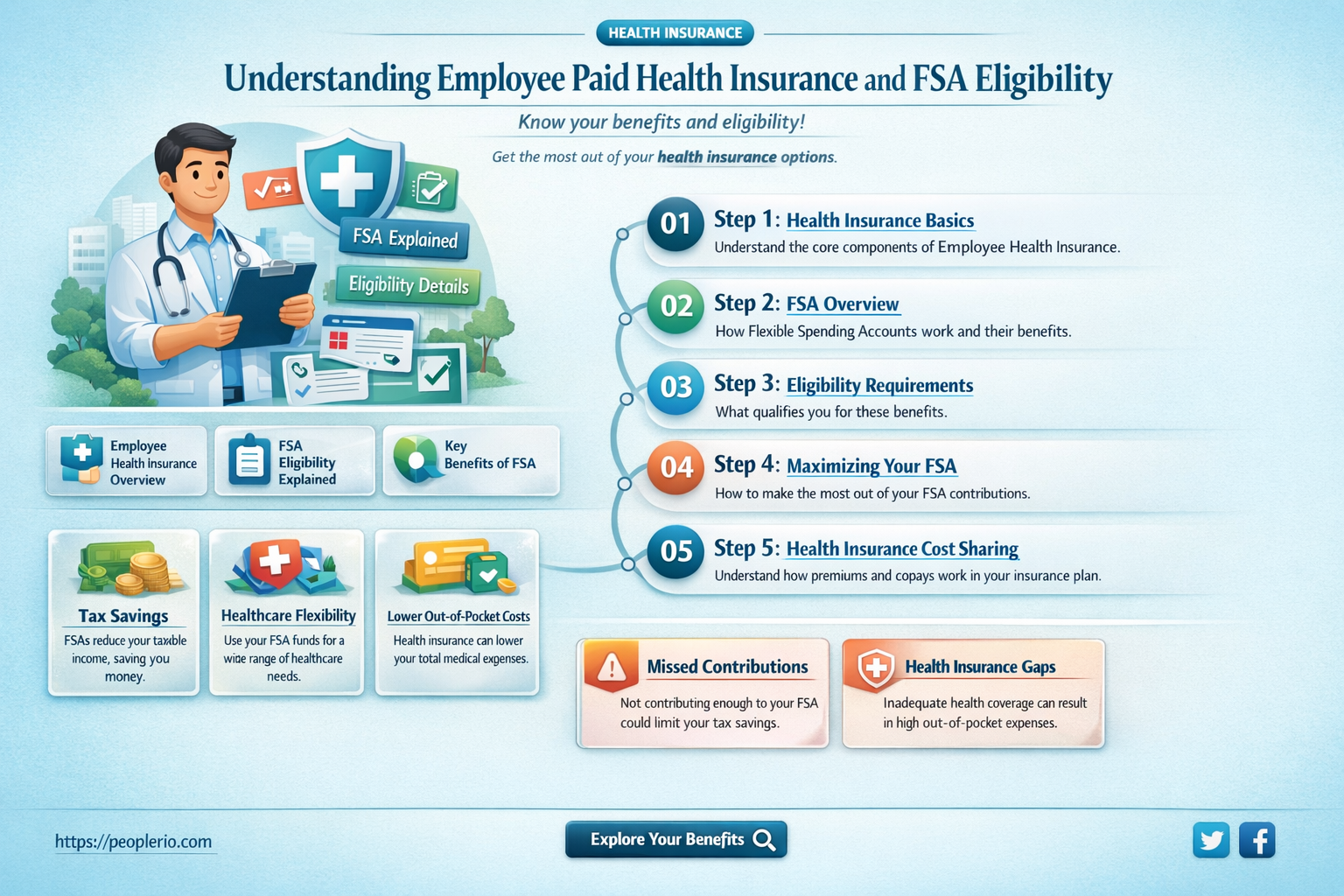

To introduce the topic 'does an employee paid health insurance qualify for 125', you could start with:

When it comes to employee benefits, understanding the nuances of health insurance and its implications on tax savings can be crucial. One common question that arises is whether employee-paid health insurance premiums qualify for tax advantages under Section 125 of the Internal Revenue Code. This section allows for the exclusion of certain benefits provided by employers from an employee's gross income, potentially leading to significant tax savings. To delve into this topic, it's essential to explore the specifics of Section 125, the conditions under which employee-paid health insurance might qualify, and the potential benefits for both employees and employers.

| Characteristics | Values |

|---|---|

| Employee Paid Health Insurance | Qualify for 125 |

Explore related products

$17.75

$23.7 $23.99

What You'll Learn

- Eligibility Criteria: Understand the conditions an employee must meet to qualify for a 125 plan

- Types of Expenses Covered: Learn about the health-related expenses that can be reimbursed under a 125 plan

