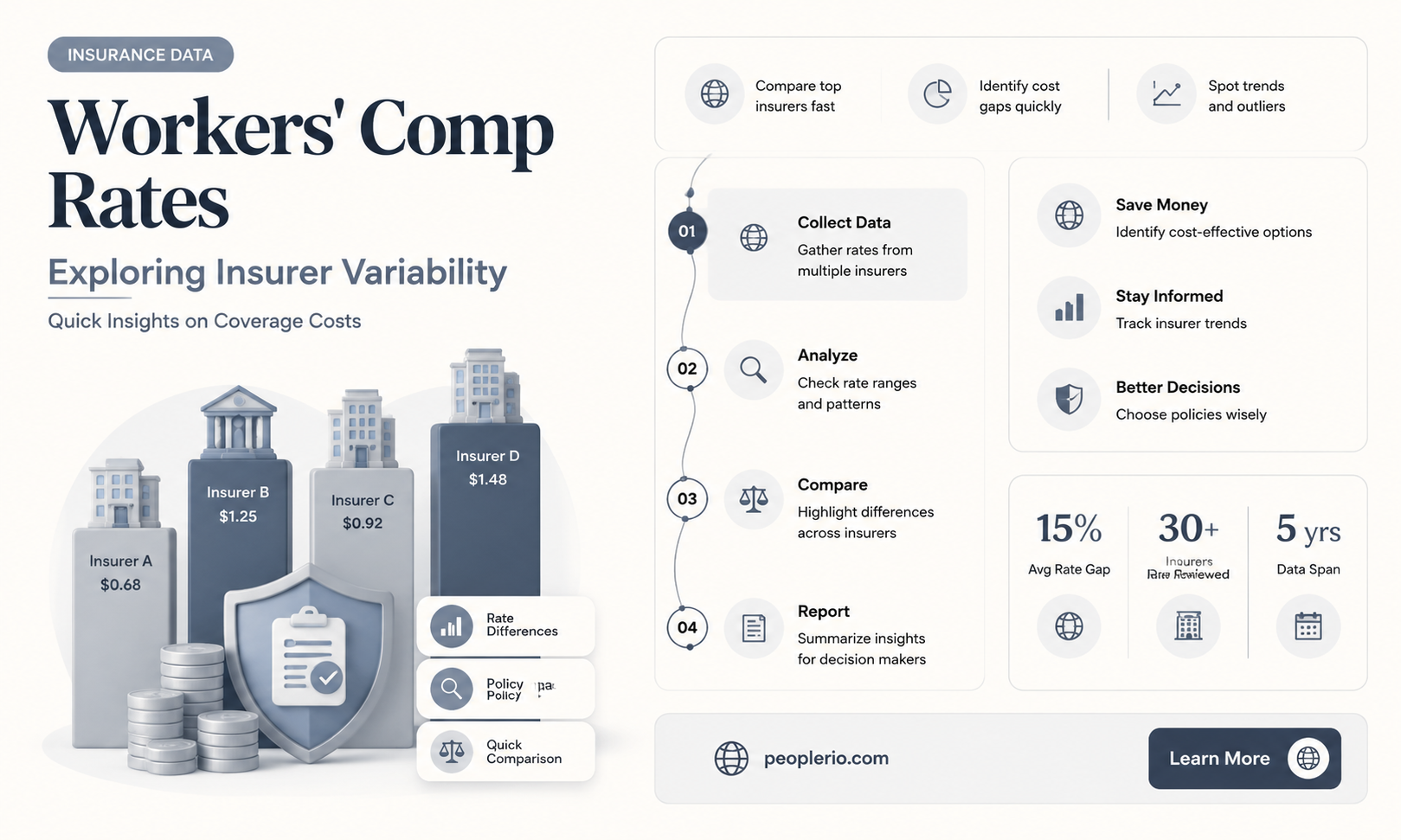

Workers' compensation insurance is a crucial aspect of business operations, providing financial protection to employees who suffer work-related injuries or illnesses. One common question among business owners and employees alike is whether workers' compensation rates vary significantly between different insurance companies. The answer to this question can be complex, as rates are influenced by a multitude of factors including the industry, the company's claims history, and the specific coverage options chosen. While there may be some variation in rates between insurers, it is important to note that the differences are often not as dramatic as one might expect. Insurance companies typically base their rates on actuarial tables and risk assessments, which means that they are generally operating within a similar framework. However, it is still advisable for businesses to shop around and compare rates from different providers to ensure they are getting the best possible coverage at a competitive price.

Explore related products

What You'll Learn

- Factors Influencing Rates: Understand the key factors that impact workers' compensation insurance rates across different companies

- Industry-Specific Variations: Explore how rates differ by industry, reflecting the unique risks and claims histories of each sector

- Geographic Differences: Analyze how location affects rates, as state regulations and local economic conditions can influence pricing

- Company Size and Experience: Investigate how the size and experience of an insurance company can lead to variations in rates offered

- Claims History Impact: Examine the role of an employer's claims history in determining the rates they are offered by insurers

![]()

Factors Influencing Rates: Understand the key factors that impact workers' compensation insurance rates across different companies

Workers' compensation insurance rates can vary significantly across different companies due to several key factors. One of the primary influences is the company's claims history. Insurers assess the frequency and severity of past claims to determine the likelihood of future claims, which directly impacts the premium rates. Companies with a history of fewer or less severe claims are likely to benefit from lower rates.

