FICA, which stands for Federal Insurance Contributions Act, is a U.S. federal payroll tax that funds Social Security and Medicare. It's typically withheld from employees' wages and matched by employers. However, when it comes to deferred compensation, the rules can be a bit more complex. Deferred compensation refers to earnings that are not paid out immediately but are instead postponed to a later date, often as part of a retirement plan or incentive program. The question of whether FICA taxes apply to deferred compensation depends on various factors, including the type of plan, the timing of the payments, and the specific provisions of the tax code. In general, FICA taxes are due on deferred compensation when it is earned, even if the payment is delayed. This means that both employees and employers may need to pay their respective FICA taxes on the deferred amount at the time it is accrued, rather than when it is actually paid out. However, there are certain exceptions and nuances to this rule, and it's important to consult with a tax professional or financial advisor to understand the specific implications for your situation.

Explore related products

$15.99 $19.95

What You'll Learn

- FICA Basics: Understanding what FICA is and how it's applied to different types of income

- Deferred Compensation: Defining what constitutes deferred compensation and its common forms

- Tax Implications: Exploring whether and how FICA taxes are applied to deferred compensation

- Exceptions and Rules: Discussing any specific exceptions or rules that might apply to certain situations

- Planning Strategies: Offering strategies for minimizing FICA taxes on deferred compensation

![]()

FICA Basics: Understanding what FICA is and how it's applied to different types of income

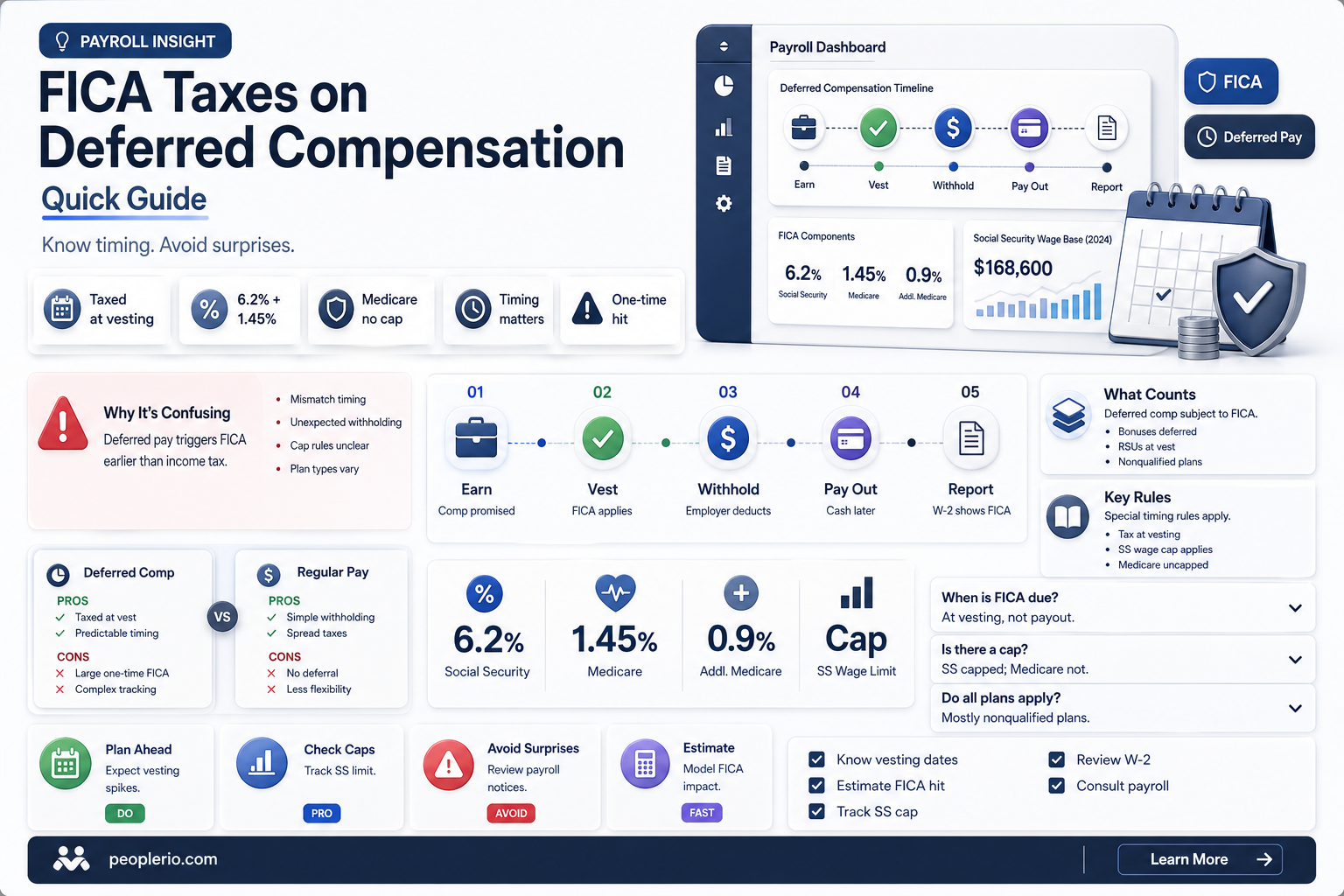

FICA, which stands for Federal Insurance Contributions Act, is a U.S. federal payroll tax that funds Social Security and Medicare. It's applied to various types of income, including wages, salaries, and tips. Employers and employees each pay a portion of FICA taxes, with the current tax rates being 6.2% for Social Security and 1.45% for Medicare.