- Contribution Limits: Discover the maximum amount an employee can contribute to their 125 plan annually

- Tax Implications: Explore how contributions and reimbursements from a 125 plan affect an employee's taxes

- Enrollment and Administration: Find out the steps to enroll in a 125 plan and how it is managed

![]()

Eligibility Criteria: Understand the conditions an employee must meet to qualify for a 125 plan

To qualify for a 125 plan, an employee must meet specific eligibility criteria set by the employer and the plan's guidelines. These criteria typically include being a full-time employee, as part-time or seasonal workers may not be eligible. The employee must also be enrolled in a health insurance plan that is compatible with the 125 plan. This means that if an employee is already receiving health insurance benefits from their employer, they may not be able to enroll in a 125 plan.

Another important criterion is the employee's income level. Some 125 plans have income limits, and employees who earn above a certain threshold may not be eligible. This is because 125 plans are designed to help employees with lower incomes afford health care expenses. Additionally, the employee must be able to demonstrate that they have a need for the plan, which may involve providing proof of health care expenses or a health condition.

The employee's age may also be a factor in determining eligibility. Some 125 plans have age limits, and employees who are above or below a certain age may not be eligible. This is because the plan's benefits may be more valuable to employees who are in a certain stage of life, such as those with young children or those who are nearing retirement.

Finally, the employee must be able to meet any additional requirements set by the employer or the plan's guidelines. This may include completing a health risk assessment, attending a health education seminar, or agreeing to participate in a wellness program. By meeting these eligibility criteria, an employee can qualify for a 125 plan and begin to take advantage of its benefits.

CVS Health Employees: Are They Healthcare Workers?

You may want to see also

Explore related products

![]()

Types of Expenses Covered: Learn about the health-related expenses that can be reimbursed under a 125 plan

A 125 plan, also known as a flexible spending account (FSA), is a tax-advantaged account that allows employees to set aside pre-tax dollars to pay for qualified health-related expenses. These plans are designed to help employees save money on healthcare costs by reducing their taxable income. But what exactly are the types of expenses that can be reimbursed under a 125 plan?

Qualified health-related expenses under a 125 plan typically include medical expenses such as doctor visits, hospital stays, and prescription medications. However, they can also cover a wide range of other health-related costs that are not typically covered by traditional health insurance plans. For example, a 125 plan may reimburse expenses for dental care, vision care, and even certain types of alternative medicine.

One important thing to note is that the expenses must be incurred during the plan year in order to be eligible for reimbursement. Additionally, the expenses must be for the employee, their spouse, or their dependents. The plan may also have specific rules and limitations on certain types of expenses, so it's important to review the plan details carefully.

Another unique aspect of 125 plans is that they often have a "use-it-or-lose-it" provision, which means that any unused funds at the end of the plan year are forfeited. This is in contrast to health savings accounts (HSAs), which allow unused funds to roll over from year to year. However, some 125 plans may offer a grace period or a carryover option, so it's important to check with the plan administrator.

In conclusion, a 125 plan can be a valuable tool for employees looking to save money on healthcare costs. By understanding the types of expenses that can be reimbursed under the plan, employees can make the most of this tax-advantaged benefit and reduce their overall healthcare expenses.

Exploring Employee Assistance Programs in Health Insurance Plans

You may want to see also

Explore related products

![]()

Contribution Limits: Discover the maximum amount an employee can contribute to their 125 plan annually

The maximum amount an employee can contribute to their 125 plan annually is a critical aspect of understanding these tax-advantaged accounts. As of 2023, the IRS allows employees to contribute up to $5,000 per year to their 125 plan, also known as a flexible spending account (FSA). This limit applies to each individual employee, meaning that if both spouses are employed and each has access to a 125 plan, they can each contribute up to $5,000, for a total of $10,000 per year for the household.

It's important to note that this contribution limit is subject to change due to inflation and other economic factors. The IRS typically announces any adjustments to the limit in the fall of each year, effective for the following calendar year. Employers may also impose their own contribution limits, which cannot exceed the IRS maximum.

When considering the contribution limit, it's essential to understand how the 125 plan works. These plans allow employees to set aside pre-tax dollars to pay for qualified medical expenses, such as deductibles, copayments, and prescription drugs. The money contributed to the plan is not subject to federal income tax, Social Security tax, or Medicare tax, which can result in significant savings for employees.

One strategy for maximizing the benefit of a 125 plan is to contribute the full amount allowed by the IRS each year. This can be done through payroll deductions, and many employers offer automatic enrollment and contribution options. Employees should carefully consider their expected medical expenses for the year when deciding how much to contribute, as any unused funds at the end of the year are typically forfeited.