Another critical factor is the nature of the business and the associated risks. Industries with higher inherent risks, such as construction or manufacturing, typically face higher workers' compensation rates. This is because the probability of workplace injuries is greater in these sectors. Conversely, businesses in lower-risk industries, like office-based companies, may enjoy more favorable rates.

The size of the company and its payroll also play a role in determining workers' compensation rates. Larger companies with higher payrolls may be able to negotiate better rates due to their greater bargaining power and the potential for bulk discounts. Additionally, companies that implement robust safety measures and training programs may be rewarded with lower premiums, as these initiatives can help reduce the risk of workplace accidents and injuries.

Geographic location is another factor that can influence workers' compensation rates. Different states have varying regulatory environments and cost of living indices, which can impact the cost of insurance. For example, states with higher medical costs or more stringent workers' compensation laws may have higher premium rates.

Lastly, the financial stability and creditworthiness of the insurance company itself can affect the rates it offers. Insurers with strong financial ratings may be able to provide more competitive rates, while those with lower ratings might charge higher premiums to mitigate their risk.

In summary, workers' compensation insurance rates are influenced by a complex interplay of factors, including claims history, industry risks, company size, geographic location, and the financial stability of the insurer. Understanding these factors can help businesses make informed decisions when selecting a workers' compensation insurance policy.

QuickBooks Conundrum: Unchecking Workers' Compensation Insurance

You may want to see also

Explore related products

![]()

Industry-Specific Variations: Explore how rates differ by industry, reflecting the unique risks and claims histories of each sector

Workers' compensation rates exhibit significant industry-specific variations, driven by the unique risks and claims histories associated with each sector. For instance, industries such as construction, manufacturing, and healthcare typically face higher rates due to the physically demanding nature of the work and the increased likelihood of workplace injuries. In contrast, industries like finance, technology, and administration generally enjoy lower rates, reflecting the comparatively safer working environments and fewer claims filed.

These variations are further influenced by factors such as the frequency and severity of claims, the effectiveness of safety measures, and the regulatory environment specific to each industry. Insurance companies analyze historical claims data and industry trends to determine rates that accurately reflect the risk profile of each sector. This results in a tailored approach to pricing workers' compensation insurance, ensuring that businesses are charged rates that align with their actual risk exposure.

Moreover, within each industry, there can be additional variations based on specific job roles and tasks. For example, in the healthcare industry, rates may differ between administrative staff, nurses, and physicians, reflecting the varying levels of risk associated with each role. Similarly, in the construction industry, rates may vary between general laborers, electricians, and roofers, due to the different hazards and physical demands of each job.

Understanding these industry-specific variations is crucial for businesses when selecting workers' compensation insurance. By working with an insurance provider that specializes in their industry, businesses can ensure they are receiving rates that accurately reflect their risk profile, potentially leading to cost savings and more comprehensive coverage. Additionally, businesses can take proactive steps to improve their safety measures and claims management processes, which can further influence their rates and overall insurance costs.

In conclusion, the significant industry-specific variations in workers' compensation rates underscore the importance of a tailored approach to insurance pricing. By considering the unique risks and claims histories of each sector, insurance companies can provide more accurate and fair rates, ultimately benefiting both businesses and employees.

Understanding Workers' Compensation Insurance Premiums: Who's Responsible?

You may want to see also

Explore related products

$14.99

![]()

Geographic Differences: Analyze how location affects rates, as state regulations and local economic conditions can influence pricing

Workers' compensation rates can vary significantly based on geographic location due to differing state regulations and local economic conditions. For instance, states with higher costs of living often have higher workers' compensation rates to reflect the increased expenses associated with medical care and lost wages. Conversely, states with lower costs of living may have lower rates. Additionally, states with more stringent workers' compensation laws may have higher rates to account for the increased likelihood of claims being filed and the higher costs associated with compliance.

The impact of local economic conditions on workers' compensation rates is also noteworthy. In areas with high unemployment rates, workers may be more likely to file claims, leading to higher rates. Similarly, in industries that are more prone to accidents and injuries, such as construction or manufacturing, workers' compensation rates may be higher to reflect the increased risk.

Insurance companies may also adjust their rates based on the specific location of the business. For example, a business located in a high-crime area may have higher workers' compensation rates due to the increased risk of workplace violence. Similarly, a business located in an area with a high incidence of natural disasters may have higher rates to account for the increased risk of property damage and business interruption.

To mitigate the impact of geographic differences on workers' compensation rates, businesses can take steps to improve workplace safety and reduce the likelihood of claims being filed. This may include implementing safety training programs, providing personal protective equipment, and maintaining a clean and well-organized work environment. Additionally, businesses can work with their insurance providers to develop customized policies that take into account the unique risks and challenges associated with their specific location and industry.

