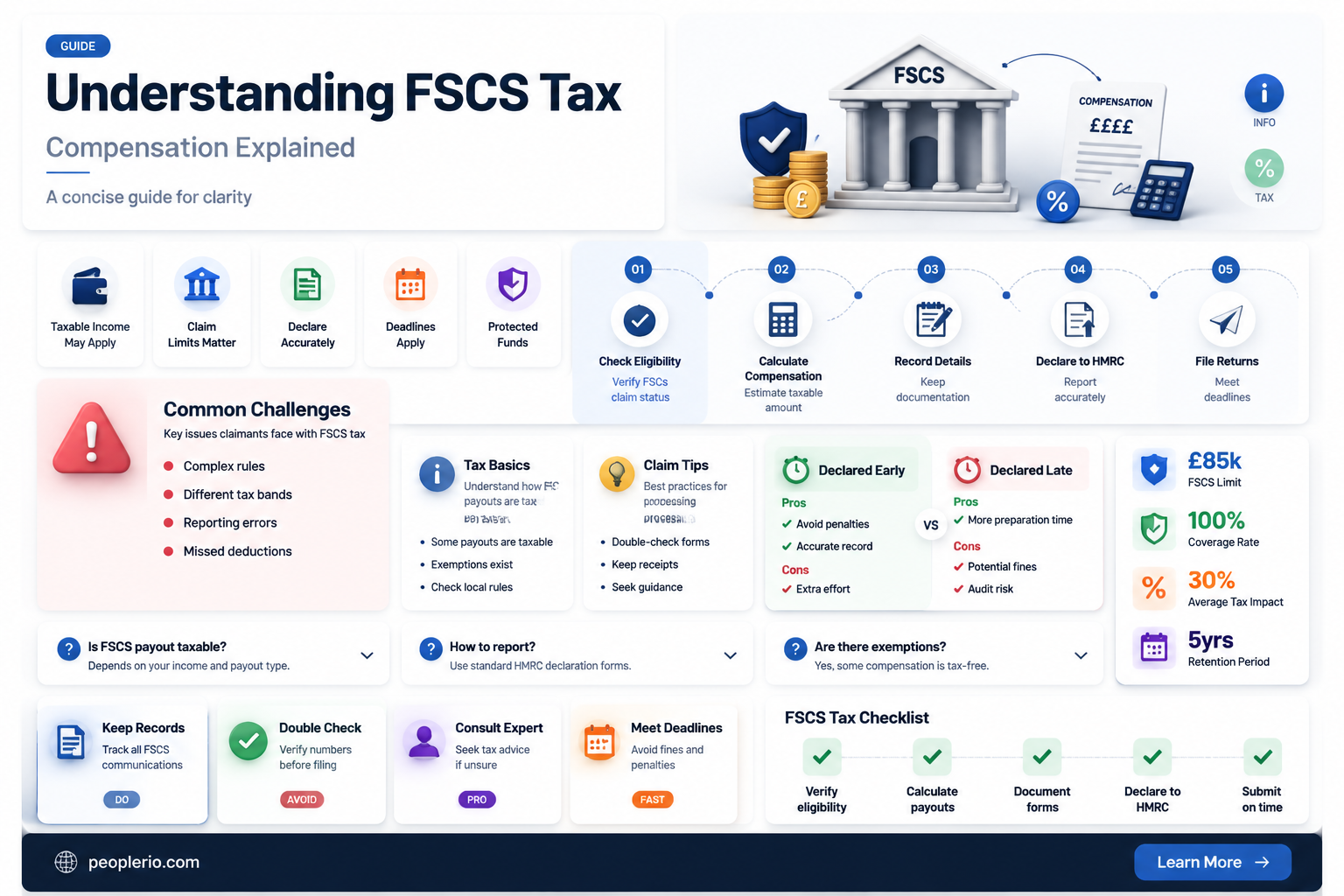

The question of whether you pay tax on Financial Services Compensation Scheme (FSCS) compensation is a common concern for individuals who have received payments from this UK-based scheme. The FSCS is designed to protect consumers when financial firms fail, providing compensation for losses up to certain limits. When it comes to taxation, the treatment of FSCS compensation can be complex and depends on various factors, including the nature of the claim and the tax laws in place at the time of receipt. Generally, compensation for loss of investments or savings may be subject to tax, while payments for losses related to certain types of insurance might be tax-free. It is essential for recipients of FSCS compensation to consult with a tax professional to understand their specific tax obligations and ensure compliance with HM Revenue & Customs (HMRC) regulations.

Explore related products

What You'll Learn

![]()

What is FSCS Compensation?

The Financial Services Compensation Scheme (FSCS) is a UK-based organization that provides compensation to consumers who have suffered financial loss due to the failure of a financial services firm. FSCS compensation is designed to protect consumers and maintain confidence in the financial services industry. It covers a wide range of financial products and services, including investments, insurance, and banking.