In conclusion, understanding the contribution limits for a 125 plan is crucial for employees looking to make the most of these tax-saving accounts. By contributing the maximum amount allowed, employees can potentially save hundreds or even thousands of dollars on their medical expenses each year.

Maximizing Tax Benefits: The Scoop on Deducting Employee Health Insurance Premiums

You may want to see also

Explore related products

![]()

Tax Implications: Explore how contributions and reimbursements from a 125 plan affect an employee's taxes

Contributions to a 125 plan, also known as a flexible spending account (FSA), are made on a pre-tax basis, which means they are deducted from an employee's gross income before taxes are calculated. This can result in significant tax savings, as the money is not subject to federal, state, or local income taxes. For example, if an employee contributes $2,000 to their 125 plan, their taxable income would be reduced by $2,000, potentially saving them hundreds of dollars in taxes, depending on their tax bracket.

Reimbursements from a 125 plan are also tax-free, as long as they are used for qualified medical expenses. This means that employees can use the funds in their 125 plan to pay for deductibles, copays, prescription medications, and other eligible healthcare costs without incurring any additional tax liability. However, it's important to note that reimbursements for non-qualified expenses may be subject to taxation and could also result in a penalty.

One of the key benefits of a 125 plan is that it allows employees to set aside a specific amount of money each year for healthcare expenses, which can help them budget for out-of-pocket costs and avoid unexpected financial burdens. Additionally, because the contributions are made on a pre-tax basis, employees can potentially save more money than they would by simply setting aside the same amount in a taxable savings account.

To maximize the tax benefits of a 125 plan, employees should carefully estimate their annual healthcare expenses and contribute accordingly. Overestimating can lead to unused funds that may be forfeited at the end of the plan year, while underestimating can result in additional out-of-pocket costs. Employees should also keep track of their qualified medical expenses throughout the year and submit reimbursement requests promptly to ensure they take full advantage of the tax-free benefits.

In conclusion, a 125 plan can provide significant tax savings for employees who use it effectively. By contributing on a pre-tax basis and using the funds for qualified medical expenses, employees can reduce their taxable income, avoid additional tax liability, and better manage their healthcare costs.

Understanding FICA: Are Employee Health Deductions Subject to Tax?

You may want to see also

Explore related products

![]()

Enrollment and Administration: Find out the steps to enroll in a 125 plan and how it is managed

To enroll in a 125 plan, an employee must first determine if their employer offers such a plan. If available, the employee should contact their human resources department to obtain the necessary enrollment forms and information. These forms typically require the employee to provide personal information, such as their name, address, and social security number, as well as details about their health insurance coverage.

Once the enrollment forms are completed, the employee should submit them to their employer's designated 125 plan administrator. This administrator is responsible for managing the plan and ensuring that all enrollments are processed correctly. The employee should also be aware of any deadlines for enrollment, as missing these deadlines may result in a delay or denial of coverage.

After submitting the enrollment forms, the employee should receive a confirmation of their enrollment from the 125 plan administrator. This confirmation should include details about the employee's coverage, such as the effective date, the amount of their flexible spending account (FSA) or health savings account (HSA), and any other relevant information.

In terms of administration, the 125 plan is typically managed by the employer's human resources department or a third-party administrator. This administrator is responsible for ensuring that the plan complies with all applicable laws and regulations, as well as for processing claims and reimbursements. The employee should be aware of the administrator's contact information and procedures for submitting claims and requesting reimbursements.

Overall, enrolling in a 125 plan involves a series of steps that require the employee to gather information, complete forms, and submit them to the appropriate administrator. By following these steps and understanding the administration of the plan, employees can take advantage of the tax savings and other benefits offered by 125 plans.

Understanding FICA: Are Employee Health Insurance Contributions Subject to FICA?

You may want to see also

Frequently asked questions

Yes, an employee-paid health insurance plan can qualify for a Section 125 plan if it meets the IRS requirements.

A Section 125 plan, also known as a cafeteria plan, is a type of employee benefit plan that allows employees to choose from a variety of benefits and pay for them with pre-tax dollars.

The IRS requires that the health insurance plan be a qualified health plan, which means it must provide minimum essential coverage and meet certain actuarial standards.

A Section 125 plan can provide employees with tax savings, as they can pay for their health insurance premiums with pre-tax dollars. This can reduce their taxable income and lower their tax liability.

A Section 125 plan works by allowing employees to elect to have a portion of their salary withheld and used to pay for their health insurance premiums. The withheld amount is not subject to federal income tax, which can provide employees with tax savings.

![RENPHO Active Thermacool 2 Massage Gun with Heat and Cold, [2026 Upgraded] Percussion Deep Tissue Handheld Neck Massager, FSA Approved, Muscle Masajeador for Men Women Athletes HSA](https://m.media-amazon.com/images/I/61mtD8h+HyL._AC_UL320_.jpg)