When it comes to deferred compensation, FICA taxes are typically paid when the income is earned, not when it's received. This means that if an employee defers part of their salary to a later date, FICA taxes will still be applied to that income at the time it's earned, even though the employee won't receive the money until later.

However, there are some exceptions to this rule. For example, if an employee defers compensation under a nonqualified deferred compensation plan, FICA taxes may not be applied until the income is actually received. This is because nonqualified deferred compensation plans are not subject to the same FICA tax rules as qualified plans, such as 401(k)s or IRAs.

It's important to note that FICA taxes are separate from income taxes, and the two are calculated differently. While FICA taxes are applied to gross income, income taxes are applied to adjusted gross income, which takes into account deductions and exemptions.

In summary, FICA taxes are applied to various types of income, including deferred compensation, and are typically paid when the income is earned. However, there are some exceptions to this rule, such as nonqualified deferred compensation plans. Understanding how FICA taxes work can help individuals make informed decisions about their finances and plan for their future.

Can VA Benefits Cover Auto Accident Injuries? What Veterans Need to Know

You may want to see also

Explore related products

![]()

Deferred Compensation: Defining what constitutes deferred compensation and its common forms

Deferred compensation refers to any payment made to an employee after they have retired or left the company, typically as a reward for their service or performance. This type of compensation can take many forms, including pensions, annuities, stock options, and bonuses. One common form of deferred compensation is a 401(k) plan, which allows employees to save a portion of their salary for retirement. Another form is a deferred bonus plan, which pays out a bonus to employees at a later date, often tied to specific performance metrics.

When it comes to FICA (Federal Insurance Contributions Act) taxes, which fund Social Security and Medicare, the question of whether or not deferred compensation is taxable can be complex. Generally, FICA taxes are withheld from an employee's wages when they are earned, not when they are paid out. However, there are some exceptions to this rule. For example, if an employee receives a bonus that is tied to their performance in a given year, but it is paid out in the following year, the bonus may still be subject to FICA taxes in the year it is earned.

In the case of deferred compensation, such as a pension or annuity, FICA taxes are typically not withheld until the payments are actually made to the employee. This is because the payments are not considered wages until they are received. However, it is important to note that there may be other tax implications associated with deferred compensation, such as income tax withholding and reporting requirements.

Employers who offer deferred compensation plans should carefully consider the tax implications and ensure that they are complying with all applicable laws and regulations. This may involve consulting with a tax professional or financial advisor to determine the best way to structure their deferred compensation plans.

In conclusion, deferred compensation can be a valuable tool for employers to attract and retain top talent, but it is important to understand the tax implications associated with these plans. By carefully considering the different forms of deferred compensation and their tax treatment, employers can ensure that they are providing their employees with a competitive benefits package while also complying with all applicable laws and regulations.

Ohio Churches and Workers' Compensation: What You Need to Know

You may want to see also

Explore related products

![]()

Tax Implications: Exploring whether and how FICA taxes are applied to deferred compensation

Deferred compensation plans are a popular tool for employers to attract and retain top talent, offering employees the opportunity to defer a portion of their income until a later date, typically retirement. However, the tax implications of these plans can be complex, particularly when it comes to FICA (Federal Insurance Contributions Act) taxes. FICA taxes, which fund Social Security and Medicare, are typically withheld from an employee's wages and paid by both the employee and the employer. But what happens when compensation is deferred?

In general, FICA taxes are applied to deferred compensation at the time the compensation is earned, not when it is paid out. This means that if an employee defers a portion of their salary, FICA taxes will be withheld and paid on that amount in the year it is earned, even though the employee may not receive the funds until years later. This can have significant implications for both employees and employers, as it may result in higher tax liabilities in the short term.

There are some exceptions to this rule, however. For example, certain types of deferred compensation plans, such as those that qualify under Section 409A of the Internal Revenue Code, may allow for the deferral of FICA taxes until the compensation is actually paid out. This can provide a significant tax advantage for employees, as it allows them to delay paying taxes on their deferred income until they are in a lower tax bracket, such as during retirement.

Employers also need to be aware of their FICA tax obligations when it comes to deferred compensation. In addition to withholding and paying FICA taxes on deferred compensation, employers may also be required to pay FICA taxes on any earnings that are attributable to deferred compensation, such as interest or investment returns. This can add to the overall tax burden for employers, particularly if they have a large number of employees participating in deferred compensation plans.