FSCS compensation is funded by a levy on financial services firms, which is based on their size and the type of services they provide. This means that consumers do not have to pay for the compensation themselves. The FSCS has a limit on the amount of compensation it can provide, which is currently set at £85,000 per person, per firm.

One of the key aspects of FSCS compensation is that it is not taxable. This means that consumers who receive compensation from the FSCS do not have to pay any tax on the amount they receive. This is an important consideration for consumers who are facing financial difficulties due to the failure of a financial services firm.

In order to be eligible for FSCS compensation, consumers must meet certain criteria. For example, they must have been a customer of the failed firm and must have suffered a financial loss as a result of the firm's failure. The FSCS also has a number of exclusions, which means that certain types of losses are not covered. For example, the FSCS does not cover losses that are a result of fraud or negligence on the part of the consumer.

The process of claiming FSCS compensation can be complex and time-consuming. Consumers must first contact the FSCS and provide them with details of their claim. The FSCS will then investigate the claim and make a decision on whether or not to provide compensation. If compensation is awarded, it will be paid directly to the consumer.

Overall, FSCS compensation is an important safety net for consumers who have suffered financial loss due to the failure of a financial services firm. It provides a way for consumers to recover their losses and move forward with their financial lives.

Understanding Taxation on Compensation in Ireland: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Tax Implications of FSCS Payments

The Financial Services Compensation Scheme (FSCS) provides a vital safety net for consumers who have suffered financial losses due to the failure of a financial services firm. However, when it comes to tax implications, the waters can become murky. In this section, we'll delve into the specific tax considerations that arise from FSCS payments, helping you understand what you need to know.

Firstly, it's essential to recognize that FSCS payments are generally considered taxable income. This means that any compensation you receive from the scheme will need to be declared on your tax return. The FSCS itself will typically deduct tax at source, but it's still your responsibility to ensure that you've paid the correct amount of tax on your compensation.

One key consideration is the timing of the payment. If you receive a lump sum payment from the FSCS, you'll need to declare this on your tax return for the year in which you received the payment. However, if you receive payments in installments, you'll need to declare each installment on your tax return for the year in which it was received. This can have implications for your tax bracket and the amount of tax you owe.

Another important factor to consider is the type of loss that the FSCS payment is compensating for. If the payment is for a loss of capital, such as the loss of an investment, then it may be possible to offset this loss against other capital gains or losses you've experienced in the same tax year. This could potentially reduce your overall tax liability.

It's also worth noting that FSCS payments may be subject to National Insurance contributions. If you're in receipt of certain benefits, such as Income Support or Pension Credit, you may be able to claim back some of the National Insurance contributions you've paid on your FSCS payment.

In conclusion, while FSCS payments provide essential compensation for those who have suffered financial losses, it's crucial to understand the tax implications of these payments. By declaring your compensation on your tax return, considering the timing and type of payment, and exploring potential offsets and benefits, you can ensure that you're meeting your tax obligations while also maximizing your compensation.

Understanding Tax Implications on Initial Workers' Compensation Benefits

You may want to see also

Explore related products

![]()

Types of Compensation Covered

The Financial Conduct Authority (FCA) in the UK operates the Financial Services Compensation Scheme (FSCS), which serves as a safety net for consumers when financial firms fail. The FSCS covers various types of compensation, primarily focusing on claims related to investments, savings, pensions, and insurance products. It's essential to understand that not all types of financial losses are covered by the FSCS, and the scheme has specific eligibility criteria and compensation limits.

One of the key types of compensation covered by the FSCS is for investments. This includes claims related to the purchase of stocks, bonds, mutual funds, and other investment products. If an investment firm fails and the consumer suffers a loss, the FSCS may provide compensation up to a certain limit, currently set at £85,000 per person per firm. It's important to note that the FSCS does not cover losses due to market fluctuations or poor investment decisions, only losses resulting from the failure of the financial firm.

Another significant area covered by the FSCS is pensions. This includes claims related to pension schemes, such as defined contribution and defined benefit plans. If a pension provider fails, the FSCS may provide compensation to help restore the pension benefits lost. The compensation limits for pensions are complex and depend on various factors, including the type of pension scheme and the age of the claimant.

Savings accounts are also protected under the FSCS. If a bank or building society fails, the FSCS will cover losses up to £85,000 per person per firm. This protection applies to individual savings accounts, joint accounts, and certain types of business accounts. However, it's crucial to understand that the FSCS does not cover losses due to fraud or other criminal activities.

Insurance products are another category covered by the FSCS. This includes claims related to life insurance, general insurance, and long-term care insurance. If an insurance company fails and the consumer suffers a loss, the FSCS may provide compensation up to the policy limits. It's important to note that the FSCS does not cover losses due to the non-disclosure of material facts or other breaches of the insurance contract.

