that the employer can reduce their taxable income by the amount of the premiums paid, which can lead to a lower tax liability.

However, the tax treatment of employee health insurance premiums can be complex. For example, if an employer offers a flexible spending account (FSA) or a health savings account (HSA) to its employees, the premiums paid by the employer may not be tax-deductible. Additionally, if an employer provides health insurance to its employees through a self-insured plan, the tax treatment of the premiums may differ from that of a fully insured plan.

It's also important to note that the tax impact of employee health insurance premiums can vary depending on the specific circumstances of the employer and the employees. For example, if an employer provides health insurance to its employees as a fringe benefit, the premiums paid by the employer may be considered taxable income to the employees. This can lead to a higher tax liability for the employees, which can offset the tax benefits of the employer's deduction.

In conclusion, the impact of employee health insurance premiums on taxable income can be significant, but it's important to consider the specific circumstances and tax implications of each situation. Employers should consult with a tax professional to ensure that they are taking advantage of all available tax benefits while also complying with applicable tax laws and regulations.

Are Employee Paid Health Insurance Premiums Subject to FUTA?

You may want to see also

Explore related products

![]()

Employer and employee contributions

Employers and employees both contribute to Social Security wages, which are used to calculate the amount of Social Security tax owed. While employer contributions are typically higher, employee contributions are also a significant portion of the total Social Security tax. It's important to note that these contributions are separate from any health insurance premiums paid by either the employer or employee.

One common misconception is that employee health insurance premiums are included in Social Security wages. However, this is not the case. Social Security wages are calculated based on an employee's gross wages, which do not include health insurance premiums. This means that employees do not pay Social Security tax on their health insurance premiums, and employers do not include these premiums when calculating their Social Security tax obligations.

Another important aspect to consider is the impact of employer-provided health insurance on an employee's taxable wages. While the cost of health insurance premiums paid by an employer is not included in an employee's gross wages for Social Security tax purposes, it can still affect the employee's taxable wages for other tax purposes, such as federal income tax. This is because employer-provided health insurance is considered a form of compensation, and therefore must be reported as taxable wages on an employee's W-2 form.

In summary, employer and employee contributions to Social Security wages are separate from health insurance premiums, and employees do not pay Social Security tax on their health insurance premiums. However, employer-provided health insurance can still affect an employee's taxable wages for other tax purposes. It's important for both employers and employees to understand these distinctions in order to accurately calculate and report their tax obligations.

Exploring the Mandate: Employee Health in Hospitals

You may want to see also

Explore related products

![]()

Tax implications and benefits

Employee health insurance premiums can have significant tax implications and benefits, both for employers and employees. One key aspect to consider is that employer contributions to employee health insurance are generally tax-deductible as a business expense. This means that employers can reduce their taxable income by the amount they pay towards employee health insurance premiums, which can lead to lower tax liabilities.

For employees, the tax benefits of health insurance premiums can be even more substantial. In many cases, employee contributions to health insurance are made on a pre-tax basis, meaning that the money is deducted from their gross income before taxes are calculated. This reduces the employee's taxable income, resulting in lower federal, state, and local tax withholdings. Additionally, any employer contributions to health insurance are not considered taxable income to the employee, further reducing their tax burden.

Another important consideration is the impact of health insurance premiums on Social Security wages. Social Security taxes are calculated based on an employee's gross wages, which includes their salary, tips, and other forms of compensation. However, employer contributions to health insurance are not considered part of an employee's gross wages for Social Security tax purposes. This means that employers do not need to pay Social Security taxes on the amount they contribute to employee health insurance premiums, which can lead to significant tax savings.

It's also worth noting that the tax implications of health insurance premiums can vary depending on the type of plan and the specific circumstances of the employer and employee. For example, self-employed individuals may be able to deduct their health insurance premiums as a business expense, but they may also be subject to additional taxes if they are not properly structured. Similarly, employers who offer health insurance plans that are not considered "qualified" under federal law may face different tax consequences than those who offer qualified plans.

In conclusion, understanding the tax implications and benefits of employee health insurance premiums is crucial for both employers and employees. By taking advantage of available tax deductions and structuring health insurance plans appropriately, businesses and individuals can reduce their tax liabilities and maximize their financial benefits.

Unveiling the Truth: Are Employee Health Incentive Programs Truly Confidential?

You may want to see also

Frequently asked questions

Yes, social security wages do include employee health insurance premiums. These premiums are considered part of the total compensation an employee receives and are subject to social security taxes.

Employee health insurance premiums are calculated based on the amount deducted from the employee's wages for health insurance coverage. This amount is added to the employee's gross wages to determine the total social security wages.

Generally, there are no exceptions to including health insurance premiums in social security wages. However, certain types of health insurance plans, such as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs), may have different tax implications and should be reviewed on a case-by-case basis.

Including health insurance premiums in social security wages can have a positive impact on an employee's benefits. It increases the total amount of wages subject to social security taxes, which can lead to higher social security benefits upon retirement or disability. Additionally, it ensures that employees are properly credited for their contributions to social security, even when a portion of their wages is deducted for health insurance.