In conclusion, while deferred compensation plans can offer significant benefits for both employees and employers, it is important to carefully consider the tax implications, particularly when it comes to FICA taxes. Understanding how and when FICA taxes are applied to deferred compensation can help individuals and businesses make informed decisions about these plans and avoid unexpected tax liabilities.

Understanding VA Compensation: Your Guide to Retroactive Pay

You may want to see also

![]()

Exceptions and Rules: Discussing any specific exceptions or rules that might apply to certain situations

While the general rule is that FICA taxes are paid on deferred compensation, there are specific exceptions and rules that apply to certain situations. One such exception is for certain types of deferred compensation plans, such as 401(k) plans, which are exempt from FICA taxes until the funds are withdrawn. This is because these plans are designed to encourage retirement savings and are therefore given preferential tax treatment.

Another exception is for deferred compensation that is paid out as a result of a disability. In this case, the FICA taxes may be waived if the disability is considered permanent and total. This is to provide financial relief to individuals who are unable to work due to a disability and may be relying on deferred compensation as a source of income.

Additionally, there are rules that apply to the timing of FICA tax payments on deferred compensation. For example, if an employee receives a lump sum payment of deferred compensation, the FICA taxes must be paid at the time of the payment. However, if the deferred compensation is paid out in installments, the FICA taxes may be paid over time as the installments are received.

It's also important to note that the rules surrounding FICA taxes on deferred compensation can be complex and may vary depending on the specific situation. For example, the tax treatment of deferred compensation may be different for government employees or for employees of certain types of organizations. Therefore, it's essential to consult with a tax professional or financial advisor to understand the specific rules and exceptions that apply to your situation.

In conclusion, while the general rule is that FICA taxes are paid on deferred compensation, there are specific exceptions and rules that apply to certain situations. These exceptions and rules can provide relief or preferential tax treatment in certain circumstances, but it's important to understand the complexities and consult with a professional to ensure compliance with the law.

Are Workers' Compensation Payments Taxable? What You Need to Know

You may want to see also

![]()

Planning Strategies: Offering strategies for minimizing FICA taxes on deferred compensation

One effective strategy for minimizing FICA taxes on deferred compensation is to carefully time the recognition of income. Since FICA taxes are levied on earned income, deferring the recognition of compensation until a later date can reduce the immediate tax burden. For example, an individual could negotiate a deferred compensation package that pays out over several years, rather than receiving a lump sum upfront. This approach spreads the income recognition over time, potentially reducing the overall FICA tax liability.

Another strategy is to utilize tax-advantaged accounts, such as 401(k) or IRA plans, to defer compensation. By contributing to these accounts, individuals can reduce their taxable income in the current year, thereby lowering their FICA tax liability. Additionally, earnings within these accounts grow tax-deferred, further minimizing the impact of FICA taxes. It's important to note, however, that there are contribution limits to these accounts, and individuals should consult with a financial advisor to determine the optimal contribution strategy.

Individuals can also consider structuring their deferred compensation as equity-based incentives, such as stock options or restricted stock units (RSUs). These types of compensation are not subject to FICA taxes until they are exercised or vested, respectively. By choosing equity-based incentives, individuals can delay the recognition of income and reduce their FICA tax liability in the short term. However, it's crucial to understand the tax implications of these incentives upon exercise or vesting, as they may be subject to other forms of taxation.

In some cases, individuals may be able to negotiate a deferred compensation package that includes a mix of cash and non-cash benefits. By allocating a portion of the compensation to non-cash benefits, such as health insurance or tuition reimbursement, individuals can reduce their taxable income and, consequently, their FICA tax liability. This strategy requires careful planning and negotiation, as the non-cash benefits must be valued and reported correctly to avoid any potential tax issues.

Finally, individuals should consider the impact of FICA tax rates on their deferred compensation planning. FICA tax rates are subject to change, and individuals should stay informed about any potential rate increases or decreases. By understanding the current and projected FICA tax rates, individuals can make more informed decisions about their deferred compensation strategies and optimize their tax planning accordingly.

Impact of Additional Drills on VA Compensation: A Detailed Analysis

You may want to see also

Frequently asked questions

FICA stands for Federal Insurance Contributions Act. It's a U.S. federal payroll tax that funds Social Security and Medicare. Deferred compensation is a portion of an employee's salary or wages that is paid out at a later date, often after retirement. The question of whether FICA is paid on deferred compensation is important because it affects both the employer's and employee's tax liabilities.

Generally, yes, FICA taxes are due on deferred compensation. According to the IRS, deferred compensation is subject to FICA taxes when it is earned, not when it is paid out. This means that both the employer and employee portions of FICA taxes should be withheld and paid when the compensation is deferred, rather than when it is eventually distributed.

There are some exceptions and special rules. For example, certain types of deferred compensation plans, like 401(k) plans, are exempt from FICA taxes. Additionally, if deferred compensation is paid out in a lump sum after retirement, it may be subject to a different tax rate than regular income. It's important to consult with a tax professional or the IRS for specific guidance on deferred compensation and FICA taxes.