In conclusion, the FSCS provides vital protection for consumers in the event of financial firm failures. However, it's essential to understand the types of compensation covered and the specific eligibility criteria and compensation limits that apply. By being aware of these details, consumers can better navigate the complexities of the FSCS and ensure they receive the appropriate level of protection.

Understanding Reasonable Compensation Requirements for C Corporations

You may want to see also

Explore related products

![]()

How to Report FSCS Compensation

To report FSCS (Financial Services Compensation Scheme) compensation, you must follow a specific process to ensure compliance with tax regulations. The first step is to obtain the necessary documentation from the FSCS, which will include a detailed breakdown of the compensation awarded to you. This documentation is crucial as it will serve as evidence of your claim when reporting the compensation to HMRC (Her Majesty's Revenue and Customs).

Once you have received the documentation, you will need to determine the tax year in which the compensation was awarded. This is important because the tax treatment of FSCS compensation can vary depending on the tax year. For example, compensation awarded in the 2023/24 tax year may be subject to different tax rules than compensation awarded in the 2022/23 tax year.

After determining the tax year, you will need to complete the appropriate tax return form. If you are an individual, you will typically need to complete the SA1000 form, which is the standard self-assessment tax return form. If you are a company, you will need to complete the CT600 form, which is the corporation tax return form. In either case, you will need to include the FSCS compensation in the appropriate section of the form.

When completing the tax return form, it is important to ensure that you accurately report the amount of FSCS compensation awarded to you. Failure to do so could result in penalties and interest charges from HMRC. Additionally, you should keep a copy of the FSCS documentation for your records, as you may need to refer to it in the future if HMRC queries your tax return.

Finally, it is worth noting that FSCS compensation is generally considered to be taxable income. This means that you will need to pay tax on the compensation awarded to you, unless there are specific circumstances that apply. For example, if the compensation is awarded for personal injury or distress, it may be exempt from tax. However, it is important to seek professional tax advice if you are unsure about the tax treatment of your FSCS compensation.

Understanding State Taxes on Deferred Compensation: A Guide

You may want to see also

Explore related products

![]()

Seeking Professional Tax Advice

Navigating the complexities of tax law, especially when it pertains to compensation from the Financial Services Compensation Scheme (FSCS), can be challenging. Seeking professional tax advice is often necessary to ensure that you comply with all relevant tax regulations and make the most of any available tax reliefs or exemptions. Tax advisors can provide tailored guidance based on your individual circumstances, helping you to understand your tax obligations and plan accordingly.

One of the key benefits of seeking professional tax advice is the ability to access expert knowledge and experience. Tax laws and regulations are constantly evolving, and a qualified tax advisor will be up-to-date with the latest changes and how they may impact your situation. They can also help you to identify potential tax-saving opportunities, such as claiming allowable expenses or utilizing tax-efficient investment strategies.

When seeking tax advice, it is important to choose a reputable and qualified professional. Look for advisors who are registered with a recognized professional body, such as the Institute of Chartered Accountants in England and Wales (ICAEW) or the Chartered Institute of Taxation (CIOT). These organizations have strict standards for their members, ensuring that they are competent and ethical in their practice.

During your initial consultation with a tax advisor, be prepared to provide detailed information about your financial situation, including your income, expenses, and any relevant documentation. This will enable the advisor to give you accurate and personalized advice. They may also ask you about your financial goals and objectives, as this can help them to develop a tax strategy that aligns with your overall financial plan.

In conclusion, seeking professional tax advice when dealing with FSCS compensation can provide you with the confidence and clarity you need to manage your tax affairs effectively. By working with a qualified tax advisor, you can ensure that you are fully compliant with tax regulations and make the most of any available tax reliefs or exemptions. This can ultimately save you time, stress, and potentially even money in the long run.

Funding the Fight: Who's Covering the Costs of COVID Vaccines?

You may want to see also

Frequently asked questions

Generally, compensation received from the FSCS is tax-free. This is because the FSCS is designed to protect consumers when financial firms fail, and the compensation is intended to restore losses without creating additional financial burdens.

Yes, there are some exceptions. For instance, if the compensation includes interest, that portion may be taxable. Additionally, if you receive compensation for a claim that was previously deducted as a loss on your tax return, you might need to report the compensation as income.

Typically, you do not need to report FSCS compensation on your tax return as it is not considered taxable income. However, it's always a good idea to consult with a tax professional to ensure that your specific situation is handled correctly.

If you're unsure about the tax implications of your FSCS compensation, it's recommended to seek advice from a qualified tax advisor or accountant. They can provide personalized guidance based on your individual circumstances and help you comply with tax regulations.