In conclusion, geographic differences can have a significant impact on workers' compensation rates, and businesses should be aware of these factors when selecting an insurance provider and developing their risk management strategies. By understanding the specific risks and challenges associated with their location and industry, businesses can take steps to reduce their workers' compensation costs and protect their employees.

Essential Guide to Workers' Compensation Insurance in Florida

You may want to see also

Explore related products

![]()

Company Size and Experience: Investigate how the size and experience of an insurance company can lead to variations in rates offered

The size and experience of an insurance company play a significant role in determining the workers' compensation rates they offer. Larger insurance companies, with more substantial financial reserves and a broader customer base, often have the flexibility to offer more competitive rates. This is because they can spread the risk across a larger pool of policyholders, reducing the impact of individual claims on their overall financial health.

In contrast, smaller insurance companies may have to charge higher rates to maintain profitability and ensure they have enough funds to cover potential claims. Their limited size means they have less room for error and must be more cautious in their underwriting practices. This can result in higher premiums for policyholders.

Experience also matters. Insurance companies with a long history of providing workers' compensation coverage are likely to have a better understanding of the risks involved and how to manage them effectively. They may have developed specialized expertise in certain industries or types of claims, allowing them to offer more tailored and cost-effective solutions.

On the other hand, newer insurance companies may still be learning the intricacies of workers' compensation and may not have the same level of expertise. This can lead to higher rates as they try to mitigate the risks they perceive.

It's important to note that while company size and experience can influence rates, they are not the only factors at play. Other considerations, such as the industry you operate in, your claims history, and the specific coverage options you choose, can also impact your workers' compensation premiums.

When shopping for workers' compensation insurance, it's essential to consider the size and experience of the insurance company, as well as other factors that may affect your rates. By doing your research and comparing quotes from multiple providers, you can find the best coverage options for your business at the most competitive prices.

Protecting Your Loved Ones: The Importance of Workman's Compensation Insurance for Family Members

You may want to see also

Explore related products

![Compensation (The Criterion Collection) [Blu-ray]](https://m.media-amazon.com/images/I/71yx5jd1XCL._AC_UL320_.jpg)

![]()

Claims History Impact: Examine the role of an employer's claims history in determining the rates they are offered by insurers

An employer's claims history plays a pivotal role in determining the workers' compensation insurance rates they are offered by insurers. This history serves as a critical indicator of the risk level associated with insuring a particular business. Employers with a history of frequent or severe claims are likely to be viewed as high-risk by insurance companies, which can result in higher premium rates. Conversely, businesses with a clean claims history or fewer incidents may benefit from lower rates, as they present a lower risk profile to insurers.

Insurance companies analyze claims history data to assess the likelihood of future claims and the potential costs associated with them. This analysis involves looking at the number of claims filed, the severity of the injuries, the duration of the claims, and the total payouts. Employers who have implemented effective safety measures and have a track record of preventing workplace injuries may be rewarded with more favorable rates. On the other hand, those who have not adequately addressed safety concerns or have a pattern of recurring incidents may face higher premiums.

The impact of claims history on insurance rates can vary depending on the industry and the specific risks associated with it. For example, businesses in high-risk industries such as construction or manufacturing may already face higher rates due to the nature of their work. However, even within these industries, employers with better claims histories can still secure more competitive rates compared to their peers with more frequent or severe claims.

To mitigate the impact of claims history on insurance rates, employers can take proactive steps to improve workplace safety and reduce the likelihood of accidents and injuries. This may include implementing safety training programs, conducting regular safety audits, investing in ergonomic equipment, and establishing clear safety protocols. By demonstrating a commitment to safety and reducing the number and severity of claims, employers can potentially lower their insurance costs over time.

In conclusion, an employer's claims history is a significant factor in determining their workers' compensation insurance rates. By understanding the role of claims history and taking steps to improve workplace safety, employers can potentially secure more favorable rates and reduce their overall insurance costs.

Understanding Workman's Comp Insurance: A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, workers' compensation rates can vary significantly by insurance company. Each insurer assesses risk differently and may offer different premium rates based on factors such as the industry, company size, claims history, and geographic location.

Several factors influence the variation in workers' compensation rates among insurance companies, including the industry's risk profile, the company's claims history, the geographic location where the business operates, and the size of the company. Insurers may also consider the effectiveness of the company's safety programs and the nature of the work performed by employees.

Businesses can compare workers' compensation rates from different insurance companies by obtaining quotes from multiple insurers, reviewing the premium rates and coverage terms, and considering the insurer's reputation and financial stability. It's also important to compare the level of customer service and the claims handling process.

Yes, there are regulatory bodies that oversee workers' compensation rates to ensure fairness. These bodies vary by jurisdiction but typically include state insurance departments or workers' compensation boards. They set guidelines for rate-making and ensure that insurers comply with these guidelines to protect both employers and employees.